Personal Loans Market Size, Share & Industry Analysis, By Lender Type (Banks, Credit Unions, Online Lenders, and Peer-to-Peer Lenders), By Loan Purpose (Debt Consolidation, Home Improvement, Medical, Education, Emergency, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

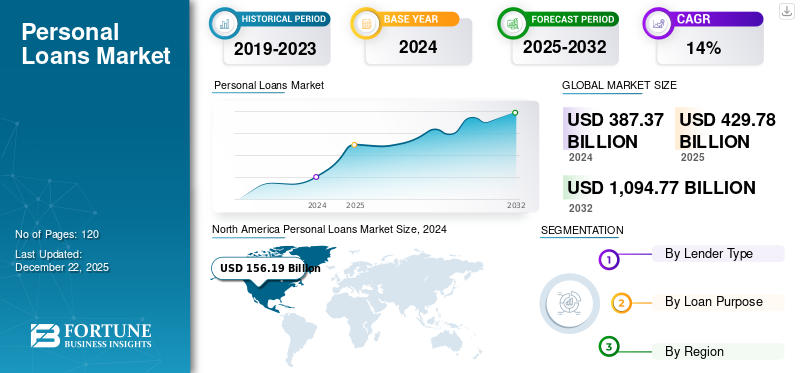

The global personal loans market size was valued at USD 429.78 billion in 2025 and is projected to grow from USD 481.18 billion in 2026 to USD 1,521.91 billion by 2034, exhibiting a CAGR of 15.50% during the forecast period. North America dominated the global market with a share of 40.10% in 2025.

The market encompasses a range of unsecured financial products that allow individuals to borrow money for various purposes without the need for collateral. These loans are typically offered by banks, credit unions, and online lenders and can be utilized for expenses such as debt consolidation, home improvements, medical bills, travel, and education. The market has seen significant growth due to factors such as changing consumer lifestyles, increasing financial needs, and the rise of digital lending platforms that simplify the application process.

Personal loan provide vital financial support by offering flexibility and quick access to funds for individuals facing unexpected expenses or planning significant purchases. They help borrowers manage their finances more effectively by consolidating high-interest debts into a single loan with lower interest rates or providing necessary funds for urgent needs such as medical emergencies or home repairs. The increasing adoption of digital platforms has made it easier for consumers to apply for a personal loan with minimal documentation and faster approvals.

Furthermore, innovative lending solutions tailored to individual credit profiles have expanded access to these types of loans, allowing a broader range of borrowers to benefit from these financial products.

The COVID-19 pandemic had a profound impact on the market, initially causing a decline in demand due to economic uncertainty and job insecurity among consumers. Many individuals turned to alternative borrowing options, such as lines of credit or secured loans, when faced with financial hardships. However, as economies began to recover and consumer confidence gradually returned, there was a resurgence in personal loan applications driven by increased spending on home renovations and debt consolidation.

The pandemic highlighted the importance of financial flexibility, leading many borrowers to rely more heavily on loans as a means of managing their finances during uncertain times.

Download Free sample to learn more about this report.

Personal Loans MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 429.78 billion

- 2026 Market Size: USD 481.18 billion

- 2034 Forecast Market Size: USD 1,521.91 billion

- CAGR: 15.50% from 2026–2034

- North America dominated the global market with a share of 40.10% in 2025.

- Banks segment is projected to dominate the market with a share of 55.16% in 2026.

- This home improvement segment is expected to gain 20% of the market share in 2025.

North American

The North America market accounted for USD 172.44 billion in 2025, representing 40.10% of the global industry, and is expected to reach USD 192.13 billion in 2026.

Europe

Europe is the second largest market estimated to be worth USD 108.57 billion in 2025, registering a CAGR of 15.74% during the forecast period (2025-2032).

Asia Pacific

In 2025, Asia Pacific represented USD 102.35 billion, accounting for 23.80% of the worldwide market, and is projected to grow to USD 116.54 billion in 2026.

U.S.

The U.S. market is estimated to gain USD 148.64 billion in 2026.

Japan

Japan is poised to acquire USD 17.09 billion in 2026.

Read More

Personal Loans Market Trends

Rise of Fintech and P2P Lending Causes Market Transformation

The market is undergoing a significant shift driven by the rise of fintech and peer-to-peer (P2P) lending platforms. These digital innovations have streamlined the borrowing process, making it more accessible and efficient. Instead of traditional banking's lengthy paperwork and approval times, online platforms now allow users to apply for loans t`with minimal documentation, meeting the growing demand for quick financial solutions. P2P lending further fuels personal loans market growth by connecting borrowers directly with investors, bypassing traditional banks and often offering lower interest rates. This democratization of lending makes these loans more attainable, especially for those who may have struggled with traditional credit access.

Looking ahead, the market growth is expected to continue as consumer preferences evolve and digital transformation deepens. The emphasis on personalization and innovation will likely result in more tailored financial products designed to meet diverse consumer needs. Concurrently, regulatory frameworks are adapting to support fintech and P2P lending, promoting fair practices and competition. As fintech continues to reshape financial services, these loans are poised to become an increasingly integral part of consumers' strategies for managing expenses and achieving their financial objectives.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Digital Transformation Drives Significant Innovation in Market

Digital transformation is a significant driver in the market, reshaping the lending landscape through the integration of advanced technologies such as Artificial Intelligence (AI), Machine Learning (ML), and big data analytics. These innovations have streamlined online application processes, allowing borrowers to complete applications with ease and receive quick approvals. This shift enhances customer experience by eliminating cumbersome paperwork and providing faster access to funds, ultimately increasing satisfaction with the lending process.

Additionally, digital platforms enable lenders to offer personalized loan products tailored to individual borrower profiles. By utilizing AI and data analytics for more accurate risk assessments, lenders can extend credit to underserved populations with limited credit histories, promoting greater financial inclusion. The automation of processes also enhances operational efficiency, reducing costs and facilitating quicker decision-making. As technology continues to evolve, it will drive further innovation in the market, creating new opportunities for both lenders and borrowers while reshaping consumer expectations around speed and convenience in financial services.

Market Restraints

Credit Risk Management Intensifies as Lenders Expand Portfolios in Uncertain Economic Conditions

Credit risk management poses a significant restraint in the market, particularly as lenders expand their portfolios amidst economic uncertainties. As the demand for loans increases, the complexity of managing credit risk intensifies. Lenders must implement robust risk assessment frameworks to mitigate potential defaults and maintain financial stability. In India, private banks are bracing for higher levels of small loan defaults until mid-2025, driven by slower economic growth. This anticipated rise in defaults necessitates scrutiny of lending practices and borrower profiles to avoid exacerbating financial risks.

Furthermore, the challenge of credit risk management can lead to cautious lending practices that may limit access to credit for certain consumer segments. Lenders, wary of the potential for increased defaults, may tighten their lending criteria or impose higher interest rates on borrowers deemed high-risk. This cautious approach can hinder financial inclusion efforts, particularly for individuals with limited credit histories or lower credit scores who are seeking loans. As a result, while the market continues to grow, the complexities of credit risk management present ongoing challenges that could restrict opportunities for both lenders and borrowers.

Market Opportunities

Government Initiatives for Financial Literacy Enhance Consumer Awareness and Increase Loan Uptake

Government initiatives aimed at enhancing financial literacy play a crucial role in educating consumers about borrowing options, ultimately leading to more informed financial decisions. Various programs, such as the National Centre for Financial Education (NCFE), have been established to promote financial education through workshops, seminars, and campaigns. These initiatives target diverse segments of the population, including youth, women, and senior citizens, ensuring that financial concepts are accessible to all. By increasing awareness of personal finance topics such as budgeting, saving, and responsible borrowing, these campaigns empower individuals to make better financial choices.

In addition to general awareness campaigns, specific initiatives such as the Financial Literacy Week organized by the Reserve Bank of India (RBI) focus on key financial concepts and products. This annual event includes public outreach programs that educate consumers on essential topics such as digital banking and debt management. By providing targeted information and resources, these initiatives help demystify financial products and services, making it easier for consumers to navigate their borrowing options. As individuals become more knowledgeable about their financial rights and responsibilities, they are more likely to engage with lending institutions confidently.

Moreover, integrating financial literacy into school curricula through initiatives such as the Money Smart School Program (MSSP) ensures that future generations are equipped with essential money management skills from an early age. By fostering a culture of financial awareness, these government-led efforts not only increase the likelihood of loan uptake but also contribute to long-term economic stability. As consumers become more financially literate, they are better positioned to avoid debt traps and leverage investment opportunities, ultimately leading to a more informed and financially secure population.

SEGMENTATION ANALYSIS

By Lender Type

Owing to Established Trust and Comprehensive Services, Banks Dominate Market Share

By lender type, the market is segmented into banks, credit unions, online lenders, and peer-to-peer lenders. A diverse array of lender types characterizes the market, each playing a distinct role in shaping the landscape.

Banks segment is projected to dominate the market with a share of 55.16% in 2026, leveraging their established reputations and comprehensive range of financial products to attract consumers. They offer various options, often accompanied by competitive interest rates and favorable loan terms. Additionally, banks benefit from their extensive branch networks and customer trust, which contribute to their dominant position in the market. However, as consumer preferences shift toward more convenient and accessible lending solutions, banks face increasing pressure to adapt and innovate.

Credit unions, while smaller in market share compared to banks, provide an attractive alternative due to their member-focused approach and lower interest rates. They often cater to specific communities or groups, fostering loyalty among their members. This segment held 56% of the market share in 2025.

On the other hand, online lenders are experiencing the highest compound annual growth rate (CAGR) in the market, driven by technological advancements and changing consumer behaviors. These digital platforms provide streamlined application processes, quick approvals, and personalized loan offerings that appeal to tech-savvy borrowers seeking efficiency. Peer-to-peer (P2P) lending is also gaining traction as it connects borrowers directly with investors, often resulting in lower interest rates and more flexible terms.

As these alternative lending models continue to grow, they challenge traditional banks by offering competitive advantages that cater to evolving consumer needs. This dynamic interplay between established banks and emerging online lenders illustrates the ongoing transformation within the market.

To know how our report can help streamline your business, Speak to Analyst

By Loan Purpose

Owing to Diverse Loan Purposes, Debt Consolidation Holds Highest Market Share

By loan purpose, the market is segmented into debt consolidation, home improvement, medical, education, emergency, and others.

The market caters to a variety of loan purposes, each reflecting different consumer needs and economic factors. Debt consolidation currently holds the highest market share, as many individuals seek to streamline their finances by combining multiple debts into a single, more manageable loan.

Home improvement is another significant application, with homeowners utilizing loans to fund renovations, repairs, or upgrades to their properties. This segment is expected to gain 20% of the market share in 2025.

Personal loans are also commonly used for education expenses, covering tuition fees, books, and other related costs.

Medical expenses represent another important segment, addressing unforeseen healthcare costs or elective procedures.

Emergency expenses are projected to have the highest compound annual growth rate in the coming years, reflecting the increasing need for immediate financial assistance to handle unexpected crises.

The "others" category encompasses various loan purposes, including weddings, vacations, and large purchases, highlighting the versatility of loans in meeting diverse consumer needs.

Debt consolidation segment is projected to dominate the market with a share of 32.99% in 2026 is likely to grow with a considerable CAGR of 13.26% during the forecast period (2026-2034).

PERSONAL LOANS MARKET REGIONAL OUTLOOK

The market covers five major regions, mainly North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Personal Loans Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 172.44 billion in 2025, representing 40.10% of the global industry, and is expected to reach USD 192.13 billion in 2026. The North American market dominates the global landscape, driven by strong consumer demand, diverse financial needs, and a robust financial infrastructure. Banks, holding the largest market share, anchor this dominance with reliable and secure lending options, providing stability and trust for consumers. The integration of digital lending platforms has amplified the region’s leadership, enhancing accessibility and enabling borrowers to secure loans quickly and conveniently.

Intensified promotional and marketing efforts have further boosted consumer awareness, fueling market growth. Supported by rising consumer spending and the increasing digitalization of financial services, North America’s market continues to expand, effectively catering to a broad audience, including underserved populations, solidifying its position as the leading region in the market.

The personal loans market share in the U.S. is significantly influenced by its large population and diverse borrowing needs. The country boasts a well-established banking system, which is increasingly complemented by a growing number of fintech firms, providing consumers with a wide array of loan products tailored to their specific requirements. The rapid adoption of digital lending platforms has transformed the way individuals access personal loans, enabling quicker application processes and immediate approvals.

Economic factors, such as elevated consumer spending levels, further enhance the demand for loans, making them a popular financial solution for various purposes, including debt consolidation and emergency expenses. As lenders continue to innovate and adapt their offerings, the U.S. remains at the forefront of the market share, reflecting its dynamic landscape where traditional banks and fintech firms coexist and compete effectively. The U.S. market is estimated to gain USD 148.64 billion in 2026.

Download Free sample to learn more about this report.

Europe

To know how our report can help streamline your business, Speak to Analyst

Europe is the second largest market estimated to be worth USD 108.57 billion in 2025, registering a CAGR of 15.74% during the forecast period (2025-2032). In Europe, the market is experiencing steady growth, influenced by varying economic conditions across different countries. The market is characterized by a mix of traditional banks and emerging fintech companies that are reshaping the lending landscape. While countries such as Germany and the U.K. dominate the market due to their strong financial systems, southern European nations are seeing an increase in demand for loans as economic recovery progresses.

The U.K. market is foreseen to grow with a value of USD 25.35 billion in 2026. Regulatory frameworks in Europe also play a crucial role in shaping lending practices, ensuring consumer protection while fostering competition among lenders. The growing acceptance of online lending platforms is expected to drive further expansion in the region as consumers seek more convenient borrowing options. Germany is poised to reach USD 27.32 billion in 2026, while France is set to hold USD 15.86 billion in the same year.

Asia Pacific

In 2025, Asia Pacific represented USD 102.35 billion, accounting for 23.80% of the worldwide market, and is projected to grow to USD 116.54 billion in 2026. The Asia Pacific region is poised for significant growth in the market, driven by rising disposable incomes and increasing consumer awareness of financial products. Countries such as India and China are witnessing a surge in demand for loans as more individuals seek financing for various purposes such as education, home improvement, and debt consolidation. China is poised to gain USD 38.18 billion in 2025.

The rapid digitalization of financial services has also made loans more accessible to a broader demographic, particularly among younger consumers who are comfortable using technology for their financial needs. As fintech companies continue to innovate and offer competitive loan products, the region is expected to experience the highest CAGR in the coming years. India is set to reach a market value of USD 30.14 billion in 2026, while Japan is poised to acquire USD 17.09 billion in 2026.

South America

South America is the fourth largest market set to reach a market value of USD 30.45 billion in 2025. In South America, the market is gradually expanding as economic conditions improve and consumer confidence rises. Countries such as Brazil and Argentina are seeing increased demand for loans as individuals seek to finance personal projects or manage unexpected expenses. However, challenges such as high inflation rates and economic volatility can impact borrowing behaviors and lender confidence. Traditional banks remain dominant in this region; however, fintech companies are beginning to penetrate the market with innovative lending solutions that cater to tech-savvy consumers. As financial literacy initiatives gain traction, there is potential for greater acceptance of loans among underserved populations.

Middle East & Africa

Middle East & Africa contributed 3.70% to the global market in 2025, with a valuation of USD 15.97 billion, and is projected to reach USD 17.34 billion in 2026. The market in the Middle East & Africa is evolving, with a growing emphasis on financial inclusion and access to credit. In many countries within this region, traditional banking systems have historically limited access to personal loans; however, recent efforts by governments and financial institutions aim to lending practices. The rise of fintech companies has introduced alternative lending solutions that appeal to younger consumers seeking quick access to funds. As economic development continues and regulatory frameworks improve, there is potential for significant growth in the market across various countries in this region. The GCC market is expected to stand at USD 4.88 billion in 2025.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Presence of Major Global Players and Strategic Partnerships in Market Drives Innovation and Growth

The market is characterized by a mix of traditional banks and fintech companies, each influencing the competitive landscape with distinct strategies. Major banks such as Wells Fargo, Barclays, and American Express leverage their established reputations and extensive networks to offer a variety of personal loan products at competitive personal loan rates. They are increasingly adopting digital solutions to enhance customer experiences and streamline processes. Conversely, fintech firms such as SoFi, LendingClub, and Avant are reshaping the market through technology-driven solutions that utilize advanced data analytics for assessing creditworthiness. These platforms provide quick approvals and cater to a tech-savvy consumer base seeking convenience.

In the Asia Pacific region, companies such as Ant Financial and WeBank focus on underbanked populations, expanding access to personal loans. The collaboration between traditional banks and fintech is likely to grow, enhancing product offerings. The average personal loan balance has risen significantly, driven by consumer demand for quick financial solutions, particularly for debt consolidation. Many individuals use loans to cut rates on high-interest credit cards into manageable monthly payments. Federal Reserve policies also play a crucial role in shaping borrowing costs and market dynamics. As personal loan balances increase, the interplay between traditional lenders and fintech innovations will continue to define the sector's future.

List of Key Personal Loan Companies Profiled:

- JPMorgan Chase (U.S.)

- Bank of America (U.S.)

- Wells Fargo (U.S.)

- Citigroup (U.S.)

- HSBC Holdings (U.K)

- Avant, LLC (U.S.)

- Goldman Sachs (U.S.)

- American Express (U.S.)

- Barclays (U.K)

- LendingClub (U.S.)

- SoFi (U.S.)

- UBS Group AG (Switzerland)

- Credit Suisse Group AG (Switzerland)

- ING Group (Netherlands)

- Mizuho Financial Group (Japan)

- Sumitomo Mitsui Trust Holdings (Japan)

- Rabobank (Netherlands)

- Royal Bank of Canada (Canada)

- Deutsche Bank AG (Germany)

- Ant Financial (China)

- WeBank (China)

KEY INDUSTRY DEVELOPMENTS:

- October 2024: JPMorgan Chase partnered with Cliffwater, FS Investments, and Shenkman Capital Management to expand its presence in the USD 1.7 trillion private credit market. As part of the collaboration, JPMorgan will originate loans and invest alongside these direct lenders, who will have limited discretion to decline participation in transactions over a specified period. JPMorgan has allocated over USD 10 billion from its balance sheet to support this effort. It aims to regain market share lost to private credit players, aligning with similar strategies by other banks such as Citigroup and Wells Fargo.

- September 2024: Mercado Libre, the Argentine e-commerce platform, obtained a USD 250 million credit line from JPMorgan over three years. As part of the deal, JPMorgan will acquire personal and business loans from Mercado Libre's credit portfolio. Mercado Libre intends to use these funds to broaden its credit offerings for SMEs and personal loan in Mexico through its fintech division, Mercado Pago.

- July 2024: Navi Finserv, the NBFC arm of Navi Technologies, secured a USD 38 million personal loan securitization deal with J.P. Morgan, marking the latter's entry into India's digital lending sector. The transaction involves pass-through certificates (PTC) backed by a pool of unsecured personal loan, with Navi Finserv planning to use the funds to expand its personal loan business. J.P. Morgan aims to strengthen its ties with innovative companies in India through this partnership.

- September 2023: Centerbridge Partners and Wells Fargo established a strategic relationship to focus on direct lending to non-sponsor middle-market companies in North America. Centerbridge plans to launch Overland Advisors to manage a new business development company targeting senior secured loans, to raise at least USD 5 billion in investable capital.

- November 2022: Wells Fargo launched Flex Loan, a digital-only, small-dollar loan designed to provide eligible customers with convenient and affordable access to funds for short-term cash needs. Accessible through the Wells Fargo Mobile Banking app, Flex Loan offers a transparent and affordable way to manage expenses, providing certainty of approval, quick access to funds, and clarity on costs.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.50% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

Lender Type, Loan Purpose, and Region |

|

Segmentation |

By Lender Type

By Loan Purpose

By Region

|

|

Companies Profiled in the Report |

JPMorgan Chase (U.S.), Bank of America (U.S.), Wells Fargo (U.S.), Citigroup (U.S.), HSBC Holdings (U.K), Goldman Sachs (U.S.), Barclays (U.K), Deutsche Bank AG (Germany), Ant Financial (China), and American Express (U.S.). |

Frequently Asked Questions

The market is projected to reach USD 1,521.91 billion by 2034.

In 2025, the market was valued at USD 429.78 billion.

The market is projected to grow at a CAGR of 15.50% during the forecast period.

By lender type, the banks segment leads the market.

Digital transformation drives significant innovation is the key factor driving market growth.

JPMorgan Chase, Bank of America, Wells Fargo, Citigroup, and Barclays are the top players in the market.

North America is expected to hold the highest market share.

By loan purpose, emergency is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us