Passive Optical Network (PON) Market Size, Share & Industry Analysis, By Type (EPON, GPON, and Others), By Component (Optical Line Terminal (OLT), Optical Network Terminal (ONT), and Optical Distribution Network (ODN)), By Application (FTTX {FTTH, FTTB and FTTP} and Mobile Backhaul) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

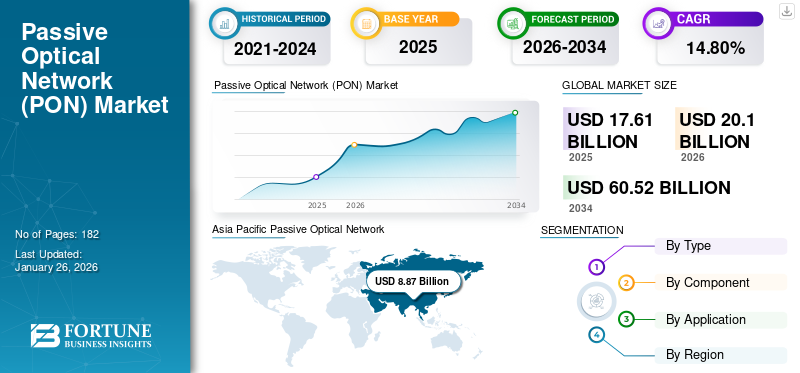

The global passive optical network (PON) market size was valued at USD 17.61 billion in 2025 and is projected to grow from USD 20.10 billion in 2026 to USD 60.52 billion by 2034, exhibiting a CAGR of 14.80% during the forecast period. Asia Pacific dominated the passive optical network (PON) market with a market share of 50.30% in 2025.

A Passive Optical Network (PON) is a fiber-based broadband technology used by internet service providers and telecommunication companies to offer a high speed internet with lower latency to the customers. This system includes different components such as Optical Network Terminal (ONT), Optical Line Terminal (OLT), and Optical Distribution Network (ODN).

The market is growing steadily due to increasing demand for ultra-fast broadband, 5G backhaul necessities, widening FTTH deployment and surging digitalization across commercial, industrial and residential sectors. Additionally, government’s fiber-infrastructure investments also accelerate the technology adoption.

Different key players operating in the market are ADTRAN, Inc., Calix, Inc., Ciena Corporation, CISCO SYSTEMS, INC., Huawei Investment & Holding Co., Ltd., Infinera Corporation, Nokia Corporation and others. These companies are expanding geographically and investing in research & development to maintain competitive advantage.

Download Free sample to learn more about this report.

Passive Optical Network [PON] Market KEY TAKEAWAYS

- 2025 Market Size: USD 17.61 billion

- 2026 Market Size: USD 20.10 billion

- 2034 Forecast Market Size: USD 60.52 billion

- CAGR: 14.80% from 2026–2034

- Asia Pacific dominated the passive optical network (PON) market with a 50.30% share in 2025.

- The GPON segment is projected to hold the largest market share with 39.73% in 2026.

- The Optical Network Terminal (ONT) segment is projected to account for the largest market share with 43.41% in 2026.

Asia Pacific

The market was valued at USD 8.87 billion in 2025, driven by extensive fiber network deployments.

North America

The market was valued at USD 4.23 billion in 2025, supported by increasing investments in PON technologies.

Europe

The market reached USD 3.09 billion in 2025, fueled by government initiatives promoting energy-efficient networking equipment.

U.S.

The market is projected to reach USD 4.00 billion by 2026, driven by expanding broadband infrastructure.

Japan

The market is projected to reach USD 1.26 billion by 2026, supported by continued fiber network expansion.

Read More

IMPACT OF RESCIPROCAL TARIFF

Reciprocal Tariffs Leads to Increased Cost of Crucial Optical Components

Reciprocal tariffs significant impact the PON market by increasing the cost of essential optical components, networking equipment and fiber cables. Increased import duties lead to higher production and procurement costs for telecom operators and manufacturers, thus resulting in highly expensive broadband deployment. It also hampers the global supply chains, causing delay in obtaining specific components and slowing 5G and FTTH related PON rollout projects. With the increase in cost, operators slow down the network upgrades, thus leading to a lapse in market growth. International vendors also face decreased competitiveness, hampering the cross border expansion and deterring collaboration in enhancing next-generation PON technologies.

MARKET DYNAMICS

Market Drivers

Surge in Next-Gen Wireless Infrastructure (5G & Beyond) Drives the Market Development

The rapid growth of 5G and different emerging next-generation wireless technologies is a significant driver for Passive Optical Network (PON) market growth. These networks demand a low latency and high capacity fiber backhaul that aids in supporting huge data traffic and dense small-cell deployment. PON solutions including 25G-PON and XGS-PON provide bandwidth and scalability needed for meeting the 5G performance demand. With operators augmenting the use of 5G technology, the demand for robust fiber infrastructure increases, thus surging investments in PON technologies.

- For instance, according to a report published in July 2022 by the Economic Co-operation and Development (OECD), high-speed optical fiber subscriptions have risen to 14%, which now accounts for 30% of the fixed broadband connections.

Market Restraints

Presence of Substitute Technologies and Residual Players to Deters the Market Growth

The PON market tends to face challenges owing to the presence of substitute technologies including fixed wireless access, DOCSIS, and conventional broadband that provide a lower cost or highly flexible option for deployment to some operators. This decreases the need for full fiber investments across certain regions. Moreover, the growing competition from well-established telecom service providers and local fiber providers also restricts the entrance of new startups in the market.

Market Opportunities

Seeking Trusted Network Solutions for Cyber Security and Secure Networking Offers Lucrative Growth Opportunities

Increase in demand for trusted and secure network infrastructure offers a prominent opportunity for the market. With increasing cyber threats, enterprises and governments globally are prioritizing networks with higher reliability, security and monitored vendor ecosystems. PON technology supports a secure and fiber based connectivity, making it highly attractive for telecom, defense, healthcare and smart city applications. Other key opportunities emerge from developing encrypted PON solutions, partnerships with organizations looking for trusted vendors, and compliance-based products.

PASSIVE OPTICAL NETWORK MARKET TRENDS

Implementation of PON Systems to Reduce Network Complexities and Smooth Connectivity Has Emerged as a Prominent Market Trend

A prominent trend reshaping the market is growing implementation of PON systems to shorten network architecture and improved connectivity. With the use of single fiber to offer multiple endpoints, PON decreases the demand for active components, lessening the maintenance demands, and operational complexity. This streamlined infrastructure allows for a faster data transmission, reduced energy consumption and enhanced reliability. Different telecom operators are growingly adopting advanced variants to aid support high-bandwidth applications, 5G backhaul and cloud services.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Wide Adoption of GPON in Broadband and Fiber Deployments Boosts Segment Growth

Based on type, the market is segmented into EPON, GPON, and others.

GPON segment held the largest Passive Optical Network (PON) market is projected to reach for 39.73% of the global market share in 2026. This growth is due to the growing use of GPON in broadband and fiber-to-the-home deployments. Additionally, its cost effectiveness, ability to support high speed services and reliability makes it an effective choice for global telecom operators.

The other segment held highest CAGR of 16.6% in 2024, and majorly includes next generation GPON. This segment’s growth is attributed to the rise in demand for greater bandwidth capacity, higher speed, and enhanced network efficiency. This makes advanced PON solutions crucial for modern broadband and 5G powered infrastructure.

To know how our report can help streamline your business, Speak to Analyst

By Component

Significant Role of ONTs in End-User Connectivity Drives Segment Growth

The market is divided into Optical Line Terminal (OLT), Optical Network Terminal (ONT), and Optical Distribution Network (ODN), based on component.

Among these, Optical Network Terminal (ONT) segment dominated the market with a revenue share of USD 6.72 billion in 2024. This growth is attributed to its essential role in connecting the end-users to fiber networks. These components allow a high-speed data transmission, seamless integration of broadband, IPTV services, voice, and efficient service delivery, thus resulting in segmental growth. The optical network terminal (ONT) segment is expected to lead by component, contributing 43.41% globally in 2026.

Optical Line Terminal (OLT) segment held highest CAGR of 16.2% in 2024. Optical Line Terminals (OLTs) exhibit the fastest growth with increasing central office upgrades. With operators expanding their fiber networks, the demand for enhanced OLTs surges. This results in improved network control, higher bandwidth, and scalable PON deployment, thus driving the segment’s growth.

By Application

Extensive Deployment Across Residential and Commercial Sectors Drive FTTX Segment Growth

The market is divided into FTTX and mobile backhaul, based on application. FTTX segment is further distributed into FTTH, FTTB and FTTP.

Among these, the FTTX segment dominated the market with a revenue share of USD 8.71 billion in 2024. This segment also held highest CAGR of 16.2% in 2024. This segmental growth is due to its extensive deployment across commercial and residential broadband networks. Additionally, the growing demand for ultra-fast connectivity and ongoing fiber-to-home initiatives globally, also boosts the segment growth.

PASSIVE OPTICAL NETWORK MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

Asia Pacific Passive Optical Network (PON) Market Size 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 4.23 billion in 2025, representing 24.00% of the global market landscape, and is expected to reach USD 4.79 billion in 2026. This growth is attributed to the growing demand for equipment including OLT to strengthen the internet speed upstream and downstream. Additionally, growing investments in R&D and PON device innovations by end user across the U.S. also contributes to the market growth. The U.S. market is projected to reach USD 4.00 billion by 2026.

For instance, in December 2022, Axion reported that the U.S. government is planning an investment of USD 1.5 billion to develop telecom infrastructure with the aid of companies such as Nokia Telecommunications Company, Telefonaktiebolaget LM Ericsson, and Samsung Electronics Co Ltd.

Europe

Europe contributed 17.50% to the global market in 2025, with a valuation of USD 3.09 billion, and is projected to reach USD 3.43 billion in 2026. This regional growth is due to growing focus of EU government on greener equipment solutions driven by growth in electricity prices and environmental concerns. Additionally, the increased demand for OLT devices to secure seamless data services also supports the regional market growth. The UK market is projected to reach USD 0.77 billion by 2026 and the Germany market is estimated to reach USD 0.95 billion by 2026.

- For instance, in December 2022, the latest FTTH Council Europe report noted that the number of users that chose for fiber-to-the-home (FTTH) services and fiber-to-the-building (FTTB) has grown from 172 million to 182.6 million homes by the year 2020.

Asia Pacific

Asia Pacific accounted for USD 8.87 billion in 2025, representing 50.30% of the global market share, and is projected to reach USD 10.32 billion in 2026. This dominance is owing to the large-scale fiber network deployments and efficient government support for digital infrastructure. Additionally, the expanding broadband penetration, 5G rollout initiatives and urbanization further boosts the market growth. The Japan market is projected to reach USD 1.26 billion by 2026, the China market is estimated to reach USD 5.92 billion by 2026, and the India market is projected to reach USD 1.45 billion by 2026.

- For instance, in February 2022, MR Organization Limited (MRO), an Ahmedabad-based PON equipment and rotatory machinery parts manufacturer company, acquired the U.K.-based Standard Air Limited part supplier of PON equipment.

South America and Middle East & Africa

The markets in South America and Middle East & Africa are growing with an expected share of USD 0.60 billion and USD 0.83 billion respectively in 2025. This growth is attributed to the increased internet penetration rate across countries including Brazil, Mexico, Argentina, and others. Additionally, key players across the region are also looking for advanced optical network terminals to acquire significant market share. GCC countries are predicted to have a market share of USD 0.16 billion by 2025. In 2025, Middle East & Africa held 4.70% of the global market, reaching a valuation of USD 0.83 billion, and is projected to grow to USD 0.91 billion in 2026.

Latin America

Latin America contributed approximately USD 0.6 billion to the global market in 2025, accounting for 3.40% share, and is expected to reach USD 0.65 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Acquisitions to Sustain their Market Positions

The PON industry is fairlt consolidated with key players including ADTRAN, Inc., Calix, Inc., Ciena Corporation, CISCO SYSTEMS, INC., Huawei Investment & Holding Co., Ltd., Infinera Corporation, Nokia Corporation, and others operating in it. These firms are expanding their product portfolio through innovations and adoption of advanced technologies to maintain the market share globally.

LIST OF KEY PASSIVE OPTICAL NETWORK COMPANIES PROFILED

- ADTRAN, Inc. (U.S.)

- Calix, Inc. (U.S.)

- Ciena Corporation (U.S.)

- CISCO SYSTEMS, INC. (U.S.)

- Huawei Investment & Holding Co., Ltd. (China)

- Infinera Corporation (U.S.)

- Nokia Corporation (Finland)

- Telefonaktiebolaget LM Ericsson (Sweden)

- TP-Link Corporation Limited. (China)

- ZTE Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- In April 2025, China launched its first 10G broadband network in Sunan County, Hebei Province, marking a significant advancement in internet infrastructure. The launch is a collaborative work of Huawei and China Unicom, and it aims to deliver download speeds up to 9,834 Mbps, upload speeds of 1,008 Mbps, and latency as low as 3 milliseconds.

- In April 2025, Huawei and China Unicom have jointly launched the first 10G broadband network in Sunan County, located in Hebei Province, China. The breakthrough is based on the globally leading 50G PON (Passive Optical Network) technology. According to the report, enhancements to the core architecture of the optical fiber access network have enabled a dramatic leap in performance—boosting throughput from gigabit to 10G levels, while reducing network latency to just milliseconds.

- In November 2023, Nokia, a prominent technology leader, marked a major advancement in the Indian broadband sector through its partnership with TATA Play Fiber to unveil India’s first WiFi6-ready broadband network. This initiative addresses the growing need for robust broadband connections, which are increasingly vital in both homes and businesses as digital connectivity assumes a fundamental role in everyday living.

- In May 2023, Vietnam Posts and Technology (VNPT, a leading Vietnam operator, announced its deployment of 10G fiber broadband services. The first phase roll out will deploy services for 10,000 homes and business in major 8 provinces of the country.

- In February 2023, Saudi Telecom Company (STC) and Huawei Technology announced their completion of first 50G PON trial in the Middle East. The trials were conducted on a live optical network with Huawei.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the Passive Optical Network market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 14.80% from 2026-2034 |

|

Historical Period |

2019-2023 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type, Component, Application and Region |

|

By Type |

· EPON · GPON · Others (Next Generation PON, etc.) |

|

By Component |

· Optical Line Terminal (OLT) · Optical Network Terminal (ONT) · Optical Distribution Network (ODN) |

|

By End-User |

· FTTX o FTTH o FTTB o FTTP · Mobile Backhaul |

|

By Region |

· North America (By Type, Component, Application and Country/Sub-region) o U.S. (By Application) o Canada (By Application) o Mexico (By Application) · Europe (By Type, Component, Application and Country/Sub-region) o U.K. (By Application) o Germany (By Application) o France (By Application) o Italy (By Application) o Spain (By Application) o Russia (By Application) o Benelux (By Application) o Nordics (By Application) o Rest of Europe · Asia Pacific (By Type, Component, Application and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o ASEAN (By Application) o Oceania (By Application) o Rest of Asia Pacific · South America (By Type, Component, Application and Country/Sub-region) o Argentina (By Application) o Brazil (By Application) o Rest of South America · Middle East & Africa (By Type, Component, Application and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 20.10 billion in 2026 to USD 60.52 billion by 2034, exhibiting a CAGR of 14.80% during the forecast period.

The market is expected to exhibit steady growth at a CAGR of 14.80% during the forecast period.

Surge in next-gen wireless infrastructure (5G & Beyond) drives the market growth.

ADTRAN, Inc., Calix, Inc., Ciena Corporation, CISCO SYSTEMS, INC., Huawei Investment & Holding Co., Ltd., Infinera Corporation, Nokia Corporation and others are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 7.65 billion in 2024.

- 2021-2034

- 2025

- 2021-2024

- 182

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us