Pharmacy Supply Chain Software Market Size, Share & Industry Analysis, By Product Type (Inventory Management Software, Procurement & Purchasing Software, Warehouse & Distribution Management Software, Order Management Software, Track-and-Trace/Serialization Software, & Others), By Supply Chain Stage (Procurement, Storage & Inventory, Distribution & Logistics, Dispensing & Replenishment, & Others), By Deployment (Cloud-Based, On-Premise, & Hybrid), By Type (Standalone & Integrated), By Mode of Operations (Centralized and Decentralized), By End User, and Regional Forecast, 2026-2034

Pharmacy Supply Chain Software Market Size and Future Outlook

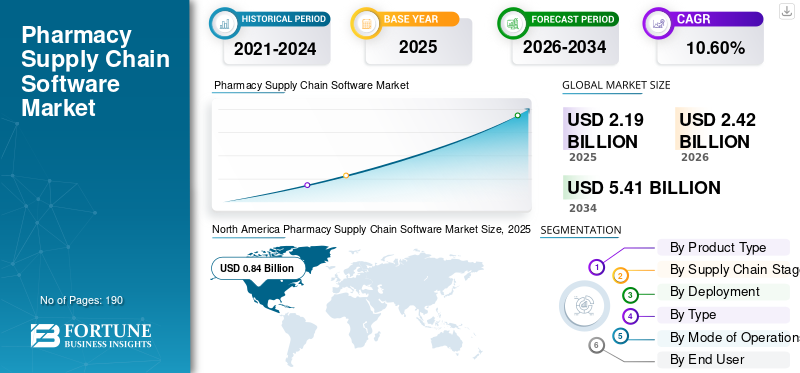

The global pharmacy supply chain software market size was valued at USD 2.19 billion in 2025. The market is projected to grow from USD 2.42 billion in 2026 to USD 5.41 billion by 2034, exhibiting a CAGR of 10.60% during the forecast period. North America dominated the pharmacy supply chain software market with a market share of 38.36% in 2025.

The global pharmacy supply chain software market is poised to grow steadily in the coming years, driven by the increasing need for better inventory visibility, tighter medication control, and stronger regulatory compliance across pharmacy networks. Healthcare providers, hospital pharmacies, and distribution-focused organizations are adopting software platforms that help manage purchasing, stock movement, replenishment, traceability, and enterprise-wide workflow coordination. As medication supply chains become more complex and cost pressures increase, software-based automation and connected pharmacy operations are becoming increasingly important for improving efficiency, reducing waste, and ensuring uninterrupted drug availability.

Strategic collaborations among key companies operating in the market and new product launches by them reinforce the market's growth potential.

- For instance, in September 2025, Oracle announced new AI-powered capabilities within Oracle Fusion Cloud Applications to help healthcare organizations streamline supply chain operations. The update added stronger inventory management and procurement capabilities to improve visibility, automate workflows, reduce costs, and support patient care. Such developments are expected to support growth in the market by helping healthcare and pharmacy organizations manage supplies more efficiently, improve purchasing decisions, and enhance operational efficiency.

Leading players in the industry, such as Omnicell, Inc., Tecsys Inc, TraceLink, Inc., and Oracle Corporation, are focusing on expanding their operations and strengthening their market positions.

Download Free sample to learn more about this report.

PHARMACY SUPPLY CHAIN SOFTWARE MARKET TRENDS

Growing Shift Toward Centralized Pharmacy Supply Chain Management is a Key Market Trend

Healthcare providers and pharmacy networks are increasingly moving toward centralized pharmacy supply chain management as it helps create a connected view of inventory, purchasing, replenishment, and medication movement across multiple sites. When supply chain decisions are managed through a centralized model, organizations can reduce duplication, improve stock visibility, standardize workflows, and respond faster to shortages or demand changes. These advantages also help lower waste, improve procurement control, and support better medication availability across the system.

- For instance, in January 2026, Tecsys published findings from a national survey showcasing that most health systems still lack real-time visibility across pharmacy supply chains, with only 1 in 5 healthcare leaders reporting full real-time visibility across care settings. This highlights why the market is shifting toward more centralized and connected pharmacy supply chain software, as health systems need stronger enterprise-wide control to manage disruptions, inventory risk, and medication flow more effectively.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Regulatory Compliance and Drug Traceability Fuels Market Growth

The global pharmacy supply chain software demand for regulatory compliance and drug traceability is increasing as pharmacies, hospitals, and other supply chain participants are under greater pressure to track medication movement more accurately and maintain secure data exchange across the supply chain. As compliance requirements become stricter, healthcare organizations need software that supports product verification, serialized data handling, transaction documentation, and end-to-end visibility. These factors create robust demand for pharmacy supply chain software as such platforms help reduce compliance risk, improve traceability, strengthen supply chain security, and support smoother pharmacy operations. As a result, regulatory compliance and drug traceability are becoming an important driver for the market.

- For instance, in November 2025, TraceLink announced that its customers were demonstrating readiness as the DSCSA dispenser deadline of November 27, 2025, approached, highlighting the growing adoption of compliance-focused supply chain solutions for dispensers and pharmacies. This development shows that as dispenser compliance deadlines approach, pharmacies and healthcare organizations increasingly need software platforms to manage better traceability, data exchange, and regulatory requirements, which supports global pharmacy supply chain software market growth.

MARKET RESTRAINTS

High Implementation Complexity and Integration Burden to Restrain Market Growth

A key restraint faced by the market is implementation complexity, which involves connecting new platforms to legacy pharmacy systems, hospital IT systems, dispensing tools, and procurement workflows. When integration becomes complex, organizations need more time, additional technical resources, and process redesign to ensure the system functions properly across sites. These factors increase deployment cost, delay go-live timelines, and create hesitation among buyers, especially those with limited IT bandwidth or fragmented pharmacy operations. As a result, adoption can slow even when the software's long-term value is clear, thereby restraining overall market growth.

- For instance, a January, 2025 NCPDP article, “Driving Pharmacy Interoperability in 2025,” highlighted that pharmacy interoperability remained difficult as pharmacies are dealing with outdated systems and complex technologies. These factors reflect the implementation and integration burden in the market, as software adoption becomes more difficult when organizations must modernize or connect multiple systems.

MARKET OPPORTUNITIES

Expansion of Centralized and Multisite Pharmacy Management Models to Offer Lucrative Growth Opportunities

The market is poised for growth as healthcare providers increasingly expand centralized and multisite pharmacy management models. When hospitals and health systems manage pharmacy inventory, replenishment, and medication workflows across multiple locations through a connected system, they improve visibility, standardize processes, and reduce duplication across sites. These factors result in better control over stock movement, faster response to shortages, and stronger coordination between central pharmacies and care locations. As a result, organizations are increasingly interested in software platforms that support enterprise-wide pharmacy operations, creating new growth opportunities for the market.

Furthermore, strategic collaborations and new product launches by key companies in the market are expected to drive growth.

- For instance, in December 2025, Omnicell launched Titan XT, an enterprise automated dispensing system powered by its OmniSphere cloud platform. The platform is designed to provide global formulary support, perpetual inventory management, enterprise-wide visibility, and centralized control of inventory management across the health system. This development highlights how vendors are building solutions specifically for centralized and multisite medication management, which supports future growth opportunities in the market.

MARKET CHALLENGES

Budget Pressures and Uncertain Return on Investment for Smaller Providers to Challenge Market Growth

The market faces a challenge as smaller providers, independent pharmacies, and resource-constrained healthcare organizations often operate under tight budgets and limited IT capacity. When software adoption requires upfront spending on licenses, integration, training, and workflow changes, these buyers become more cautious about investing unless the financial return is very clear and near-term. This slows decision-making and can delay modernization projects, especially when organizations are already managing margin pressure, labor shortages, and rising operating costs, limiting faster adoption across smaller and mid-sized pharmacy settings.

- For instance, Community Pharmacy England’s “Pressures Survey 2025 Funding and Profitability Report” highlighted that pharmacies continue to face mounting operational costs, inflationary pressures, and ongoing medicine supply issues, and said these financial pressures are limiting pharmacy owners' ability to keep their businesses afloat and deliver services. This highlights how pharmacies are under financial strain; investments in new supply chain software can be postponed even if the technology could improve long-term efficiency.

Segmentation Analysis

By Product Type

Inventory Management Software Led Market Due to Its Crucial Applications

Based on the product type, the market is categorized into inventory management software, procurement & purchasing software, warehouse & distribution management software, order management software, track-and-trace/serialization software, demand forecasting & supply planning software, returns & recall management software, analytics & reporting software, and others.

The inventory management software segment accounted for the largest market share. Pharmacy organizations need strong control over stock visibility, expiry tracking, replenishment, and medication availability before they can expand into more advanced supply chain functions. These solutions directly help reduce stockouts, lower waste, improve order accuracy, and support day-to-day pharmacy operations across hospitals and multisite networks. Since inventory is the core operational layer of the pharmacy supply chain, demand for inventory-focused software remains higher than for narrower categories such as returns management or standalone analytics.

- For instance, in May 2025, Omnicell launched new products for perioperative and clinic settings featuring RFID-enabled dispensing and intelligent inventory management software designed to improve inventory visibility and medication management. Such product innovation reflects the continued centrality of inventory control as a purchase priority for pharmacy organizations, which supports the dominance of this segment.

The analytics & reporting software segment is expected to grow at a CAGR of 12.52% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Supply Chain Stage

Increasing Pressure for Stock Visibility Boosted Storage & Inventory Segment Growth

Based on the supply chain stage, the market is segmented into procurement, storage & inventory, distribution & logistics, dispensing & replenishment, reverse logistics, and others.

In 2025, the storage & inventory segment accounted for the largest revenue share. Storage and inventory are where pharmacies face the most immediate operational pressure, including stock visibility, product availability, expiry handling, and inventory balancing across locations. Software spending is often concentrated here as better storage and inventory control directly improve medication access, support compliance, and reduce waste from overstocking or stockouts. Key companies are focusing on technologically advanced offerings and the regulatory approvals that accompany them to strengthen their market positions.

- For instance, in July 2025, Oracle launched Advanced Inventory Management within Oracle Cloud SCM to help organizations streamline warehouse operations, simplify inventory transactions, and accelerate order fulfillment. This shows that vendors continue to invest strongly in inventory-stage capabilities, reinforcing the leading position of the storage and inventory segment.

The reverse logistics segment is projected to grow at a CAGR of 11.49% over the forecast period.

By Deployment

Cloud-based Segment Led Market Due to Greater Flexibility and Operational Visibility

Based on deployment, the market is segmented into cloud-based, on-premise, and hybrid.

In 2025, the cloud-based segment dominated the market. Many pharmacy organizations are increasingly preferring software that can connect multiple locations, support real-time updates, reduce local infrastructure burden, and enable faster rollout across enterprise networks. Cloud models also make it easier to scale functionality, support analytics, and connect inventory, workflow, and compliance data through a shared platform. As pharmacy supply chains become more distributed and data-driven, cloud deployment offers greater flexibility and operational visibility than traditional, isolated systems, leading the market.

- For instance, in June 2025, Omnicell announced that OmniSphere, its cloud-native software workflow engine and data platform, received HITRUST CSF i1 certification. This development highlights how vendors are strengthening cloud-based pharmacy platforms to support secure, enterprise-scale medication and supply chain operations, which supports the dominance of the cloud-based segment.

In addition, the hybrid segment is projected to grow at a CAGR of 8.20% during the study period.

By Type

Integrated Segment Led Market as It Creates Stronger Business Value

Based on type, the market is segmented into standalone and integrated.

The integrated segment accounted for the largest pharmacy supply chain software market share in 2025. Integrated solutions provide a connected platform that links inventory, procurement, replenishment, compliance, and operational workflows. When software modules work together, organizations reduce manual handoffs, improve data accuracy, and gain better end-to-end visibility across the medication supply chain. This creates stronger business value than isolated applications, especially for health systems and pharmacy networks managing complex operations.

- For instance, in November 2025, TraceLink announced that its customers were demonstrating readiness as the DSCSA dispenser deadline arrived, highlighting the need for connected compliance, traceability, and supply chain data exchange across pharmacy operations. This supports the dominance of integrated platforms as regulatory readiness increasingly depends on systems that connect multiple functions rather than operate in silos.

The standalone segment is projected to grow at a CAGR of 9.08% during the study period.

By Mode of Operations

Efficient Operations Through Centralized Mode of Operations Boosted Segmental Growth

Based on the mode of operations, the market is segmented into centralized and decentralized.

In 2025, the centralized dominated, accounting for the largest market share. Centralized operations are likely to dominate the market as health systems and large pharmacy networks are increasingly moving toward enterprise-wide control of purchasing, inventory, replenishment, and medication distribution across multiple care sites. A centralized model helps standardize workflows, balance inventory, reduce duplication, and strengthen oversight of pharmacy stock movement. It also allows organizations to respond more quickly to shortages and demand fluctuations through a unified operating structure. Underscoring these benefits, centralized operating models are estimated to account for a larger share of the market.

- For instance, in December 2025, Omnicell launched Titan XT, described as delivering enterprise-wide visibility and stronger pharmacy control for a growing health system through the OmniSphere platform. Such development directly reflects the market shift toward centralized medication and inventory management, supporting the dominance of the centralized segment.

The decentralized segment is projected to grow at a CAGR of 9.93% over the study period.

By End User

Hospital Pharmacies Segment Commanded Market as They Manage Complex Medication Inventories

Based on end user, the market is segmented into retail pharmacies, hospital pharmacies, pharmaceutical wholesalers & distributors, specialty pharmacies, and others.

Hospital pharmacies dominated the market in 2025. They manage complex medication inventories, higher compliance requirements, multisite coordination, critical care demand, and greater pressure to prevent shortages and waste than many other end users. These operational demands make hospital pharmacies more dependent on software for purchasing, inventory control, shortage response, and workflow management. Therefore, hospital pharmacies are estimated to have accounted for the largest market share.

- For instance, in April 2025, Bluesight released its 11th Annual Hospital Pharmacy Operations Report, highlighting rising technology adoption to address compliance and procurement pressures facing hospital pharmacies. This supports the dominance of the hospital pharmacy segment as it shows that hospitals remain a major buyer group for software that improves pharmacy supply chain and operational performance.

The specialty pharmacies segment is projected to grow at a CAGR of 11.40% over the study period.

Pharmacy Supply Chain Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Pharmacy Supply Chain Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.77 billion and maintained its leading position in 2025 at USD 0.84 billion. Growth in the region is being supported by DSCSA-driven traceability and dispenser-readiness requirements in the U.S., which are pushing pharmacies, hospital systems, and distributors to adopt software for serialized data exchange, verification, and end-to-end visibility.

U.S. Pharmacy Supply Chain Software Market

The U.S. market is estimated at around USD 0.85 billion in 2026, accounting for roughly 35.28% of the global revenues.

Europe

Europe is projected to grow at 9.57% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.67 billion in 2026. The regional market is growing as hospitals and pharmacy systems increase automation and digitalization to improve medication safety, inventory control, and workflow efficiency. At the same time, the Falsified Medicines Directive continues to support demand for traceability-related software.

U.K. Pharmacy Supply Chain Software Market

The U.K. market is estimated at around USD 0.13 billion in 2026, representing roughly 5.45% of global revenues.

Germany Pharmacy Supply Chain Software Market

Germany's market is projected to reach approximately USD 0.15 billion in 2026, equivalent to around 6.14% of global revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 0.56 billion in 2026 and secure the position of the third-largest region in the market. Market growth in Asia Pacific is being driven by rapid healthcare digitalization, rising hospital modernization, and stronger interest in real-time medicine stock tracking and centralized procurement workflows, especially in large public health systems.

Japan Pharmacy Supply Chain Software Market

The Japanese market in 2026 is estimated at around USD 0.10 billion, accounting for approximately 3.99% of global revenues.

China Pharmacy Supply Chain Software Market

The Chinese market in 2026 is estimated at around USD 0.18 billion, representing approximately 7.40% of global sales.

India Pharmacy Supply Chain Software Market

The Indian market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 3.14% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.16 billion in 2026. The market is expanding as pharmacies in the region remain highly exposed to stock shortages and import dependence, which is increasing the need for better inventory planning, availability management, and digitally enabled pharmacy operations. In the Middle East & Africa, the GCC is set to reach USD 0.04 billion in 2026.

South Africa Pharmacy Supply Chain Software Market

The South African market is projected to reach approximately USD 0.02 billion in 2026, accounting for roughly 0.66% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations by Key Players to Propel Market Progress

The global pharmacy supply chain software market is highly consolidated, with companies such as Omnicell, Inc., Tecsys Inc, TraceLink, Inc., Oracle Corporation, SAP SE, and Bluesight holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in June 2023, Tecsys Inc, a leading provider of AI-powered cancer diagnostics, collaborated with Thales, a global leader in software monetization and licensing, to accelerate the profitability of its software, protect its core technology, and enhance back-office software automation. Such strategic collaborations aim to drive market growth.

McKesson Corporation, ScriptPro LLC, and Liberty Software are some of the prominent players in the market. They focus on technological innovations, strategic alliances, and new product introductions to reinforce their positions in the market.

LIST OF KEY PHARMACY SUPPLY CHAIN SOFTWARE COMPANIES PROFILED

- Omnicell, Inc. (U.S.)

- Tecsys Inc. (Canada)

- TraceLink, Inc. (U.S.)

- Oracle Corporation (U.S.)

- SAP SE (Germany)

- Bluesight (U.S.)

- McKesson Corporation (U.S.)

- ScriptPro LLC (U.S.)

- Liberty Software (U.S.)

- PioneerRx, LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Teva Pharmaceutical Industries Ltd. launched Teva Rise, an open innovation platform designed to harness the power of a variety of disruptive technologies, including AI, industry 4.0 smart manufacturing, digital health, and biotech, by connecting startups and technology companies with Teva’s business units. The initiative aimed to co-create solutions for the challenges faced by the pharmaceutical industry and to drive patient impact and business transformation.

- November 2025: Axtria Inc. launched its AI-Powered Launch Excellence for Emerging Pharma offering, a solution designed to help emerging and mid-sized pharmaceutical companies accelerate brand launches and achieve commercial excellence.

- August 2025: Celcius Logistics launched Celcius+, specialized logistics vertical focused exclusively on the pharmaceutical supply chain. The solution was designed to address temperature control, compliance, and real-time visibility requirements for medicines, vaccines, and other sensitive products.

- June 2025: Tecsys Inc. launched TecsysIQ, a cloud-native intelligence layer that helps healthcare organizations unify fragmented data and deliver AI-powered insights across clinical, operational, and financial systems. The innovative solutions accelerate the development of AI-enabled applications and data-driven decision-making that improve patient care and strengthen health system performance.

- August 2024: Pfizer Inc. introduced PfizerForAll, a user-friendly digital platform designed to make access to healthcare and managing health and wellness more seamless for people across the U.S. PfizerForAll helps individuals and their families cut down on the time and steps needed to take important health actions such as getting care, filling prescriptions, and finding potential savings on Pfizer medicines.

REPORT COVERAGE

The report provides a detailed global pharmacy supply chain software market analysis of the industry across key business and operational parameters. It covers market size estimation and forecast analysis, while examining how the market is evolving across product type, supply chain stage, deployment model, software type, mode of operations, and end-user categories. The study also evaluates the impact of rising demand for inventory visibility, regulatory compliance, centralized pharmacy management, and workflow automation on market growth. In addition, it reviews the competitive landscape by assessing major companies, their product offerings, strategic developments, and market positioning. The report further includes analysis of growth drivers, restraints, challenges, and opportunities, along with regional market trends and developments influencing adoption across different healthcare and pharmacy settings.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.60% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Supply Chain Stage, Deployment, Type, Mode of Operations, End User, and Region |

| By Product Type |

|

| By Supply Chain Stage |

|

| By Deployment |

|

| By Type |

|

| By Mode of Operations |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.19 billion in 2025 and is projected to reach USD 5.41 billion by 2034.

In 2025, the market value in North America stood at USD 0.84 billion.

The market is expected to grow at a CAGR of 10.60% over the forecast period of 2026-2034.

The inventory management software segment led the market.

Increasing demand for regulatory compliance and drug traceability is fueling market growth.

Omnicell, Inc., Tecsys Inc., TraceLink, Inc., Oracle Corporation, and SAP SE are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us