Pharmacy Benefit Management Market Size, Share & Industry Analysis, By Service (Specialty Pharmacy Services, Benefit Plan Design & Administration, Pharmacy Claims Processing, Formulary Management, and Others), By Service Provider (Insurance Companies, Retail Pharmacies, and Standalone PBMs), and Regional Forecast, 2026-2034

Pharmacy Benefit Management Market Size Overview

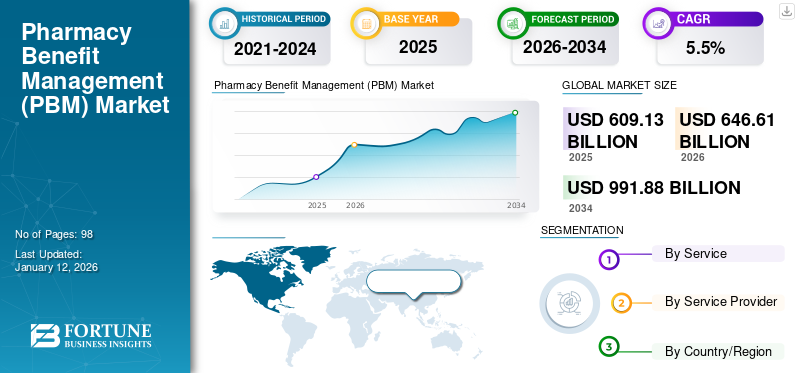

The global pharmacy benefit management market size was valued at USD 609.13 billion in 2025 and is projected to grow from USD 646.61 billion in 2026 to USD 991.88 billion by 2034, exhibiting a CAGR of 5.5% during the forecast period. U.S dominated the pharmacy benefit management market with a market share of 96.96% in 2024.

Pharmacy benefit management companies exist among insurance providers, pharmacy stores, and drug manufacturers. They negotiate with drug manufacturers and retail pharmacies to manage generic and branded drug spending. The rising prevalence of chronic diseases and increasing healthcare expenditure in developed and emerging countries are resulting in the growing demand for cost management of prescription drugs. This leads to a boost in demand for these services in the global market.

Download Free sample to learn more about this report.

PHARMACY BENEFIT MANAGEMENT MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 609.13 billion

- 2026 Market Size: USD 646.61 billion

- 2034 Forecast Market Size: USD 991.88 billion

- CAGR: 5.5% from 2026–2034

- U.S. dominated the market with a 96.96% share in 2024.

- The Specialty Pharmacy Services segment is projected to hold the largest market share 35.95% in 2026.

- The Insurance Companies segment is projected to account for the largest market share 78.31% in 2026.

North America

Driven by a large insured population, favorable regulations, and the strong presence of pharmacy benefit managers, with the U.S. market projected to reach USD 626.47 billion in 2026.

Asia Pacific

Growth is driven by rising healthcare spending, digitalization, and expanding insurance coverage.

Europe

Growth is supported by advanced healthcare infrastructure, favorable regulations, and increasing adoption of digital health solutions.

U.S.

The market is projected to reach USD 626.47 billion in 2026, supported by favorable government policies and more than 270 million Americans served by PBM companies.

Japan

Growth is supported by increasing healthcare digitalization, rising prescription drug utilization, expanding pharmaceutical reimbursement programs, and demand for efficient pharmacy benefit management solutions.

Read More

Drug price inflation has recently impacted healthcare spending, increasing the adoption of these services among health insurance providers. Hence, the rising prevalence of chronic diseases and drug price inflation have been instrumental in propelling the pharmacy benefit management market growth.

- For instance, according to a research report by KAISER FAMILY FOUNDATION, the drug cost of around 17.0% of the total Medicare Part D and Part B drugs increased by more than 7.5% in 2020 compared to the previous year.

Thus, a significant increase in drug cost is fueling the demand and adoption of Pharmacy Benefit Management (PBM) services and is expected to further augment the market growth during the forecast period.

The COVID-19 pandemic had a positive impact on the global market. The higher price of the COVID-19 vaccine and specialty drugs increased the demand for pharmacy benefit management services, leading to a significant increase in the revenue of major players. However, due to the completion of vaccination drives in the majority of the countries, along with the availability of a wide range of medication at a lower price, the revenue of key companies operating in the market returned to the pre-pandemic level by 2021 and 2022.

Pharmacy Benefit Management Market Trends

Increasing Adoption of Machine Learning to Smoothen Workflow Boosts Market Growth

The rising adoption of pharmacy benefit management services among insurance providers, retail pharmacy chains, and drug manufacturers is shifting the preference of service providers from conventional workflow to advanced workflow by utilizing machine learning. As a result, the companies can provide a streamlined supply chain, quick mail order delivery, and cater to many insurance and retail pharmacy chains within a short period.

For instance, CAPITAL RX, a prominent player in the U.S., utilizes Machine Learning (ML) and Artificial Intelligence (AI) algorithms to reduce human error and time for claim processing. Thus, the integration of ML and AI technology into the workflow is leveraging the companies to reduce medical costs and increase the efficiency of the coverage procedures.

Moreover, machine learning (ML) algorithms can analyze vast amounts of data to identify suspicious claims patterns, potentially saving billions of dollars in fraudulent spending costs. Furthermore, they can help analyze patient data to recommend the most effective medications based on individuals, improving treatment outcomes and reducing costs.

- For instance, in January 2023, Optum Rx Price Edge was designed for buyers to find the best price, whether on or off the pharmacy benefit. This advanced offering compares a member’s on-benefit cost-share with the prices available via discount cards.

Download Free sample to learn more about this report.

Pharmacy Benefit Management Market Growth Factors

Increasing Pharmaceutical Expenses to Drive Market Growth

The global population's rising prevalence of chronic diseases is increasing the demand for treatment options. As a result, numerous large pharmaceutical companies are concentrating on developing high-cost branded medications to treat chronic diseases. This led to an increase in pharmaceutical spending significantly in the past few years.

- For instance, according to a report published by Pharmaceutical Technology, drug prices in the U.S. increased by 4.0% in 2021, breaking a trend of a slow rise in previous years. According to the SingleCare Administrators, the price of individual prescription drugs will increase by 5% in 2021.

This, along with an increasing number of prescription filings in recent years for a wide range of chronic diseases, including cardiovascular diseases, chronic lung diseases, and others, is increasing healthcare expenditure. For instance, according to a survey report by SingleCare Administrators in 2022, an estimated 4 billion prescriptions are dispensed each year in the U.S. and is further expected to experience a significant hike in the prescription filing count within a few years.

Moreover, the expensive and complex medications require specialized handling and management, which PBMs are equipped to provide. Thus, a significant rise in drug cost, along with an increase in the number of prescription filing globally, is leading to an increase in the health care burden. This has resulted in increased demand and adoption for these services to reduce drug costs, manage pharmaceutical spending, and aid market expansion during the forecast period.

RESTRAINING FACTORS

Lack of Transparency in Profit Earnings Responsible for Restricting Adoption

Increasing drug spending and growing prescription filing globally are key factors driving market growth. However, various transparency issues associated with pharmacy benefit management business practices are always a concern in pharmacy benefit management services. The revenue sources of these services are rarely disclosed to the insurance providers, retail pharmacy units, or drug manufacturers. As a result, a large proportion of drug costs goes to the service providers.

- For instance, a research article by Berkeley Research Group in January 2022 reported that more than half of total spending on brand medicines goes to the supply chain, including pharmacy benefit managers, rather than the drug manufacturers.

Thus, drug manufacturers and insurance providers are experiencing a significant decrease in profit. As a result, most insurance providers abandon collaborating with PBMs, while those who have, feel reluctant. Hence, the adoption rate of these services is reducing and is anticipated to hinder market growth during the forecast period.

Pharmacy Benefit Management Market Segmentation Analysis

By Service Analysis

Rising Demand for Specialty Medicines Resulted in Segmental Dominance

By service, the market is segmented into specialty pharmacy service, benefit plan design & administration, pharmacy claims processing, formulary management, and others. The specialty pharmacy services segment is projected to dominate the market with a share of 35.95% in 2026. The rising prevalence of chronic and rare diseases increased the demand for treatment options such as specialty drugs. However, high-priced drugs are unaffordable for the majority of the patient population, leading to the growing demand for these services to decrease the price of specialty drugs to an affordable range. In addition, the development of innovative drugs further increases the demand for specialty pharmacy services that offer newer treatment options. The growing demand for specialty drugs is driving the specialty pharmacy services segment growth.

The benefit plan design & administration segment is expected to grow with the highest CAGR during the forecast period due to increasing number of patients opting for medical insurance coverage and benefit plan design for their medical treatment. According to the Centers for Medicare and Medicaid Services (CMS) Medicare Advantage Enrollment Files, 30.8 million people in the U.S. were enrolled in a Medicare Advantage plan, which accounted for 51.0% of the eligible Medicare population in 2023.

To know how our report can help streamline your business, Speak to Analyst

By Service Provider Analysis

Consolidation Between Insurers and Service Providers Led to Major Dominance of Insurance Companies Segment

Based on service provider, the market is divided into insurance companies, retail pharmacies, and standalone PBMs. The insurance companies segment will account for 78.31% market share in 2026. An increasing number of mergers and acquisitions between insurance companies and pharmacy benefit management service providers leads to segmental dominance during the forecast period. Furthermore, the rise in number of individuals covered by commercial insurance is also expected to boost the segment growth during the forecast period.

- For instance, in October 2021, First Medical Health Plan, Inc. renewed and extended its partnership with Abarca Health LLC. for pharmacy benefit management services for an additional three years with a novel financial model.

The retail pharmacies segment is anticipated to grow with the highest CAGR during the study period. An increasing number of retail pharmacy units and the entrance of big companies, including Amazon & Walmart into the retail pharmacy chain are some of the major key factors attributed to the rapid growth of the segment.

REGIONAL INSIGHTS

U.S Pharmacy Benefit Management Market Size, 2026 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market size in the U.S. stood at USD 626.47 billion in 2026. The presence of a large patient population under medical coverage, favorable government regulations for pharmacy benefit managers, and the increasing number of pharmacy benefit managers in the country are the prominent factors for regional dominance.

- For instance, according to a report by the National Association of Insurance Commissioners, in March 2021, around 66 pharmacy benefit management companies in the U.S. served more than 270.0 million Americans.

Canada is expected to grow with the highest CAGR during the forecast period. Increasing pharmaceutical spending and a growing number of prescription filings in Canada are leading to increased demand for pharmacy benefit management services.

- For instance, according to a report by the Government of Canada, Canadian public drug plans witnessed an expenditure of USD 12.5 billion on prescription drugs in 2019-2020, an increase of 3.7%. Additionally, the expansion of the network by key market players in Canada is anticipated to foster the adoption rate of these services during the study period.

The market in the rest of the world is anticipated to grow with a significant CAGR during the forecast period. An increasing number of health awareness programs and a rising number of health plan offerings by insurance providers in Brazil and South Africa are anticipated to boost the adoption rate of pharmacy services. Therefore, this will propel the demand and adoption of pharmacy benefit management services and substantially boost market growth during 2025-2032.

Key Industry Players

Inorganic Growth Strategies by Key Players Led to Market Dominance

Major players, such as CVS Health, OptumRx, Inc., and Cigna, dominate the market. Constant focus on inorganic growth strategies, including partnership and acquisition of other players to expand the brand presence, are some of the key contributing factors to market dominance.

Prominent players, including Medimpact, Anthem, Inc., and other companies are focusing on introducing new solutions and features to expand their portfolios and increase customer reach. For instance, in September 2020, Medimpact introduced a new solution to integrate prescription discount card savings with a traditional plan. Centene Corporation and Abarca Health LLC are the other key players operating in the market.

LIST OF TOP PHARMACY BENEFIT MANAGEMENT COMPANIES:

- CVS Health (U.S.)

- Cigna (U.S.)

- OptumRx, Inc. (U.S.)

- Anthem, Inc. (U.S.)

- Centene Corporation (U.S.)

- Abarca Health LLC. (U.S.)

- Medimpact (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- December 2023 - CVS Health announced plans to launch CVS CostVantage with pharmacy benefit management services for their commercial payors in 2025 to ensure a smooth transition.

- November 2023 – OptumRx, Inc., the pharmacy benefits manager (PBM) operated by the healthcare company UnitedHealth, announced plans to move eight popular insulin products to preferred status on its standard formulary for commercially insured individuals in the U.S.

- July 2023- CVS Caremark announced a partnership with the discount drug service provider GoodRx to reduce out-of-pocket prescription costs for millions of people.

- April 2023 – Cigna’s pharmacy benefit management (PBM) unit announced the launch of a new pricing plan that will comprise precise information on rebates as pharmacy middlemen are under increased scrutiny by the U.S. lawmakers for their opaque drug pricing practices.

- December 2022 - Anthem, Inc. announced that IngenioRx, its pharmacy benefit management partner, on January 1, 2023, will join the Carelon family of companies, changing its name to CarelonRx.

- October 2022 - Cigna’s pharmacy benefit management business, Express Scripts, entered into a new strategic collaboration with Centene Corporation to increase the affordability and accessibility of prescription medications for consumers.

- January 2022 – Centene Corporation acquired Magellan Health, Inc. to provide whole-health, integrated healthcare solutions with better health outcomes at lower costs.

- November 2021 - Anthem, Inc. agreed to acquire Integra Managed Care to grow its Medicaid business and increase its network.

- April 2021 - CVS Caremark entered into a larger contract with the Government-wide Service Benefit Plan, allowing CVS Health to regain the specialty pharmacy business.

- May 2020 – Express Scripts introduced a new program, Express Scripts Parachute Rx, to ensure that Americans can secure many prescription medications at affordable and predictable prices during the COVID-19 pandemic.

- May 2020 – Anthem, Inc. launched IngenioRx, an innovative pharmacy benefits manager with clinical expertise and a digital-first approach to personalize member experiences. This launch helped the company to increase customer reach and company revenue.

- December 2019 - OptumRx, Inc. acquired Diplomat, a specialty pharmacy and infusion services provider, aiming to lower the overall cost of care and expand its portfolio.

REPORT COVERAGE

The pharmacy benefit management market research report provides a detailed analysis of the industry and focuses on key aspects such as leading companies, services, and service providers. Moreover, it offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the market report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service

|

|

By Service Provider

|

|

|

By Country/Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market is projected to grow from USD 646.61 billion in 2026 to USD 991.88 billion by 2034.

In 2026, the U.S. market value stood at USD 626.47 billion.

The market will exhibit steady growth at a CAGR of 5.5% during the forecast period (2026-2034).

By service, the specialty pharmacy services segment is leading the market.

Increasing pharmaceutical expenses and rising number of prescription filing are the key drivers of the market.

CVS Health, OptumRx, Inc., and Cigna are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 98

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us