Piezoelectric Materials Market Size, Share & Industry Analysis, By Material (Piezoceramics {PZT and Lead-free Ceramics}, Piezopolymers, Piezocomposites, and Others), By Application (Actuators, Motors, Transducers, Sensors, SONAR, Generators & Transformers, Acoustic Devices, Resonators, and Others), By End-use Industry (Automotive, Healthcare, IT & Telecom, Consumer Goods, Aerospace & Defense, and Others), and Regional Forecast, 2025-2032

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

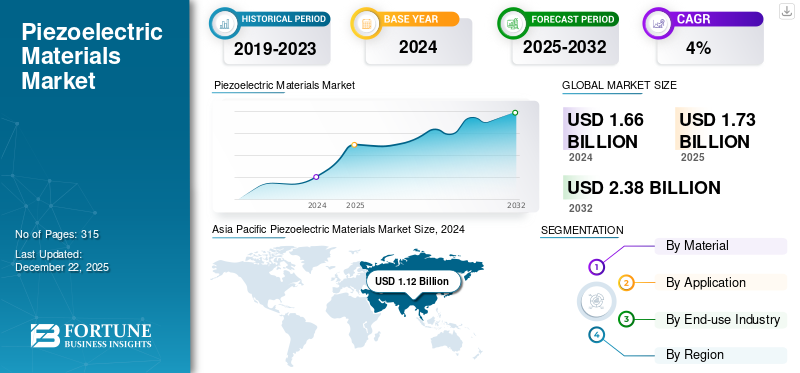

The global piezoelectric materials market size was valued at USD 1.66 billion in 2024. The market is projected to grow from USD 1.73 billion in 2025 to USD 2.38 billion by 2032, exhibiting a CAGR of 4.64% during the forecast period (2025-2032). Asia Pacific dominated the piezoelectric materials market with a market share of 67.47% in 2024.

Piezoelectricity is a property exhibited by few materials, which produces an electric field when a force is applied. On the other hand, when an electric field is applied across the material, it displays deformation in its dimensions. These materials convert mechanical energy to electrical energy and vice versa. Due to this property, they are referred to as transducers. These materials use piezoelectricity to measure changes in speed, strain, stress, force, or heat by converting the differential in energy into electrical charge. Based on this effect, such materials find application in producing and detecting sound and frequency, SONAR, ignition devices, and pressure & displacement measurement systems.

Currently, piezoelectric devices employ a wide variety of materials such as Rochelle salt, quartz crystal, ceramics, macro-fiber composites, polymers, flexoelectric materials, and ferroelectrets. The selection of material for different applications is based on properties such as stability, consistency, malleability, high input-to-output ratio, and heat & humidity resistance. Primarily, quartz crystals were employed in piezoelectric devices. However, its inability to react at low voltages and function at temperatures above 300ᵒC obligated its replacement by modern materials such as piezo composites and piezoceramics.

The consumer goods sector is a significant driver of the market. Growing purchasing power, high living standards, and rapid urbanization in several developed and developing countries are expected to drive the consumer goods sector, thereby driving product demand in the coming years.

Furthermore, companies operating in the market have modified their production plants to accommodate the growing demand from the healthcare industry. They have also developed novel products in combination with healthcare electronics manufacturers to study coronavirus and its traits. For instance, PI Ceramics developed piezoceramics that enable precise liquid handling for in vitro diagnostics for early diagnosis and disease detection. PI Ceramics GmbH, L3Harris Technologies, Inc., CeramTec, TDK Corporation, and Solvay are key players operating in the market.

Download Free sample to learn more about this report.

Global Piezoelectric Materials Market Overview

Market Size & Forecast:

- 2024 Market Size: USD 1.66 billion

- 2025 Market Size: USD 1.73 billion

- 2032 Forecast Market Size: USD 2.38 billion

- CAGR: 4.6% from 2025–2032

Market Share:

- Asia Pacific dominated the Piezoelectric Materials Market with a 67.47% share in 2024, driven by its position as a global manufacturing hub for electronics, consumer goods, and increasing government incentives for domestic production in China, India, Japan, South Korea, and Taiwan.

- By material, Piezoceramics are expected to retain the largest market share in 2025, supported by their high sensitivity, adaptability via doping, and widespread use in actuators, transducers, and sensors across the electronics and automotive industries.

Key Country Highlights:

- China: Leads regional market growth due to strong consumer electronics and automotive manufacturing base and government-led production incentives.

- United States: Rising aerospace and healthcare sectors, including space exploration and precision diagnostic devices, drive piezoelectric material demand.

- Japan: Significant investments in advanced consumer electronics and miniaturized sensing devices fuel domestic consumption.

- India: Rapid growth in consumer goods, telecom, and automotive sectors expands demand for piezoelectric sensors and actuators.

- Germany: Resurgence in automotive R&D, including electric and autonomous vehicles, supports demand for advanced sensing and control technologies.

- Brazil/Mexico: Expanding IT & telecom presence supports moderate growth in demand for piezoelectric sensors and actuators.

- UAE/South Africa: Growing electronics and healthcare sectors in the Middle East & Africa are driving demand for piezoelectric components in diagnostic and monitoring devices.

Piezoelectric Materials Market Trends

Development of Lead-Free Piezoceramics has Emerged as a Growing Trend in the Market

While lead zirconate titanate (PZT) is the most widely used piezoceramic material, its usage is constrained due to the presence of lead in the compound, which subjects PZT to regulations such as the Restrictions of Hazardous Substances (RoHS) Directive 2002/95/EC adopted by the EU. Therefore, the development of lead-free piezoceramics is a large, ongoing research area. Lead-free piezoceramics consist of three main compositional families: alkaline niobate perovskite-based ceramics, titanate-based ceramics, and bismuth perovskite-based ceramics. Furthermore, polymers showing piezoelectric properties, including polysulfone and polyvinylidene fluoride (PVDF), are under study to provide compliant product materials. As lead is considered to be poisonous to humans, such research on the replacement of lead-based ceramics is expected to gain further momentum in the near future and alter the course of the market toward further growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Demand for Automation in End-Use Industries to Boost Market Growth

End-use industries such as automotive and electronic manufacturing have pushed for automation in their manufacturing lines. This push has increased demand for devices such as sensors, transducers, actuators, and motors to run the production line smoothly. As these devices use properties endowed by the product materials to measure various quantities such as pressure, strain, acceleration, and acoustic intensity, the demand for such materials is projected to expand considerably with the increasing dependence of industries on automation.

Over the years, major manufacturing companies have expanded their investments in introducing automation systems as an effective method to minimize running costs during development. The growing importance of automation in manufacturing industries to improve productivity and minimize lead time is projected to encourage the use of sensors, transducers, actuators, and motors. This is anticipated to boost the demand for piezoelectric materials during the forecast period.

Increasing Spending on Aerospace & Defense to Encourage Product Demand

In recent years, governments of India, China, the U.S., Israel, and Japan have significantly increased their budget on defense activities. These governments invest heavily in building missile guidance systems, radars, and drones to strengthen their armed forces’ capabilities. Furthermore, an increase in space exploration activities has led to an increase in the usage of devices such as sensors, acoustic devices, and SONARs to study space objects and related environments. These devices require special product materials that can detect the slightest change in their range, sustain in harsh conditions, and provide accurate & consistent results. With private space agencies such as SpaceX taking a jump into providing space exploration services, the demand for such materials is expected to inflate the global piezoelectric materials market growth during the forecast period.

The demand for military equipment is on the rise as governments across the globe are focused on military modernization amid rising global security issues. The uncertainty and continuing ambiguity of the current international security climate are expected to increase current defense investment over the next five years.

The global commercial space market is expected to witness steady investment in new and current space technology and facilities, with funding coming mainly from governments and venture capital. Sales in the commercial space industry arise mainly from the production of satellites used for Earth observation and communications, from launch vehicles used to position these payloads in orbit.

Market Restraints

Lack of Differentiation between Signals and Noise to Diminish Adoption of Piezoelectric Materials

While piezo materials find extensive application in sensing and energy conversion devices, common materials such as PZT and natural piezo crystals are unable to differentiate between actual signals and noise present in the system, which may result in an inaccurate outcome, affecting the performance of the device where the piezoelectric material is employed. Furthermore, when subjected to harsh environments such as heavy stress and high temperature, the consistency of results provided by the material is severely affected, further restricting its adoption for application in different conditions.

Market Opportunities

Advances in Energy Harvesting Using Piezoelectric Materials May Create Market Growth Opportunities

Energy harvesting and sustainability initiatives are expected to create various market growth opportunities. As global energy consumption continues to rise and environmental concerns intensify, industries are seeking innovative, efficient, and sustainable solutions to generate and conserve energy.

The product materials, capable of converting mechanical stress, such as ambient vibrations and mechanical movements, into electrical energy, offer an attractive, low-maintenance alternative to traditional power sources.

These materials can be integrated into devices that harvest energy from various sources, including industrial machinery, vehicular motion, foot traffic on urban walkways, and even natural phenomena such as wind-induced vibrations in bridges and buildings. This technology is particularly useful in remote or low-power applications where conventional electricity grids may be impractical or too expensive.

Market Challenges

High Manufacturing Costs Challenge Market Growth

The production of advanced product materials, such as single crystals and textured ceramics, involves complex processes including Templated Grain Growth (TGG), requiring expensive raw materials, significant energy, and skilled labor. This leads to high production costs and affects pricing strategies, limiting availability, especially in price-sensitive markets. High manufacturing costs present a significant challenge for players in the market, affecting production and pricing strategies.

Impact of COVID-19

Stalled End-use Industry Due to Pandemic Impacted Market Growth

The outbreak of the COVID-19 pandemic negatively impacted the growth of the market. Disruption of the supply chains caused a shortage of raw materials and lowered production. Moreover, restrictions on transportation imposed by the governments of different countries also contributed to the decline in market growth during the pandemic. Crucial end-use industries such as the electronics and automotive sectors faced restricted operations and shutdowns, which critically impacted the demand for products in the market. However, COVID-19 presented a spike in demand for equipment such as pyrometers, oximeters, automated ventilators, and electronic thermometers. These devices utilize piezo materials to convert one form of energy to another and thus demand the product during this crisis.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Policies such as the U.S.-led semiconductor export controls and China's retaliatory mineral restrictions directly affect the piezoelectric material availability. The Trump-era tariffs further complicate cross-border trade, increasing costs for manufacturers reliant on global supply chains.

Segmentation Analysis

By Material

Piezoceramics Material Segment to Hold Dominant Share in the Market Due to its Excellent Piezoelectric Properties

Based on material, the market is classified into piezoceramics, piezopolymers, piezocomposites, and others. Piezoceramics are further bifurcated into lead zirconate titanate (PZT) and lead-free ceramics.

Piezoceramics are expected to hold the dominant share of the market due to its excellent piezoelectric properties, including high sensitivity and operating temperature. The consumption of PZT is increasing for the manufacturing of transducers and actuators, as the performance of PZT can be easily modified based on the usage of doping materials. While doping with niobium produces soft-PZT, which increases its response capabilities, doping with iron forms hard-PZT, which shows negligible hysteresis in the piezoelectric response. Such adaptability of piezoceramic materials has resulted in their large-scale consumption in the electronics and automotive industries. The segment captured 67% of the market share in 2024.

On the other hand, piezo composites are swiftly gaining market share as they are preferable for application in ultrasonic equipment, non-destructive testing, and underwater acoustics. Composites offer smaller acoustic impedance than piezoceramics, are more plastic, and can better adapt to mechanical loads. They possess better piezoelectric sensitivity and electromechanical activity and thus are considered to be effective alternatives to piezoceramics.

By Application

Sensors Segment to Grow with the Highest CAGR Due to Its Application in Various Fields

In terms of application, the market is segmented into actuators, motors, transducers, sensors, SONAR, generators & transformers, acoustic devices, resonators, and others.

The sensors segment is expected to grow at a considerable CAGR owing to its application in various fields, including automatic vehicles, manufacturing lines, and consumer electronics. Sensors detect the change in energy and convert the difference into electrical signals, which are used to make necessary changes in the system. For instance, the TV's remote control has a pressure sensor, which detects the pressure on a button and converts it into an electrical signal that activates the IR blaster present on the remote. Inside the television unit, the IR sensor detects the change in energy and converts it into a digital signal, providing control of the unit. The automotive and healthcare sectors are significant drivers of the piezoelectric sensors market. In automotive applications, piezoelectric sensors are used in collision detection, active safety systems, and tire pressure monitoring. In healthcare, they are used in ultrasonic imaging, pacemakers, and hearing aids.

On the other hand, an actuator converts electrical signals sent by the system or user into mechanical energy to control the designated part to perform a certain action in the manufacturing line. Thus, the actuators segment is expected to account for the largest piezoelectric materials market share in the global market, with its application ranging from precision control of industrial machining tools, vehicle acceleration & braking systems, and robotic arms used in various end-use industries. The segment is set to capture 30% of the market share in 2025.

The transducers segment is likely to grow with a substantial CAGR of 4.80% during the forecast period (2025-2032).

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Consumer Goods to Account for Largest Share Due to Wide Range of Applications

Based on end-use industry, the market is segmented into automotive, healthcare, IT & telecom, consumer goods, aerospace & defense, and others.

Consumer goods such as TVs, washing machines, remote-controlled toys, and microwaves utilize piezo materials to provide control and operation of these products. With the large-scale consumption of such consumer goods expected with improving consumer spending capacity in emerging economies, this market segment is expected to maintain its lead in the global market. The segment is predicted to capture the market share of 60% in 2025.

The automotive industry is trailing the consumer goods industry. It is projected to grow at a stable CAGR during the forecast period owing to the requisition of these materials for actuators, fuel injectors, sensors, and braking systems present in the automobile. Furthermore, fuel atomizers, seat belt buzzers, airbag sensors, and tire pressure sensors are a few major automotive parts wherein these materials find application, thus resulting in the automotive industry holding a considerable share of the global market. The segment is set to grow with a considerable CAGR of 4.25% during the forecast period (2025-2032).

PIEZOELECTRIC MATERIALS MARKET REGIONAL OUTLOOK

Asia Pacific

Asia Pacific Piezoelectric Materials Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market size in Asia Pacific stood at USD 1.06 billion in 2023 and USD 1.12 billion in 2024. Asia Pacific is projected to be the dominant region during the forecast period. The region emerged as a manufacturing hub for electronics and consumer goods, with China, Japan, Taiwan, India, and South Korea focusing on expanding their production capabilities. China is expected to reach a market value of USD 0.74 billion in 2025. Governments of countries in the Asia Pacific are providing tax rebates and incentives to electronics manufacturers setting up newer production plants after the slowdown caused by COVID-19. They shall further expand the market size during the forecast period. India is estimated to reach USD 0.06 billion in 2025, while Japan is foreseen to reach USD 0.11 billion in the same year.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is the second largest market expected to hold a valuation of and USD 0.23 billion in 2025, exhibiting a CAGR of 2.88% during the forecast period (2025-2032). The region shall provide growth opportunities for the market owing to the growth in the aerospace and healthcare industries. The U.S. is planning extensive space exploration programs, wherein product materials will be utilized in sensing objects in space and remote access of the spacecraft components. Thus, the rising aerospace industry in the country is expected to surge market growth. The U.S. market is set to be worth USD 0.20 billion in 2025.

Europe

Europe is the third largest market expected to gain USD 0.19 billion in 2025. The automotive sector in this region is expected to rejuvenate after the slowdown caused by the coronavirus pandemic. The U.K. market is estimated to reach USD 0.01 billion in 2025. Studies regarding driverless, automated cars shall also expand in the region, providing a boost to the market. Germany is poised to grow with a valuation of USD 0.06 billion in 2025, while France is anticipated to hold USD 0.02 billion in the same year.

Latin America

Latin America is the fourth largest market estimated to be valued at USD 0.07 billion in 2025. While the market in Latin America is still in its infancy, the growing presence of end-use industries, especially IT & telecom, in the region shall result in the expansion of the market.

Middle East & Africa

On the other hand, the Middle East & Africa have observed an increasing demand for piezo materials due to the region's expanding electronics and healthcare industries. The GCC market is expected to expand and reach a valuation of USD 0.17 billion in 2025.

Competitive Landscape

Key Market Players

Focus on Product Development by Key Players to Maintain a Strong Stance in the Market

The competitive landscape depicts a fairly consolidated market with a handful of manufacturing companies accounting for a majority share. Key players are investing a large number of resources in the research and development of novel materials and their applications as a course to gain market share.

Furthermore, key players operating in the market have adopted the strategy of capacity expansion and acquisition of smaller enterprises to improve their offering portfolio and services. This trend is projected to positively impact the global market during the forecast period.

LIST OF KEY PIEZOELECTRIC MATERIALS COMPANIES

- PI Ceramics GmbH (Germany)

- APC International, Ltd. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- CeramTec (Germany)

- Arkema (France)

- Solvay (Belgium)

- Sparkler Ceramics (India)

- Piezomechanik GmbH (Germany)

- TDK Corporation (Japan)

- Hong Kong Piezo Co. Ltd. (China)

- Mide Technology (U.S.)

- Meggitt PLC (U.K.)

- HOERBIGER Motion Control GmbH (Germany)

- Piezo Kinetics Inc. (U.S.)

- TRS Technologies, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025 – CeramTec developed a new bismuth sodium titanate-barium titanate (BNT-BT) based lead-free piezoceramic, and it has great potential for medical applications.

- December 2024 – PI Ceramic introduced a new fully automated production line for multilayer technology to accelerate the production of small-scale series and prototype development projects. The company has invested around USD 1.08 million in the development and installation of this new production line with the goal of cutting its time for sample production by half and increasing flexibility in the manufacturing of piezoceramics.

- October 2022 – PI Ceramic invested USD 16.24 million to construct a new building in Lederhose, Germany. This move has increased the company’s production capacity of high-quality piezo components by approximately 50 percent. The company aims to continue to invest in capacity expansion, considering the rise in demand for its products and solutions.

- April 2020 – CTS Corporation announced the expansion of its product portfolio by introducing four crystal families for application in automotive-grade crystal resonators. The newly developed products shall find application in automotive, industrial, medical, and aerospace & defense industries, wherein a wide range of operating temperatures is present, and provide the company with excellent growth opportunities in the near future.

- July 2019 – PI Ceramic GmbH announced the expansion of its production facility present in Lederhose, Thuringia. The expansion shall increase the facility’s area from 12,000 sq m. to 19,500 sq m. The additional area is to have an additional line for the production of multilayer product materials and an administrative center.

REPORT COVERAGE

The global market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, materials, end-use industries, and applications. Besides this, the research report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the growth rate of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Unit |

Volume (Million Cubic Centimetres) and Value (USD Billion) |

|

Growth Rate |

CAGR of 4.6% from 2025 to 2032 |

|

Segmentation |

By Material

|

|

By Application

|

|

|

By End-use Industry

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.66 billion in 2024 and is projected to reach USD 2.38 billion by 2032.

Growing at a CAGR of 4.6%, the market will exhibit steady growth during the forecast period (2025-2032).

The consumer goods segment is the leading end-use industry in the market.

Considerable investments by countries such as India, China, and the U.S. in space exploration activities to improve the strength of their military are a key factor in boosting this markets growth.

Asia Pacific held the highest market share in 2024.

The focus of automotive and electronics manufacturing companies on automation of manufacturing plants to reduce the occurrence of product failures, coupled with high demand for consumer electronics are factors expected to enhance the adoption of these materials.

- 2019-2032

- 2024

- 2019-2023

- 315

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us