Phototherapy Equipment Market Size, Share & Industry Analysis, By Product (Conventional Phototherapy Equipment, LED Phototherapy Equipment, and Fiber Optic Phototherapy Equipment), By Application (Skin Disease Treatment {Psoriasis, Vitiligo, Eczema, and Others} and Neonatal Jaundice Management), By End-user (Hospitals & Clinics and Homecare Settings), and Regional Forecast, 2026-2034

Phototherapy Equipment Market Size and Future Outlook

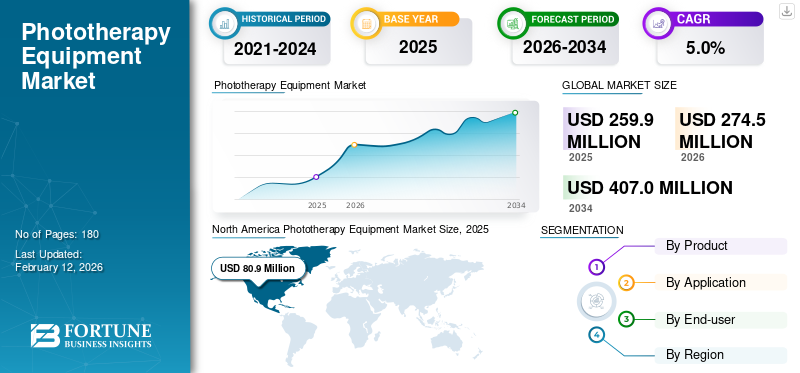

The global phototherapy equipment market size was valued at USD 259.9 million in 2025. The market is projected to grow from USD 274.5 million in 2026 to USD 407.0 million by 2034, exhibiting a CAGR of 5.0% during the forecast period. North America dominated the global market with a market share of 31.13% in 2025.

Phototherapy equipment covers medical light-based systems that deliver controlled wavelengths, most commonly UVB/UVA for dermatology and blue light for neonatal care, to treat chronic skin disorders and reduce bilirubin in newborn jaundice. The market includes full-body phototherapy cabins used in hospitals and specialty clinics, targeted/spot devices, and neonatal systems such as overhead LED units and fiber-optic blankets used at the bedside. Growth is driven by steady demand from two clinical streams including recurring dermatology treatments for flare-prone conditions and the ongoing need for safe, rapid bilirubin reduction in neonatal units. In routine care, UK clinical information on newborn jaundice describes hospital phototherapy as a key treatment when bilirubin levels are high, reinforcing consistent equipment utilization in maternity and NICU settings.

Furthermore, GE HealthCare, Dräger, Natus Medical, and ATOM Medical held the largest market share, driven by growing investments and tactical initiatives, such as new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

Phototherapy Equipment Market Key Takeaways

- 2025 Market Size: USD 259.9 million

- 2026 Market Size: USD 274.5 million

- 2034 Forecast Market Size: USD 407.0 million

- CAGR: 5.0% from 2026–2034

- North America dominated the global phototherapy equipment market with a 31.13% share in 2025.

- LED phototherapy equipment segment is projected to grow at a 8.6% CAGR during the forecast period.

- Homecare settings segment is projected to grow at a 8.2% CAGR during the forecast period.

North America

North America held USD 77.6 million revenue in 2024 and maintained leadership with strong regional demand base.

Europe

Europe is projected to reach USD 78.7 million in 2026, supported by steady healthcare expansion and adoption growth.

Asia Pacific

Asia Pacific is predicted to be valued at USD 75.5 million in 2026, reflecting increasing healthcare infrastructure development.

U.S.

The U.S. market is projected to represent USD 74.6 million in 2026, capturing 29.0% of global revenue.

Japan

The Japan market is projected to generate USD 10.2 million in 2026, contributing 3.7% of global revenue.

Read More

PHOTOTHERAPY EQUIPMENT MARKET TRENDS

Preferential Shift Toward LED Phototherapy Equipment to be a Significant Market Trend

Across segments, the market is steadily shifting from older lamp-based designs to LED-driven platforms, primarily as LEDs simplify maintenance cycles, reduce downtime, and can support tighter dose control. This transition is playing out alongside more “service-ready” purchasing patterns, in which providers expect installation support, preventive maintenance, and consumable planning, not just device delivery. A clear trend is the move toward LED-based phototherapy and tighter measurement of delivered dose, especially in neonatal care, where wavelength match and irradiance thresholds are central to effectiveness.

On the neonatal side, structured procurement is also common in global health supply chains. UNICEF’s catalogue positioning of LED phototherapy systems with accessories highlights how buyers increasingly prefer standardized device packages that are deployment-ready.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Patient Pool that Need Phototherapy to Fuel Market Growth

Phototherapy remains a practical, protocol-driven option where clinicians need a non-systemic, repeatable treatment. In dermatology, the addressable pool is sustained by long-term conditions that often require multiple treatment courses over time. The NHS describes vitiligo as a long-term condition, and atopic eczema as a common itchy skin condition affecting all ages, underscoring the chronic, recurring nature of patient need.

Furthermore, in neonatal care, the care pathway is time-sensitive, as it requires immediate actions to avoid further complications. For instance, if bilirubin levels are high, phototherapy is used in the hospital to lower them and reduce the risk of serious complications. Moreover, rising strategic investment in neonatal care is supported by the rising global burden of newborn risk.

- For instance, the WHO’s newborn mortality fact sheet published in March 2024 highlights that 2.3 million newborns died in 2022 and stresses the need for intensified quality intrapartum and newborn care.

In this environment, neonatal monitoring and treatment equipment, including phototherapy, remains central. Thus, the underlying disease burden and the expanding patient pool that need phototherapy are likely to boost the overall market.

MARKET RESTRAINTS

Budget Constraints and Safety Issues to Limit Market Growth

Even when clinical demand is clear, purchasing decisions for phototherapy equipment can be slow as these devices sit in capex budgets and require ongoing governance. Hospitals often bundle purchase decisions with accessories, installation needs, and service cover, which increases the perceived “all-in” cost. A UK public procurement notice published in January 2025 for phototherapy equipment (UVA/UVB cabins, accessories, and service elements) illustrates how procurement is handled as a structured, value-based purchase rather than an impulse upgrade.

Clinical safety requirements also shape adoption. In neonatal settings, treatment is delivered under strict monitoring, including temperature checks, hydration surveillance, and repeated bilirubin testing, so providers must ensure staff training, protocols, and device upkeep are robust. In dermatology, UV exposure requires dose accuracy, patient selection, and adherence to safety precautions, which can limit expansion into lower-resource clinics without specialist oversight. Finally, differences in regulatory regimes and device classifications across regions can lengthen commercialization timelines and increase compliance costs, especially for manufacturers selling in North America, Europe, and Asia Pacific.

MARKET OPPORTUNITIES

Home-based Models and Targeted UV Systems that Reduce Clinic Dependency to Create Significant Growth Opportunities

The biggest opportunity is to convert phototherapy from a “clinic-only” modality into a hybrid model that fits modern care pathways. Smaller, more guided, and easier-to-monitor devices can reduce the bottleneck created by three-times-a-week clinic schedules, particularly for chronic dermatologic diseases that require maintenance therapy. This is where connected workflows, dose guidance, and treatment logging matter as the more a device supports protocol adherence and clinician oversight, the more comfortable providers and payers become in expanding its use beyond the clinic. Regulatory momentum also supports this shift. The continued innovation in localized, targeted treatment can shorten session times, reduce total-body exposure, and increase throughput for busy practices.

On the neonatal side, hospitals in emerging markets are also seeking robust, low-maintenance systems aligned with guidance that emphasizes measurable irradiance and targeted wavelengths, creating room for suppliers that can offer durable devices, along with training and service packages.

MARKET CHALLENGES

Adherence, Maintenance Discipline, and Proving Value in Real-World Settings to Challenge Market Growth

The market’s hardest challenge is that phototherapy sits at the intersection of device performance and human behavior. For dermatology indications, outcomes depend on regular attendance and correct dosing progression; missed sessions can slow response, frustrate patients, and reduce the perceived value of therapy, especially when symptoms recur. In hospitals, maintenance discipline is non-negotiable: irradiance varies by device configuration and upkeep, and clinical guidance emphasizes that correct wavelength and adequate irradiance are critical to treatment effectiveness. That creates ongoing demands for training, periodic verification, and process checks, work that smaller facilities may struggle to sustain.

Regulatory and procurement complexity also matters: health systems may require evidence of safety, service support, spare parts availability, and standard operating procedures before scaling across multiple sites. In home settings, the challenge becomes governance, ensuring appropriate patient selection, physician oversight, and safe use, so that expanded access does not increase adverse events. Also, manufacturers must demonstrate economic benefits beyond clinical efficacy, such as fewer clinic visits, reduced complications, faster results, and stronger patient support. Without clear real-world value stories, buyers may delay upgrades or choose lower-cost systems, slowing premium device adoption despite strong underlying demand.

Segmentation Analysis

By Product

Wide Adoption of Conventional Phototherapy Equipment in Several Healthcare Settings to Drive Segment Growth

Based on product, the market is segmented into conventional phototherapy equipment, LED phototherapy equipment, and fiber optic phototherapy equipment.

To know how our report can help streamline your business, Speak to Analyst

Conventional phototherapy systems still hold a large installed base, especially in dermatology clinics and hospitals, as they are proven, familiar, and deeply embedded in clinical workflows. Many providers already own cabinets and panels that remain serviceable with routine maintenance, so replacement is often a planned, multi-year decision rather than an immediate switch. Procurement behavior reinforces this as public tenders continue to specify UVA/UVB cabin solutions and associated tube sets and accessories, indicating ongoing demand for conventional-format systems in day-to-day service delivery.

Additionally, the LED phototherapy equipment segment is projected to grow at a CAGR of 8.6% during the forecast period.

By Application

Wide Phototherapy Utilisation in Skin Disease Treatment Segment to Propel Growth

By application, the market is classified into skin disease treatment and neonatal jaundice management. Furthermore, skin disease treatment is further segmented into psoriasis, vitiligo, eczema, and others.

Skin disease treatment segment lead the phototherapy equipment market share as dermatology phototherapy is used repeatedly across a wide pool of chronic patients and across multiple indications. Conditions such as atopic eczema and vitiligo are long-term, and care often involves ongoing symptom management rather than a one-time intervention, which supports sustained equipment utilization in outpatient settings.

Additionally, the neonatal jaundice management segment is estimated to grow at a CAGR of 4.1% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals & Clinics to Propel Segment Growth

On the basis of end-user, the market is classified into hospitals & clinics and homecare settings.

Hospitals and clinics dominate as phototherapy is most often delivered under supervised protocols that require trained staff, calibrated dosing, and monitoring. Neonatal phototherapy is typically initiated in a hospital when bilirubin is high, with continuous checks during treatment and frequent bilirubin testing to confirm response, requirements that naturally anchor demand in maternity wards and NICUs. In dermatology, full-body cabins and higher-throughput systems are primarily installed in specialist clinics and hospital departments, where providers can standardize safety procedures and manage scheduling across many patients.

In addition, the homecare settings segment is projected to grow at a CAGR of 8.2% during the forecast period.

Phototherapy Equipment Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Phototherapy Equipment Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 77.6 million, and is expected to reach USD 80.9 million in 2025. Growth in North America is largely replacement-and-upgrade driven, supported by sustained healthcare spending and a steady flow of dermatology and neonatal use cases. U.S. healthcare expenditure is projected to continue expanding through the decade, supporting capital refresh cycles for clinic-based UV systems and neonatal phototherapy platforms. On the product side, frequent FDA clearances keep the competitive set active and encourage providers to modernize equipment, particularly in targeted/UV systems used for psoriasis, vitiligo, and eczema. Together, higher spending capacity and continuous product availability sustain regional growth.

U.S. Phototherapy Equipment Market

In 2026, the U.S. market is projected to represent USD 74.6 million, capturing 29.0% of total global revenue.

Europe

Europe is expected to achieve a 3.5% growth rate in the coming years, the second-highest globally, reaching USD 78.7 million by 2026. Europe’s growth is anchored in public-system procurement, installed-base upgrades, and the scale of healthcare delivery across European Union markets, with the ongoing investment in hospital and outpatient infrastructure, where phototherapy cabins and panels are commonly deployed. Replacement demand is reinforced by structured tendering. In addition, neonatal phototherapy devices can accelerate standardized purchasing and upgrades across trusts.

U.K. Phototherapy Equipment Market

The U.K. market is projected to reach USD 10.9 million by 2026, accounting for 4.0% of the global market revenue.

Germany Phototherapy Equipment Market

Germany's market is projected to reach about USD 14.1 million by 2026, representing roughly 5.1% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 75.5 million, ranking as the third-largest globally. Asia Pacific growth is fueled by a larger neonatal care demand base, expanding hospital capacity, and rising adoption of dermatology phototherapy in urban outpatient networks. From a need perspective, WHO’s newborn mortality update highlights that neonatal risk remains concentrated in regions that include parts of Asia (with high neonatal mortality rates reported for Central/Southern Asia), keeping maternal-newborn care investment high, where phototherapy is a core, time-sensitive intervention for hyperbilirubinemia.

Japan Phototherapy Equipment Market

Japan is projected to generate approximately USD 10.2 million in revenue by 2026, contributing nearly 3.7% to the global market.

China Phototherapy Equipment Market

China’s market is projected to reach approximately USD 24.6 million by 2026, contributing about 9.0% to global revenues.

India Phototherapy Equipment Market

India is projected to contribute approximately USD 11.7 million by 2026, corresponding to about 4.3% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate phototherapy equipment market growth, with Latin America expected to reach around USD 19.4 million by 2026. Latin America is typically a “steady build” market growth and is supported by the gradual expansion of specialty outpatient care and the continued strengthening of maternal and child health services. Growth in Middle East & Africa is shaped by two powerful forces including the neonatal health priorities, especially in parts of Sub-Saharan Africa, and capacity expansion in higher-spend markets such as GCC.

GCC Phototherapy Equipment Market

By 2026, the GCC is expected to generate approximately USD 4.0 million in the market, accounting for nearly 1.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce Market Position of Prominent Players

The phototherapy equipment market is highly fragmented, split mainly between dermatology UV phototherapy and neonatal phototherapy. Key players such as GE HealthCare, Dräger, Natus Medical, and ATOM Medical held the largest market share.

Moreover, other key players, such as Phothera, Herbert Waldmann, STRATA Skin Sciences, and Shanghai SIGMA High-tech, compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve therapy outcomes.

LIST OF KEY PHOTOTHERAPY EQUIPMENT MARKET COMPANIES PROFILED IN REPORT

- GE HealthCare (U.S.)

- Dräger (Germany)

- Natus Medical (U.S.)

- ATOM Medical (Japan)

- Phothera (U.S.)

- Herbert Waldmann (Germany)

- STRATA Skin Sciences (U.S.)

- Shanghai SIGMA High-tech (China)

- Xuzhou Kernel Medical (China)

- Ningbo David Medical Device (China)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Mennen Medical received FDA clearance for BiliWrap. BiliWrap is the world’s first and only portable, disposable phototherapy system. The BiliWrap system treats unconjugated hyperbilirubinemia in neonates and premature babies.

- April 2025: APK Technology received FDA clearance for an Ultraviolet Phototherapy Device.

- March 2025: Boston Aesthetics received FDA clearance for a 308nm UV Phototherapy System. The 308nm UV Phototherapy System is intended to be used for the treatment of psoriasis, vitiligo, seborrheic dermatitis, atopic dermatitis, and leukoderma.

- February 2025: Shenzhen Kaiyan received FDA clearance for the CurrentBody LED 4-in-1 Zone Facial Mapping Mask. This Class II over-the-counter device is designed for targeted anti-aging, acne treatment, and skin rejuvenation.

- February 2025: Xuzhou Kernel Medical received FDA clearance for a 308nm Excimer Phototherapy Device. 308nm Excimer Phototherapy Device is intended to be used for the treatment of psoriasis and vitiligo.

- December 2024: Shanghai SIGMA High-tech received FDA clearance for a UV phototherapy device.

- December 2023: Daavlin received FDA clearance for DT Controlled Phototherapy Equipment. The DT Controlled Phototherapy Equipment is indicated for the treatment of diagnosed skin disorders.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.0% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product, Application, End-user, and Region |

|

By Product |

· Conventional Phototherapy Equipment · LED Phototherapy Equipment · Fiber Optic Phototherapy Equipment |

|

By Application |

· Skin Disease Treatment o Psoriasis o Vitiligo o Eczema o Others · Neonatal Jaundice Management |

|

By End-user |

· Hospitals & Clinics · Homecare Settings |

|

By Region |

· North America (By Product, By Application, By End-user, and By Country) o U.S. (By Product) o Canada (By Product) · Europe (By Product, By Application, By End-user, and By Country/Sub-region) o Germany (By Product) o U.K. (By Product) o France (By Product) o Spain (By Product) o Italy (By Product) o Scandinavia (By Product) o Rest of Europe (By Product) · Asia Pacific (By Product, By Application, By End-user, and By Country/Sub-region) o China (By Product) o Japan (By Product) o India (By Product) o Australia (By Product) o Southeast Asia (By Product) o Rest of Asia Pacific (By Product) · Latin America (By Product, By Application, By End-user, and By Country/Sub-region) o Brazil (By Product) o Mexico (By Product) o Rest of Latin America (By Product) · Middle East & Africa (By Product, By Application, By End-user, and By Country/Sub-region) o GCC (By Product) o South Africa (By Product) o Rest of the Middle East & Africa (By Product) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 259.9 million in 2025 and is projected to reach USD 407.0 million by 2034.

In 2025, the market value stood at USD 80.9 million.

The market is expected to exhibit a CAGR of 5.0% during the forecast period of 2026-2034.

The conventional phototherapy equipment segment led the market by product.

The key factors driving the market are the rising prevalence of chronic skin conditions.

GE HealthCare, Drager, Natus Medical, and ATOM Medical are some of the major players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us