Patient Experience Technology Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (On-Premise, Cloud-based, and Hybrid), By Application (Appointment Scheduling & Access, Patient Communication & Engagement, Virtual Care, Patient Feedback / VoC & Service Recovery, Inpatient Engagement / Point-of-Care Experience, and Others), By End User (Healthcare Providers {Hospitals & ASCs, Post-Acute & Long-Term Care Facilities, and Others}, Healthcare Payers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

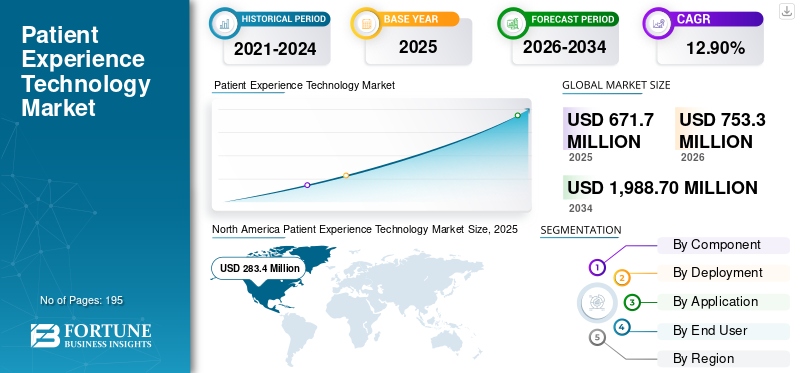

The global patient experience technology market size was valued at USD 671.7 million in 2025. The market is projected to grow from USD 753.3 million in 2026 to USD 1,988.7 million by 2034, exhibiting a CAGR of 12.90% during the forecast period. North America dominated the global patient experience technology market with a share of 42.19% in 2025.

Patient experience technologies include software platforms and digital tools designed to enhance patient engagement, communication, satisfaction, and care coordination across the healthcare journey. The global market is rapidly growing within the digital health and healthcare IT industry. This can be attributed to factors such as shift toward value-based healthcare, growing digitalization, and others.

Several key industry players, such as Oracle, Epic Systems Corporation, and GetWellNetwork, Inc. are shaping the overall market through various strategic initiatives, in turn maintaining their market positions.

Download Free sample to learn more about this report.

PATIENT EXPERIENCE TECHNOLOGY MARKET Key Takeaways

- 2025 Market Size: USD 671.7 million

- 2026 Market Size: USD 753.3 million

- 2034 Forecast Market Size: USD 1,988.7 million

- CAGR: 12.90% from 2026–2034

- North America dominated the global patient experience technology market with a share of 42.19% in 2025.

- The appointment scheduling & access segment is expected to lead the market with a 28.8% share in 2026.

- The cloud-based segment is projected to record the fastest growth, exhibiting a CAGR of 15.65% during the forecast period.

North America

North America’s market size in 2024 was at USD 252.9 million and maintained its dominance in 2025 with USD 283.4 million. Advanced healthcare IT infrastructure and strong emphasis on patient satisfaction metrics have propelled the regional market’s growth.

Europe

Europe is projected to witness a CAGR of 12.54% over the forecast timeframe and achieve USD 201.2 million by 2026. The region is anticipated to witness second highest growth driven by digital health initiatives and public healthcare modernization programs.

Asia Pacific

Asia Pacific is expected to be valued at USD 176.4 million in 2026 and is anticipated to be the fastest-growing regional market due to expanding healthcare access and increasing mobile health adoption.

U.S.

The U.S. market is estimated at USD 293.6 million in 2026, accounting for approximately 39.0% of global market revenue, supported by technological advancements and widespread adoption of patient engagement solutions.

Japan

Japan's market is projected to reach USD 53.0 million in 2026, representing around 7.0% of global revenue, driven by growing investments in digital healthcare technologies and patient-centered care initiatives.

Read More

PATIENT EXPERIENCE TECHNOLOGY MARKET TRENDS

Shift Toward Automation to Reduce Staff Workload is a Prominent Trend

In recent years, healthcare providers are rapidly shifting toward automation resulting in complete digital intake, automated registration/check-in, appointment actions, and online payments. This is aimed at reducing front-desk workload and streamline throughput. Furthermore, this trend is driven by staffing shortages and rising call-center volumes, so providers are prioritizing patient experience platforms that automate repetitive admin tasks while keeping the patient journey consistent.

- In September 2025, Phreesia acquired AccessOne to expand its healthcare payment solutions, reinforcing the market direction toward integrated, self-serve patient financial experiences.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Global Shift Toward Value-based Healthcare is Driving Market Growth

The global shift toward value-based care delivery is a key driver for the patient experience technology market growth. This is because provider and payer incentives increasingly reward quality, outcomes, and patient experience, not just visit volume. As healthcare organizations take on more accountability for total cost of care, they invest in PXT tools that reduce friction across the journey. Value-based healthcare also increases the need for measurement and continuous improvement, pushing adoption of experience analytics and closed-loop workflows.

- According to the data published by Centers for Medicare & Medicaid Services in January 2025, 53.4% of Traditional (fee-for-service) Medicare beneficiaries are in an accountable care relationship, indicating accelerating VBHC penetration.

MARKET RESTRAINTS

Budget Constraints and Limited IT Resources to Hamper Market Growth

Budget constraints and limited IT resources are a major market restraint for patient experience technology market growth. The implementation of PXT requires integration work, training, workflow redesign, and ongoing optimization, which results in increasing burden on the organizations. This constraint is most visible in smaller/community hospitals and in systems facing multi-year margin pressure.

- For instance, according to an article published by American Hospital Association (AHA) in April 2025, hospitals and health systems continue to face persistent economic challenges.

MARKET OPPORTUNITIES

Expansion of Telehealth and Virtual Care Services Create Growth Prospects

The expansion of telehealth and virtual care creates a strong market opportunity for patient experience technology. As providers move toward hybrid care models, the demand for PXT platforms to coordinate across channels and reduce friction is significantly increasing. Virtual care also increases demand for digital triage, automated patient communications, and experience feedback. The opportunity is strengthened by supportive regulatory policies across the world.

- In February 2025, Hartford HealthCare (HHC) announced its plans for the introduction of a new virtual health platform in April.

MARKET CHALLENGES

Data Privacy and Cybersecurity Risks Pose a Critical Challenge to Market Growth

Data privacy and cybersecurity risks remain a significant challenge. PXT platforms include highly sensitive patient data thus, any breach or outage can quickly lower patient trust erosion, regulatory exposure, and operational disruption. Additionally, providers also face increased risk since many PXT workflows rely on integrations with EHRs, messaging gateways, analytics tools, and cloud services. This increases the cost and complexity of deployments and can delay purchasing decisions.

- In May 2025, Kettering Health suffered a cybersecurity incident linked to the Interlock

Segmentation Analysis

By Component

Recurring SaaS Subscription Models Fuel Software Segment’s Growth

Based on type, the market is divided into software and services.

The software segment is expected to hold the largest global patient experience technology market share. The segment’s dominance is driven by recurring SaaS subscription models, frequent feature upgrades, and the ability to deploy quickly across multi-site networks versus service-heavy, one-time projects. Software also delivers measurable ROI by reducing call-center load, no-shows, and administrative effort, which accelerates adoption. In addition, vendors increasingly bundle multiple modules into unified platforms, further concentrating revenues in software. Moreover, new product launches by operating players are also aimed at propelling the segmental revenue generation.

- In March 2025, Talkdesk introduced Talkdesk AI Agents for Healthcare, a software solution designed to automate routine patient/member inquiries and improve experience through agentic AI.

The services segment is anticipated to rise with a CAGR of 14.88% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

High Demand for On-premise Solutions to Boost Segmental Growth

On the basis of deployment, the market is divided into on-premise, cloud-based, and hybrid.

The on-premise segment dominated the global market in 2025 due to increased preference for data residency and privacy requirements, lower latency for in-facility applications, and easier alignment with legacy EHR infrastructure. In addition, security teams often prefer on-premise for more direct governance over access controls, patching cycles, and audit readiness. In 2026, the segment is set to hold 60.5% share.

- For instance, Epic Systems Corporation is one of the leading companies that offers on-premise solutions.

The cloud based segment is anticipated to rise with a CAGR of 15.65% over the forecast period.

By Application

Increasing Patient Volume to Propel Segmental Growth

Based on application, the market is divided into appointment scheduling & access, patient communication & engagement, virtual care, patient feedback / voc & service recovery, inpatient engagement / point-of-care experience, and others.

The appointment scheduling & access segment is expected to account for the largest patient experience technology market share. Factors supporting the segment dominance include increasing patient volume, rising digitalization in all aspects of healthcare, and increasing need for improving capacity utilization and patient satisfaction. The segment is set to hold 28.8% share in 2026.

- According to an article published in February 2025 by Relatient, an industry-wide surge in patient self-scheduling adoption was observed in the study.

The patient communication & engagement segment is anticipated to rise with a CAGR of 15.16% over the forecast period.

By End User

High Adoption by Hospitals Supported their Leading Position

Based on end user, the market is segmented into healthcare providers {hospitals & ASCs, post-acute & long-term care facilities, and others}, healthcare payers, and others.

The healthcare providers segment captured the dominating position in the global market and will capture a 82.1% market share in 2026. Most PXT investments are driven by provider priorities such as reducing call-center burden, improving capacity utilization, lowering no-shows, and meeting rising consumer expectations for “digital-first” care access. Providers also account for the majority of enterprise deployments because these platforms must integrate with hospital workflows and EHR systems to deliver measurable operational and experience outcomes. In addition, multi-site health systems increasingly standardize a single patient engagement stack across facilities, further concentrating spend within provider organizations.

In addition, healthcare payers are projected to grow at a CAGR of 16.26% during the study period.

Patient Experience Technology Market Regional Outlook

By geography, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Patient Experience Technology Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America’s market size in 2024 was at USD 252.9 million and maintained its dominance in 2025 with USD 283.4 million. Advanced healthcare IT infrastructure and strong emphasis on patient satisfaction metrics have propelled the regional market’s growth. Presence of well-established players in the country coupled with technological advancements in the offerings have supported the market growth in the U.S.

U.S. Patient Experience Technology Market

The U.S. market captured the highest share of the North American market and can be analytically approximated at around USD 293.6 million in 2026, accounting for roughly 39.0% of the global market.

Europe

Europe is projected to witness a CAGR of 12.54% over the forecast timeframe and achieve USD 201.2 million by 2026. The region is anticipated to witness second highest growth driven by digital health initiatives and public healthcare modernization programs.

U.K Patient Experience Technology Market

The U.K. market in 2026 is estimated at around USD 45.0 million, representing roughly 6.0% of global revenues.

Germany Patient Experience Technology Market

Germany’s market is projected to reach approximately USD 41.2 million in 2026, equivalent to around 5.5% of global sales.

Asia Pacific

Asia Pacific’s market is projected to be valued at USD 176.4 million in 2026 and secure the third position in the global market. Asia Pacific is the fastest-growing region due to expanding healthcare access, mobile health adoption, and rising healthcare expenditure.

Japan Patient Experience Technology Market

Japan in 2026 is estimated at around USD 53.0 million, accounting for roughly 7.0% of global revenues.

China Patient Experience Technology Market

China’s market is projected to reach revenues of around USD 32.4 million in 2026, representing roughly 4.3% of global sales.

India Patient Experience Technology Market

India’s market in 2026 is estimated at around USD 31.4 million, accounting for roughly 4.2% of global revenues.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are likely to witness a comparatively slower growth rate. Latin America will reach USD 34.1 million in 2026. Increasing investments in healthcare IT infrastructure in the region is driving the region’s growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Active Involvement of Key Companies in Strategic Initiatives to Strengthen Market Position

The global market represents a semi-consolidated structure owing to the presence of several well-established players as well as emerging companies. Prominent companies such as Oracle, Epic Systems Corporation, and GetWellNetwork, Inc. account for the dominating shares in the global market. These players focus on different strategic initiatives including partnerships & collaborations, new product launches, and others to maintain their market positions.

Other key players in the patient experience technology market include Veradigm LLC and Press Ganey. These players are also undertaking various strategies to gain market share.

LIST OF KEY PATIENT EXPERIENCE TECHNOLOGY COMPANIES PROFILED

- Epic Systems Corporation (U.S.)

- Oracle (U.S.)

- GetWellNetwork, Inc. (U.S.)

- Veradigm LLC (U.S.)

- National Research Corporation (U.S.)

- Press Ganey (U.S.)

- Luma Health Inc. (U.S.)

- Relatient (U.S.)

- Hyro (U.S.)

- Phunware Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Luma Health acquired Tonic Health with an aim to expand AI-native platform for patient intake and EHR integration.

- September 2025: Sutter Health and Hyro signed partnership agreement to incorporate its AI-powered patient communication tools.

- May 2025: GellWell Inc. launched Opal, an on-demand AI patient assistant for hospital experience and post-discharge support.

- March 2025: Relient introduced Dash Direct, an intelligent, open scheduling API platform designed to help organizations automate and manage patient interactions.

- February 2025: HURT! partners with Relatient for the expansion of access and improved experiences for orthopedic patients.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 12.90% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component, Deployment, Application, End User, and Region |

|

By Component |

· Software · Services |

|

By Deployment |

· On-Premise · Cloud-based · Hybrid |

|

By Application |

· Appointment Scheduling & Access · Patient Communication & Engagement · Virtual Care · Patient Feedback / VoC & Service Recovery · Inpatient Engagement / Point-of-Care Experience · Others |

|

By End User |

· Healthcare Providers o Hospitals & ASCs o Post-Acute & Long-Term Care Facilities o Others · Healthcare Payers · Others |

|

By Region |

· North America (By Component, Deployment, Application, End User, and Country) o U.S. o Canada · Europe (By Component, Deployment, Application, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Component, Deployment, Application, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Component, Deployment, Application, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Component, Deployment, Application, End User, and Country/Sub-region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 671.7 million in 2025 and is projected to reach USD 1,988.7 million by 2034.

In 2025, North Americas market value stood at USD 283.4 million.

The market is expected to exhibit a CAGR of 12.90% during the forecast period of 2026-2034.

By component, the software segment is expected to lead the market.

Global shift toward value-based care is primarily driving market expansion.

Oracle, GetWellNetwork, Inc., and Epic Systems Corporation are the major players in the global market.

North America dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 195

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us