PC Gaming Market Size, Share & Industry Analysis, By Game Type (Shooter, Action, Sports, Role Playing, and Others), By Revenue Model (In-Game Purchases, Game Purchase, and Advertising), By Platform (Online and Offline), By End-User (Male and Female), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

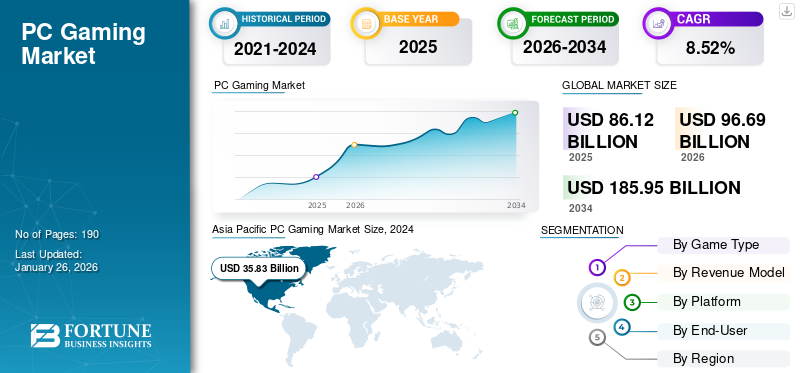

The global PC gaming market size was valued at USD 86.12 billion in 2025 and is projected to grow from USD 96.69 billion in 2026 to USD 185.95 billion by 2034, exhibiting a CAGR of 8.52% during the forecast period. Asia Pacific dominated the PC gaming market with a market share of 46.7% in 2024.

PC games are increasingly becoming popular among budding gamers due to the powerful processing technologies and better graphics than mobile, tablet, or console-based gaming. The increasing number of casual & hardcore PC gamers purchasing newer gaming subscription services to showcase their gaming performance drives the global market growth. In addition, consistent introduction of the laptop games made of AI, mixed reality, and innovative graphic design technologies by the leading players including Electronic Arts, Inc., Microsoft Corporation, Sony Group Corporation, Tencent Holdings Ltd., and Nintendo Co. Ltd. accelerate the sales of laptop games globally.

- Below mentioned are the percentage of U.S. gamers (aged above 8 years) who played on PC game platforms over generations in 2023 (Entertainment Software Report ‘Essential Facts 2024’):

- Alpha/Gen Z – 54%

- Millennials – 48%

- Generation X – 39%

- Boomers/Silent – 43%

- Asia Pacific witnessed PC gaming market growth from USD 31.69 Billion in 2023 to USD 35.83 Billion in 2024.

Download Free sample to learn more about this report.

Global PC Gaming Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 86.12 billion

- 2026 Market Size: USD 96.69 billion

- 2034 Forecast Market Size: USD 185.95 billion

- CAGR: 8.52% from 2026–2034

Market Share:

- Asia Pacific dominated the PC gaming market with a 46.7% share in 2024, driven by increasing spending on gaming subscriptions, in-game purchases, and the rapid growth of online gaming communities in China, Japan, and India.

- By game type, the Shooter segment is expected to retain the largest market share in 2025, supported by widespread popularity of competitive titles like PUBG, Call of Duty, and Fortnite, along with rising eSports engagement.

Key Country Highlights:

- China: Leads the regional market due to a massive player base, strong sales of gaming desktops, and rising adoption of cross-platform gaming and cloud-based services.

- India: Witnessing fast growth in gaming PC shipments and government incentives attracting gaming hardware manufacturers under schemes like the expanded PLI.

- United States: Home to major game developers and platforms like Epic Games and Valve; rising in-game spending and game purchases contribute significantly to market revenues.

- Japan: Strong cultural affinity for gaming and high PC penetration support steady market growth; also benefits from exclusive regional game releases and local development studios.

- Germany & France (Europe): High demand for cloud-based and online multiplayer PC games, along with increased in-game purchase activity, fuels Western and Central European market growth.

PC GAMING MARKET TRENDS

Rise of Cross-Platform Play with Interactive Features to Create Newer Market Growth Avenues

Emergence of cross-platform gaming enabling users gain unified and inclusive console and mobile gaming experiences with their laptops. Growing number of companies offering cross-platform play experiences to the users create newer market growth avenues globally. In addition, increasing consumer purchases of the cross-platform online games featuring real-time interaction, enhanced graphics, and other innovative features favor the services revenues globally.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Gaming Laptop Penetration to Drive Market Growth

Rising demand for gaming laptops and desktops with dedicated RAM space, cooling systems, and GPU, coupled with the growing popularity of eSports tournaments, sponsorships, and streaming platforms games, including Twitch, Facebook gaming, YouTube gaming, and others, accelerate the global PC gaming market growth. In addition, advancements in developing high-performing processors and graphics technologies that support entertaining PC video gaming experiences have skyrocketed service revenues.

- In the financial year 2022, HP, a global laptop brand, doubled its gaming PC shipments in India, reaching 0.28 million from 0.13 million in 2021.

MARKET RESTRAINTS

Higher Costs of Gaming Subscriptions and Game Purchases to Restrain Market Growth

Higher costs of in-game subscriptions and game purchases limit its demand among middle-income gamers. In addition, higher prices of PC video gaming peripherals, including headphones, joystick, gamepad, keyboard, mouse, and others, hamper consumer gaming services spending globally. Besides, the incidences of game addiction due to the play gaming of intense graphics for a duration exceeding the prescribed limit restrains its demand across many countries.

MARKET OPPORTUNITIES

Advancements in Cloud Gaming and Game Streaming to Favor Market Growth

The rise of cloud gaming platforms enabling users to play high-end games without using hardware or gaming peripherals creates newer opportunities in the cloud-based PC video gaming industry. In addition, consistent entertainment firms’ integration of AI and machine learning features in PC video gaming solutions allows gamers to predict competitor gamers’ actions in the multiplayer environment, creating newer PC gaming market growth prospects.

Segmentation Analysis

By Game Type

Higher Gamers’ Spending on Shooter Game Purchases Result in Shooter Segment to Lead Market

Based on various game types, PC gaming market analysis include shooter, action, sports, role playing, and others.

Significant gamers are spending on in-game purchases while playing multiple shooting games, including PUBG, Call of Duty, Fortnite, and others, resulted in the shooter segment holding a majority global PC gaming market share in 2025.

- The average daily player count of the EPIC Games-owned Fortnite Creative and UEFN increased by 15% in 2024 compared to 2023.

In addition, the growing popularity of competitive gaming requiring professional-level precision in player movement and actions in multiplayer shooting games accelerates the shooter segment’s revenue growth.

Others segment covers the analysis of various game types, including adventure, racing, fighting, strategy, and others. Broadening gamers’ necessities to spend on multiple games to reveal their gaming skills on social media channels led to the others segment experiencing the fastest growth during the forecast period of 2025-2032.

By Revenue Model

In-Game Purchases Segment led the Market Due to Significant Gamers Spending on In-Game Features

The global market is segmented by revenue model into in-game purchases, game purchases, and advertising.

In-game purchases segment exhibited a leading global market share in 2025. The segment is also slated to grow at a fastest rate during the forecast period of 2025-2032. Gaming companies provide interactive gaming experiences based on the user’s behavioral and psychological responses to stimulate gamers to make in-game purchases. In-game purchases enable users to unlock more adventurous gaming levels and express their gaming skills. Significant gamers’ spending on in-game purchases led to this segment capturing a major market share in 2024. Rising consumer spending on online gaming subscriptions to play games for longer duration skyrockets the in-game purchases segment at the fastest rate during the forecast period of 2025-2032.

By Platform

Higher Preference for Offline Gaming to Avoid Interruption of Game Upgrades Result in Offline Segment to Lead Market

Based on the platform, the global market is bifurcated online and offline.

Gamers spend money on offline gaming installations to avoid the interruption of game upgrades and internet disconnection issues in online gaming. Higher consumer spending on offline gaming downloads resulted in the offline segment holding a major market share in 2025.

The growing popularity of cloud gaming applications and online gaming platforms offering enhanced gaming experiences to users accelerates the online segment at the fastest rate during the forecast period of 2025-2032.

By End-User

Higher Men’s Inclination Toward Gaming Activities Resulted in Men Segment to Lead Market

Based on end-users, the market is bifurcated into male and female.

Higher men’s inclination toward indoor PC video gaming resulted in the men's segment holding a major market share in 2025. In addition, the greater availability of games designed specifically for men results in significant PC game sales revenue generation from the men segment.

The increasing number of women consumers expressing their gaming skills on social media platforms accelerates women's segmental growth.

PC Gaming Market Regional Outlook

The market is categorized by geography into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific PC Gaming Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market with a 46.70% share. The region generated revenues of USD 35.83 billion in 2024. The region’s market is projected to grow at the fastest rate of 10.13% during the forecast period of 2025-2032. The higher number of PC/desktop gamers spending on gaming subscription plans and in-game purchases resulted in significant service revenue generation in China, Japan, and Southeast Asia. Growing number of online gamers and their purchases of gaming desktops in India and China accelerate market growth in these countries. Governmental financial assistance in attracting investments for the entertainment industry supports further market development across many countries in the region.

- For instance, in October 2021, the Government of India broadened the PLI Incentive scheme to attract USD 437.78 million in investment from gaming device makers in the Indian gaming industry.

North America

The North American region exhibited a second-leading global market share in 2024. The adoption of gaming PCs is significant in Canada and the U.S., resulting in considerable revenue from game purchases by consumers in the region. In addition, key players’ strong lineup of newer game releases increases the sales from the paid downloadable content and microtransactions, favoring the North American market growth.

- One thousand one hundred game titles were released on Epic Game stores in 2022. The top titles by player spend are Epic's Fortnite, Genshin Impact, and EA Sports FC 24.

Europe

European region exhibited a third-leading global PC gaming market share in 2024. Higher demand for the PC game online services, allowing consumers to compete online and access cloud services, resulted in a considerable revenue generation for the services in the Western European region. In addition, the rising number of PC gamers making in-game purchases skyrockets market growth in the Western and Central European regions.

Rest of the World

Growing indoor gaming leisure trends and increasing penetration of the social media channels covering PC gaming competitions and newer insights uplift the number of gamers, driving the market growth in Brazil, Saudi Arabia, and UAE. Rising internet penetration and growing accessibility to gaming laptops support the service revenue growth in the Southern African region.

COMPETITIVE LANDSCAPE

Key Industry Players

Consistent Key Players' PC Game Releases Allows Them Dominate Global Market

The global market is concentrated with companies such as Electronic Arts, Inc., Microsoft Corporation, and Sony Group Corporation, consistently focusing on releasing multiplatform gaming products to increase their business presence in the global gaming industry.

- For instance, in 2025, Electronic Arts, Inc. announced a multiyear UEFA license extension with the launch of an exclusive PC free-to-download FIFA Online 4 title for Asian, Russian, Polish, and Turkish gamers.

LIST OF KEY PC GAMING COMPANIES PROFILED

- Microsoft Corporation (U.S.)

- Nintendo Co. Ltd. (Japan)

- Rovio Entertainment Corporation (Finland)

- Nvidia Corporation (U.S.)

- Valve Corporation (U.S.)

- Electronic Arts, Inc. (U.S.)

- Sony Group Corporation (Japan)

- Bandai Namco Holdings Inc. (Japan)

- Tencent Holdings Ltd. (China)

- Activision Blizzard, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Plug In Digital, a global video game publisher and distributor, acquired PixelRatio, a video game development studio company, to expand its PC gaming business in Europe.

- March 2025: Xsolla, a global video game commerce company, announced its updates of Xsolla Cloud Gaming solution powered by new Amazon GameLift AWS Streams to allow gamer developers to provide high-quality PC and mobile gaming experiences to remote game players.

- February 2025: With its subsidiary company Rockstar Games, Take-Two-Interactive launched GTA 6 for the PC platform.

- February 2023: Anzu announced exclusive partnerships with Livewire to expand their business in the in-game advertising revenues covering different titles across mobile, PC, and console.

- January 2022: Microsoft Corporation acquired Activision Blizzard, a global PC gaming brand, to accelerate its business across PC & game consoles and cloud gaming.

REPORT COVERAGE

The global PC gaming market analysis provides market size & forecast by all the segments included in the report. It includes details on the market dynamics and PC/console gaming trends expected to drive the market during the forecast period. In addition, it provides information on key industry developments, new product launches, and details on partnerships, mergers & acquisitions. It covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.52% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Game Type

|

|

By Revenue Model

|

|

|

By Platform

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 86.12 billion in 2025 and is projected to record a valuation of USD 185.95 billion by 2034.

In 2024, the market value stood at USD 35.83 billion.

The global market is projected to grow at a CAGR of 8.52% during the forecast period of 2026-2034.

The shooter segment led the market by game type.

The rising gaming laptop penetration is uplifting the revenues of PC gaming services globally, thereby driving market growth.

Electronic Arts, Inc., Microsoft Corporation, and Sony Group Corporation are the top players in the market.

Asia Pacific dominated the PC gaming market with a market share of 46.7% in 2024.

Advancements in cloud gaming and game streaming are key factors favoring market growth.

- 2021-2034

- 2025

- 2021-2024

- 190

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us