Precision Guided Munitions Market Growth, Size, Share, and Analysis, By Platform (Land, Airborne, and Naval), By Operational Mode (Autonomous and Semi-Autonomous), By Type (Tactical Missiles, Guided Rockets, Torpedoes, Interceptor Missiles, and Others), By Component (Guidance & Navigation Systems, Target Acquisition Systems, Propulsion Systems, and Others), By System Type (Inertial Navigation System, Global Positioning Systems, EO/IR, Radar Homing, and Others), By Speed (Subsonic, Supersonic, and Hypersonic), By Range (Short Range, Medium Range, and Others), and Global Forecast 2026-2034

KEY MARKET INSIGHTS

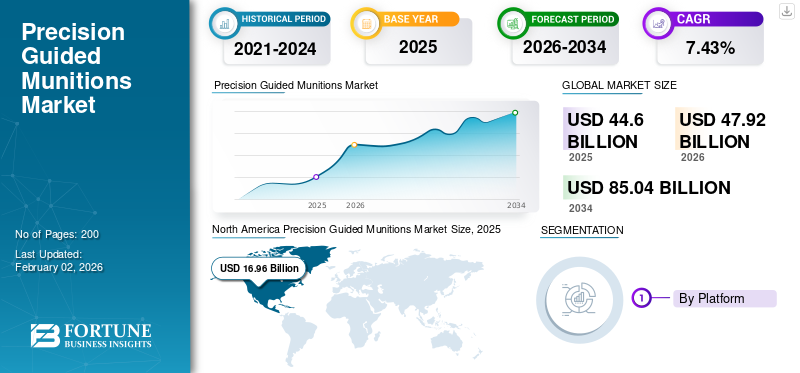

The global precision guided munitions market size was valued at USD 44.60 billion in 2025 and is projected to grow from USD 47.92 billion in 2025 to USD 85.04 billion by 2034, exhibiting a CAGR of 7.43% during the forecast period. North America dominated the guided munitions market with a market share of 38.03% in 2025.

Precision guided munitions are missiles and bombs equipped with guidance systems to strike specific targets with accuracy, minimizing collateral damage. They achieve this accuracy through various technologies such as GPS, laser guidance technology, and inertial navigation systems. The need for enhanced operational effectiveness, reduced collateral damage, and increased military spending drives the demand for precision-guided munitions (PGMs). Factors such as geopolitical tensions, advancements in guidance technologies, and the modernization of military equipment are also contributing to this demand.

Major players in the Precision Guided Munitions market analysis report include Lockheed Martin Corporation, Northrop Grumman Corporation, and Boeing Company, among others. These companies are driving the growth of the Precision Guided Munitions market by investing in next-generation Munitions with enhanced guidance systems, increased autonomy, and advancements in propulsion technologies, as well as AI and ML integration in precision guided munitions to accurately hit the target is further in demand. The rising defense sector, increasing spending, heightened geopolitical tension, and growing threats are prompting these players to innovate and collaborate with military forces globally.

Download Free sample to learn more about this report.

PRECISION GUIDED MUNITIONS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 44.60 billion

- 2026 Market Size: USD 47.92 billion

- 2034 Forecast Market Size: USD 85.04 billion

- CAGR: 7.43% from 2026–2034

- North America dominated the precision-guided munitions market with a 38.03% share in 2025.

- The semi-autonomous segment is expected to account for 62.54% of the market by 2026.

- The airborne platform segment is projected to lead the market with a 42.76% share in 2026.

North America

North America generated USD 16.96 billion in 2025, supported by strong defense spending and military modernization programs.

Europe

Europe accounted for 24.10% of the global market in 2025, driven by NATO defense upgrades and security investments.

Asia Pacific

Asia Pacific captured 22.52% of the global market in 2025, fueled by rising defense budgets and modernization initiatives.

U.S.

The market is projected to reach USD 16.65 billion in 2026.

Japan

The market is projected to reach USD 1.21 billion in 2026

Read More

Market Dynamics

Market Drivers

Rising Military Spending and Demand for Advanced Weapons Drive Market Growth

Nations globally are focused on developing their existing weapon capabilities, fueled by factors such as increasing geopolitical tensions, countermeasure efforts, and the need to modernize the aging fleet. Moreover, nations such as the U.S. and Russia are focusing on making conventional ammunition into precision-guided munitions by installing the precision-guided kit into the existing ammunition. Additionally, demand for advanced defense weaponry is increasing, for instance, PGMs, with guidance systems such as GPS, laser guidance technology, and infrared sensors, offer superior accuracy, minimizing collateral damage and enhancing the effectiveness of military operations.

Regional Conflicts and Increasing Tension Fuels Market Growth

Regional conflicts such as the ongoing Russia-Ukraine war have fueled the demand for advanced precision-guided munitions in Europe. For instance, in July 2025, the US will provide aid to help Ukraine upgrade cheap drones into precision weapons. Pentagon contract worth USD 50 million agreed with US-German firm as Russia steps up its nightly bombardment.

Moreover, in December 2024, the Kalashnikov completed delivery of high-precision weapons, marking an achievement in the company's operations. The deliveries consist of systems, such as surface-to-air guided missiles (SAMs) for the Strela air defense system, air-launched guided anti-tank missiles "Vikhr-1," and guided artillery shells "Kitolov-2M."

These precision-guided weapons, which have witnessed large use in the ongoing Special Military Operation (SMO) in the Russia-Ukraine war as well as in the recent Israel-Iran conflict, have resulted in the market experiencing a significant increase in both production and deployment of precision-guided munitions.

Market Restraints

High Development and Procurement Costs with Integration Complexities Hinder Market Growth

The initial investment in developing or procuring the precision-guided munitions ranges from several million to billions, depending upon several factors such as integrated technology, required range, and other weapon capabilities. PGMs require specialized integration, testing, and maintenance procedures, including specific storage requirements, electronics maintenance, and software updates. This can add to the overall cost and complexity of their deployment, resulting in hindering the market growth.

For Instance, according to towards report on missiles and bombs cost reported that the AIM-9X Sidewinder (Air Force) Unitary cost is around USD 0.47 million, the AIM-9X Sidewinder (Navy) is around USD 0.43 million and the cost of GBU-53/B Storm Breaker/Small Diameter Bomb II (SDB II) (Air Force) is USD 0.19 million. These unit prices are averages for the entire projected 2021 Fiscal Year orders.

Sensors Reliability and Export Restriction to Hamper Market Growth

The accuracy and reliability of autonomous PGMs depend heavily on sensor data, and errors or malfunctions in sensor readings or targeting algorithms can lead to misdirection. Moreover, factors such as weather, light, and obscurants (smoke, dust) can negatively impact the accuracy of sensor-based guidance systems. Apart from this, advancements in sensor bandwidth, miniaturization, and integration of subsystems are needed to overcome these restraints for creating more versatile and accurate PGMs.

Market Opportunities

Technological Advancement from Sensors Miniaturization to Integration of AI & ML Drives Market Opportunity

The integration of artificial intelligence and machine learning transforms PGMs into "smart weapons" with enhanced capabilities such as advanced defense, target recognition, real-time trajectory correction, autonomous decision-making, and network-enabled capabilities. Moreover, PGMs with multiple guidance systems combine technologies such as GPS, Inertial Navigation Systems (INS), laser, infrared (IR), and radar to enhance accuracy and adaptability, ensuring effective operation even in challenging conditions.

Additionally, the use of innovative materials and manufacturing techniques, such as 3D printing, enables the creation of complex and customized munitions, offering potential advantages in logistics and adaptability to different combat situations. It opens the market opportunity for new players to enter the market.

For instance, in May 2023, the U.S. Army awarded BAE Systems a contract worth USD 72.5 million for three years. This contract involves the continuous research and development of precision-guided munitions.

Precision Guide Munition Market Trends

Development of Smaller PGMs for Real-time Targeting Adjustments Drives Market Trend

Development of smaller, more powerful PGMs for wider deployment, the integration of AI and data analytics for real-time targeting adjustments, and the creation of PGMs for use across multiple domains (land, air, sea, and space). Ensuring that PGMs can operate seamlessly with different platforms and communication systems across different domains is crucial for effective joint operations. These advancements aim to improve the effectiveness and adaptability of PGMs in modern warfare.

For instance, in July 2024, OKSI won a contract to supply multiple contracts totaling nearly USD 6 million from USSOCOM and the Air Force Research Laboratory (AFRL) for their ARMGDN seeker. ARMGDN is a capability enhancement to BAE Systems’ APKWS laser-guidance kit, providing passive target acquisition and tracking for precision engagements.

Download Free sample to learn more about this report.

Autonomous Targeting Technologies Becoming More Prevalent in Market

While GPS is a primary guidance system, alternative navigation is being developed for GPS-denied environments. The integration of AI and autonomous capabilities enables PGMs to operate with minimal human intervention, improving accuracy and reducing operational costs. Additionally, there is also significant investment in hypersonic PGM technology. Modernization programs are driving the adoption of PGMs, and collaborations between governments and manufacturers are fostering innovation.

For instance, in June 2025, Sweden signed a contract with European missile manufacturer MBDA for the supply of Akeron MP anti-tank guided missiles, which feature the IR seeker and GPS Seeker.

Impact of Increasing Geopolitical Tensions, Ongoing, and Recent Conflicts in Europe, the Middle East, and the Asia Pacific.

Growing geopolitical tensions and regional fights, primarily in the South China Sea, Eastern Europe (Russia-Ukraine), and the Middle East (Israel-Iran & Hamas), are significantly fast-tracking the demand for Precision Guided Munitions.

Russia-Ukraine Conflict

Increased Demand

The Russia-Ukraine war has significantly influenced the precision-guided munitions (PGM) market by highlighting their crucial role in modern warfare and revealing both their strengths and vulnerabilities. The war has demonstrated the value of PGMs, leading to increased demand from countries seeking to enhance their military capabilities.

The conflict has encouraged increased demand for PGMs due to their demonstrated effectiveness in striking targets with precision and reducing collateral damage. However, the war has also exposed challenges related to GPS jamming and the effectiveness of PGMs in highly contested electromagnetic environments.

Miniaturization

The need for smaller, lighter PGMs that can be deployed from various platforms, including drones, is also gaining attention. For instance, in June 2025, Ukraine launched an innovative series of attacks against four Russian airbases, including some deep within Russian territory. In this Spider Web mission, they used precision-guided munitions in the form of inexpensive quad-copters armed with small explosive charges.

Middle East Precision Guidance Munitions Market View after Israel – Iran & Hamas Conflict

The Israel-Hamas conflict and subsequent tensions with Iran have significantly affected the Middle East's precision-guided munitions (PGM) market, with increased demand for advanced weaponry and a shift in regional power dynamics.

Israel, a major player in the PGM industry, has witnessed a surge in weapons sales, particularly to European nations, while also facing the challenge of adapting its defense systems to counter evolving threats.

For instance, in July 2025, in total, Israel dropped more than 4,000 precision-guided munitions on Iran, striking distances as far as 1,400 miles from Israeli bases. Highlighting the importance and need for advanced precision-guided munitions. Further fueling the demand for PGMs in Europe and the ME&A region

Increasing South China Sea Tension to Fuel the Demand for PGMs

The South China Sea dispute involves overlapping territorial and maritime claims by several countries, primarily China, Brunei, Taiwan, Philippines, Vietnam, and Malaysia. These tensions have resulted in driving the demand for Sea Platform-based PGMs, with regional tensions and territorial disputes fueling increased defense spending and modernization efforts.

SEGMENTATION ANALYSIS

By Platform

The platform divides the market into land, airborne, and naval platforms.

The airborne segment is projected to dominate the market with a share of 42.76% in 2026, as air-launched precision-guided munitions (PGMs) can cover long distances, enabling attacks on targets located deep within enemy territory or in areas that are difficult for other platforms to reach. Additionally, the airborne segment is preferred for missions such as Suppression of Enemy Air Defenses (SEAD), close air support, strategic interdiction, and counterterrorism, providing flexibility and effectiveness across a range of scenarios.

The naval segment is anticipated to show fastest growth with registering the highest CAGR during the forecast period. A combination of factors drives the naval segment growth, including increased naval spending, the need for advanced anti-ship and anti-submarine warfare capabilities, and the ongoing development of network-centric warfare. These factors are driving demand for PGMs that can operate in challenging maritime environments and offer superior accuracy and versatility.

These precision guided munitions market trends are particularly noticeable in the Asia Pacific region, where maritime disputes in the South China Sea and the need to strengthen defense capabilities are driving investments in precision-guided weapons.

To know how our report can help streamline your business, Speak to Analyst

By Operation Mode

The operation mode segment divides the market into autonomous and semi-autonomous segments.

The autonomous segment holds the largest global precious guided munitions market share and is anticipated to be the fastest growing segment during the forecast period. The segment dominance is attributed to increasing demand for advanced military capabilities that enhance operational efficiency and reduce the need for human intervention in high-risk combat scenarios. Investments in defense modernization programs are fueling the development and acquisition of autonomous systems, allowing militaries to maintain strategic superiority.

The semi-autonomous precision guided munitions segment is projected to dominate the market with a share of 62.54% in 2026, by operational mode segment. Semi-autonomous is driven by a combination of factors, including increased demand for precision strikes, cost-effectiveness compared to fully autonomous systems, and a growing preference for loitering munitions.

For instance, GPS-guided systems (autonomous) are vulnerable to jamming and interference, while semi-autonomous systems can utilize other guidance systems such as laser-guided or infrared guidance to overcome the limitation, resulting in semi-autonomous segments holding a substantial share in the market for precision guided munitions.

By Type

Furthermore, the market by type is segmented into tactical missiles (surface to surface and air to surface), guided rockets (surface to surface, air to surface, and surface to air), torpedoes, interceptor missiles (MANPADS and Mobile ADS), loitering munitions (recoverable and expendable), and guided ammunition (guided mortars, guided artillery shells, and glide bombs).

Tactical missiles dominated the precision-guided munitions market projected to dominate the market with a share of 38.58% in 2026. Tactical missiles' versatility and effectiveness in modern warfare, particularly in scenarios that require short to medium-range engagement and high precision strikes. Their widespread adoption across various platforms including ground launchers, aircraft, and naval vessels, coupled with advancements in guidance systems, contributes to their dominance in the market for precision guided munitions.

For instance, in January 2024, the Australian government ensured Australia starts manufacturing Guided Multiple Launch Rocket System (GMLRS) missiles from 2025, following the signing of a USD 37.4 million contract between Defense and Lockheed Martin Australia.

The loitering munitions segment is anticipated to be the fastest-growing segment in the PGMs market. The fastest-paced growth of the segment is attributed to their unique ability to combine intelligence, surveillance, reconnaissance (ISR), and strike capabilities into a single, cost-effective system. This makes them an attractive choice in modern warfare scenarios, including asymmetric and urban environments, where the ability to loiter, identify targets, and strike with precision is crucial. This results in the segment's fastest growth.

For instance, in June 2024, UVision Inc., a global leader in aerial loitering systems, and Mistral Inc., a distinguished player in the US defense industry, secured a USD 73.5 million contract with the U.S. Government to supply Hero-120SF Loitering Munitions for the U.S. Special Operations Command.

By Systems

The systems segment divided the market into guidance & navigation systems, target acquisition systems, propulsion systems, warheads, and power supply systems.

Guidance & navigation systems segment is anticipated to hold a dominant market share of 37.77% in 2026. The dominance of these systems is attributed to their widespread use in various types of precision-guided munitions, such as tactical missiles, guided rockets, and loitering munitions, among others, where precision and reliability are important. Additionally, G&N systems significantly improve the accuracy and effectiveness of these weapons. Increased global defense spending, advancements in fully autonomous missiles, and the growing space-based defense industry are key drivers of this dominance.

For instance, in January 2023, CAES was awarded a contract worth more than USD 24 million from Northrop Grumman to provide M-Code GPS antennas for Precision Guidance Kits (PGK).

The target acquisition systems segment is anticipated to be the fastest-growing segment during the forecast period. Targeting acquisition systems play a crucial role in enabling precision strikes and enhancing operational efficiency. Moreover, increasing emphasis on AI and ML to get the maximum efficiency in target acquisitions and precise hitting is further driving the market growth.

By Technology

The system type segment divides the market into Inertial Navigation System (INS), Global Positioning System (GPS), EO/IR, radar homing, laser-guided, dual-technology, and others.

The Inertial Navigation Systems (INS) segment dominates the precision guided munitions market. INS provides a self-contained, highly reliable navigation solution independent of external signals, making it crucial for precision targeting various environments. GPS, EO/IR, Radar Homing, and Laser-Guided systems offer complementary capabilities and are often integrated with INS to enhance accuracy and target acquisition.

Dual-technology segments are anticipated to be the fastest-growing segment in the market during the 2025-2032 period. Dual technology allows PGMs enhanced flexibility and effectiveness in diverse operational environments. These systems combine multiple guidance methods (such as laser and GPS) to offer greater targeting precision and adaptability, making them valuable in a range of applications.

Ongoing advancements in sensor fusion, AI, and machine learning are further enhancing the capabilities of dual-technology systems, making them more reliable and effective, according to Polaris Market Research.

For instance, in January 2024, the U.S. Air Force awarded Raytheon, an RTX business, a USD 345 million contract to produce and deliver more than 1,500 StormBreaker smart weapons. StormBreaker is the leading air-to-surface, network-enabled weapon that can engage moving targets in all weather conditions using its multi-effects warhead and tri-mode seeker.

By Speed

The speed segment categorizes the market into subsonic, supersonic, and hypersonic.

The sub-sonic sub-segment dominates the speed segment. The dominance of the sub-sonic segment is attributed to its cost-effectiveness, reliability, and compatibility with existing military platforms. Sub-sonic PGMs, such as cruise missiles, are used widely due to their ability to deliver precise strikes with minimal collateral damage, aligning with modern warfare policies that highlight precision and efficiency. Additionally, Sub-sonic PGMs are often designed to be compatible with a wide range of existing military platforms, such as aircraft, ships, and submarines, making them a practical choice for many defense forces.

For instance, in August 2023, the U.S. Army awarded Raytheon Technologies a contract worth USD 200 million to supply advanced precision-guided artillery munitions. This contract highlights the ongoing commitment to enhancing U.S. land-based artillery capabilities through modern PGM systems.

The supersonic segment is anticipated to be the fastest-growing segment during the forecast period, by registering the highest CAGR. The growth is primarily driven by the need for advanced weaponry in modern warfare. Increasing geopolitical tensions, military modernization programs, and the strategic advantages offered by supersonic are further driving the demand for advanced, reliable, and more lethal supersonic PGMs.

Additionally, continued advancements in propulsion, materials, and guidance systems, and integration of artificial intelligence and machine learning are driving the development of even faster and accurate hypersonic and supersonic weapons.

By Range

The market is segmented by range into short range (up to 100 km), medium range (100 – 250 km), long range (250 – 500 km), and extended range (above 500 km).

The short-range (up to 100 km) segment dominates the market, holding the largest share of the precision-guided munitions market, and is anticipated to be the fastest-growing segment during the forecast period. Short-range weapons' versatility, affordability, and suitability for various conflict scenarios, particularly in urban warfare and counter-insurgency operations, result in short-range PGMs dominating the market. Short-range PGMs include guided artillery, loitering munitions, and laser-guided rockets, which are effective against close-range, time-critical threats and offer advantages such as accuracy, minimal collateral damage, and logistics costs. Additionally, short-range PGMs are easier to deploy and reload, making them suitable for circulating and maneuvering in intensive operations.

Moreover, the use of low-cost PGM kits is further driving the segment growth, as this kit converts conventional unguided munitions into precision-guided weapons. This transformation is driven by advancements in guidance technology, including GPS, inertial navigation, and laser guidance technology.

For instance, in August 2024, Finland secured a USD 70 million deal for 5,500 M1156A1 Precision Guidance Kits from the U.S. Department of State for artillery ammunition.

The medium-range (100-250 km) segment holds the second-largest market share, attributable to the segment's balance of range and versatility. This makes it a popular choice for military forces across various applications.

Precision Guide Munition Market Regional Outlook

Based on region, the market is divided into North America, Europe, Asia Pacific, Middle East, and the rest of the World.

North America

North America Precision Guided Munitions Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 16.96 billion in 2025, representing 38.03% of the global industry, and is expected to reach USD 18.26 billion in 2026. Driven by substantial defense expenditure, early adoption of advanced technologies, and ongoing military modernization programs. The region's strong focus on homeland security and counter-terrorism initiatives further fuels market growth.

The U.S. holds a leading position in the North American precision guided munitions market size, driven by its strong economy, technological advancements, and substantial defense spending. With the presence of key players in the region, such as RTX Corporation, Northrop Grumman, Lockheed Martin Corporation, and others. Moreover, the US has been at the forefront of adopting and integrating technologies such as AI, machine learning, and data analytics into precision-guided munitions. The U.S. market is projected to reach USD 16.65 billion by 2026.

For instance, in August 2024, the U.S. Army awarded Saab an Indefinite Delivery, Indefinite Quantity (IDIQ) contract worth USD 494 million over five years for the XM919 Individual Assault Munition (IAM) program. Saab’s solution is the AT4CS TW (Confined Space Tandem Warhead).

Europe

The precision-guided munitions market in Europe is experiencing significant growth, driven by increasing security concerns and defense spending. The market is fueled by several factors such as ongoing conflict between Russia and Ukraine, rising geopolitical tensions, NATO defense upgrades, and growing homeland security budgets. Europe recorded a market size of USD 10.75 billion in 2025, capturing 24.10% of the global market share, and is projected to reach USD 11.51 billion in 2026.

For instance, in June 2025, NATO member countries are increasing defense spending, with a promise to allocate 5% of GDP towards defense by 2035, which will result in creating a strong demand for advanced security solutions such as air-defense systems, advanced threat detection systems, and precision-guided munitions. They will allocate at least 3.5% of GDP annually based on the agreed definition of NATO defense expenditure by 2035 to resource core defense requirements and to meet the NATO Capability Targets. The UK market is projected to reach USD 5.23 billion by 2026, and the Germany market is projected to reach USD 1.91 billion by 2026.

Asia Pacific

In 2025, Asia Pacific represented USD 10.05 billion, accounting for 22.52% of the worldwide market, and is projected to grow to USD 10.87 billion in 2026. Factors such as ongoing territorial disputes, rising military spending, and modernization programs are driving the Asia Pacific Precision Guided Munitions Market growth. Rising tensions and territorial disputes between countries such as India and Pakistan, China and Taiwan, the recent Thailand and Cambodia conflict, and the South China Sea dispute in the region are fueling the demand for advanced weaponry, including PGMs, to enhance defense capabilities. The Japan market is projected to reach USD 1.21 billion by 2026, the China market is projected to reach USD 5.04 billion by 2026, and the India market is projected to reach USD 2.5 billion by 2026.

Major countries such as China, India, Japan, Australia, and South Korea are investing heavily in the PGMs acquisition and development. For instance, India is strengthening its defense capabilities with missiles the Prithvi, Agni, and Brahmos, while China is also investing heavily in precision strike systems.

For instance, in January 2024, India’s Ministry of Defense awarded a contract to Bharat Dynamics Limited for the supply of advanced precision-guided munitions worth USD 500 million. This procurement is part of India's strategy to enhance its military capabilities amid escalating regional tensions.

Middle East

The Middle East holds a significant share of the precision-guided munitions market, and the growth in the region is driven by regional conflicts, rising defense spending, and modernization efforts. Saudi Arabia, UAE, and Israel, among others, are major players in this market, with these countries investing heavily in advanced weaponry and domestic defense manufacturing. Middle East & Africa contributed 9.29% to the global market in 2025, with a valuation of USD 4.14 billion, and is projected to reach USD 4.41 billion in 2026.

For instance, in March 2025, the U.S. State Department approved the first sale of advanced precision kill weapon systems to Saudi Arabia for an estimated cost of USD 100 million. The Advanced Precision Kill Weapon System (APKWS) approved for sale to Saudi Arabia is a laser-guided rocket that can hit both airborne and surface targets, it said in a statement on Thursday.

Rest of the World

Africa and Latin America further divide the rest of the world segment. The Latin America market was valued at USD 2.7 billion in 2025, capturing 6.06% of global revenue, and is estimated to reach USD 2.87 billion in 2026. Africa and Latin America regions hold smaller but growing shares in the global precision-guided munitions market. These regions, particularly Brazil, Argentina, Egypt, and South Africa, are experiencing increased demand due to heightened security concerns, geopolitical instability, and growing defense budgets.

Competitive Landscape

Key Industry Players

Defense OEM Manufacturers Characterize the Market with Technological Advancements and Strategic Partnerships

The competitive landscape of the precision guided munitions market is expected to grow, featuring key players such as Lockheed Martin, Northrop Grumman Corp., and RTX, among others. Key players focus on growing investment in research and development, a diversified product portfolio of precision guided munitions, and strategic acquisitions. The key market players focus on business expansion strategies such as agreements, mergers and acquisitions, product portfolio growth, and long-term innovation contracts with multinational companies included in the market.

These companies are leveraging advanced technologies, including AI and ML integration, enhanced sensor technology, and improved lightweight materials to enhance the effectiveness of their detection, tracking, and identification of targets. Overall, the focus on technological integration with AI & ML, as well as advanced guidance systems, will drive significant growth in the market over the coming years.

LIST OF KEY PRECISION GUIDE MUNITION COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Raytheon Technologies (U.S.)

- General Dynamics Corporation (U.S.)

- Boeing Company (U.S.)

- BAE Systems (U.K.)

- Elbit Systems (Israel)

- Israel Aerospace Industries (Israel)

- Kongsberg Gruppen (Norway)

- Leonardo S.p.A. (Italy)

- MBDA (Europe)

- Rheinmetall AG (Germany)

- Saab AB (Sweden)

- Thales Group (France)

- General Atomics (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In March 2025, the U.S. State Department approved a USD 91.2 million sale of precision-guided munitions to Australia. Through this contract, Canberra will receive 54 Guided Multiple Launch Rocket Systems-Alternate Warhead (GMLRS-AW) rounds, along with telemetry kits, engineering services, and related support.

- In June 2025, BAE Systems signed a new contract worth USD 62 million with the Swedish Defense Materiel Administration to supply additional BONUS precision-guided munitions to the Swedish Armed Forces.

- In January 2024, France's defense agency announced a tender for the production of 155-mm artillery shells currently being held by Spanish companies. The main condition of the tender is companies’ ability to produce shells in large volumes. The tender is due to close in January 2024, after which the Ministry will place a large order for 155mm ammunition. The cost of allocated funds for the purchase of 155-mm artillery ammunition is USD 531 million.

- In April 2024, the U.K. provided Dual-Mode Paveway IV guided bombs to Ukraine to boost its military capabilities. The British government announced that it would provide its largest-ever tranche of military aid to Ukraine as part of a deal worth USD 622 million.

- In April 2024, South Korean defense prime Hanwha Aerospace signed a second executive contract with the Polish Armament Agency to supply additional K239 Chunmoo multiple launch rocket systems (MLRS), long-range CTM-290 guided missiles, and transfer of launch module and rocket technology. In contrast, worth USD 3.55 billion, the firm will supply 218 systems and several thousand precision munitions along with logistics and training support through 2025.

- In October 2024, the U.S. Air Force awarded Boeing a contract worth USD 600 million to supply Joint Direct Attack Munition (JDAM) and Laser JDAM testing and integration. The indefinite-delivery/indefinite-quantity contract covers technical services and support, aircraft and weapon system integration, and sustainment.

- In December 2024, Israeli company SpearUAV has announced a contract for its Viper 300 loitering munitions valued at USD 20 million, with options that could increase the total to USD 60 million.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphases key aspects such as key players, offerings, objects, and end-user of precision guided munitions. Moreover, the report deals with insights into precision guided munitions market trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, market status, and highlights key industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have subsidized the sizing of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.43% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Platform

|

|

By Operation Mode

|

|

|

By Type

|

|

|

By Systems

|

|

|

By Technology

|

|

|

By Speed

|

|

|

By Range

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 47.92 Billion in 2026 and is anticipated to be USD 85.04 billion by 2034.

The market is anticipated to grow at a CAGR of 7.43% over the forecast period.

The top fifteen players in the industry are Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies, General Dynamics Corporation, Boeing Company, BAE Systems Inc., Elbit Systems Inc., Israel Aerospace Industries, Kongsberg Gruppen, and Leonardo S.p.A. MBDA, Rheinmetall AG, Saab AB, Thales Group, and General Atomics based on parameters such as services portfolio, regional presence, and industry experience.

North America dominated the guided munitions market with a market share of 38.03% in 2025.

Regional conflicts and increasing tension in the Middle East & Africa, and some regions of Asia Pacific, further fuel the market

Sensors reliability and export restriction to hamper the market growth

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us