Pharmaceutical Membrane Filtration Market Size, Share & Industry Analysis, By Products (Membrane Filters {Polyethersulfone (PES) Filters, Polyvinylidene Fluoride (PVDF) Filters, Polytetrafluoroethylene (PTFE) Filters, Nylon Filters, and Others}, Filtration Systems, and Consumables & Others), By Technique (Microfiltration, Ultrafiltration, Nanofiltration, and Others), By Usage (Single Use and Reusable), By Scale (R&D Scale, Pilot-scale, and Commercial Scale), By Application (Final Product Processing, Raw Material Filtration, & Virus Filtration), By End User, and Regional Forecast, 2026-2034

Pharmaceutical Membrane Filtration Market Size and Future Outlook

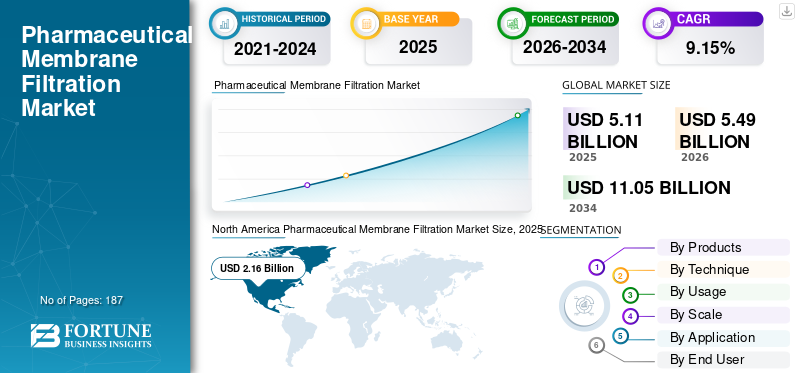

The global pharmaceutical membrane filtration market size was valued at USD 5.11 billion in 2025. The market is projected to grow from USD 5.49 billion in 2026 to USD 11.05 billion by 2034, exhibiting a CAGR of 9.15% during the forecast period. North America dominated the global pharmaceutical membrane filtration market with a market share of 42.27% in 2025.

The pharmaceutical membrane filtration is an important purification and separation technology that is widely used by end users to ensure product sterility, clarity, and quality. This marketspace is anticipated to witness significant growth over the study period, owing to the increasing demand from the biopharmaceutical industry for manufacturing biologics and biosimilars. In addition, to maintain a competitive edge, various key players are focusing on strategic activities such as collaborations and acquisitions to enhance product offerings.

Furthermore, the market is dominated by several key players, with Merck KGaA and Sartorius AG occupying the leading positions. Advanced technology integration and strengthening product offerings through collaborations further enhance the positions of these companies in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rapid Expansion of Biologics & Biosimilars Manufacturing to Boost the Market Growth

The rapid expansion of biologics & biosimilars manufacturing is one of the key factors driving global market growth. Biologics, including Monoclonal Antibodies (mAbs), recombinant proteins, hormones, vaccines, and advanced therapies, require filtration-intensive purification and sterile processing workflows, far exceeding the filtration needs of conventional small-molecule drugs. With biologics accounting for a significant share of new global drug approvals and biosimilars expanding rapidly across emerging and regulated markets, the demand for high-throughput, high-performance membrane filtration systems is growing at an accelerated pace. Additionally, the expansion of manufacturing capabilities by key players also boosts the market growth.

- For instance, in September 2025, Merck launched a USD 161.81 million filter manufacturing facility in Ireland. This production plant is aimed at strengthening the company’s in-region-for-region supply resilience.

MARKET RESTRAINTS:

High Operational and Capital Costs to Restrict Market Expansion

One of the most significant challenges restraining the global gf membrane filtration market growth is the high capital investment and operational cost associated with advanced filtration systems. Pharmaceutical and biotechnology companies, especially smaller firms, emerging manufacturers, and those in developing markets, face substantial financial barriers when adopting state-of-the-art membrane filtration technologies. Owing to this, the market is expected to experience limited growth to a certain extent.

- For instance, several mid-sized biologics manufacturers in India and Latin America have reported delays in integrating high-capacity UF/DF skids.

MARKET OPPORTUNITIES:

Capacity Expansion in Asia Pacific Region to Offer Lucrative Growth Opportunities

The Asia Pacific region represents one of the most significant growth opportunities in the market. Over the past few years, the region has been transforming into a global biologics manufacturing hub, driven by substantial R&D investments, supportive regulatory frameworks, and rapidly expanding domestic pharmaceutical industries. Countries such as China, South Korea, Singapore, and India have implemented strategic initiatives to develop advanced bio manufacturing ecosystems. This includes constructing new biologics production plants, expanding vaccine manufacturing capacity, developing CDMO facilities, and upgrading bioprocessing infrastructures. This has resulted in an increasing demand for upstream and downstream membrane filtration technologies, in turn creating lucrative growth opportunities for pharmaceutical membrane filtration.

- · For instance, Samsung Biologics, Wuxi Biologics are some of the leading CDMOs in the Asia Pacific region that have expanded their capabilities to fulfill the growing market demands.

PHARMACEUTICAL MEMBRANE FILTRATION MARKET TRENDS:

Increasing Adoption of Single-Use Technologies (SUTs) is a Prominent Global Market Trend

The market is witnessing a strong and sustained shift toward Single-Use Technologies (SUTs), which has emerged as one of the prominent trends in the market. Pharmaceutical and biotechnology manufacturers increasingly prefer disposable, pre-assembled, and gamma-sterilized filtration solutions over traditional stainless-steel, reusable systems due to their versatility, operational efficiency, and compliance benefits. Due to their increasing adoption among end users, major players are expanding their single-use filtration portfolios, thereby supporting the global pharmaceutical membrane filtration growth.

For instance, Thermo Fisher Scientific Inc., Merck KGaA, Cytiva (Danaher), and Sartorius AG are some of leading players in the market that offer single use membrane filtration products.

MARKET CHALLENGES:

Slow Adoption of Advanced Technologies in Developing Regions Poses a Significant Challenge for Market Growth

One of the major challenges in the global market for pharmaceutical membrane filtration is the slow adoption of advanced technologies in developing regions. While these regions are expanding their pharmaceutical production capabilities, many facilities continue to rely on basic microfiltration systems, older reusable filtration units, and limited-scale clarification technologies, rather than transitioning to modern ultrafiltration/diafiltration (UF/DF), virus filtration, or single-use filtration systems used widely in developed countries. This slow adoption is due to high capital requirements, a lack of skilled personnel, and other factors.

For example, several Indian vaccine and biosimilar manufacturers reported delays in adopting high-throughput virus filtration systems due to high cost, technical complexities, and supply chain disruptions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Products

Rising Need for Sterilization-grade Filtration amid Strict Regulations Drives Membrane Filters Segment Growth

Based on products, the market is classified into membrane filters, filtration systems, and consumables & others.

The membrane filters segment held the largest global pharmaceutical membrane filtration market share in 2025. These filters are increasingly used for sterilization-grade filtration. The strict regulation necessitates the need for high microbial control in sterile manufacturing processes, driving the adoption of advanced membrane filtration systems.

· For instance, in April 2024, Asahi Kasei started selling a membrane system to produce WFI (water for injection), a type of sterile water filtration used for the preparation of injections.

On the other hand, the filtration systems is the fastest-growing segment and is expected to record the highest CAGR of 9.83% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technique

Broad Use across Bioprocessing Workflows and Raw Material Handling Drives the Microfiltration Segment Expansion

In terms of technique, the market is categorized into microfiltration, ultrafiltration, nanofiltration, and others.

The microfiltration segment led the market, accounting for the largest share in 2025. The segment is anticipated to dominate with a 43.9% share in 2026. This growth is driven by its broad applicability of microfiltration across upstream and downstream bioprocessing workflows, making it the most frequently used technique in pharmaceutical manufacturing. In addition, microfiltration is widely used in raw material processing, a foundational requirement for upstream bioprocessing. The high frequency and repetition of these steps in both clinical and commercial manufacturing cycles significantly increase total membrane consumption. This contributes to the segment’s leading market position.

For instance, in August 2023, Merck KGaA expanded its filtration media and membrane production capabilities to support increased demand for upstream and clarification-related microfiltration products.

The nanofiltration segment is expected to grow at a CAGR of 9.81% over the forecast period.

By Usage

Advantages of Single Use Products to Lead the Growth of the Segment

On the basis of usage, the market is divided into single use and reusable.

In 2025, the single use segment held the dominant position in the global market. The segment is anticipated to dominate with a 55.3% share in 2026. This growth is attributed to the widespread adoption of flexible, contamination-free, and cost-efficient bioprocessing workflows globally across biopharmaceutical and vaccine manufacturing. Single-use filtration products have become essential components in modern bioprocess facilities due to their operational convenience and regulatory advantages. Additionally, growing investments in single-use bioprocessing systems, along with expansions of biologics manufacturing capacity, have also contributed to the dominant market position of this segment.

For instance, in October 2023, Thermo Fisher Scientific Inc. announced an expansion of its single-use technologies manufacturing capacity in the U.S. and Europe, including increased production of single-use filtration assemblies and sterilizing-grade disposable modules.

The reusable segment is expected to grow at a CAGR of 7.09% over the forecast period.

By Scale

Surge in Commercial Manufacturing to Lead the Growth of the Segment

Based on scale, the market is categorized into R&D scale, pilot scale, and commercial scale.

The commercial segment accounted for the largest market share in 2025. The segment is anticipated to dominate with a 51.0% share in 2026. This growth is driven by the rapid expansion of large-scale biologics, biosimilars, vaccines, and advanced therapy manufacturing, which require high-capacity, GMP-compliant filtration systems, contributing to the dominance of the segment over the study period. Additionally, the expansion of commercial GMP production sites by key companies also supports the segment growth.

For instance, in June 2023, Samsung Biologics expanded its commercial biologics manufacturing capabilities by initiating the construction of a new large-scale manufacturing plant in South Korea.

The R&D segment is expected to grow at a CAGR of 7.25% over the forecast period.

By Application

Rising Sterility Requirements in Biopharmaceutical and Injectable Production Drives Final Product Processing Segment Growth

In terms of application, the market is categorized into final product processing, raw material filtration, virus filtration, cell separation, and others.

The final product processing segment captured the leading share of the market in 2025. The segment is anticipated to dominate with a 39.8% share in 2026. This dominance is primarily attributed to the critical role of sterile filtration in the final stages of drug manufacturing, particularly in the production of biopharmaceuticals, vaccines, recombinant proteins, and injectable therapies. As these products must meet stringent sterility and purity standards before fill–finish operations, final product processing relies heavily on 0.22 µm sterilizing-grade membranes, virus removal filters, and high-performance PES/PVDF membranes. Additionally, ongoing investments by major biopharmaceutical companies in new fill–finish facilities, single-use sterile filtration systems, and automated integrity testing platforms strengthen the segment’s contribution to global market growth.

For instance, in May 2023, Merck KGaA expanded its life science manufacturing capabilities in the U.S. and Europe, including upgrades to sterilizing-grade filtration and single-use system production.

The virus filtration segment is expected to grow at a CAGR of 11.73% over the forecast period.

By End User

Increasing Focus on Biopharmaceutical Manufacturing Activities to Drive the Pharmaceutical & Biotechnology Companies Segmental Growth

In terms of end user, the market is categorized into pharmaceutical & biotechnology companies, CROs & CDMOs, academic & research institutes, and others.

The pharmaceutical & biotechnology companies segment accounted for the largest market share of the pharmaceutical membrane filtration in 2025 and is expected to maintain its dominance in 2026 with an estimated 59.3% share. This leading position is primarily driven by an extensive use of membrane filtration technologies across biologics, vaccines, cell & gene therapies, and advanced therapeutic manufacturing workflows. Moreover, leading pharmaceutical and biotechnology companies continue to expand manufacturing capacities, advance production lines, and invest in single-use and automated filtration technologies to support scalable, flexible, and contamination-free operations. Such strategic investments directly amplify the demand for pharmaceutical membrane filtration solutions.

For instance, in July 2023, Sartorius AG added a cell culture media manufacturing facility in Puerto Rico. The facility expanded the company’s cell culture media capacities. Such developments are needed to ensure the segment's growth.

The CROs & CDMOs segment is expected to grow at a CAGR of 12.31% over the forecast period.

Pharmaceutical Membrane Filtration Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Pharmaceutical Membrane Filtration Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 2.02 billion, and maintained its leading position in 2025, with a value of USD 2.16 billion. The region is anticipated to dominate the global market due to the increasing focus of biopharmaceutical companies on the manufacturing activities of biologics and biosimilars. The increased production of biopharmaceuticals is expected to drive the North America’s market growth. In 2026, the U.S. market is estimated to reach USD 2.14 billion. Additionally, operating companies in the region are launching new products, in turn boosting the market growth.

For instance, in November 2021, DuPont Water Solutions (DWS) introduced DuPont TapTec LC HF-4040 Reverse Osmosis (RO) membrane filter in the market for pharmaceutical membrane filtration.

Europe and Asia Pacific

Regions, such as Europe and the Asia Pacific, are expected to experience notable growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 8.80%, which is the second highest among all regions, and reach a valuation of USD 1.47 billion by 2026. This can be attributed to the increasing manufacturing capabilities of operating players in the region, leading to a growing demand for filtration solutions. Backed by these factors, the U.K. is expected to record valuation of USD 0.33 billion, Germany USD 0.30 billion, and France USD 0.24 billion in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 1.26 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are estimated to reach USD 0.23 and USD 0.39 billion respectively in 2026.

Latin America and the Middle East & Africa

Over the forecast period, the Latin America and the Middle East & Africa regions are likely to witness reasonable growth in this market space. The Latin America market is set to reach a valuation of USD 0.25 billion in 2026. The increasing focus of global companies on Latin American countries to enhance pharmaceutical self-sufficiency is expected to further drive growth in these regions. In addition, the increasing research and development activities in the Middle East & Africa region, especially in the GCC, are anticipated to drive the regional market growth. The GCC market captured a value of USD 0.08 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Collaborations and Portfolio Expansion Supported the Leading Position of Key Companies

The global market for pharmaceutical membrane filtration is moderately concentrated, with a few multinational companies accounting for a major share of the industry. These key players focus on membrane innovation, advanced filtration systems, automation, and single-use technologies. Their leadership is reinforced by strong geographical presence, strong customer relationships across end users, and consistent investment in portfolio diversification.

Danaher Corporation, Merck KGaA, and Sartorius AG are some of the significant players in the market. These companies are increasingly adopting strategic partnerships, acquisitions, and technology-integration initiatives to strengthen their competitive position and meet the growing demand for high-performance filtration solutions.

For instance, in June 2024, Danaher’s Cytiva business expanded its filtration manufacturing capacity across the U.S. and Europe to support the rising global demand for sterile and UF/DF membranes used in biologics and mRNA therapeutics.

Apart from this, other prominent players in the market include 3M, Repligen Corporation, Thermo Fisher Scientific Inc., and others. These companies are undertaking various strategic initiatives such as investments in R&D to enhance their market presence.

LIST OF KEY PHARMACEUTICAL MEMBRANE FILTRATION COMPANIES PROFILED:

- Danaher Corporation. (U.S.)

- Merck KGaA (Germany)

- Sartorius AG (Germany)

- 3M (U.S.)

- Repligen Corporation (U.S.)

- Parker Hannifin Corp (U.S.)

- Eaton (Ireland)

- Thermo Fisher Scientific Inc. (U.S.)

- Cytiva (U.S.)

- Avantor, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Merck KGaA acquired the chromatography business of JSR Life Sciences. The acquisition aimed to strengthen company’s downstream process offering of advanced filtration and chromatography solutions.

- July 2025: Repligen Corporation collaborated with Novasign to integrate Novasign’s machine-learning modeling workflow into Repligen’s TFF/filtration systems, advancing digitalization in filtration equipment.

- April 2025: Amazon Filters launched a new suite of pharmaceutical-grade membrane filters and housings tailored for API, sterile products, and high-potency APIs at INTERPHEX show in New York, U.S.

- February 2025: Thermo Fisher Scientific Inc. announced its plans to acquire the filtration/purification business of Solventum for approximately USD 4.1 billion, thereby significantly expanding its bioprocess filtration portfolio.

- January 2025: Toray Industries, Inc. announced the development of high-efficiency separation membrane module for biopharmaceutical manufacturing processes.

REPORT COVERAGE

The global market analysis provides a comprehensive study of market size and forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It also provides overviews of technological advancements, product development, key industry developments, mergers and acquisitions, and strategic insights into market growth. The market forecast report also encompasses a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Global Pharmaceutical Membrane Filtration Market Scope | |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.15% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Products

By Technique

By Usage

By Scale

By Application

By End User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.11 billion in 2025 and is projected to reach USD 11.05 billion by 2034.

In 2025, the market value stood at USD 2.16 billion.

The market is expected to exhibit a CAGR of 9.15% during the forecast period of 2026-2034.

The membrane filters segment led the market in terms of products in 2025.

The increasing biologics & biosimilars manufacturing to cater to increasing demand for innovative therapies is a key factor driving the market.

Danaher Corporation, Merck KGaA, and Sartorius AG are some of the prominent players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us