Polymethyl Methacrylate Market Size, Share & Industry Analysis, By Form (Extruded Sheets, Cast Acrylic Sheets, Pellets, Beads, and Others), By Application (Signs & Displays, Automotive, Building & Construction, Electrical & Electronics, Consumer Goods, and Others), and Regional Forecast, 2026-2034

POLYMETHYL METHACRYLATE MARKET SIZE and FUTURE OUTLOOK

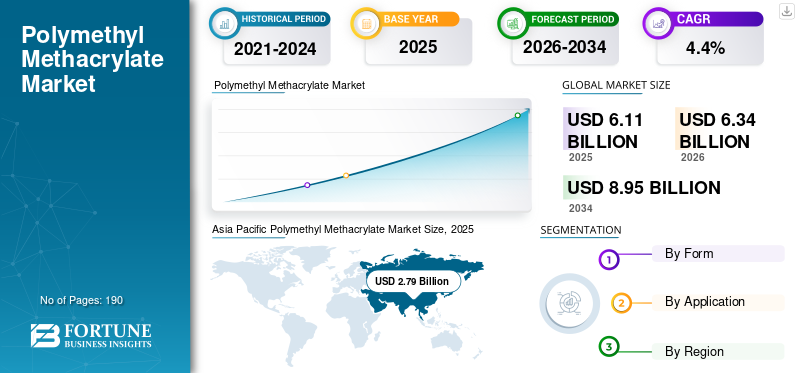

The global polymethyl methacrylate market size was valued at USD 6.11 billion in 2025. The market is projected to grow from USD 6.34 billion in 2026 to USD 8.95 billion by 2034 at a CAGR of 4.4% during the forecast period. Asia pacific dominated the polymethyl methacrylate market with a market share of 45.66% in 2025.

Polymethyl methacrylate (PMMA) is a transparent thermoplastic, widely known as acrylic or acrylic glass, and is valued for its high optical clarity, weather resistance, surface hardness, lightweight nature, and ease of processing. The product market is influenced by demand from industries that require transparent, durable, lightweight, and aesthetically attractive materials as alternatives to glass and certain other plastics. It also includes competitive activity among manufacturers related to capacity expansion, product innovation, application development, and circular or recycled PMMA solutions. Key players in the market include Mitsubishi Chemical Corporation, Röhm GmbH, Trinseo PLC, Sumitomo Chemical Co., Ltd., CHIMEI Corporation, Kuraray Co., Ltd., PLASKOLITE, and 3A Composites, as well as regional acrylic sheet producers and specialty PMMA suppliers.

Download Free sample to learn more about this report.

POLYMETHYL METHACRYLATE MARKET TRENDS

Shift Toward Optical Performance, Lightweight Design, and Circular PMMA Systems to be a Significant Market Trend

A trend in the global market is the move toward higher optical performance and application-specific grades rather than simple commodity volume growth. PMMA suppliers are increasingly positioning their portfolios around light management, surface appearance, heat resistance, weatherability, and design flexibility for end uses such as automotive lighting, optical display, appliances, construction, and consumer products. Trinseo, for example, highlights PMMA grades for automotive, appliance, lighting, building and construction, and consumer goods. At the same time, Mitsubishi Chemical emphasizes the use of PMMA sheets in signage, displays, LCDs, and light guide plates.

At the same time, the category is seeing a strong circularity and recycling trend. PMMA has a more favorable recycling pathway than many other transparent plastics as it can be chemically recycled back toward high-purity recycled monomer. Trinseo’s depolymerization facility in Rho, Italy, is a visible example of this shift, demonstrating that suppliers are seeking to combine PMMA’s traditional strengths in clarity and durability with a stronger circular value proposition.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Product Demand from Signs, Displays, and Light-Management Applications to Drive Market Growth

One of the strongest drivers for the polymethyl methacrylate market growth is broad use of product in signage, displays, and light-management applications. PMMA offers high transparency, weather resistance, surface quality, and processability, which makes it well-suited for illuminated signs, retail displays, light guide plates, and outdoor visual applications. Mitsubishi Chemical explicitly positions its SHINKOLITE PMMA sheet for signage, displays, LCDs, and light guide plates, which directly supports this segment as a major structural demand base.

This driver remains important as these applications value a combination of clarity, durability, UV resistance, and fabrication flexibility. Compared with many alternative transparent materials, PMMA performs well in aesthetic and outdoor-use environments, which supports repeat demand across commercial infrastructure, retail refurbishment, advertising systems, and architectural display formats.

MARKET RESTRAINTS

Regulatory and Compliance Burden Across Chemicals and Materials Chains to Restrict Growth

A major restraint for the product market is the growing regulatory and compliance burden surrounding chemicals production, monomers, additives, and downstream materials management. In the European Union, REACH requires manufacturers and importers to gather information on substances and manage the associated risks, which increases registration, documentation, traceability, and compliance obligations across chemical value chains. For PMMA suppliers and formulators, this can raise operating costs and lengthen qualification timelines, especially when serving regulated end uses or multiple geographies.

This restraint matters as PMMA competes in sectors such as automotive, electronics, and medical devices, where qualification standards are already demanding. When compliance costs rise, suppliers face pressure not only on manufacturing economics but also on reformulation, testing, and customer approval cycles, which can slow commercial rollout of new grades and reduce flexibility in lower-margin segments.

MARKET OPPORTUNITIES

Circular PMMA and Chemical Recycling Create New Growth Space

One of the biggest opportunities in the market is the development of chemical recycling and circular acrylic systems. Trinseo’s PMMA depolymerization facility in Italy demonstrates a pathway for recovering high-purity recycled monomer for reuse in demanding applications. This is strategically important as it improves PMMA’s sustainability case without requiring the market to give up the optical performance, weatherability, and appearance benefits that make the material attractive in the first place.

This opportunity is likely to become more important as customers in automotive, construction, and consumer-facing sectors place greater emphasis on recycled content and circular design. PMMA is comparatively well-positioned here as its depolymerization pathway can support high-value reuse rather than only downcycling, which may help suppliers defend premium applications over the long term.

MARKET CHALLENGES

Limited Recycling Infrastructure and End-of-Life Collection Challenge Market Growth

A major challenge for the market is that although PMMA is chemically recyclable, the collection, sorting, and recycling infrastructure is still not scaled evenly across regions and applications. Trinseo’s depolymerization investment is promising, but it also shows that circular PMMA is still in development and scale-up phase rather than being universally established. That means the market still faces practical limitations in securing feedstock streams and building closed-loop systems at a commercial scale.

This is strategically important as sustainability expectations are rising rapidly across plastics markets. If PMMA recycling pathways do not scale quickly enough, the material could face procurement pressure from accounts prioritizing circularity targets, even if PMMA remains technically attractive.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions can restrain the product market by making raw-material sourcing, export flows, and downstream manufacturing costs more volatile. The OECD’s 2024 inventory states that export restrictions on industrial raw materials are becoming more prevalent and more prohibitive, potentially creating spillover effects across interconnected supply chains. For PMMA, this matters as the market depends on globally linked methacrylate and petrochemical chains, and disruptions can affect availability, lead times, and pricing stability.

The effect is especially relevant in Asia, where capacity expansion and demand growth remain central to the market. Röhm explicitly states that China is the world’s largest MMA and product market, so any geopolitical or trade disruption involving Asia can have an outsized effect on global PMMA balances, procurement decisions, and regional investment strategies.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the global product market is increasingly focused on three themes: circularity, higher-performance grades, and application-specific innovation. Circularity is visible in depolymerization and recycled-monomer pathways, while higher-performance development is evident in the push toward impact-resistant, flame-retardant, optical, and light-management grades. Mitsubishi Chemical’s emphasis on flame-retardant and impact-resistant SHINKOLITE products, along with Trinseo’s light-management and heat-resistant PMMA offerings, shows that innovation is moving toward tailored performance rather than basic resin commoditization.

SEGMENTATION ANALYSIS

By Form

Pellets Segment Dominate Due to their Broad Use in Molding Compounds and Downstream Processing

Based on form, the market is segmented into extruded sheets, cast acrylic sheets, pellets, beads, and others.

Among these, the pellets segment has the dominant polymethyl methacrylate market share. This dominance is primarily driven by the widespread use of PMMA pellets as the main feedstock for injection molding, extrusion, and compounding applications across automotive, consumer goods, electronics, and industrial products. Pellets offer ease of handling, process consistency, and suitability for large-volume manufacturing, making them the preferred commercial form for processors serving multiple downstream industries.

The extruded sheets segment accounts for a significant market share, supported by its extensive use in signage, displays, architectural glazing, partitions, retail fixtures, and lighting covers. These sheets are valued for their optical clarity, lightweight nature, weather resistance, and ease of fabrication, which makes them suitable for both indoor and outdoor applications. Their broad use in visual communication and construction-linked applications continues to support strong market demand. The segment is projected to grow at 4.6% CAGR during the forecast period.

The cast acrylic sheets segment represents positive market growth. It maintains an important position due to its superior optical quality, greater thickness flexibility, and better surface finish compared with extruded sheets. These properties make cast sheets especially suitable for premium applications such as aquariums, sanitaryware, high-end displays, medical panels, and specialized industrial components. Their higher customization potential also supports their demand in value-added segments.

The others segment registers notable growth, including specialty PMMA forms, intermediate formats, and custom material configurations developed for specific technical or industrial requirements.

By Application

To know how our report can help streamline your business, Speak to Analyst

Signs & Displays Lead Due to High Optical Clarity, Weather Resistance, and Design Flexibility

Based on application, the market is segmented into signs & displays, automotive, building & construction, electrical & electronics, consumer goods, and others.

The signs & displays segment holds the leading share of the global product market. This dominance is mainly driven by PMMA’s excellent transparency, surface gloss, UV resistance, and ease of fabrication, which make it highly suitable for advertising boards, illuminated signage, retail displays, exhibition fixtures, and decorative panels. PMMA is widely preferred for these applications as it offers a glass-like appearance at a lower weight and better impact resistance in many commercial environments.

The automotive segment represents the second-largest application area. PMMA is increasingly used in automotive lighting systems, instrument panels, interior trims, glazing components, and exterior design parts where optical quality, weatherability, and dimensional stability are important. The segment continues to benefit from ongoing vehicle lightweighting, styling requirements, and the growing use of transparent and illuminated design features in modern vehicles. The segment is expected to grow by 4.8% during the forecast period.

The building & construction segment is experiencing strong market growth, supported by its use in glazing, partitions, roofing elements, sound barriers, panels, sanitaryware, and decorative architectural features. Its durability, outdoor resistance, and aesthetic appeal make it a useful material for residential and commercial construction.

The others segment is seeing notable growth and includes applications such as medical devices, aerospace components, lighting systems, industrial parts, and other niche uses where optical performance, light weight, and durability are required.

POLYMETHYL METHACRYLATE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Polymethyl Methacrylate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global market. The region’s leading position is supported by its large-scale manufacturing base, strong demand from signage, electronics, automotive, and construction sectors, and the presence of major PMMA production and processing hubs. China, Japan, India, and other Asian economies contribute significantly to regional demand through the broad use of PMMA in display materials, automotive parts, electronic components, and consumer products. The region also benefits from strong industrialization, urban infrastructure development, and high consumption of fabricated acrylic products.

China Polymethyl Methacrylate Market

China’s market is one of the largest globally, with 2025 revenue valued at USD 23.62 billion, representing roughly 27.6% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America registers positive growth during the forecast period. The regional market is supported by consistent demand from building materials, automotive components, displays, medical products, and consumer goods. The U.S. remains the major contributor in the region due to its strong industrial demand, developed infrastructure, and broad application of PMMA across the commercial, transportation, and household sectors. Demand for premium acrylic materials in signage, architectural glazing, and consumer products also supports regional growth.

U.S. Polymethyl Methacrylate Market

In 2025, the U.S. market was valued at USD 0.69 billion, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 11.4% of global market sales.

Europe

Europe registers significant growth during the forecast period. The region maintains a strong market position due to its established automotive industry, advanced industrial base, mature construction sector, and broad use of engineered polymer materials. Applications in automotive lighting, architectural panels, industrial glazing, sanitary products, and specialty display systems support demand for PMMA in Europe. In addition, the presence of major material suppliers and the increasing focus on sustainable, high-performance plastic systems continue to support the market.

Germany Polymethyl Methacrylate Market

The Germany market was valued at around USD 0.39 billion in 2025, representing roughly 6.5% of global market revenues.

U.K. Polymethyl Methacrylate Market

The U.K. market was valued at around USD 0.12 billion in 2025, representing roughly 1.9% of global market revenues.

Latin America

The market in this region is driven by demand from building materials, automotive manufacturing, signage, and household products, particularly in Brazil, Mexico, and other developing economies. While the region remains smaller than Asia Pacific, Europe, and North America, improving industrial activity and urban development continue to support PMMA consumption across several downstream applications.

Brazil Polymethyl Methacrylate Market

Brazil market was valued at around USD 0.14 billion in 2025, representing roughly 2.2% of global market revenues.

Middle East & Africa

The region's growth is supported by infrastructure activity, commercial construction, industrial expansion, and the rising use of durable, transparent materials in architectural and display applications. Demand is particularly strong in the GCC, where construction and industrial investment continue to create opportunities for acrylic sheets, panels, and fabricated PMMA products.

GCC Polymethyl Methacrylate Market

The GCC market was valued at around USD 0.22 billion in 2025, representing roughly 3.6% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Adopting Capacity, Circularity, and Application-led Strategies to Strengthen their Market Positions

The global market is moderately consolidated around a mix of integrated methacrylate producers, specialty acrylic manufacturers, and sheet-focused processors. Competition is shaped by backward integration into MMA, brand strength in acrylic sheet and molding compounds, application support in automotive, electronics, signage, and construction, and, increasingly, by recycling and circular-acrylic capabilities.

Major participants such as Mitsubishi Chemical, Röhm, Trinseo, Sumitomo Chemical, CHIMEI, and Kuraray compete on optical performance, weatherability, specialty grades, and supply consistency rather than solely on commodity pricing.

LIST OF KEY POLYMETHYL METHACRYLATE COMPANIES PROFILED IN REPORT

- Mitsubishi Chemical Corporation (Japan)

- Röhm GmbH (Germany)

- Trinseo PLC (U.S.)

- Sumitomo Chemical Co., Ltd. (Japan)

- CHIMEI Corporation (Taiwan)

- Kuraray Co. Ltd. (Japan)

- PLASKOLITE (U.S.)

- 3A Composites GmbH (Germany)

- LX MMA Corp. (South Korea)

- Makevale Group (U.K.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Lummus Technology and Sumitomo Chemical announced the commercial availability of PMMA chemical recycling technology, aimed at closed-loop PMMA and lower-emissions acrylic recycling.

- February 2025: Trinseo and Lapo announced the joint development of eyewear lenses containing recycled PMMA, highlighting commercial traction for recycled-content acrylic resins in value-added optical applications.

- October 2024: Kuraray announced ISCC PLUS certification for PARAPET™ methacrylic resin produced at its Niigata Plant, supporting the company’s sustainable-material positioning in methacrylic resin.

REPORT COVERAGE

The polymethyl methacrylate market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, form, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Growth Rate | CAGR of 4.4% from 2026 to 2034 |

| Segmentation | By Form, By Application, and By Region |

| By Form |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 6.11 billion in 2025 and is projected to reach USD 8.95 billion by 2034.

Recording a CAGR of 4.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The signs & displays segment is expected to lead the market during the forecast period.

Asia Pacific held the highest market share in 2025.

Rising demand from signs, displays, and light-management applications drives the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us