Polypropylene Fiber in Mobility & Transportation Market Size, Share & Industry Analysis, By Product Type (Staple Fibers, Filament Yarns, and Functional Fibers), By End Use Industry (Automotive, Railways, Marine, Aviation, and Urban Air Mobility (UAM)), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

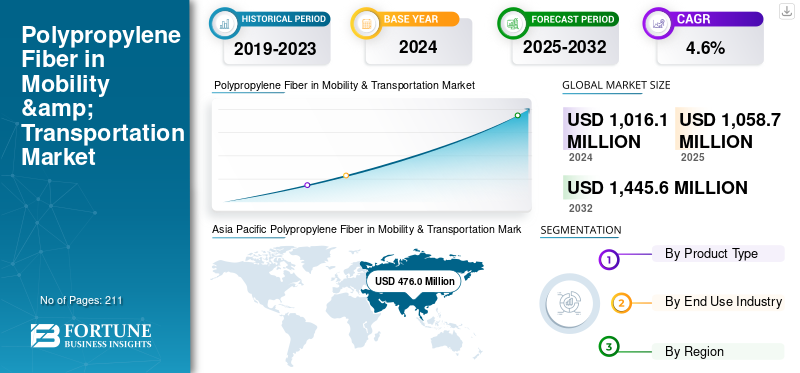

The global polypropylene fiber in mobility & transportation market size was valued at USD 1,016.1 million in 2024. The market is projected to grow from USD 1,058.7 million in 2025 to USD 1,445.6 million by 2032, exhibiting a CAGR of 4.6% during the forecast period. Asia Pacific dominated the global market with a market share of 45.96% in 2024.

Polypropylene (PP) fiber refers to a lightweight, durable synthetic fiber derived from polypropylene resin, valued for its low density, chemical resistance, moisture repellence, abrasion resistance, and excellent cost-to-performance balance. Within the mobility and transportation sector, PP fibers are widely used across automotive interiors, rail and transit systems, marine vessels, aviation cabins, and emerging urban mobility platforms. Key applications include carpets, floor and trunk liners, acoustic and thermal insulation, interior trim substrates, seating systems, and underbody or semi-exterior components. The inherent lightweight nature of PP fibers supports vehicle mass reduction, while their recyclability and compatibility with mono-material systems align well with global sustainability and circular economy goals. Such exceptional parameters are set to create a progressive environment for market expansion.

Furthermore, the global market of polypropylene fiber in mobility and transportation is shaped by a mix of large integrated fiber producers and specialized automotive-focused suppliers, including Indorama Ventures, Beaulieu International Group, Asahi Kasei Corporation, RadiciGroup, and emerging high-capacity Asian manufacturers such as Hubei Botao Synthetic Fiber. Ongoing investments in lightweight fiber engineering, recycled-content PP fibers, acoustic optimization, and compliance with stringent automotive and transportation safety standards continue to strengthen competitive positioning.

Download Free sample to learn more about this report.

Polypropylene Fiber in Mobility and Transportation Market Key Takeaways

- 2024 Market Size: USD 1,016.1 million

- 2025 Market Size: USD 1,058.7 Million

- 2032 Forecast Market Size: USD 1,445.6 Million

- CAGR: 4.6% from 2025–2032

- Asia Pacific dominated the polypropylene fiber in mobility & transportation market with a 45.96% share in 2024.

- The staple fibers segment accounted for the largest market share in 2024.

- The automotive segment held the dominant end-use market share in 2024.

Asia Pacific

Asia Pacific is projected to reach USD 523.9 million in 2025.

North America

North America is projected to reach USD 206.9 million in 2025.

Europe

Europe is projected to reach USD 291.8 million in 2025.

U.S.

The market is estimated at USD 175.8 million in 2025.

Japan

Strong automotive production and growing demand for lightweight, recyclable vehicle materials continue to support market growth.

Read More

POLYPROPYLENE FIBER IN MOBILITY & TRANSPORTATION MARKET TRENDS

Expansion of Electric Vehicle Production and Increasing Per-Vehicle Use of Engineered Textile Components to Drive Market Growth

The rapid expansion of electric vehicle (EV) production is a key driver of the market. EV platforms require enhanced acoustic and thermal management due to the absence of engine noise, resulting in increased use of engineered textile components, such as nonwoven insulation, floor systems, and interior trims. As a result, PP fiber consumption per vehicle is rising compared to conventional internal combustion engine models. In addition, EV manufacturers emphasize lightweighting and energy efficiency to extend driving range, further favoring PP fiber–based solutions due to their low density and durability.

- According to the International Energy Agency (IEA), global EV production in 2025 experienced significant growth, with projections indicating that over 20 million new electric cars would be sold by year-end, accounting for roughly a quarter of all new vehicles.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Automotive Lightweighting and Fuel Efficiency Mandates to Drive PP Fiber Demand

Globally, lightweighting has become a structural priority in the automotive sector as governments tighten fuel efficiency and emissions regulations across passenger and commercial vehicle fleets. Polypropylene (PP) fiber benefits directly from this shift as it combines low density, adequate mechanical strength, chemical resistance, and cost efficiency, making it well-suited for replacing heavier traditional materials in multiple automotive components. With a density of 0.90 g/cm³, PP is one of the lightest commodity polymers, enabling meaningful vehicle weight reduction without compromising functional performance.

Regulatory frameworks, such as fleet-average fuel-economy standards in North America, CO₂ emission limits in Europe, and fuel-consumption norms in the Asia Pacific region, implicitly incentivize OEMs to substitute metals, rubber, and heavier plastics with lightweight polymer-based solutions. Staple and continuous fibers are increasingly engineered into nonwoven and composite structures that play an essential role in improving fuel efficiency, which will drive the polypropylene fiber in mobility & transportation market growth in the foreseeable period.

MARKET RESTRAINTS

Competition from Glass-Fiber, Carbon-Fiber Composites, and Engineered Thermoplastics to Restrain Market Growth

The increasing adoption of glass-fiber, carbon-fiber composites, and engineered thermoplastics in structural and semi-structural automotive applications is expected to restrain growth in the PP fiber market for mobility and transportation. These materials offer superior mechanical strength, stiffness, and heat resistance, making them well-suited for load-bearing components, structural reinforcements, and high-performance applications where PP fibers cannot meet the functional requirements. As OEMs pursue aggressive lightweighting and safety targets, particularly in premium vehicles and electric platforms, composite materials are increasingly preferred for parts requiring higher structural integrity.

MARKET OPPORTUNITIES

Increasing Use of Recycled and Circular Polypropylene Fibers in Mobility Applications to Create Lucrative Growth Opportunities

The growing use of recycled and circular PP fibers in mobility applications is emerging as a structurally important growth driver for the global polypropylene fiber market, particularly as automotive, rail, and commercial vehicle manufacturers accelerate their transition toward low-carbon material portfolios. Mobility OEMs are under pressure from both regulatory and commercial sources to reduce vehicle lifecycle emissions, increase recycled content, and demonstrate progress toward circular economy targets. PP fibers are already valued in mobility applications for their low density, chemical resistance, and cost efficiency. It is increasingly being reformulated using post-consumer and post-industrial recycled polypropylene without compromising functional performance. This shift is expanding the addressable market for PP fibers beyond conventional virgin material demand, creating new revenue streams for fiber producers.

Segmentation Analysis

By Product Type

Staple Fibers Lead Market as Automotive Interiors and Nonwoven Applications Dominate Demand

Based on product type, the PP fiber market for mobility and transportation is segmented into staple fibers, filament yarns, and functional fibers.

The staple fibers segment accounted for the largest share of the global polypropylene fiber in mobility & transportation market share in 2024. The segment’s growth is driven by its extensive use in automotive carpets, floor mats, trunk liners, wheel-arch liners, and insulation felts. Staple fibers remain the preferred choice for needle-punched and thermal-bonded nonwovens, which form the backbone of automotive interior and acoustic applications. Their cost efficiency, abrasion resistance, lightweight properties, and recyclability make them highly compatible with high-volume passenger cars and commercial vehicles.

The functional fibers segment is the fastest-growing, registering a CAGR of 5.1% by value over the forecast period. Growth is driven by increasing demand for acoustic insulation, thermal management, fire-retardant, and specialty PP fibers, particularly in electric vehicles and advanced mobility platforms. Functional fibers enable higher performance in noise reduction, lightweighting, and safety compliance, positioning them as the key value-growth driver despite a smaller base.

By End Use Industry

To know how our report can help streamline your business, Speak to Analyst

Automotive Dominates as EV Adoption and Interior Material Intensity Increase

Based on end use industry, the market is segmented into automotive, railways, marine, aviation, and urban air mobility (UAM).

The automotive segment accounted for the dominant share of PP fiber demand in 2024, supported by the widespread use of PP fibers in interior trims, flooring systems, seating components, insulation layers, and semi-exterior parts. Growth is underpinned by global passenger car and light commercial vehicle production, increasing SUV penetration, and the transition toward electric vehicles. EV platforms, in particular, require enhanced acoustic and thermal insulation, directly increasing the use of PP-based nonwovens and functional fibers. Additionally, OEMs' focus on lightweighting and recyclability continues to favor PP fibers over heavier or multi-material alternatives.

The urban air mobility (UAM) segment is the fastest-growing end-use, expanding at a CAGR of 6.7% by value. Although currently small in absolute terms, UAM growth is driven by rising investment in eVTOL platforms, lightweight interior systems, and next-generation mobility concepts. Railways and aviation exhibit moderate but steady growth, driven by rolling stock expansion, refurbishment cycles, and aircraft interior upgrades, while marine demand remains stable, primarily driven by replacement needs.

Polypropylene Fiber in Mobility & Transportation Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Polypropylene Fiber in Mobility & Transportation Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 499.5 million, and was expected to maintain the leading share in 2025, with USD 523.9 million. The region’s dominance is underpinned by its leadership in vehicle manufacturing and the expansion of its transportation infrastructure. The region accounts for over half of global vehicle production, led by China, India, Japan, and South Korea, which collectively manufacture more than 55% of the world’s automobiles. In parallel, large-scale investments in metro systems, high-speed rail, and urban transit, especially in China and India, support additional PP fiber consumption in rail interiors.

China Polypropylene Fiber in Mobility & Transportation Market

Based on Asia Pacific’s strong contribution and China’s manufacturing strength, the China market recorded at USD 304.3 million in 2025, accounting for roughly 28.7% of global revenues.

India Polypropylene Fiber in Mobility & Transportation Market

The India market in 2025 secured USD 56.3 million. The nation’s growth is supported by demand that is expected to rise with increasing vehicle production and technological advancements.

North America

North America remains a significant regional market, projected to reach USD 206.9 million by 2025. The North American PP fiber market in mobility is mature yet dynamic, striking a balance between performance demands and significant pushes for sustainability and technological advancements. Key trends include high consumption in the U.S., growth in Canada for EV components, and a significant focus on sustainability through recycling and bio-based options, with innovations in high-performance fibers and recycled content. The region is a major producer and consumer, leveraging shale gas to create cost-effective feedstocks and foster a progressive market environment.

U.S. Polypropylene Fiber in Mobility & Transportation Market

The U.S. market in 2025 was estimated at USD 175.8 million, accounting for approximately 16.6% of global revenues.

Europe

Europe was projected to experience a growth rate of 4.3% in the coming years, reaching a valuation of USD 291.8 million by 2025. Europe represents a high-value, regulation-driven market for PP fibers in mobility and transportation. European OEMs operate under some of the strictest CO₂ emission, noise, fire safety, and recyclability regulations globally, which strongly favor lightweight, mono-material interior solutions. Overall, growth in Europe is driven less by volume expansion and more by material substitution, functional upgrading, and sustainability-led adoption.

Germany Polypropylene Fiber in Mobility & Transportation Market

The Germany market reached USD 79.3 million in 2025, equivalent to around 7% of global revenues. Germany is the largest market for PP fiber in Europe for mobility and transportation, driven by its position as the region’s leading automotive manufacturing base. The country produces around 4 million vehicles annually, with a strong concentration of premium passenger cars, commercial vehicles, and advanced mobility platforms driving strong demand for PP Fibers.

U.K. Polypropylene Fiber in Mobility & Transportation Market

The U.K. market in 2025 recorded USD 47.6 million, accounting for roughly 5% of global revenues. Automotive production in the U.K. is smaller than in Germany or France. Still, it remains significant, particularly in passenger cars and premium vehicle segments, which support demand for PP fibers in interior trims, flooring, and insulation materials.

Rest of World

The Rest of the World is expected to witness moderate growth during the forecast period, with a market valuation of USD 60.4 million in 2025. The region, comprising Latin America and the Middle East & Africa, remains smaller in scale but is structurally important. Demand is largely driven by the localization of automotive assembly, the expansion of commercial vehicle fleets, and the development of infrastructure. PP fibers are favored for their cost-effectiveness, durability, and performance in high-temperature and demanding operating environments, particularly in the Middle East & Africa.

COMPETITIVE LANDSCAPE

Key Industry Players

Application-Driven Performance and Lightweight Innovation Define Competitive Positioning

The market is shaped by manufacturers with strong fiber engineering capabilities, large-scale production capacity, and close alignment with automotive OEMs and Tier-1 interior suppliers. Competitive differentiation is increasingly driven by lightweight performance, acoustic and thermal efficiency, recyclability, and application-specific fiber design, rather than volume alone. Key players, including Indorama Ventures, Beaulieu International Group, Asahi Kasei Corporation, RadiciGroup, and leading Asian PP fiber producers, maintain strong market positions through diversified product portfolios, long-term automotive qualifications, and global supply footprints. Other participants continue to enhance competitiveness through the development of functional fibers, recycled-content solutions, and regional capacity expansion, particularly in the Asia Pacific.

LIST OF KEY POLYPROPYLENE (PP) FIBER IN MOBILITY & TRANSPORTATION COMPANIES PROFILED

- Asahi Kasei Corporation (Japan)

- Beaulieu International Group (Belgium)

- GEOTEXAN (Spain)

- Goonvean Fibres (England)

- Hubei Botao Synthetic Fiber Co., Ltd. (China)

- IFG International Fibres Group (Sweden)

- Indorama Ventures (Thailand)

- Radici Partecipazioni SpA (Italy)

- Yusheng Enterprise Limited (China)

KEY INDUSTRY DEVELOPMENTS

- February 2023: Asahi Kasei and Mitsui Chemicals, both prominent players in the Japanese nonwovens sector, created a new integrated company by merging their nonwovens divisions, which was operational by the end of October 2023. This initiative will be executed through a corporation-type demerger, which will enable the formation of the new integrated entity, subject to regulatory approvals in Japan and Thailand, where both companies are currently based.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report on polypropylene fiber in mobility & transportation also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 4.6% from 2025-2032 |

|

Unit |

Value (USD Million) Volume (Kiloton) |

|

Segmentation |

By Product Type, End Use Industry, and Region |

|

By Product Type |

· Staple Fibers · Filament Yarns · Functional Fibers |

|

By End Use Industry |

|

|

By Region |

· North America (By Product Type, By End Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Product Type, By End Use Industry, and Country/Sub-region) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Product Type, By End Use Industry, and Country/Sub-region) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Rest of World (By Product Type, and By End Use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1,016.1 million in 2024 and is projected to reach USD 1,445.6 million by 2032.

Recording a CAGR of 4.6%, the market is slated to exhibit steady growth during the forecast period.

The automotive end use industry segment led in 2024.

Asia Pacific held the highest market share in 2024.

The automotive lightweighting and fuel-efficiency mandates drive market growth.

- 2019-2032

- 2024

- 2019-2023

- 211

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us