Phosphate Market Size, Share & Industry Analysis, By Product Type (Ammonium, Calcium, Phosphoric Acid, Potassium, Sodium, and Others), By Application (Agrochemicals, Food & Beverages, Animal Feed, Detergent & Cleaning, Water Treatment Chemicals, and Others), and Regional Forecast, 2026-2034

Phosphates Market Overview

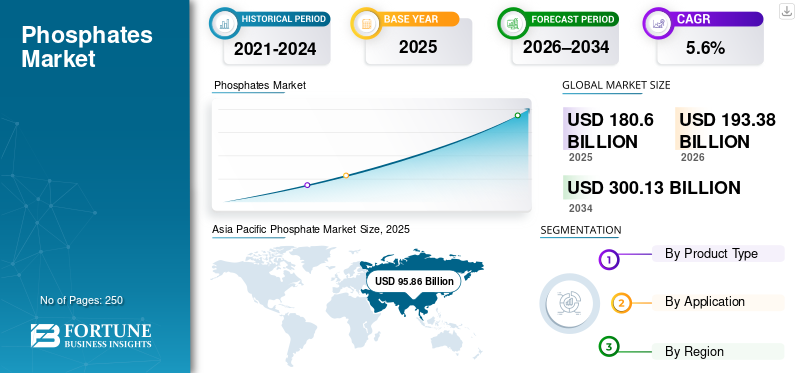

The global phosphate market size was valued at USD 180.60 billion in 2025. The market is projected to grow from USD 193.38 billion in 2026 to USD 300.13 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period. Asia Pacific dominated the phosphate market with a market share of 53.08% in 2025.

Phosphate is an inorganic chemical compound derived from phosphate rock and is an essential nutrient widely used across agriculture, food processing, detergents, water treatment, and animal nutrition. The market plays a critical role in sustaining global food security, as phosphorus is a key macronutrient required for plant growth and metabolic processes. Among various forms, ammonium product type dominates consumption due to its high nutrient concentration and suitability for fertilizer applications. Rising global population, increasing food demand, and declining arable land continue to reinforce the importance of phosphate-based inputs in agriculture. Additionally, the mineral is extensively used in food additives, cleaning agents, and water treatment chemicals, supporting diversified demand beyond agriculture. Its roles in industrial processing, pH regulation, and corrosion control further drive market expansion.

Major producers operate across integrated mining, processing, and downstream formulation value chains, ensuring consistent global supply. The major players operating in the market comprise OCP Group, The Mosaic Company, Nutrien Ltd., Yara International ASA, and PhosAgro Group.

Download Free sample to learn more about this report.

Phosphate Market Key Takeaways

- 2025 Market Size: USD 180.60 billion

- 2026 Market Size: USD 193.38 billion

- 2034 Forecast Market Size: USD 300.13 billion

- CAGR: 5.6% from 2026-2034

- Asia Pacific dominated the phosphate market with a 53.08% share in 2025.

- The ammonium segment held the largest market share in 2025.

- The food & beverages segment is projected to grow at a CAGR of 5.1% during the forecast period.

Asia Pacific

Asia Pacific led the market in 2025, driven by high agricultural intensity and strong food demand.

Europe

Europe reached USD 23.61 billion in 2025 and is expected to witness steady growth.

Middle East & Africa

The Middle East & Africa market was valued at USD 33.06 billion in 2025.

U.S.

The market reached USD 16.72 billion in 2025, supported by demand from agriculture and food processing industries.

Japan

Growing focus on agricultural productivity and food security is supporting phosphate demand.

Read More

PHOSPHATE MARKET TRENDS

Agriculture and Process Optimization to Foster Market Expansion

The market is witnessing evolving trends driven by sustainability requirements and efficiency-focused agricultural practices. A prominent trend is the increasing adoption of high-efficiency product-based fertilizers that improve nutrient uptake and reduce runoff-related environmental impacts. Another key trend is the gradual shift toward integrated product value chains, where producers invest in mining, beneficiation, and fertilizer manufacturing to improve cost control and supply reliability. In non-agricultural sectors, the demand for low-phosphate and phosphate-free detergent formulations is influencing product innovation. Additionally, advancements in phosphoric acid purification and specialty phosphate processing are supporting higher-value applications in food and industrial uses. Regionally, the Asia Pacific continues to expand capacity, while Europe emphasizes regulatory compliance and nutrient management. These trends reflect how the market is structurally adapting to environmental, regulatory, and efficiency-driven requirements.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Agricultural Dependence and Nutrient Requirements to Drive Product Demand

The market is primarily driven by strong, sustained demand from the agricultural sector. Phosphorus is an essential plant nutrient, making product-based fertilizers indispensable for crop production worldwide. Increasing population growth, rising food consumption, and the need to maximize yields from limited arable land continue to drive fertilizer demand. Another key driver is the expansion of agrochemical usage in emerging economies, supported by government initiatives to improve food security. Additionally, the demand from food processing, animal feed, and water treatment sectors contributes to baseline consumption. Industrial uses in detergents and cleaning formulations further support the phosphate market growth. These structural drivers ensure consistent multi-sector usage, thereby sustaining long-term market stability.

MARKET RESTRAINTS

Regulatory Standards and Approval Processes to Slow Market Growth

Despite strong demand, the market faces restraints related to environmental regulations and resource availability. Stringent controls on product runoff and eutrophication have increased regulatory scrutiny on fertilizer usage in several regions. Mining and beneficiation of phosphate rock are capital-intensive and subject to environmental permitting challenges. Additionally, the geographical concentration of product reserves exposes the market to supply risks and price volatility. High energy and logistics costs further affect production economics. In detergents, regulatory pressure to reduce product content limits growth in specific applications. These factors increase compliance costs and restrict operational flexibility, moderating market expansion in highly regulated regions.

MARKET OPPORTUNITIES

Food Security Concerns and Industrial Diversification to Create Growth Avenues

The market presents significant growth opportunities driven by global food security concerns and expanding industrial applications. One important opportunity lies in the increasing use of phosphate fertilizers in emerging economies to improve crop yields and agricultural productivity. Another opportunity is the growing demand for food-grade phosphate used as preservatives, stabilizers, and acidity regulators in processed foods and beverages. The expansion of water treatment infrastructure also creates opportunities for phosphate-based corrosion inhibitors and treatment chemicals. Additionally, rising livestock production supports product demand in animal feed formulations. Investment in sustainable mining practices and nutrient recovery technologies further enhances long-term supply security. These factors are expanding the scope of product use across regions and industries, thereby strengthening the market's long-term growth prospects.

MARKET CHALLENGES

Supply Concentration and Price Volatility to Affect Market Stability

The market faces challenges related to supply concentration and fluctuating input costs. Phosphate rock reserves are unevenly distributed globally, making supply chains sensitive to geopolitical developments and trade policies. Volatility in mining costs, energy prices, and logistics expenses directly affects product pricing. Another challenge is balancing agricultural demand with environmental sustainability requirements, which necessitates efficient nutrient management. Additionally, the limited availability of high-grade phosphate rock increases the complexity of beneficiation. Addressing these challenges requires long-term resource planning, technological innovation, and regulatory alignment, influencing overall market stability.

RESEARCH AND DEVELOPMENT ACTIVITIES

R&D activities in the market are focused on improving nutrient use efficiency and reducing environmental impact. The development of controlled-release fertilizers, enhanced-efficiency product formulations, and nutrient recovery technologies is gaining traction. Advances in phosphoric acid purification also support food-grade and industrial applications. These innovations enhance regulatory compliance and long-term competitiveness of products in the market.

Segmentation Analysis

By Product Type

High Agronomic Efficiency to Push the Dominance of Ammonium Segment

Based on product type, the market is segmented into ammonium, calcium, phosphoric acid, potassium, sodium, and others.

The ammonium segment held the leading market share in 2025. This is due to its high phosphorus content and superior agronomic efficiency. Products such as monoammonium phosphate (MAP) and diammonium phosphate (DAP) are widely used in fertilizer formulations as they provide readily available phosphorus and nitrogen, supporting improved crop yields. Their compatibility with modern farming practices, including precision agriculture and blended fertilizers, further strengthens adoption. Strong demand from cereal, oilseed, and cash crop cultivation across both developed and emerging economies drives high consumption volumes. Additionally, the ammonium product type offers easier handling and storage than alternative formulations. These functional and economic advantages ensure consistent global demand, reinforcing the dominant position of the ammonium product type in the market.

The calcium segment accounts for a significant share of the market due to its extensive use in food, animal feed, and pharmaceutical applications. These compounds are valued for their high bioavailability of calcium and phosphorus, making them suitable for nutritional supplementation and food fortification. In animal feed, calcium product type supports bone development and metabolic functions, driving steady demand from the livestock sector. The segment is anticipated to grow at a CAGR of 4.7% over the forecast period.

The phosphoric acid segment is poised to grow at a CAGR of 5.3% over the analysis period. These acids play a critical role in the market as a key intermediate used in fertilizer production and industrial applications. It is primarily used in the manufacturing of ammonium phosphate, calcium phosphate, and other downstream products. Beyond fertilizers, phosphoric acid is used in food & beverage processing as an acidity regulator and in metal treatment and water treatment applications. The rising demand from fertilizer manufacturers directly supports phosphoric acid consumption, while growth in food-grade and industrial applications adds diversification.

By Application

Agrochemicals Segment Leads the Market owing to Significant Role in Enhancing Crop Productivity

By application, the market is segmented into agrochemicals, food & beverages, animal feed, detergent & cleaning, water treatment chemicals, and others.

The agrochemicals segment leads the global phosphate market share and is driving market growth as phosphorus plays an indispensable role in plant growth and crop productivity. Phosphate-based fertilizers are critical for root development, energy transfer, and overall plant metabolism, making them essential across cereal, oilseed, and horticultural crops. Rising global population, increasing food production, and declining arable land have intensified the need to maximize agricultural yields, directly supporting global fertilizer demand. Additionally, the adoption of modern farming practices and balanced nutrient management supports sustained consumption. Driven by these factors, the agrochemicals segment accounts for the largest share of the global market.

To know how our report can help streamline your business, Speak to Analyst

The food & beverages segment is expected to grow at a CAGR of 5.1% over the forecast period. In this industry, phosphates are widely used as functional additives due to their ability to act as acidity regulators, emulsifiers, stabilizers, and preservatives. They play a key role in processed foods such as baked goods, dairy products, meat, seafood, and beverages by improving texture, moisture retention, and shelf life. The growing consumption of packaged and processed foods, particularly in urban and developing regions, continues to support demand.

Furthermore, phosphates are an essential component of animal feed formulations, supplying phosphorus required for bone development, metabolism, and overall animal health. Calcium and other feed-grade products are extensively used in poultry, cattle, swine, and aquaculture feed. The globally rising demand for meat, dairy, and seafood products has driven the expansion of livestock farming, thereby directly supporting product consumption in feed applications. The animal feed segment is poised to expand at a CAGR of 6.2% over the analysis period.

Phosphate Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Phosphate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest and fastest-growing region in the global market, driven by high agricultural intensity and population-driven food demand. China and India are the primary consumers, supported by extensive fertilizer usage to improve crop yields across cereals, rice, and horticultural crops. Government-backed food security programs and fertilizer subsidy schemes further strengthen product consumption. Additionally, expanding domestic product processing capacity and integrated fertilizer production improve supply reliability. The rising demand from animal feed and water treatment applications also contributes to regional consumption. Despite environmental concerns about nutrient runoff, sustained agricultural dependency ensures continued demand, thereby positioning the Asia Pacific as the dominant region in the global market.

To know how our report can help streamline your business, Speak to Analyst

China Phosphate Market

The China market reached a value of USD 83.4 billion in 2025, accounting for approximately 46.2% of global revenues. Strong demand for product-based fertilizers, driven by intensive crop cultivation, government-backed food security programs, and efforts to improve agricultural productivity, continues to support market growth.

India Phosphate Market

In 2025, the India market touched a valuation of around USD 1.31 billion. The rising fertilizer consumption to support food grain production for a growing population, combined with government subsidy programs and soil nutrient management initiatives, is driving product demand. Additionally, the expansion of livestock farming and the increasing use of feed-grade products are supporting steady market growth.

North America

North America remains a significant regional market and reached a value of USD 18.63 billion in 2025. North America holds a substantial market share, supported by large-scale, mechanized agriculture and well-established animal feed industries. The product usage in water treatment and industrial cleaning applications contributes to baseline demand. Regulatory frameworks emphasize nutrient efficiency and environmental protection, encouraging optimized fertilizer application rather than volume growth. These factors result in steady, efficiency-driven consumption patterns, thereby maintaining North America’s stable position in the global market.

U.S. Phosphate Market

The U.S. market reached a value of USD 16.72 billion in 2025, representing approximately 9.3% of regional revenues. The country records a dominant regional demand due to extensive cultivation of corn, soybeans, and wheat, which rely heavily on product-based fertilizers. Strong demand from livestock farming further supports the feed-grade product consumption.

Europe

The Europe market, which reached a valuation of USD 23.61 billion in 2025, is projected to record modest growth. The regional market is shaped by stringent environmental regulations aimed at reducing nutrient runoff and eutrophication. As a result, fertilizer application growth remains limited, with demand focused on efficient, precise nutrient management. Major agricultural economies such as France, Germany, and Spain support baseline product consumption, while the demand from food processing and water treatment applications adds diversification. Moreover, the regulatory pressure has reduced product usage in household detergents, limiting growth in that segment.

Germany Phosphate Market

The Germany market touched a value of around USD 3.44 billion in 2025, representing approximately 1.9% of regional demand. The product consumption is supported by construction activity, building renovations, and ongoing investment in water supply and wastewater infrastructure, all of which are conducted under strict quality and performance standards.

U.K. Phosphate Market

The U.K. market hit a valuation of USD 2.44 billion in 2025, accounting for roughly 1.4% of regional revenues. Stable demand for fertilizers, driven by crop cultivation and soil nutrient management, and continued product use in food processing and water treatment applications, is supporting market growth.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to experience moderate growth over the forecast period. Latin America is an emerging growth region for the market, driven by expanding agricultural production and export-oriented farming. Countries such as Brazil and Argentina rely heavily on phosphate fertilizers to support large-scale cultivation of soybeans, corn, and sugarcane. The increasing adoption of modern agricultural practices and rising fertilizer penetration rates further support demand growth. In the Middle East & Africa, growth is driven by food security initiatives and expanding agricultural activity. African countries are increasing fertilizer usage to improve crop productivity and reduce dependence on food imports. In the Middle East, the product demand is supported by integrated fertilizer production and export-oriented industries. The Middle East & Africa market size reached USD 33.06 billion in 2025.

Morocco Phosphate Market

The Morocco market accounted for around USD 23.65 billion in 2025, representing approximately 13.1% of regional revenues. Strong growth is driven by the country’s vast phosphate rock reserves and integrated product mining-to-fertilizer production capacity, supporting both domestic use and large-scale exports. Additionally, the rising global fertilizer demand and investments by state-backed producers are strengthening Morocco’s position as a key hub for product supply.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players’ Emphasis on Long-term Supply Agreements to Consolidate their Market Standing

The market is moderately consolidated, led by vertically integrated players with substantial control over phosphate rock resources and downstream production. Competition is driven by production scale, cost efficiency, and supply security. Leading companies focus on value-added products, sustainable fertilizer solutions, and long-term supply agreements. Regional producers serve domestic demand, while global players emphasize exports and integration, shaping the competitive dynamics through scale and resource advantage.

LIST OF KEY PHOSPHATES COMPANIES PROFILED

- OCP Group (Morocco)

- The Mosaic Company (U.S.)

- Nutrien Ltd. (Canada)

- Yara International ASA (Norway)

- PhosAgro Group (Russia)

- ICL Group Ltd. (Israel)

- EuroChem Group (Switzerland)

- Foskor (Pty) Ltd. (South Africa)

- Jordan Phosphate Mines Company (JPMC) (Jordan)

- Ma’aden (Saudi Arabia)

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.6% from 2026 to 2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Product Type, Application, and Region |

| By Product Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 180.60 billion in 2025 and is projected to reach USD 300.13 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 5.6% during the forecast period of 2026-2034.

The agrochemicals segment leads the market by application.

Asia Pacific holds the highest market share.

Agricultural dependence and nutrient requirements are key factors expected to drive market growth.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us