Plant-Based Packaging Market Size, Share & Industry Analysis, By Material (Bioplastics, Bagasse, Paper & Paperboard, Cellulose, Starch-based, and Others), By Packaging Type (Rigid Packaging and Flexible Packaging), By End-use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare, and Others), and Regional Forecast, 2026-2034

Plant-Based Packaging Market Size and Future Outlook

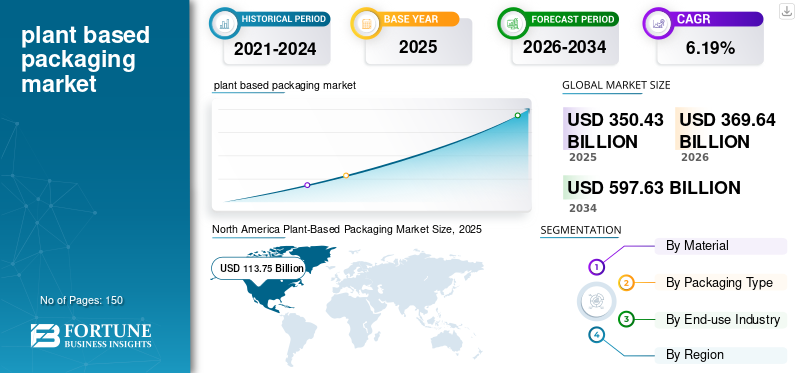

The global plant-based packaging market size was valued at USD 350.43 billion in 2025. The market is projected to grow from USD 369.64 billion in 2026 to USD 597.63 billion by 2034, exhibiting a CAGR of 6.19% during the forecast period. North America dominated the global plant-based packaging market with a market share of 32.46% in 2025.

The global plant-based packaging industry refers to the sector dedicated to the creation, manufacturing, and distribution of packaging materials sourced from renewable, biological, and non-fossil-based origins, including corn starch, sugarcane, bamboo, bagasse, algae, wood pulp, and various forms of agricultural or organic biomass. These packaging options are designed to offer sustainable alternatives to conventional petroleum-derived plastics, featuring advantages such as biodegradability, compostability, recyclability, and a reduced environmental impact. The growing consumer demand for plant-based packaging is fostering market growth.

Furthermore, the market is dominated by several major players, including Amcor Plc, Tetra Pak, and Gerresheimer AG, at the forefront. A broad portfolio, innovative product launches, and strong initiatives aimed at the expansion of geographical presence have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

PLANT-BASED PACKAGING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 350.43 billion

- 2026 Market Size: USD 369.64 billion

- 2034 Forecast Market Size: USD 597.63 billion

- CAGR: 6.19% from 2026–2034

- North America dominated the global plant-based packaging market with a market share of 32.46% in 2025.

- The bagasse material segment is expected to grow at a CAGR of 6.30% over the forecast period.

- The flexible packaging segment is expected to grow at a CAGR of 5.66% over the forecast period.

North America

North America held the dominant market share in 2024, valued at USD 107.61 billion, and maintained its leading position in 2025, with a value of USD 113.75 billion.

Europe

The European region recorded a growth rate of 5.92%, the second-highest among all regions, and reached a valuation of USD 86.31 billion in 2025.

Asia Pacific

The market in the Asia Pacific reached a valuation of USD 66.23 billion in 2025.

U.S.

In 2025, the U.S. market is estimated to reach USD 91.35 billion.

Japan

Japan’s plant-based packaging market is expanding steadily through growing sustainability initiatives, increasing demand for biodegradable materials, and corporate efforts to reduce packaging waste in line with circular economy objectives.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Consumer Preference for Sustainable & Eco-Friendly Packaging to Drive Market Growth

The global transition toward sustainable living has significantly increased consumer demand for sustainable, environmentally friendly packaging, establishing plant-based packaging as a preferred option across various sectors. Rising public awareness of the detrimental environmental effects of traditional plastics, such as microplastic contamination, excessive landfill waste, and greenhouse gas emissions, has prompted consumers to opt for products packaged in biodegradable, compostable, or recyclable materials. Furthermore, as global climate issues become more pressing, the demand for sustainable packaging driven by consumers is anticipated to grow stronger, positioning it as a crucial long-term growth factor for the industry.

MARKET RESTRAINTS:

Limited Infrastructure for Composting & Recycling Hampers the Market Expansion

One significant limitation facing the global plant-based packaging market is the insufficient composting and recycling infrastructure, which hampers the effective management of bio-based materials at the end of their life cycle. While plant-based packaging is intended to be biodegradable or compostable, a considerable number of these materials require industrial composting conditions, such as specific temperatures, moisture levels, and controlled environments, to decompose effectively.

Additionally, waste management companies face operational challenges as the existing infrastructure is primarily designed for conventional plastics. This gap in infrastructure fosters reluctance among brands to fully adopt plant-based alternatives, as the lack of end-of-life solutions undermines the circularity and cost-effectiveness of sustainable packaging systems.

MARKET OPPORTUNITIES:

Innovations in Feedstock Diversification to Offer Lucrative Growth Opportunities

Innovations in feedstock diversification are generating substantial growth prospects for the plant-based packaging sector by expanding the range of sustainable raw materials beyond conventional crops, such as corn, sugarcane, and potato starch. Historically, the dependence on food-grade biomass has raised issues regarding food-versus-fuel competition, agricultural land utilization, and price fluctuations. To address these challenges, manufacturers are increasingly investigating alternative feedstocks, including algae, seaweed, agricultural residues, bamboo, hemp, wood pulp, bagasse, and even waste streams such as spent grain or fruit peels. These non-food sources offer plentiful, cost-effective, and eco-friendly raw materials that greatly enhance the sustainability profile of plant-based packaging.

PLANT-BASED PACKAGING MARKET TRENDS:

Surge in Bio-Based PET & Plant-Derived Bottles Emerges as a Market Trend

The increase in bio-based PET and plant-derived bottles is emerging as a significant trend within the plant-based packaging sector, fueled by the growing demand for sustainable yet high-performance packaging solutions. Bio-based PET, which is created using plant-derived ethanol sourced from sugarcane, corn, or other biomass materials, possesses the same physical and chemical properties as traditional PET. This makes it entirely compatible with current manufacturing processes and recycling systems.

Such seamless integration presents a considerable advantage for manufacturers in the beverage, personal care, and household product industries, who seek durable, transparent, and lightweight packaging that offers robust barrier properties. Prominent companies such as Coca-Cola, PepsiCo, and Nestlé are intensifying their investments in bio-PET to enhance their sustainable packaging solutions, which include bottles that are either partially or fully derived from plant-based sources.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Scalability Issues in Biopolymer Production are a Key Challenge to Market Development

Scalability remains one of the primary obstacles to the commercialization and widespread adoption of plant-based biopolymers such as PLA, PHA, and starch-based plastics. In contrast to traditional plastics, which benefit from decades of extensive manufacturing infrastructure and well-established global supply chains, the production of biopolymers is still in its developmental stages. It requires significant capital investment in specialized fermentation units, polymerization facilities, and cutting-edge processing technologies. The limited production capacities result in elevated per-unit costs, which complicate manufacturers' ability to compete with inexpensive petrochemical plastics in high-volume applications.

Segmentation Analysis

By Material

Superior Performance, Versatility & Sustainability Alignment Drive Bioplastics Segment Leadership

In terms of material, the market is categorized into bioplastics, bagasse, paper & paperboard, cellulose, starch-based, and others.

The bioplastics segment captured the largest share of the market in 2025. The segment dominated with a 38.84% share. The growth of this segment is driven by its ability to provide an optimal combination of sustainability, performance, and manufacturability. Materials such as PLA, PHA, bio-PET, and starch-based polymers exhibit mechanical and barrier properties that are comparable to those of conventional plastics. It makes them suitable for various applications, including food packaging, bottles, pouches, films, and rigid containers. Moreover, bioplastics facilitate various end-of-life options, such as industrial composting, recyclability, or biodegradation, which align closely with the increasing global sustainability goals and governmental regulations aimed at reducing single-use plastics.

The bagasse material segment is expected to grow at a CAGR of 6.30% over the forecast period.

By Packaging Type

Strength, Product Protection, and Broad Application Suitability to Boost the Rigid Packaging Segmental Growth

In terms of packaging type, the market is categorized into rigid packaging and flexible packaging.

The rigid packaging segment captured the largest plant-based packaging market share in 2025. The segment dominated with a 62.93% share. The growth of this segment is driven by its exceptional durability, structural integrity, and product safeguarding attributes, which are crucial for high-volume sectors such as food & beverages, personal care, household products, and healthcare. Rigid plant-based formats, including bio-plastic bottles, jars, trays, clamshells, and molded fiber containers, offer remarkable resistance to impact, moisture, and contamination, thereby ensuring product safety and prolonging shelf life. These characteristics render rigid packaging particularly appropriate for products that necessitate stable shape retention, secure sealing, and tamper resistance.

The flexible packaging segment is expected to grow at a CAGR of 5.66% over the forecast period.

By End-use Industry

High Consumption, Safety Needs & Rapid Shift toward Sustainable Packaging Drives Food & Beverages Segment Dominance

Based on end-use industry, the market is segmented into food & beverages, personal care & cosmetics, healthcare, and others.

To know how our report can help streamline your business, Speak to Analyst

In 2024, the global market was dominated by the food & beverages in terms of end-use industry. Furthermore, the segment is set to hold a 42.82% share in 2025. The segment leads the market, as it accounts for the highest volume of packaged products globally and experiences significant pressure to shift toward sustainable options. In light of growing concerns regarding plastic pollution, waste production, and food safety, food & beverage manufacturers are progressively utilizing plant-based materials such as PLA, PHA, molded fiber, bio-PET, and bagasse to package ready-to-eat meals, drinks, dairy products, snacks, fresh produce, and takeaway items. These materials provide outstanding barrier properties, odor neutrality, and durability, which help maintain product freshness and prolong shelf life while adhering to stringent food-contact safety regulations.

Additionally, the personal care & cosmetics segment is projected to grow at a CAGR of 6.16% during the study period.

Plant-Based Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Plant-Based Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant market share in 2024, valued at USD 107.61 billion, and maintained its leading position in 2025, with a value of USD 113.75 billion. In this region, the plant-based packaging market growth is primarily driven by strong corporate commitments to sustainability, high consumer demand for eco-friendly packaging, and the expansion of organic and natural product segments. Major brands and retailers such as Walmart, Amazon, Unilever, and Whole Foods are encouraging suppliers to adopt compostable and plant-based packaging to meet their ESG targets. State-level bans on single-use plastics, along with advances in bioplastics innovation from the U.S. research institutions, further accelerate adoption.

In 2025, the U.S. market is estimated to reach USD 91.35 billion. The market is experiencing significant growth, fueled by consumer demand for sustainable options, more stringent regulations regarding plastics, and corporate objectives. Strong growth is anticipated as materials such as cornstarch, sugarcane, seaweed, and mushroom fibers begin to substitute conventional plastics in the food, personal care, and retail sectors.

Europe and the Asia Pacific

Regions, such as Europe and the Asia Pacific, are anticipated to experience notable growth in the coming years. The European region recorded a growth rate of 5.92%, the second-highest among all regions, and reached a valuation of USD 86.31 billion in 2025. Europe is currently the fastest-growing region, largely due to rigorous regulatory frameworks, including the EU Single-Use Plastics Directive, Extended Producer Responsibility (EPR), and the Circular Economy Action Plan. Governments are proactively encouraging the use of compostable and bio-based packaging by offering incentives and implementing plastic taxes.

Backed by these factors, Germany recorded a valuation of USD 18.30 billion, the U.K. USD 15.59 billion, and France USD 13.61 billion in 2025.

After Europe, the market in the Asia Pacific reached a valuation of USD 66.23 billion in 2025 and secured the position of the third-largest region in the market. The growth of the Asia Pacific region is driven by large urban populations, increasing environmental consciousness, and growing concerns regarding plastic pollution, especially in China, India, Indonesia, and Southeast Asia. Governments are implementing stringent prohibitions on single-use plastics and promoting the use of biodegradable materials.

In the region, China and India reached a valuation of USD 21.32 billion and USD 17.88 billion, respectively, in 2025.

Latin America and the Middle East & Africa

Over the forecast period, the Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space. The Latin America market, in 2025, reached a valuation of USD 52.28 billion. The increasing awareness and demand among the middle class for environmentally friendly solutions in the food, beverage, and personal care sectors are driving market adoption.

In the Middle East & Africa, South Africa is recorded a valuation of USD 9.09 billion in 2025. In the Middle East & Africa, the factors influencing the market vary considerably, as government-driven initiatives for waste reduction and heightened environmental regulations are fostering a growing interest in sustainable packaging.

COMPETITIVE LANDSCAPE

Key Industry Players:

Extensive Product Portfolio with Strong Distribution Network of Key Companies Supported their Leading Position

The market exhibits a semi-concentrated structure, with numerous small to mid-size companies actively operating worldwide. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Huhtamaki, Tetra Pak International SA, and Amcor are among the leading players in the market. A comprehensive range of plant-based packaging products, a global presence through a strong distribution network, and collaborations with research and academic institutions are a few characteristics that support the dominance of these players.

Apart from this, other prominent players in the market include Sealed Air, Pactiv Evergreen Inc., Ficus Pax, and others. These companies are undertaking various strategic initiatives, including investments in R&D and partnerships with pharmaceutical companies, to enhance their market presence.

LIST OF KEY PLANT-BASED PACKAGING COMPANIES PROFILED:

- Huhtamaki (Finland)

- Tetra Pak International SA- (Switzerland)

- Amcor (Switzerland)

- Sealed Air (U.S.)

- Pactiv Evergreen Inc. (U.S.)

- Ficus Pax (India)

- Tipa Ltd. (Israel)

- Pappco Greenware (India)

- Mondi (U.K.)

- Eco Packer (India)

- The Meyers Printing Companies, Inc. (U.S.)

- Stora Enso (Finland)

- Pactap (India)

- Vegware (Scotland)

- Tessera Sustainable Packaging (Greece)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Braskem, a leading company in the industrial-scale production of biopolymers, presented a new generation of bio-based and circular product solutions designed to expedite the transformation of the plastics industry. This initiative included collaborations with Dutch Brands Bottle Up & Eurobottle. Additionally, it featured a partnership with the German brand Polytan. Through its sustainable portfolio, Braskem unveiled product launches and partnerships that embody sustainability and innovation across packaging, healthcare, hygiene, and consumer goods.

- May 2025: Intec Bioplastics, Inc. announced the successful introduction of its latest sustainable packaging solution, EarthPlus Hercules Bioflex Stretch Wrap, suitable for both pallet and food wrapping applications. Hercules Bioflex is resistant to both heat and cold temperatures and is composed of 35% renewable plant-based materials, significantly lowering its customers' carbon footprint. A reduction in plastic usage in packaging leads to a decrease in microplastics.

- May 2025: Myco, a company based in the Czech Republic, launched a biodegradable substitute for polystyrene packaging using mushroom mycelium and organic waste materials such as sawdust. The mycelium serves as a natural adhesive, shaping the waste into a robust, shock-resistant substance suitable for packaging purposes. This eco-friendly alternative is entirely biodegradable and can be composted, decomposing within weeks, in contrast to polystyrene, which may require centuries to break down.

- September 2024: Marigold Health Foods partnered with Sonoco to introduce its entirely recyclable packaging for a range of natural, plant-based food items, such as stock cubes, sauces, and alternatives to meat and fish. The completely recyclable packaging solution, developed by Sonoco, demonstrates Marigold’s dedication to sustainability and innovation, establishing a new benchmark in the industry.

- April 2024: Savor Brands Coffee Packaging introduced COMPOST+, a plant-based industrial compostable metallized barrier film, at the Specialty Coffee Association’s Specialty Coffee Expo. These advanced barrier materials are engineered to preserve the flavor and aroma of coffee, ensuring it remains at its best.

REPORT COVERAGE

The market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It encompasses details on market dynamics and trends expected to drive the market during the forecast period. It provides information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and the profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.19% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Material · Bioplastics · Bagasse · Paper & Paperboard · Cellulose · Starch-based · Others |

|

By Packaging Type · Rigid Packaging · Flexible Packaging |

|

|

By End-use Industry · Food & Beverages · Personal Care & Cosmetics · Healthcare · Others |

|

|

By Geography · North America (By Material, Packaging Type, End-use Industry, and Country) o U.S. o Canada · Europe (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 350.43 billion in 2025 and is projected to reach USD 197.79 billion by 2034.

In 2025, the North America market value stood at USD 113.75 billion.

The market is expected to exhibit a CAGR of 6.19% during the forecast period of 2026-2034.

The rigid packaging segment led the market by packaging type in 2025.

The key factors driving the market growth are the rising consumer preference for sustainable & eco-friendly packaging.

Huhtamaki, Tetra Pak International SA, Amcor, Sealed Air, Pactiv Evergreen Inc., and Ficus Pax are some of the prominent players in the market.

North America dominated the market in 2025.

The rising innovations in feedstock diversification is one of the prominent factors expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us