Polyvinyl Alcohol Market Size, Share & Industry Analysis, By Grade (Fully Hydrolyzed PVA, Partially Hydrolyzed PVA, and Modified/Specialty Grades), By End-Use Industry (Paper, Textiles, Construction, Adhesives, Packaging, and Others), and Regional Forecast, 2026-2034

Polyvinyl Alcohol Market Size and Future Outlook

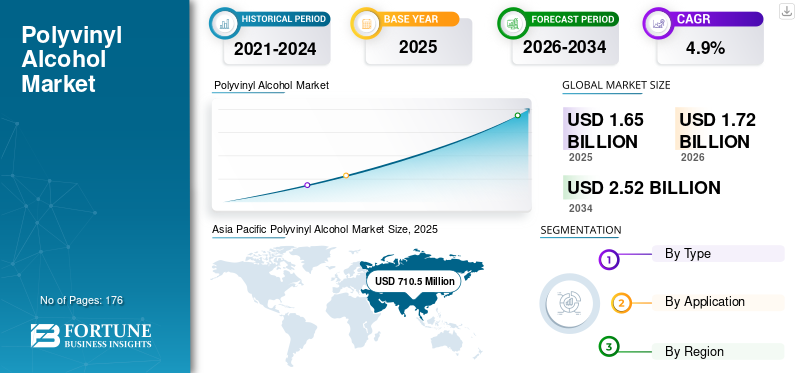

The global polyvinyl alcohol market size was valued at USD 1,656.4 million in 2025. The market is projected to grow from USD 1,720.5 million in 2026 to USD 2,525.8 million by 2034, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the polyvinyl alcohol market with a market share of 42.89% in 2025.

Polyvinyl alcohol (PVA) is a specialty polymer used in adhesives, paper coatings, packaging films, textiles, and construction materials. Its demand depends on industries that need strong bonding, good film-forming ability, water solubility, and resistance to oils and chemicals. It is valued in applications where product quality, process efficiency, and environmental compatibility are important. Globally, the market is supported by steady demand from the packaging, paper, textile, and industrial sectors. Growth is mainly driven by performance-based uses, sustainability trends, and gradual expansion in end-use industries, rather than by any sudden rise in overall consumption volume.

A limited number of well-established companies with advanced manufacturing integration and deep process knowledge hold a dominant position in the market. Major players such as KURARAY CO., LTD., Sekisui Specialty Chemicals America, Mitsubishi Chemical Corporation, China Petrochemical Corporation, Denka Company Limited, and regional manufacturers focus on product quality, application-specific grades, and consistent supply support. Further, resulting in a moderately consolidated market characterized by stable demand, technical entry barriers, and controlled capacity expansion.

Download Free sample to learn more about this report.

Polyvinyl Alcohol Market Key Takeaways

- 2025 Market Size: USD 1,656.4 million

- 2026 Market Size: USD 1,720.5 million

- 2034 Forecast Market Size: USD 2,525.8 million

- CAGR: 4.9% from 2026–2034

- Asia Pacific dominated the market with a 42.89% share in 2025.

- The partially hydrolyzed PVA segment is expected to grow at a 5.4% CAGR over the forecast period.

- The packaging segment is expected to grow at a 5.7% CAGR over the forecast period.

North America

North America reached USD 366.7 million in 2025.

Asia Pacific

Asia Pacific led the market with a value of USD 710.5 million in 2025.

Europe

Europe is expected to reach USD 392.5 million in 2025.

U.S.

The market was valued at USD 327.2 million in 2025.

Germany

The market reached USD 78.7 million in 2025.

Read More

POLYVINYL ALCOHOL MARKET TRENDS

Shift Toward Specialty Grades and Functional Film Applications is Reshaping the Market

A key trend in the market is the rising demand for specialty grades and functional film applications with more controlled performance. Manufacturers are increasingly developing products with tailored solubility, better film strength, improved barrier properties, and suitability for technical uses. This shows that the market is gradually moving beyond standard applications toward more value-added demand. From a business perspective, product differentiation and performance improvement are becoming more important for strengthening market position, meeting specific customer needs, and supporting growth in higher-value applications.

- According to Eurostat, the EU generated 79.7 million tons of packaging waste in 2023, of which 40.4% was paper and cardboard. This supports the trend toward more functional film and coating materials, where polyvinyl alcohol is increasingly used in specialty packaging applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand from Packaging and Paper Applications Supports Market Growth

PVA demand is mainly influenced by its increasing use in packaging and paper applications, where film-forming ability, surface strength, and barrier performance are important. In packaging, it is used in specialty films and soluble packaging formats that require high strength and controlled dissolution. In paper applications, it improves coating performance, printability, and surface quality, making it valuable in high-performance paper processing. The steady expansion of packaging quality requirements and paper coating needs continues to drive strong demand for such alcohol across these end-use segments.

- According to Statistics Canada, pulp and paper exports rose 12.2% in September 2024. This supports steady demand in paper-related applications where polyvinyl alcohol is used for coating and binding performance.

MARKET RESTRAINTS

Strong Dependence on Cyclical End-Use Industries Creates Demand Volatility for Product

Polyvinyl alcohol demand is constrained by its high dependence on end-use industries affected by economic cycles, particularly packaging, textiles, construction, paper, and adhesives. When manufacturing activity slows, construction demand weakens, or consumer spending becomes uncertain, demand from these sectors can decline. Since it is used mainly in industrial and performance-based applications, its consumption is aligned with production trends in downstream markets. This makes the market more sensitive to economic slowdowns, cost pressure, and changing demand patterns across key end-use industries.

- As per the U.S. Census Bureau, construction value in 2025 was 1.4% lower than in 2024. This shows how cyclical-sector weakness, such as in construction, can affect demand for PVA in downstream industrial applications.

MARKET OPPORTUNITIES

Rising Use in Water-Soluble and Specialty Packaging Applications Creates Future Growth Potential

Polyvinyl alcohol has growth potential in water-soluble and specialty packaging applications, where controlled dissolution, film strength, and environmental compatibility are important. Its properties make it suitable for packaging detergents, agrochemicals, and other unit-dose products that require convenience and reliable performance. As industries develop more functional and sustainability-focused packaging solutions, the product's use can expand beyond its traditional applications. This creates clear long-term opportunities for the market, supported by product innovation and the growing need for specialty packaging materials.

- According to Eurostat, paper and cardboard packaging waste in the EU reached 34.0 million tons in 2022, making it the largest packaging waste material stream. This supports long-term opportunities for PVA in paper coatings and specialty packaging applications.

MARKET CHALLENGES

Cost Competitiveness and Product Consistency Remain Key Challenges

Polyvinyl alcohol producers face a key challenge in balancing cost competitiveness with consistent product quality. Since the material is used in performance-sensitive applications such as food packaging, paper coatings, adhesives, and textiles, even small changes in quality, viscosity, or solubility can affect customer acceptance. At the same time, producers must manage raw material, energy, and operating costs in a market where pricing flexibility is often limited. This creates pressure on manufacturers to maintain stable production standards while protecting margins and meeting the specific requirements of different end-use applications.

- According to the U.S. Bureau of Labor Statistics, producer prices for goods rose 2.5% in 2025, highlighting the broader cost pressure manufacturers face in managing margins and product consistency.

Segmentation Analysis

By Grade

Strong Film Strength and Chemical Resistance Support Dominance of Fully Hydrolyzed PVA in Consumption

Based on grade, the market is segmented into fully hydrolyzed PVA, partially hydrolyzed PVA, and modified/specialty grades.

The fully hydrolyzed PVA segment accounted for a significant polyvinyl alcohol market share in 2025. This grade leads market consumption as it offers high tensile strength, strong film-forming performance, better chemical resistance, and lower water sensitivity compared to other grades. These properties make it suitable for applications that require durability, structural stability, and reliable performance across industrial processes. Its strong position is supported by demand from end uses where material strength and performance consistency are more important than ease of dissolution. As industries continue to favor dependable, high-performance material grades, fully hydrolyzed PVA remains the leading segment in the market.

The partially hydrolyzed PVA segment is expected to grow at a 5.4% CAGR over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-Use Industry

Strong Use in Coating, Binding, and Surface Treatment Positions Paper as Primary Demand Anchor

By end-use industry, the market is segmented into paper, textiles, construction, adhesives, packaging, and others.

The paper segment accounted for the largest share in 2025. Paper leads to polyvinyl alcohol demand as the material is widely used in coating, binding, and surface treatment applications where strength, printability, and surface quality are important. It improves paper performance by enhancing coating efficiency, pigment binding, and resistance properties, making it valuable for high-quality paper and paperboard production. As paper manufacturers continue to focus on product quality, processing efficiency, and functional performance, PVA remains an important material in this segment, supporting stable demand across a broad range of paper applications.

The packaging segment is expected to grow at a 5.7% CAGR over the forecast period.

Polyvinyl Alcohol Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Polyvinyl Alcohol Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market in 2025 with a value of USD 710.5 million, and is expected to retain its leading role in 2026, reaching USD 741.6 million. The region’s leadership is supported by its large-scale manufacturing base, strong paper and textile production, and broad consumption across packaging, adhesives, and construction applications. High industrial activity, cost-competitive production, and the presence of major downstream processing industries continue to support steady PVA demand, especially in high-volume and performance-driven applications.

China Polyvinyl Alcohol Market

Given Asia Pacific’s strong contribution and China’s large-scale manufacturing footprint, the China market was estimated at USD 308.7 million in 2025, accounting for approximately 43.4% of regional revenues. Demand is supported by the country’s extensive paper, textile, and packaging manufacturing base, as well as strong product use in adhesives, construction materials, and other industrial applications. Its well-established chemical processing industry and high-volume production environment continue to support steady consumption across both standard and performance-oriented grades.

India Polyvinyl Alcohol Market

The Indian market size in 2025 was valued at around USD 73.2 million. Growth is supported by expanding paper and textile production, rising demand from adhesives and packaging applications, and increasing use in construction materials. Expanding downstream manufacturing supports steady demand for PVA grades.

North America

North America remains a significant regional market and reached USD 366.7 million in 2025. Demand is supported by the established use of PVA across paper, adhesives, packaging, construction, and textile applications. The region benefits from mature industrial infrastructure, reliable downstream processing capabilities, and steady demand for performance-oriented grades. However, polyvinyl alcohol market growth remains moderate, as consumption is largely replacement-driven and overall volume expansion is limited by the region’s relatively mature end-use industries.

U.S. Polyvinyl Alcohol Market

The U.S. market in 2025 was valued at USD 327.2 million, representing approximately 89.2% of global revenues. Consumption is driven by demand from paper processing, adhesives, food packaging, construction materials, and textile applications, where PVA is valued for its film-forming ability, binding performance, and suitability for high-quality industrial processes.

Europe

Europe is projected to record modest growth over the forecast period, reaching a valuation of USD 392.5 million by 2025. Strict environmental standards, high energy costs, and strong emphasis on product quality and processing efficiency shape the region. Despite these challenges, steady demand from paper, packaging, adhesives, construction, and textile applications continues to support PVA consumption across industrial and specialty end-use sectors.

Germany Polyvinyl Alcohol Market

Germany’s market reached approximately USD 78.7 million by 2025, equivalent to around 20.0% of the regional market. Demand is supported by strong paper, packaging, adhesive, and construction industries, as well as steady use in technical applications that require reliable film-forming and binding performance.

U.K. Polyvinyl Alcohol Market

The U.K. market in 2025 was valued at USD 71.0 million, accounting for roughly 18.1% of regional revenues. Consumption is concentrated in paper processing, adhesives, packaging, and selected construction and textile applications, where PVA is used for its film-forming ability, binding performance, and process reliability.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth during the forecast period. The Latin America market reached a valuation of USD 109.0 million in 2025, supported by expanding paper and packaging activity, rising adhesive demand, and increasing PVA use in construction and textile applications. In the Middle East & Africa, demand is supported by paper processing, packaging, adhesives, and gradual growth in downstream industrial manufacturing. The Middle East & Africa market reached USD 77.7 million in 2025. Growth in both regions remains steady, supported by improving industrial activity and broader application development across key end-use sectors.

GCC Polyvinyl Alcohol Market

The GCC market accounted for around USD 43.3 million in 2025, representing approximately 55.7% of regional revenues. The increasing packaging industry, construction development, and growing downstream industrial processing support demand. Increasing use in adhesives, paper-related applications, and industrial formulations continues to support market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

High Entry Barriers and Technical Complexity Drive Market Consolidation and Strategic Focus Among Key Players

The market is fairly concentrated and requires a high level of technical expertise, as production know-how, quality consistency requirements, and application-specific performance standards create significant barriers to entry. These factors limit new participation and concentrate supply among a small group of global producers with established manufacturing capabilities and process expertise.

Leading players such as KURARAY CO., LTD., Sekisui Specialty Chemicals America, Mitsubishi Chemical Corporation, China Petrochemical Corporation, and Denka Company Limited focus primarily on improving product quality, developing specialty grades, and strengthening customer-specific supply rather than pursuing aggressive capacity expansion. Recent activities across these key companies highlight a strategic emphasis on performance enhancement, application diversification, and gradual movement toward higher-value product segments to support long-term market positioning.

LIST OF KEY POLYVINYL ALCOHOL COMPANIES PROFILED

- KURARAY CO., LTD. (Japan)

- Sekisui Specialty Chemicals America (U.S.)

- Mitsubishi Chemical Corporation (Japan)

- BOULING CHEMICAL CO., LIMITED (China)

- China Petrochemical Corporation (China)

- Guangzhou Minwei PVA Sales Co., Ltd. (China)

- SNP, Inc. (U.S.)

- Denka Company Limited. (Japan)

- Merck KGaA (Germany)

- 6 Aquapak Polymers Limited (U.K.)

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.9% from 2026-2034 |

| Unit | Value (USD Million), Volume (Kiloton) |

| Segmentation | By Grade, End-Use Industry, and Region |

| By Grade |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1,656.4 million in 2025 and is projected to reach USD 2,525.8 million by 2034.

Recording a CAGR of 4.9%, the market is slated to exhibit steady growth during the forecast period.

The paper end-use industry led the market in 2025.

Asia Pacific held the highest market share in 2025.

The rising PVA demand in packaging, paper, and adhesive applications is the key driver of the market growth, supported by its film-forming, binding, and coating properties.

- 2021-2034

- 2025

- 2021-2024

- 176

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us