Prescription Sunglasses Market Size, Share & Industry Analysis, By Frame Style (Round, Square, Aviator, Rectangle, and Others), By Lens Type (Polarized and Non-Polarized), By Application (Myopia, Hyperopia, and Others), By Distribution Channel (Retail Store, Online Store, and Ophthalmic Clinics), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

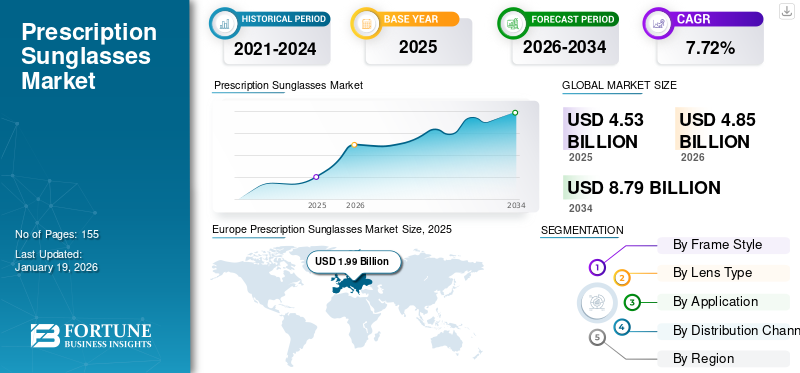

The global prescription sunglasses market size was valued at USD 4.53 billion in 2025. The market is projected to grow from USD 4.85 billion in 2026 to USD 8.79 billion by 2034, exhibiting a CAGR of 7.72% during the forecast period. Europe dominated the prescription sunglasses market with a market share of 26.24% in 2025.

Prescription sunglasses offer both correction and protection properties at the same time. As a result, they are designed for individuals who need optical correction (such as eyeglasses) and want to shield their eyes from harmful ultraviolet (UV) rays.

The market is anticipated to grow, driven by the growing awareness of UV protection among patients with vision disorders and refractive errors. This is expected to fuel the demand for such products across the globe. Moreover, the surge of online optical stores and the integration of artificial intelligence (AI) in lens fitting are also contributing to the market expansion.

Key players in the market include Carl Zeiss Meditec AG, EssilorLuxottica, and SAFILO GROUP S.P.A. These companies are expanding their product portfolio and distribution network to gain a significant portion of the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Burden of Ocular Disorders to Propel Market Expansion

The increasing burden of ocular diseases such as myopia and presbyopia, especially among children and adolescents, and reluctance among the general population toward vision correction are leading to a large population base suffering from vision impairment globally. Additionally, untreated refractive errors are among the leading causes of vision impairment and blindness globally.

- For instance, according to the 2025 data published by the International Myopia Institute (IMI), an estimated 30.0% of the population is suffering from nearsightedness globally. Furthermore, according to the same source, an estimated 50.0% of the population will be myopic by 2050 globally.

Additionally, the focus of major players on emerging markets is also anticipated to increase the penetration of such products in high-potential markets such as China, India, and Brazil, which is expected to drive the global prescription sunglasses market growth.

Market Restraints

Limited Reimbursement for Eyewear Products May Hamper Market Growth

In many developing and developed countries, the majority of the insurance providers do not cover sunglasses or any other prescription glasses in medical insurance policies. For instance, the U.S. Centers for Medicare and Medicaid Services does not offer coverage for eyeglasses and contact lenses. It only provides partial coverage for corrective lenses if the patient has undergone cataract surgery to implant an intraocular lens.

In India, National Insurance Company Limited products such as spectacles, sunglasses, contact lenses, hearing aids, and cochlear implants are excluded from coverage. This may lead patients to pay out-of-pocket costs for such products. In such a scenario, the limited coverage for prescription sunglasses may deter their usage among individuals who are not able to pay out-of-pocket costs.

Market Opportunities

Rising Myopia Cases and Innovation Fuels Market Growth

The market in emerging nations is rising due to the increasing awareness of prescription sunglasses, entry of major players, and increasing cases of myopia and other ophthalmic disorders. This is mainly due to the growing demand for consumers' high quality and technologically advanced products in India and China due to a large patient pool. Such a scenario offers high potential for key players for their product growth. Moreover, prominent companies are shifting from traditional distribution models toward omnichannel models.

- For instance, in July 2024, Lenskart founders invested almost USD 20 million in the omnichannel to extend the marketing network for prescription sunglasses.

This distribution model enables companies to market their products directly to customers via online channels. This is expected to represent a significant opportunity for key players to cater to untapped markets in developing regions.

Market Challenges

High Costs of Prescription Sunglasses May Hamper Market Growth

Prescription sunglasses typically cost more than regular sunglasses or other prescription eyewear products. These costs are significantly high due to lens customization and the use of high-quality materials, which may limit accessibility and adoption in price-sensitive regions.

Moreover, the tariffs imposed on imported eyewear components, including sunglasses, particularly between the U.S., Europe, and China, are anticipated to increase the prices of these products.

Key players are also facing stricter import/export rules in such countries, which is expected to hamper product adoption and hinder market growth.

Prescription Sunglasses Market Trends

Merging of Fashion and Function to Emerge as the Latest Market Trend

Currently, prescription sunglasses are considered as smart wearables. Integration with bluetooth and augmented reality functionalities is opening new applications of such products in fitness, entertainment, and hands-free communications.

- In May 2025, Meta announced that it will introduce Ray-Ban Meta glasses to India, combining iconic style and advanced technology to let people stay connected.

Additionally, these sunglasses are part of high-end fashion collections, influenced by collaborations among luxury brands and optical giants. Moreover, key players are focused on designing new product lines to increase product diversification with higher availability in the market.

Moreover, a shift toward the utilization of sustainable materials such as recycled plastics, bio-acetate, and bamboo in frames is gaining traction. Users, especially millennials and Gen Z, are opting for eco-friendly brands.

Download Free sample to learn more about this report.

IMPACT OF COVID-19

COVID-19 Lockdowns Disrupted Supply Chains Resulting in Market Decline

The COVID-19 pandemic witnessed a negative impact on the global market in 2020. The eyewear industry heavily relies on the global supply chain, particularly from manufacturing hubs such as China. As a result, the lockdown restrictions and closure of many factories during the pandemic disrupted the supply chain and led to a product shortage. Moreover, the reduced number of patient visits to ophthalmologists also leads to decreased prescriptions, thereby declining the product’s adoption rate. Such a scenario led to negative growth in 2020 due to the pandemic.

However, the relaxation of pandemic restrictions led to a gradual rise in patient visits for eye examinations and an increase in the production and supply of products. This helped the market regain its momentum in 2021 and 2022.

SEGMENTATION ANALYSIS

By Frame Style

Popularity of Rectangular Frame as a Fashionable Option Fuel Segment Growth

Based on frame style, the market is classified into round, square, aviator, rectangle, and others.

The rectangle segment dominated the market in 2024, attributable to the high preference for this shape among aged individuals as well as young adults, encouraging major players to introduce new models. As a result, this is boosting its availability globally, contributing to the segment’s expansion.

- For instance, according to the article published by Specsview Technologies Private Ltd., rectangle sunglasses are considered a fashionable and adaptable option for individuals wishing to improve their appearance.

The square shape accounted for the second-largest share of the global market in 2024. Square frames can enhance both round and angular face shapes, adding definition and balance. Additionally, the popularity of square sunglasses is influenced by their presence in pop culture and fashion trends, which is expected to fuel the segment's growth.

By Lens Type

Rising Awareness of UV Protection Boosted Non-Polarized Segment Growth

Based on lens type, the market is classified into polarized and non-polarized.

The non-polarized segment dominated the market in 2024. In countries with high sunlight, non-polarized sunglasses provide essential UV protection and vision correction, making them a viable and fashionable choice for many users. Such a scenario is anticipated to drive the segment growth in the forthcoming years.

The polarized segment held a substantial market share in 2024. The visual clarity offered by polarized lenses has made them a popular choice for individuals spending a lot of time outdoors or having specific needs for enhanced vision.

- For instance, as recorded in May 2019, Duplin Eye Associates polarized prescription lens wearers are empowered to see more clearly in every outside situation.

By Application

High Prevalence of Myopia Fueled Segment Growth

Based on application, the market is classified into myopia, hyperopia, and others.

The myopia segment dominated the market in 2024. The growth is attributed to the increasing detection rate of myopia (nearsightedness) among the majority of the global population. This is increasing the recommendation of prescription glasses, including sunglasses, for individuals who spend most of their time outdoors.

- For instance, according to the article published by Pair Eyewear in January 2025, more than 40.0% of U.S. individuals are suffering from nearsightedness.

The hyperopia segment held the second-largest market share in 2024. The growth is attributed to the increasing incidence of hyperopia in recent years. People with hyperopia often need to wear glasses for close vision, and prescription sunglasses help them maintain clear vision in bright outdoor conditions.

By Distribution Channel

Strategic Initiatives by Key Players Fueled Retail Store Segment Growth

Based on distribution channel, the market is segmented into retail store, online store, and ophthalmic clinics.

The retail stores segment dominated the market in 2024 due to the strong emphasis of key market players on the acquisition of shares in the retail outlets of eyewear products to increase the supply of sunglasses.

- For instance, in July 2024, Fielmann AG announced the acquisition of Shopko Optical, an optical retailer operating over 140 stores in the U.S.

The online stores segment is projected to expand at the highest CAGR in the forthcoming years. This is highly attributed to the increasing sale of sunglasses due to the rapid growth in online delivery, which provides customers access to top brands. Moreover, several online stores have started providing branded sunglasses, including prescription ones from prominent market players.

The ophthalmic clinics segment is projected to grow at a significant rate during the forecast period. The increasing diagnostic rate of vision issues through ophthalmologists is expected to fuel the sale of eyewear products, such as prescription sunglasses, through these channels, which is expected to drive the segment’s growth in the coming years.

Prescription Sunglasses Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Europe

Europe Prescription Sunglasses Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe maintained a strong presence in the global market, reaching USD 1.99 billion in 2025, accounting for 26.24% share, and is expected to reach USD 2.13 billion in 2026. The growth was due to the strong fashion culture in Germany, France, and Italy, which is propelling the demand for prescription sunglasses. Moreover, the presence of leading distributors in these countries is also increasing product availability.

- For instance, as of 2025, Shade Station offers prescription sunglasses at discounted prices in the U.K.

North America

The North America region captured 17.25% of the global market in 2025, generating USD 1.28 billion in revenue, and is projected to reach USD 1.36 billion in 2026. The market is expanding primarily due to greater patient awareness of vision correction treatments and higher penetration of eyewear products, including prescription sunglasses, in developed countries.

In the U.S., the strong presence of industry giants and early adoption of wearable tech is projected to drive the country’s market growth during the forecast period.

- For instance, Warby Parker expanded its presence with 40 physical stores across the U.S. and Canada in 2023.

Asia Pacific

In 2025, Asia Pacific generated USD 0.82 billion, contributing 12.43% to global market revenue, and is projected to grow to USD 0.89 billion in 2026. Increasing middle-class income and booming e-commerce platforms are making prescription sunglasses more accessible in India and Southeast Asian countries. The rising prevalence of ocular diseases in the region is expected to contribute to the high penetration of such products for vision correction.

- For instance, according to the data published by the CORXEL in August 2021, an estimated more than 400 million people in China are presbyopic.

Latin America and the Middle East & Africa

The Latin American market is expected to grow significantly during the forecast period. The Latin America market generated USD 0.28 billion in 2025, representing 11.77% of the global market landscape, and is expected to reach USD 0.3 billion in 2026. The growth can be attributed to the increasing healthcare expenditure in Brazil, which may have contributed to the affordability of prescription sunglasses with increasing fashion trends.

Middle East & Africa recorded a market size of USD 0.17 billion in 2025, capturing 9.44% of the global market share, and is projected to reach USD 0.18 billion in 2026. The increasing awareness about sun protection in the Middle Eastern region is driving the demand for the utilization of sunglasses, including prescribed ones. In addition, the rising number of ophthalmologists in the region is contributing to the high diagnostic rate and recommendation of sunglasses in the region.

- For instance, as reported by the National Center for Biotechnology Information (NCBI) in March 2024, Saudi Arabia had 2,608 registered ophthalmologists, translating to about 81 ophthalmologists for every 1 million residents as recorded in January 2023.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Implementation of Strategic Initiatives to Increase Their Market Share

The market is fragmented, with many companies, including Carl Zeiss Meditec AG and EssilorLuxottica, accounting for substantial global market share. The dominance of these companies is attributable to the increasing number of product launches and strategic collaborations with other players to strengthen their market positions.

Fielmann AG, SAFILO GROUP S.P.A., and others, are focusing on strengthening their distribution network and launching e-commerce websites to increase product reach and sales globally. This is expected to improve their market share during the forecast period.

List of Key Prescription Sunglasses Companies Profiled

- Carl Zeiss Meditec AG (Germany)

- EssilorLuxottica (U.S.)

- Fielmann AG (Germany)

- SAFILO GROUP S.P.A. (Italy)

- FASTRACK LTD. (India)

- Maui Jim, Inc. (U.S.)

- De Rigo Spa (Italy)

- Shuron (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: SAFILO GROUP S.P.A. and Under Armour renewed their global eyewear licensing agreement till 2031, extending their partnership until 2031. This collaboration aims to deliver lightweight and versatile eyewear solutions, including prescription sunglasses.

- November 2024: EssilorLuxottica, in collaboration with the World Council of Optometry (WCO), announced a virtual event featuring a series of live sessions titled "Presbyopia and Aging Eye to raise awareness and promote prescription glasses.

- April 2024: Carl Zeiss Meditec AG acquired the Dutch Ophthalmic Research Center (D.O.R.C.) with the aim of increasing its product offerings and expanding into the market.

- September 2023: EssilorLuxottica introduced the Ray-Ban Reverse Collection in travel retail locations in Italy and Switzerland through collaborative installations with Dufry.

- May 2023: Carl Zeiss Meditec AG opened its first ZEISS VISION CENTER in Mumbai to revolutionize the way locals experience vision care and eyewear solutions, including prescription sunglasses.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.72% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Frame Style

|

|

By Lens Type

|

|

|

By Application

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.85 billion in 2025 and is projected to reach USD 8.79 billion by 2034.

In 2025, the market value stood at USD 1.99 billion.

The market is expected to exhibit a CAGR of 7.72% during the forecast period.

The rectangle segment leads the market by frame style.

The key factors driving the market are the increasing prevalence of ocular diseases and increasing fashion trends among users.

Carl Zeiss Meditec AG and EssilorLuxottica are the top players in the market.

Europe dominated the prescription sunglasses market with a market share of 26.24% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 155

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us