Passenger Cars Market Size, Share & Industry Analysis, By Vehicle Type (Hatchbacks, Sedans and SUVs & Crossovers), By Propulsion (ICE and Electric), By Vehicle Class (Economy, Mid-Range and Premium), By Size (Small, Mid-Size, and Large), By Drivetrain (Rear-Wheel Drive, Front-Wheel Drive, All-Wheel Drive, and Four-Wheel Drive), and Regional Forecasts, 2026-2034

(Offer valid till 15th Aug 2026)

Passenger Cars Market Overview

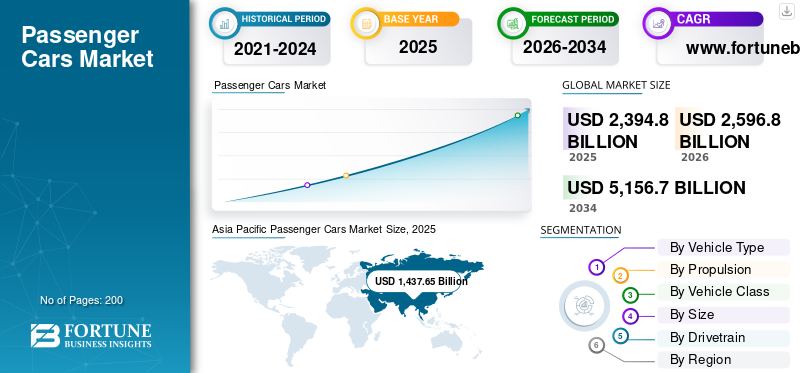

The passenger cars market size was valued at USD 2,394.8 billion in 2025. The market is projected to grow from USD 2,596.8 billion in 2026 to USD 5,156.7 billion by 2034, exhibiting a CAGR of 9.0% during the forecast period. Asia Pacific dominated the passenger cars market with a market share of 60.03% in 2025.

The market represents the worldwide production, sales, and use of vehicles designed mainly for personal mobility, including hatchbacks, sedans, SUVs, and crossovers. It is closely linked with the automotive industry, urbanization, rising disposable incomes, financing availability, and changing consumer preferences. The growing demand for passenger cars in emerging economies is a result of more household shifts from two-wheelers or public transport to private vehicles. In mature economies, replacement demand, connected features, safety technologies, and electrified models are supporting the market’s growth.

The industry is expected to evolve through electrification, software-defined vehicles, hybrid powertrains, connected services, and smarter manufacturing. Electric vehicle adoption will rise strongly, however ICE vehicles will remain relevant in several regions due to affordability, infrastructure limits, and consumer familiarity. SUVs and utility vehicles will continue gaining traction as buyers prefer higher seating, larger cabins, perceived safety, and versatile usage.

Passenger cars are used for personal commuting, family mobility, corporate fleets, ride-hailing, rental services, and premium lifestyle transportation. Growth will also be supported by fuel efficiency improvements, hybridization, lightweight materials, and localized automobile manufacturing. However, raw material prices, battery costs, fuel prices, interest rates, and supply chain pressure can influence affordability.

Key players such as Ford Motor Company and General Motors are investing in EV platforms, hybrid SUVs, digital cockpits, and flexible production networks to address changing consumer demands and expand passenger car sales.

Download Free sample to learn more about this report.

PASSENGER CARS MARKET TRENDS

SUVs and Crossovers Reshape Global Passenger Car Preferences

A major trend is the continued shift toward SUVs and crossovers. Consumers prefer utility vehicles as they offer higher seating, cargo flexibility, road presence, and family usability. Automakers are responding with compact SUVs, electric SUVs, hybrid crossovers, and premium AWD models. This trend is raising average selling prices and strengthening value growth across the market.

- In 2023, IEA analysis showed SUVs reached nearly half of global car sales, confirming the structural shift toward larger passenger vehicles.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Household Mobility Needs and SUV Demand Accelerate Passenger Car Sales

The market is growing as rising disposable incomes, urban expansion, financial access, and lifestyle upgrades increase private vehicle ownership. Consumers are demanding safer, more spacious, and technology-rich cars, especially SUVs and crossovers. Strong demand from China, India, the U.S., and emerging markets supports passenger car sales, while hybrid and EV launches are helping automakers meet fuel economy and emission requirements.

- In May 2025, Toyota revealed the new RAV4 with hybrid and plug-in hybrid powertrains, strengthening demand for electrified compact SUVs.

MARKET RESTRAINTS

High Ownership Costs and Raw Material Volatility Limit Affordability

Rising vehicle prices, higher borrowing costs, insurance expenses, and volatile raw material prices are limiting affordability, especially for first-time buyers. Battery minerals, steel, aluminum, semiconductors, and logistics costs can raise production expenses. In price-sensitive regions, this slows replacement cycles and delays upgrades from used vehicles or two-wheelers to new passenger cars.

MARKET OPPORTUNITIES

Electric and Hybrid Cars Create Growth across Emerging Markets

Electrification creates a strong opportunity as governments, automakers, and consumers shift toward lower-emission vehicles. Electric vehicle EV sales are expanding through falling battery costs, Chinese exports, charging growth, and policy support. Hybrid vehicles also offer a practical bridge where charging infrastructure is limited. This supports market expansion without relying only on conventional ICE growth.

- In May 2025, IEA projected electric car sales above 20 million in 2025, representing more than one-quarter of global car sales.

MARKET CHALLENGES

EV Infrastructure and Policy Uncertainty Slow Transition Speed

The market faces challenges from uneven charging infrastructure, changing subsidies, grid readiness, and uncertain emissions policy. These issues can slow EV adoption, especially outside China and Europe. Automakers must balance ICE, hybrid, and EV investments while protecting margins. Delays in charging expansion may also reduce consumer confidence in fully electric passenger cars.

- For instance, in 2025, IEA highlighted uncertainty in the U.S. EV outlook, with sales expected at only around 11% of total car sales.

Segmentation Analysis

By Vehicle Type

SUVs and Crossovers Dominate Due to Utility and Premium Appeal

On the basis of vehicle type, the market is segmented into hatchbacks, sedans and SUVs & crossovers.

SUVs and crossovers dominate by holding the largest passenger cars market share as consumers prefer spacious cabins, higher ground clearance, flexible cargo space, and stronger safety perception. These vehicles also command higher ASPs (Average Selling Prices), improving automaker margins. Increased demand for compact SUVs in Asia and premium utility models in North America has shifted model portfolios away from hatchbacks and sedans.

- In May 2025, Toyota’s redesigned RAV4 emphasized hybrid and plug-in hybrid utility, showing OEM focus on electrified SUV demand.

The sedans segment is expected to grow at a CAGR of 8.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

ICE Dominates Due to Cost and Infrastructure Advantage

On the basis of propulsion, the market is segmented into ICE and electric.

ICE vehicles dominate as they are affordable, widely available, and support existing fueling infrastructure. In Latin America, Africa, India, and parts of Southeast Asia, charging gaps and price sensitivity keep ICE relevant. Hybrids are also extending combustion-based platforms while improving fuel efficiency, allowing OEMs to meet near-term consumer demands.

The electric segment is expected to grow at a CAGR of 14.5% over the forecast period.

By Vehicle Class

Mid-Range Vehicle Class Leads through Affordability and Features

On the basis of vehicle class, the market is segmented into economy, mid-range, and premium.

The mid-range vehicle class dominates as they balance price, comfort, technology, and practicality. This segment includes popular sedans, compact SUVs, and crossovers that meet family and commuting needs. Buyers are moving above entry-level models for safety, infotainment, automatic transmission, and hybrid options, however many still avoid premium pricing.

- In 2025, Chevrolet Equinox EV production continued in Mexico, supporting mid-range electric crossover availability for mainstream buyers.

The premium segment is expected to grow at a CAGR of 10.9% over the forecast period.

By Size

Mid-Size Cars Dominate Through Family and Urban Use

On the basis of size, the market is segmented into small, mid-size, and large.

Mid-size cars dominate as they suit both city driving and family travel. They offer better comfort than small cars while remaining more affordable than large premium vehicles. Compact SUVs, mid-size sedans, and crossovers form the core of global demand, especially in China, Europe, India, and North America.

- In 2025, Cadillac Lyriq and Chevrolet Blazer/Equinox EV platforms showed how mid-size electric crossovers are expanding mainstream and premium demand.

The large segment is expected to grow at a CAGR of 11.3% over the forecast period.

By Drivetrain

Front-Wheel Drive Dominates Through Cost and Efficiency

Based on drivetrain, the market is sub-divided into rear-wheel drive, front-wheel drive, all-wheel drive, and four-wheel drive.

Front-wheel drive dominates as it is affordable, lighter, space-efficient, and common in hatchbacks, sedans, and compact SUVs. It supports fuel efficiency and suits urban markets where affordability matters. AWD is growing in SUVs and EVs, but FWD remains the volume leader across Asia, Europe, and Latin America.

- For instance, in 2025, Toyota’s bZ3X electric compact crossover in China used a front-motor, front-wheel-drive layout, reflecting cost-efficient EV packaging.

The all-wheel drive segment is anticipated to register a CAGR of 13.2% over the forecast period.

Passenger Cars Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

Asia Pacific

Asia Pacific Passenger Cars Market Size, 2025 (USD Billion

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 1,437.6 billion, and also maintained the leading share in 2024, with USD 1,267.5 billion. The region dominates due to China’s scale, India’s rising ownership, Japan’s hybrid strength, and South Korea’s export-oriented OEM base. China, Japan, and South Korea remain central to automobile manufacturing, while India and ASEAN add high-volume growth from rising disposable incomes. Asia Pacific also leads EV adoption, compact SUV demand, and localized production, giving it the largest market share in global passenger car sales.

- In 2025, IEA projected China’s electric cars to reach around 60% of total car sales, supporting APAC’s leadership.

China Passenger Cars Market

China’s market is projected to be one of the largest, with 2025 revenues hitting USD 1,044.8 billion, representing roughly 43.6% of the global market.

India Passenger Cars Market

In 2025, India reached around USD 85.3 billion, accounting for roughly 3.6% of the global revenues.

Europe

Europe is estimated to reach USD 573.2 billion in 2026 and secure second position in the market. The region will grow through electrification, hybrid adoption, premium vehicles, and regulatory pressure on emissions. Germany, the U.K., France, Italy, and Spain remain important markets, while the rest of Europe adds recovery-led demand. Strong charging networks, company-car policies, and premium OEMs support EV and hybrid penetration, though affordability pressure and slower economic growth may limit rapid volume expansion.

Germany Passenger Cars Market

Germany achieved USD 141.5 billion in 2025, accounting for roughly 5.9% of global revenues.

U.K. Passenger Cars Market

In 2025, the U.K. market captured around USD 95.1 billion, accounting for roughly 4.0% of global revenues.

North America

North America is projected to record a growth rate of 5.9% in the coming years, and reach a valuation of USD 212.3 billion in 2026, mainly through value expansion rather than strong unit growth. The U.S. market is mature, but SUVs, premium crossovers, EVs, and technology-rich models lift average selling prices. The U.S. remains heavily utility-focused, while Canada follows similar trends and Mexico benefits from manufacturing and affordability-led demand.

U.S. Passenger Cars Market

Based on North America’s strong contribution and the U.S.’ dominance within the region, the U.S. market is estimated at around USD 200.6 billion for 2025, representing roughly 8.4% of the global market.

Latin America

Latin America is projected to record a growth rate of 11.6% in the coming years, and reach a valuation of USD 81.6 billion by 2026. The region will grow through recovery in Brazil, Argentina, Chile, Colombia, and Mexico-linked supply chains. Compact cars remain important, but SUV and crossover demand is rising as consumers upgrade. Financial availability, urbanization, Chinese EV imports, and better model supply will support growth, although currency volatility and interest rates remain constraints.

Middle East & Africa

The Middle East & Africa is projected to record a growth rate of 13.4% in the coming years, and reach USD 123.3 billion in 2026. The region will grow through GCC premium SUV demand, Turkey’s large vehicle base, and rising motorization in Africa. Saudi Arabia and UAE favor larger SUVs and luxury vehicles, while South Africa and North Africa support compact and mid-range demand. Infrastructure expansion, population growth, and fleet replacement will support long-term passenger cars market growth in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Automakers Compete Through Electrification, Scale, and Product Renewal

The competitive landscape of the market is shaped by large global OEMs, regional manufacturers, EV specialists, and premium brands. Companies compete through product launches, pricing, localization, electrification, connected technologies, and flexible manufacturing. Toyota, Volkswagen, Hyundai, BYD, Stellantis, general motors, ford motor company, Honda, Nissan, BMW, and Mercedes-Benz are strengthening their portfolios with hybrids, BEVs, premium SUVs, and software-led features.

Automakers are increasingly using modular platforms to lower development cost and launch multiple models faster. EV-focused players are expanding through battery partnerships, direct sales, and software upgrades, while legacy OEMs are defending scale through hybrid technology and global distribution. In China, price competition and fast model cycles are reshaping strategies. In Europe, emissions rules are pushing EV and hybrid launches. In North America, large SUVs, crossovers, and premium EVs remain key profit pools.

Competitive advantage now depends on battery sourcing, digital architecture, brand trust, safety features, production flexibility, and the ability to satisfy growing demand across different price points. Companies are also targeting affordability because customers are sensitive to high interest rates and raw material prices.

- In October 2024, Hyundai began producing the 2025 IONIQ 5 at its USD 7.6 billion Georgia Metaplant to localize U.S. EV SUV supply.

LIST OF KEY PASSENGER CARS COMPANIES PROFILED

- Toyota Motor Corporation (Japan)

- Volkswagen Group (Germany)

- Hyundai Motor Company (South Korea)

- Kia Corporation (South Korea)

- BYD Company Limited (China)

- Honda Motor Co., Ltd. (Japan)

- Nissan Motor Co., Ltd. (Japan)

- Stellantis N.V. (Netherlands)

- General Motors (U.S.)

- Ford Motor Company (U.S.)

- Tesla, Inc. (U.S.)

- BMW Group (Germany)

- Mercedes-Benz Group AG (Germany)

- Renault Group (France)

- Geely Automobile Holdings (China)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Stellantis announced a five-year strategy involving nearly USD 70 billion in investment to accelerate electrification, software integration, and passenger vehicle innovation. The company plans to introduce 60 new models by 2030, including 29 fully electric vehicles, while expanding EV production and digital mobility capabilities across major global markets.

- December 2025: Nissan began production of the third-generation Leaf EV at its Sunderland plant in the U.K. The model is linked to a USD 600 million investment and offers up to 386 miles of range.

- September 2025: BMW unveiled the Neue Klasse iX3 electric SUV. The vehicle introduced 800V architecture, up to 805 km WLTP range, and 400 kW fast charging.

- May 2025: Stellantis unveiled the all-new Jeep Compass on the STLA Medium platform. It offers mild hybrid, plug-in hybrid, and battery-electric powertrain options.

- March 2025: Volkswagen launched the Tera subcompact SUV in Brazil. The model is also planned for South African production, strengthening Volkswagen’s emerging-market SUV portfolio.

- March 2025: Hyundai Motor Group confirmed that its Georgia Metaplant America facility would target annual production capacity of 500,000 electric and hybrid vehicles. The expansion supports growing North American EV demand and strengthens Hyundai’s regional manufacturing footprint for passenger SUVs, crossovers, and next-generation electrified vehicles.

- March 2025: BYD launched the Sealion 05 EV in China. The compact electric SUV includes BYD’s God’s Eye C driver-assistance system and up to 520 km CLTC range.

REPORT COVERAGE

The global passenger cars market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Propulsion, Vehicle Class, Size, Drivetrain, and Region |

| By Vehicle Type |

|

| By Propulsion |

|

| By Vehicle Class |

|

| By Size |

|

| By Drivetrain |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2,394.8 billion in 2025 and is projected to reach USD 5,156.7 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 1,437.6 billion.

The market is expected to exhibit a CAGR of 9.0% during the forecast period.

SUVs & crossovers segment led the market based on vehicle type.

Rising household mobility needs and SUV demand is one of the key factors driving the global market.

Toyota Motor Corporation, Hyundai Motor Company, Ford Motor Company, and Kia Corporation are some of the top players in the market.

In terms of share, Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us