Passenger Car Bushing Market Size, Share & Industry Analysis by Application (Suspension, Engine, Chassis, Interior, Exhaust, and Transmission), By Material (Rubber, Polyurethane, Brass, Aluminum, Bronze, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

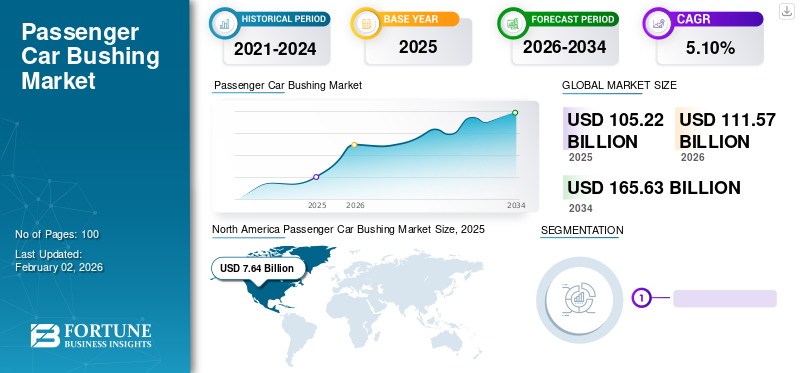

The global passenger car bushing market size was valued at USD 105.22 billion in 2025. The market is projected to grow from USD 111.57 billion in 2026 to USD 165.63 billion by 2034, exhibiting a CAGR of 5.10% during the forecast period.

The market plays a crucial role in the broader automotive components industry driven by the continuous demand for smoother ride quality, noise reduction, and enhanced vehicle performance and comfort along with stability. Passenger car bushings, typically made from rubber, polyurethane, or composite materials, are used in various parts of a car including the suspension system, control arms, engine mounts, and steering components. As vehicles become more performance- and comfort-focused, the demand for durable and high-performance bushing materials is increasing. The rise of electric vehicles (EVs) and hybrid cars also contributes to the market’s evolution, as these vehicles require bushings capable of handling different weight distributions and vibration.

The market includes a mix of global manufacturers and regional suppliers. Notable players include Continental AG, ZF Friedrichshafen AG, Tenneco Inc., Sumitomo Riko, and Vibracoustic, all of which offer a range of automotive bushing solutions. These companies focus on innovation in material science and product design, aiming to improve durability, reduce noise, vibration, and harshness (NVH) and meet the evolving demands of modern passenger vehicles.

Download Free sample to learn more about this report.

PASSENGER CAR BUSHING MARKET TRENDS

Shift toward High-Performance Synthetic Materials in Bushings is a Prominent Market Trend

One of the most significant trends in the market is the growing use of high-performance synthetic materials, such as polyurethane, thermoplastic elastomers (TPE), and advanced composites, in place of traditional natural or synthetic rubber. This shift is primarily driven by the limitations of rubber under extreme operating conditions, including exposure to heat, oil, road salts, and mechanical stress, which can lead to premature wear, cracking, and deformation.

Polyurethane passenger car bushings, for example, are known for their excellent resistance to abrasion, chemicals, and aging. They also offer superior load-bearing capacity and retain their shape better under pressure. These properties make them particularly attractive for both OEMs and the automotive aftermarket, especially in applications requiring improved performance.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Ride Comfort and Noise Reduction to Push Market Expansion

One of the primary factors driving passenger car bushing market growth is the rising consumer expectation for improved ride comfort and cabin quietness. As vehicle buyers become more discerning especially in the mid- to high-end segments, automakers are under pressure to deliver cars that offer smooth handling, minimal vibration, and low cabin noise. Bushings play a crucial role in this by acting as isolators between metal components in the suspension, chassis, and steering systems. They absorb shocks from road irregularities, reduce the transmission of engine vibrations, and help maintain vehicle stability.

MARKET RESTRAINTS

Durability and Performance Limitations of Traditional Materials to Hamper the Market Growth

A significant restraint in the market is the limited durability and performance of traditional rubber-based materials, particularly under harsh operating conditions. Most conventional bushings are made from natural or synthetic rubber, which, while cost-effective and flexible, can degrade over time when exposed to heat, oil, moisture, road salts, and mechanical stress. This degradation can lead to hardening, cracking, and eventual failure of the bushing, affecting vehicle performance, comfort, and safety. These limitations become more pronounced in regions with extreme weather conditions or poor road infrastructure, where bushings are subjected to constant stress.

MARKET OPPORTUNITIES

Growing Electric Vehicle (EV) Adoption to Create Market Opportunity

The accelerating global shift toward electric vehicles (EVs) presents a major growth opportunity for market players. Unlike traditional internal combustion engine (ICE) vehicles, EVs have distinct structural and performance characteristics that demand more advanced bushing solutions. EVs are typically heavier due to large battery packs and this added weight places greater stress on suspension and chassis components, increasing the need for durable and high-performance passenger car bushings that can handle heavier loads without compromising comfort.

MARKET CHALLENGES

Rising Cost of Raw Materials and Supply Chain Disruptions to Create Challenges for Market Growth

One of the major challenges affecting the market expansion is the rising cost and inconsistent availability of raw materials, such as synthetic rubber, polyurethane, and specialized elastomers. These materials are critical for manufacturing bushings that meet performance, durability, and NVH (noise, vibration, harshness) requirements. However, fluctuations in global oil prices, geopolitical tensions, and environmental regulations have impacted the supply and cost stability of these raw materials. Furthermore, delays in material sourcing or shipping can slow down production timelines for both OEMs and aftermarket suppliers, increasing lead times and operational costs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Application

Surging Bushing Demand for Riding Comfort to Fuel the Growth of the Suspension Segment

Based on application, the market is segmented into suspension, engine, chassis, interior, exhaust, and transmission.

The suspension segment led the global passenger car bushing market share in the year 2024. The increasing demand for better riding comfort and vehicle stability and rising product adoption are driving substantial expansion of the suspension segment. The necessity for sophisticated transmission bushings has been fueled by the rising complexity of contemporary transmissions and the desire for a more comfortable driving experience.

By Material

Rubber's Great Vibration-Damping Capabilities to Support the Segmental Growth

The market is segmented by material into rubber, polyurethane, brass, aluminum, bronze, and others.

Among these, the rubber segment dominated the global market share in 2024. The dominance of rubber passenger car bushings is owing to its superior vibration damping capabilities and affordability. Furthermore, advancements in rubber technology are driving the development of high-damping rubber components.

The polyurethane segment is likely to grow at the highest CAGR during 2025-2032. The growth is driven by its excellent durability, light weight, and improved performance in applications such as electric vehicles.

Passenger Car Bushing Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Passenger Car Bushing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 7.64 billion in 2025, representing 7.26% of the global market share, and is projected to reach USD 8.09 billion in 2026. The market in North America is driven by a mature automotive sector, high consumer expectations for ride comfort, and a steady shift toward electric vehicles. Automakers in the region emphasize advanced suspension technologies, creating demand for durable and performance-optimized bushings. The focus on vehicle safety, along with road conditions in various parts of the region, supports the need for robust bushing systems. Regulatory standards on vehicle emissions and performance also encourage innovation in bushing materials and designs. OEMs and aftermarket players alike are adopting new technologies to enhance NVH (noise, vibration, harshness) performance. The U.S. market is projected to reach USD 6.14 billion by 2026.

Europe and the Asia Pacific

Other regions such as Europe and Asia Pacific, are anticipated to witness notable market growth in the coming years. During the forecast period, in 2025, the Asia Pacific held 64.62% of the global market, reaching a valuation of USD 67.99 billion, and is projected to grow to USD 72.37 billion in 2026. The Japan market is projected to reach USD 9.23 billion by 2026, the China market is projected to reach USD 41.68 billion by 2026, and the India market is projected to reach USD 13.05 billion by 2026. Asia Pacific is the most dynamic and rapidly expanding region in the global passenger car bushing industry, driven by high vehicle production in countries such as China, India, Japan, and South Korea. Rising middle-class income, growing urbanization, and increased car ownership fuel the consistent demand for passenger vehicles, particularly compact and mid-size models. After Asia Pacific, the European market was valued at USD 27.43 billion in 2025, capturing 26.07% of global revenue, and is estimated to reach USD 28.8 billion in 2026. Europe’s bushing market is heavily influenced by stringent regulations around vehicle emissions and noise reduction. Automakers in the region are increasingly turning to lightweight and sustainable bushing materials to meet environmental targets while enhancing ride quality. The UK market is projected to reach USD 4.82 billion by 2026, while the Germany market is projected to reach USD 5.15 billion by 2026.

Rest of the World

Over the forecast period, the rest of the world, which includes the Middle East, Africa, and parts of Latin America, would witness moderate growth. The market in these regions is anticipated to have reached a valuation of USD 6.75 billion in 2025. The market is growing steadily but faces challenges such as infrastructure limitations and economic variability.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize the Delivery of High-Quality Bushings to Strengthen their Dominant Positions

The market is moderately consolidated, with a mix of global automotive component manufacturers and regional players competing on the basis of product durability, material innovation, and cost efficiency. Leading passenger car bushing companies focus on delivering products that enhance ride comfort, reduce vibration, and meet the performance demands of modern vehicles, including electric and hybrid models. Competition is also influenced by advancements in material science, with manufacturers increasingly using polyurethane, thermoplastic elastomers, and composite materials to offer longer service life and improved NVH (noise, vibration, harshness) control.

LIST OF KEY PASSENGER CAR BUSHING COMPANIES PROFILED

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Jotex Rubber Industrial Co., Ltd. (Taiwan)

- Sumitomo Riko Company Limited (Japan)

- DuPont de Nemours, Inc. (U.S.)

- BOGE Rubber & Plastics (Belgium)

- Vibracoustic SE (Germany)

- Hyundai Polytech India Pvt. Ltd. (India)

- Nolathane (Australia)

- Hutchinson Paulstra (France)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, MAHLE unveiled HD technology, claiming superiority over original equipment parts in Korea. MAHLE HD's technological prowess includes MAHLE HD ball pins, MAHLE HD rubber bushings, and MAHLE HD stabilizer links.

- In July 2024, Standard Motor Products acquired Nissens Automotive boosting its thermal management and bushing offerings within Europe.

- In April 2024, WinPart, a leading automotive spare parts distributor, announced its exclusive partnership with Kavo Parts, a renowned spare parts supplier for passenger cars and light commercial vehicles, in Europe. This strategic alliance marks a significant milestone in WinPart's commitment to offering its clientele with an extensive array of top-tier and affordable products.

- In January 2024, Rheinmetall AG secured an order from a global automaker for rocker arm bushings intended for heavy transport engine variants. The contract’s scope includes supplying high-precision engine component bushings, underscoring reliance on trusted suppliers for critical performance parts.

- In June 2023, Hyundai Polytech Mexico expanded in Coahuila. The company invested USD 13 million to expand its existing plant, reaching a cumulative investment of USD 24 million. The new extension will be for the manufacturing of plastic auto parts such as dust covers, thermoforming, anti-vibration systems, precision injection, steering parts, and a wide variety of rubber parts.

REPORT COVERAGE

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.10% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application · Suspension · Engine · Chassis · Interior · Exhaust · Transmission |

|

By Material · Rubber · Polyurethane · Brass · Aluminum · Bronze · Others |

|

|

By Geography North America (By Application, Material, and Country) · U.S. · Canada Europe (By Application, Material, and Country) · U.K. · Germany · France · Rest of Europe Asia Pacific (By Application, Material, and Country) · China · Japan · India · South Korea · Rest of Asia Pacific Rest of the World (By Application, Material, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 105.22 billion in 2025 and is projected to reach USD 165.63 billion by 2034.

In 2025, the North America market value stood at USD 7.64 billion.

The market is expected to grow at a CAGR of 5.10% during the forecast period of 2026-2034.

The increasing demand for ride comfort and noise reduction is a key factor propelling the market.

Continental AG (Germany), ZF Friedrichshafen AG (Germany), Jotex Rubber Industrial Co., Ltd. (Taiwan), Sumitomo Riko Company Limited (Japan), DuPont de Nemours, Inc. (U.S.), and BOGE Rubber & Plastics (Belgium) among others are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 100

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us