Pembrolizumab Market Size, Share & Industry Analysis, By Product Type (KEYTRUDA IV and KEYTRUDA QLEX / SC Pembrolizumab), By Disease Indication (NSCLC, Melanoma, HNSCC, Urothelial Carcinoma, RCC, TNBC, Gastric/GEJ/Esophageal Cancers, Cervical Cancer, and Others), By Age Group (Pediatric and Adults), By Type (Branded and Biosimilar), By Therapy Setting (Early-stage / Perioperative, Advanced / Metastatic, and Others), By Route of Administration (IV and SC), By End User (Hospitals, Specialty Cancer Clinics, Ambulatory Infusion Centers, and Others), and Regional Forecast, 2026-2034

Pembrolizumab Market Size and Future Outlook

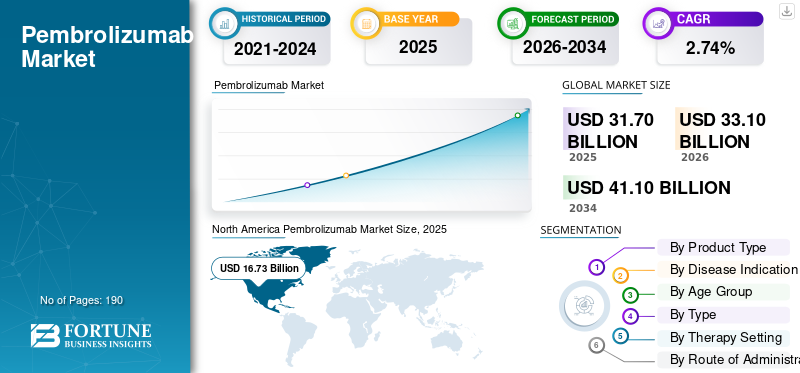

The global pembrolizumab market size was valued at USD 31.70 billion in 2025. The market is projected to grow from USD 33.10 billion in 2026 to USD 41.10 billion by 2034, exhibiting a CAGR of 2.74% during the forecast period. North America dominated the pembrolizumab market with a market share of 52.77% in 2025.

The market is growing steadily because the drug has become one of the most widely used immuno-oncology therapies across multiple cancer types and treatment settings. Its market expansion is being supported by continued label additions, strong physician confidence, and rising use in earlier lines of therapy, which increases the eligible patient pool. The market also benefits from the shift toward biomarker-driven cancer treatment, where pembrolizumab is often positioned as a key therapy option. In addition, ongoing clinical research and development along with lifecycle expansion into new formulations are helping the product maintain strong commercial momentum across major regions.

Key companies are increasingly focusing on new product launches and their subsequent approvals from respective authorities to capitalize on the market's growth potential.

- For instance, in September 2025, Merck & Co., Inc. received U.S. FDA approval for KEYTRUDA QLEX for subcutaneous use in adults across most solid tumor indications. The development adds a more convenient administration option, improving treatment delivery efficiency and supporting broader product adoption in oncology care settings.

Furthermore, leading players such as Merck & Co., Inc., Samsung Bioepis Co., Ltd, Sandoz AG., and Celltrion, Inc, are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

Global Pembrolizumab Market KEY TAKEAWAYS

- 2025 Market Size: USD 31.70 billion

- 2026 Market Size: USD 33.10 billion

- 2034 Forecast Market Size: USD 41.10 billion

- CAGR: 2.74% from 2026–2034

- North America dominated the global market with a 52.77% share in 2025 and a market value of USD 16.73 billion.

- The KEYTRUDA IV segment dominated the market, supported by established adoption, infusion-based workflows.

- The NSCLC segment dominated the market in 2025, driven by a large patient population.

North America

The region dominated the market with a value of USD 16.73 billion in 2025.

Europe

The market is projected to reach USD 7.60 billion in 2026 and record a growth rate of 2.26% over the coming years.

Asia Pacific

The region is projected to reach USD 6.24 billion in 2026, securing its position as the third-largest regional market.

U.S.

The market is estimated to reach USD 15.64 billion in 2026.

Japan

The market is estimated to reach USD 1.46 billion in 2026.

Read More

PEMBROLIZUMAB MARKET TRENDS

Growing Role of Immunotherapy in Standard Cancer Care is a Prominent Market Trend

The growing role of immunotherapy in standard cancer care strengthening as oncologists increasingly use immunotherapy not only in advanced disease but also in earlier treatment settings and perioperative regimens. As clinical evidence continues to show survival and event-free survival benefits, pembrolizumab is moving closer to routine treatment pathways across multiple tumor types. This wider clinical integration increases physician confidence, expands the eligible patient population, and supports more consistent product adoption across hospitals and oncology centers. As a result, the rising use of immunotherapy as part of standard cancer care is becoming an important trend shaping long-term market growth.

- For instance, in June 2025, Merck announced that the U.S. FDA approved KEYTRUDA for PD-L1 positive resectable locally advanced head and neck squamous cell carcinoma as neoadjuvant treatment, continued as adjuvant treatment with radiotherapy with or without cisplatin, and then as a single agent. This is significant because it shows pembrolizumab moving deeper into structured treatment pathways rather than being limited to later-stage use, which reflects the broader trend of immunotherapy becoming part of standard cancer care.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Global Cancer Burden Supporting Pembrolizumab Demand and Driving Growth

The global market is expanding as the overall cancer burden remains high, driving strong demand for advanced immuno-oncology therapies. As the number of patients diagnosed with major cancers such as lung, breast, colorectal, bladder, and kidney cancer rises, the need for effective systemic treatment also increases. This supports greater use of pembrolizumab, especially given its approval across multiple tumor types and treatment settings. Additionally, growing diagnosis rates, broader testing, and earlier treatment intervention are helping more patients enter the addressable treatment pool. As a result, the rising global cancer burden is driving demand for pembrolizumab.

- For instance, in November 2024, the World Health Organization's cancer agency, the International Agency for Research on Cancer (IARC), estimated the global burden of cancer. WHO also published survey results from 115 countries, showing that the majority do not adequately finance priority cancer and palliative care services as part of universal health coverage (UHC). The IARC estimates, based on the best sources of data available in countries in 2022, highlight the growing burden of cancer, the disproportionate impact on underserved populations, and the urgent need to address cancer inequities worldwide.

MARKET RESTRAINTS

High Treatment Costs and Reimbursement Pressure are Hampering Market Growth

The global market faces an important restraint: high treatment costs and reimbursement pressure. Pembrolizumab is a premium-priced immunotherapy, so its adoption is slower in markets with limited healthcare budgets and strict reimbursement reviews. Since payers and public health systems closely examine cost-effectiveness before granting broad coverage, patient access can be delayed or restricted even after regulatory approval. This reduces the speed of commercial uptake, especially in cost-sensitive countries and public reimbursement systems. As a result, high pricing and uneven reimbursement remain key factors restraining the pembrolizumab market growth.

- For instance, in January 2025, a published article in the Journal of Pharmaceutical Policy and Practice highlighted that the time to reimbursement for pembrolizumab varied across the U.K., Australia, and Israel, showing that reimbursement processes can delay patient access even in developed healthcare systems. This reflects how pricing review, health technology assessment, and payer negotiations can slow the commercial expansion of pembrolizumab despite its clinical value.

MARKET OPPORTUNITIES

Continuous Label Expansion across Multiple Tumor Types to Offer Growth Opportunities

The global pembrolizumab market is witnessing strong growth opportunities driven by continuous label expansion across multiple tumor types. This opportunity is growing because each new approval allows pembrolizumab to enter an additional cancer setting, treatment line, or patient subgroup, thereby directly expanding its commercial reach. As the product gains use across more solid tumors and earlier treatment stages, physicians become more confident in prescribing it, and healthcare providers integrate it more widely into oncology pathways. This also helps Merck strengthen the product lifecycle, improve brand presence, and expand the addressable patient pool over time. As a result, continuous regulatory expansion is creating long-term revenue opportunities for the global market.

- For instance, in February 2026, Merck announced that KEYTRUDA and KEYTRUDA QLEX plus paclitaxel ± bevacizumab was approved for certain adults with PD-L1-positive platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal carcinoma. This is an important market opportunity because it expands pembrolizumab into another difficult-to-treat cancer setting, increases the eligible treatment population, and supports further penetration across gynecologic oncology.

MARKET CHALLENGES

Strict Regulatory Requirements and Approval Complexity Pose a Challenge for Market Growth

A key market challenge for the global market is rising biosimilar and patent cliff pressures. This challenge is becoming more important, as pembrolizumab is a high-value biologic with very large global sales, which naturally attracts biosimilar developers. As more companies move their pembrolizumab biosimilars into clinical development and partnership stages, future competition is expected to increase, putting pressure on pricing, market share, and long-term revenue growth for the originator brand. This can reduce the product's exclusivity advantage over time and make it harder to sustain premium pricing across markets. As a result, the approaching biosimilar wave and patent-related pressures are emerging as major challenges for long-term growth.

- For instance, in June 2025, Dr. Reddy's and Alvotech announced a collaboration to co-develop and commercialize a biosimilar candidate to Keytruda (pembrolizumab) for global markets. The development highlights that multiple companies are already preparing for future competition in this space, which increases the likelihood of pricing pressure and revenue erosion once biosimilar entry becomes commercially viable.

Segmentation Analysis

By Product Type

KEYTRUDA 1V Dominates Due to its Increasing Preference for Integrated Solutions

Based on product type, the market is categorized into KEYTRUDA IV and KEYTRUDA QLEX/SC Pembrolizumab.

KEYTRUDA IV dominated the market because intravenous pembrolizumab has been the most established commercial format for years, giving it a much longer adoption period than the newer version. Since hospitals and oncology providers have already built infusion-based workflows around IV pembrolizumab, the product has benefited from entrenched prescribing habits, greater familiarity with reimbursement, and routine use across many tumor types. This has helped IV remain the largest revenue-generating format. As a result, the long-established market presence of IV pembrolizumab has likely kept this segment in the leading position.

- For instance, in March 2025, Merck announced that its investigational subcutaneous pembrolizumab demonstrated noninferior pharmacokinetics compared with intravenous KEYTRUDA in the pivotal 3475A-D77 trial. This is significant because it shows that IV pembrolizumab was already the established reference standard in the market before SC expansion began.

The KEYTRUDA QLEX is expected to grow at a CAGR of 20.44% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

High Prevalence and Disease Burden of NSCLC Puts it in a Leading Position

Based on disease indication, the market is segmented into NSCLC, melanoma, HNSCC, urothelial carcinoma, RCC, TNBC, gastric/GEJ/esophageal cancers, cervical cancer, and others.

In 2025, the NSCLC segment dominated the market as it represents one of the largest oncology treatment populations, and pembrolizumab has established a strong position in this disease across both earlier-stage and advanced settings. As non-small cell lung cancer (NSCLC) has a high incidence and pembrolizumab has generated long-term survival data in multiple KEYNOTE studies, physician confidence and prescribing volume have remained strong. This creates a larger treated patient base and more sustained revenue contribution than many smaller tumor segments.

- For instance, in October 2025, Merck announced that KEYTRUDA demonstrated a long-term survival benefit in certain patients with earlier or advanced NSCLC, including continued findings from KEYNOTE-671. This reinforces why NSCLC remains the most commercially important disease area for pembrolizumab.

The others segment is projected to grow at a CAGR of 4.93% over the forecast period.

By Age Group

Strong Demand by Adults Segment to Enable Segmental Dominance

Based on age group, the market is segmented into pediatric and adult.

In 2025, the adult age group, which primarily represents adults, is likely to dominate, as most pembrolizumab use is concentrated in adult solid tumor populations rather than pediatric oncology. This is because the majority of approved indications, treatment volumes, and real-world prescribing opportunities for pembrolizumab are in adult cancers, including NSCLC, HNSCC, urothelial carcinoma, RCC, and others. Since adult oncology accounts for a much broader patient population and is used more frequently across treatment lines, it naturally generates the largest share of global pembrolizumab market demand.

- For instance, in September 2025, Merck announced that the FDA approved KEYTRUDA QLEX for subcutaneous use in adults across most of its solid tumor indications. This highlights how the largest commercial expansion continues to center on adult oncology populations.

The pediatric segment is projected to grow at a CAGR of 6.01% during the study period.

By Type

Limited Competition to Branded Pembrolizumab Places it at the Top Position

Based on type, the market is segmented into branded and biosimilar.

The branded segment dominates as market is centered on Merck's originator brand, KEYTRUDA, while biosimilar has not yet entered the market. As KEYTRUDA has global approvals, extensive clinical data, and a fully established commercial footprint, it continues to capture the vast majority of market revenue. In addition, the absence of marketed pembrolizumab biosimilars in major regions has allowed the branded product to maintain pricing power and market leadership.

- For instance, in February 2026, Merck's fourth-quarter 2025 materials reported USD 31.7 billion in 2025 sales for KEYTRUDA/KEYTRUDA QLEX.

The biosimilar segment is projected to grow at a CAGR of 45.90% during the study period.

By Therapy Setting

Advanced/Metastatic Disease Therapy Setting Leads with its Robust Commercial Output

Based on therapy setting, the market is segmented into early-stage/perioperative, advanced/metastatic, and others.

The advanced or metastatic disease dominated as pembrolizumab first built its commercial base in late-stage oncology, where immunotherapy adoption became standard earlier and across more indications. Because patients with advanced or metastatic cancer often require systemic therapy quickly, and because pembrolizumab has broad use in these settings, treatment demand has remained large and commercially important. Although early-stage and perioperative use is expanding, the metastatic setting still benefits from longer-standing market penetration across multiple tumor types.

- For instance, in February 2026, Merck announced that the U.S. FDA approved KEYTRUDA and KEYTRUDA QLEX plus paclitaxel ± bevacizumab for certain adults with PD-L1-positive platinum-resistant ovarian carcinoma as second- or third-line treatment. This is significant because it shows continued commercial expansion in later-line, advanced disease settings, which remain a major source of demand.

The early-stage/perioperative segment is projected to grow at a CAGR of 6.27% during the study period.

By Route of Administration

Extensive Use of IV in Standard Care to Lead Growth in the Segment

Based on route of administration, the market is segmented into IV and SC.

IV dominated as intravenous delivery has been the standard route for pembrolizumab since launch, and majority of the real-world treatment infrastructure was built around infusion administration before SC entry. Since providers already had established infusion chairs, protocols, staff training, and reimbursement systems for IV KEYTRUDA, the IV route captured the bulk of treatment volume for a long period.

- For instance, in June 2025, Merck announced FDA approval of KEYTRUDA for PD-L1-positive resectable locally advanced HNSCC as part of a perioperative regimen, and this approval was based on the long-established KEYTRUDA treatment model, which had been built primarily on IV administration. This supports the idea that IV remained the dominant route before SC expansion began to scale.

The SC segment is projected to grow at a CAGR of 1.55% over the study period.

By End User

Increasing Demand in Pharmaceutical & Biopharmaceutical Companies Due to Large Patient Volumes to Lead Growth

Based on end user, the market is segmented into hospitals, specialty cancer clinics, ambulatory infusion centers, and others.

The specialty cancer clinics dominates, as pembrolizumab treatment decisions often depend on biomarker testing, oncology specialist oversight, infusion or injection capability, and close monitoring for immune-related adverse events. These clinics are highly focused on cancer management and are well-positioned to efficiently and consistently implement immunotherapy protocols across different tumor types. This concentration of oncology expertise supports stronger utilization than more general care settings.

- For instance, in November 2025, the European Commission approved subcutaneous KEYTRUDA for all adult indications approved in the European Union, and Merck noted that a healthcare provider can administer it in one minute. This is important for specialty cancer clinics as a faster provider-administered format can improve throughput and convenience in dedicated oncology treatment centers.

The others segment is projected to grow at a CAGR of 7.36% over the study period.

Pembrolizumab Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Pembrolizumab Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 15.77 billion and maintained its leading position in 2025 with USD 16.73 billion. The market is growing in North America as the region has a high cancer burden, strong adoption of biomarker testing, and broad use of immunotherapy in standard oncology care. In the U.S., the American Cancer Society estimates about 2.04 million new cancer cases in 2025, which supports sustained demand for therapies such as pembrolizumab.

U.S. Pembrolizumab Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 15.64 billion in 2026, accounting for roughly 47.24% of the global market.

Europe

Europe is projected to depict a 2.26% growth rate over the coming years, the second-highest among all regions, and reach USD 7.60 billion in 2026. The regional market has a strong oncology healthcare infrastructure and active policy support for cancer diagnosis and treatment. Europe's Beating Cancer Plan continues to support prevention, screening, diagnosis, and strengthening of the treatment system, helping expand access to advanced oncology therapies.

U.K Pembrolizumab Market

The U.K. is estimated at around USD 1.38 billion in 2026, representing roughly 4.17% of the global market.

Germany Pembrolizumab Market

Germany's market is projected to reach approximately USD 1.70 billion in 2026, equivalent to around 5.14% of the global market.

Asia Pacific

Asia Pacific will reach USD 6.24 billion in 2026 and secure the third position because of the large patient base, improving cancer care capacity, and expanding the use of advanced oncology medicines across major countries. WHO notes the Western Pacific region constitutes 1.9 billion people, and Merck has continued to secure new KEYTRUDA approvals in Japan, showing ongoing regional treatment expansion.

Japan Pembrolizumab Market

In 2026, Japan is estimated to achieve USD 1.46 billion, accounting for approximately 4.40% of the global market.

China Pembrolizumab Market

China is projected to be one of the largest worldwide, with 2026 revenues estimated to reach USD 2.16 billion, representing approximately 6.52% of global sales.

India Pembrolizumab Market

India will hit USD 0.51 billion in 2026, accounting for roughly 1.55% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. Latin America is set to reach a valuation of USD 1.09 billion in 2026. In Latin America the cancer burden is rising while regional health systems are placing more attention on earlier diagnosis and access to essential cancer medicines. In the Middle East & Africa, the GCC is set to reach USD 0.40 billion in 2026.

South Africa Pembrolizumab Market

The South African market is projected to reach approximately USD 0.19 billion in 2026, accounting for roughly 0.57% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations by Key Players to Propel Market Progress

The global pembrolizumab market is highly consolidated, with Merck & Co., Inc., Samsung Bioepis Co., Ltd., Sandoz AG, Celltrion, Inc., Shanghai Henlius Biotech, Inc., and Bio-Thera Solutions, Ltd. holding significant share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive their market share gains.

- For instance, in September 2025, Merck & Co., Inc. received approval from the U.S. FDA for KEYTRUDA QLEX (pembrolizumab and berahyaluronidase alfa-pmph) injection for subcutaneous administration in adults across most solid tumor indications for KEYTRUDA (pembrolizumab). Berahyaluronidase alfa is a variant of human hyaluronidase developed and manufactured by Alteogen Inc.

Other notable players include Dr. Reddy's Laboratories Ltd., Alvotech, and Biocon Biologics Limited. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY PEMBROLIZUMAB COMPANIES PROFILED

- Merck & Co., Inc. (U.S.)

- Samsung Bioepis Co., Ltd. (South Korea)

- Sandoz AG (Switzerland)

- Celltrion, Inc. (South Korea)

- Shanghai Henlius Biotech, Inc. (China)

- Bio-Thera Solutions, Ltd. (China)

- Reddy's Laboratories Ltd. (India)

- Alvotech (Iceland)

- Biocon Biologics Limited (India)

- Organon & Co. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Moderna, Inc. and Merck & Co., Inc. announced median five-year follow-up data from the Phase 2b KEYNOTE-942/mRNA-4157-P201 study, evaluating intismeran autogene (mRNA-4157 or V940). It is an investigational mRNA-based individualized neoantigen therapy (INT), in combination therapies with KEYTRUDA (pembrolizumab). It is for patients with high-risk melanoma (stage III/IV) following complete resection.

- October 2025: Merck & Co., Inc. announced results demonstrating KEYTRUDA (pembrolizumab) plus Padcev (enfortumab vedotin-ejfv) reduced the risk of event-free survival (EFS) events by 60% and reduced the risk of death by 50% when given before and after surgery (radical cystectomy) versus surgery alone, in patients with muscle-invasive bladder cancer (MIBC) who are not eligible for or declined cisplatin-based chemotherapy.

- September 2025: Shanghai Henlius Biotech, Inc. dosed the first subject for a phase 1 multi-centre clinical trial (HLX17-MRST001) of the company's independently developed investigational pembrolizumab biosimilar HLX17 (recombinant anti-PD-1 humanized antibody injection) in China. Previously, the investigational new drug (IND) applications of HLX17-MRST001 have been approved by the U.S. Food and Drug Administration (FDA) and the National Medical Products Administration (NMPA) as an adjuvant therapy for certain resected solid tumors.

- September 2025: Shanghai Henlius Biotech, Inc. received approval for an investigational new drug (IND) application from the U.S. FDA for its HLX17, a proposed pembrolizumab biosimilar developed by the company, as an adjuvant therapy for certain resected solid tumors.

- June 2025: Alvotech, a global biotech company specializing in the development and manufacture of biosimilar medicines for patients worldwide, collaborated with Dr. Reddy's Laboratories Ltd to codevelop, manufacture, and commercialize a biosimilar candidate to Keytruda (pembrolizumab) for global markets.

REPORT COVERAGE

The global market analysis includes a comprehensive study of market size and forecast across all segments covered in the report. It contains detailed information on key market dynamics, growth drivers, restraints, challenges, and emerging markets expected to influence the growth during the forecast period. It also provides insights into major clinical and commercial developments, including label expansions, new formulation advancements, regulatory approvals, and biosimilar pipeline activity. Additionally, the report covers key industry developments, including partnerships, collaborations, and competitive strategies adopted by key participants. Further, it offers a detailed competitive landscape, including market share analysis and profiles of major companies operating in the global market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 2.74% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Disease Indication, Age Group, Type, Therapy Setting, Route of Administration, End User, and Region |

| By Product Type |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Therapy Setting |

|

| By Route of Administration |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 31.70 billion in 2025 and is projected to reach USD 41.10 billion by 2034.

In 2025, North America’s market value stood at USD 16.73 billion.

The market is expected to grow at a CAGR of 2.74% over the forecast period of 2026-2034.

The KEYTRUDA IV segment is expected to lead the market.

The rising global cancer burden is supporting demand for pembrolizumab and driving market growth.

Merck & Co., Inc., Samsung Bioepis Co., Ltd., Sandoz AG, Celltrion, Inc., and Shanghai Henlius Biotech, Inc. are the major market players in the global market.

In terms of share, North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us