Primary Cells Market Size, Share & Industry Analysis, By Source (Human and Animal), By Type (Hematopoietic Cells, Hepatocytes, Renal Cells, Gastrointestinal Cells, Lung Cells, Heart Cells, Dermal Cells, Musculoskeletal Cells, and Others), By Application (Basic Cell Biology Research, Safety, Toxicity, & ADME Testing, Regenerative Medicine/Tissue Engineering, and Others), By End User (Pharmaceuticals & Biotechnology Companies, Academic & Research Institutes, CROs & CDMOs, and Others), and Regional Forecast, 2026-2034

Primary Cells Market Size and Future Outlook

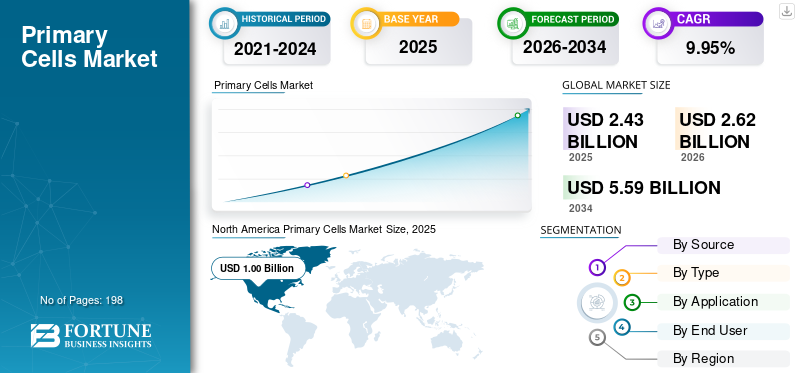

The global primary cells market size was valued at USD 2.43 billion in 2025 and is projected to grow from USD 2.62 billion in 2026 to USD 5.59 billion by 2034, exhibiting a CAGR of 9.95% during the forecast period. North America dominated the primary cells market with a market share of 41.15% in 2025.

Primary cells are obtained straight from living tissues and are commonly employed in research and preclinical settings due to their closer retention of the physiological traits of their original tissue compared to immortalized cell lines. The global market is expanding as pharmaceutical and biotechnology firms, academic and research organizations, and CROs & CDMOs enhance their use of human-relevant in vitro models for drug discovery, disease modeling, immunology, oncology, toxicology, and the development of cell-based assays. The market is also benefiting from ongoing product innovation in cryopreserved primary cells, serum-free and optimized culture media, specialized growth kits, and custom isolation and characterization services that improve workflow efficiency, reproducibility, and application-specific performance across research settings.

Key players operating in the global market include Thermo Fisher Scientific Inc., Merck KGaA, Lonza, PromoCell, and others. These companies are focusing on portfolio expansion, donor sourcing capabilities, custom isolation services, media and supplement optimization, application-specific product development, and strategic collaborations to strengthen their market presence.

Download Free sample to learn more about this report.

PRIMARY CELLS MARKET TRENDS

Shift toward Reduced Animal Testing and New Approach Methodologies is a Major Trend

A significant trend in the market is the increasing movement toward minimizing animal testing and embracing New Approach Methodologies (NAMs). Pharma and biotech firms are progressively utilizing human primary cells, organoids, tissue chips, and sophisticated in vitro assays since these models offer more human-relevant safety and efficacy information compared to conventional animal-only testing. This trend directly enhances the need for human-sourced primary cells such as hepatocytes, renal cells, airway epithelial cells, immune cells, and cardiac cells, utilized in ADME, toxicity assessments, disease modeling, and drug reaction studies. With regulators becoming more receptive to non-animal testing information, companies are expected to boost investment in validated cell-based models as well as primary-cell-specific media, supplements, and assay systems. This is additionally assisting CROs and CDMOs in broadening primary-cell-based testing offerings for pharmaceutical clients. Consequently, the market is shifting from standard research purposes to more valuable translational and regulatory-supportive applications. These factors are supporting the overall global primary cells market growth.

- For instance, in April 2025, the U.S. FDA announced a plan to phase out animal testing requirements for monoclonal antibodies and other drugs by using more human-relevant methods, including AI-based models, cell lines, organoids, and other NAMs. This regulatory shift supports wider adoption of primary-cell-based models in preclinical drug development.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Human-Relevant in Vitro Models to Boost Market Growth

The increasing need for human-relevant in vitro models is a major factor propelling the global market, as drug developers require test systems that better represent actual human biology. Primary cells preserve functions specific to their tissue and biological traits related to the donor, allowing them to be valuable for initial drug discovery, toxicity assessment, disease modeling, and translational studies. This is raising the need for human hepatocytes, renal cells, airway epithelial cells, immune cells, and cardiac cells, particularly among pharmaceutical and biotech firms aiming to enhance the prediction of clinical results. Since traditional animal models and immortalized cell lines frequently do not accurately reflect human responses, companies are moving toward models based on primary cells, organoids, and tissue-chip technologies. This change additionally facilitates increased investment in matched media, growth supplements, donor-specific cells, leukopaks, and personalized isolation services. Consequently, primary cells are transitioning from standard research instruments to essential components in valuable preclinical and translational processes.

- For instance, in December 2025, Pluristyx launched Organoid COMMONS, a public-private consortium with nine other industry leaders to establish global standards for non-animal drug testing models and accelerate the adoption of human-relevant organoid systems. Such initiatives support broader use of human-cell-based in vitro models and strengthen demand for high-quality primary cells.

MARKET RESTRAINTS

High Cost of Primary Cells and Matched Culture Systems to Limit Market Growth

The high cost of primary cells and matched culture systems acts as a restraint, as these products are much more expensive than routine immortalized cell lines and general cell culture media. Researchers often need to buy not only the primary cell vial, but also matched media, supplements, coatings, donor documentation, and sometimes custom isolation or characterization services. This increases the total cost per experiment and limits repeated use, especially among academic labs, small biotech companies, and price-sensitive CROs. High-value products such as pooled human hepatocytes and leukopaks are particularly costly as they require donor sourcing, screening, isolation, cryopreservation, quality control, and cold-chain logistics. As a result, some users may reduce experiment scale, reuse lower-cost cell lines, or shift to alternative models where possible. This slows adoption in emerging regions and restricts primary cell use mainly to well-funded translational, toxicology, and immunology workflows.

- For instance, Thermo Fisher Scientific Inc. has listed Gibco 5-donor human plateable hepatocytes at USD 1,944.65 per vial, while Fisher Scientific listed STEMCELL Technologies fresh human peripheral blood leukopak at USD 4,076.34 per unit. These public supplier prices show why premium primary cells and donor-derived products can create a cost barrier for routine or high-throughput research use.

MARKET OPPORTUNITIES

Growth in Regenerative Medicine & Tissue Engineering Research to Offer Lucrative Market Opportunities

The expansion of regenerative medicine and tissue engineering studies is generating a significant market potential for primary cells, as researchers require biologically relevant cells to construct, assess, and confirm tissue repair models. Primary dermal cells, musculoskeletal cells, endothelial cells, epithelial cells, and immune cells are extensively utilized in studies on wound healing, scaffold evaluation, tissue regeneration, and the creation of engineered tissue models. With the growing focus on restoring damaged skin, cartilage, bone, blood vessels, and organ-like tissues, there is a rising need for superior donor-derived cells, appropriate media, supplements, and tailored isolation services. This chance is particularly significant for pharmaceutical companies, biotechnology firms, academic institutions, and contract research organizations creating sophisticated in vitro models and regenerative systems.

Primary cells assist researchers in assessing cell attachment, growth, tissue response, inflammation, and healing activity under conditions that more accurately mimic human biology. Consequently, regenerative medicine is broadening the application of primary cells beyond fundamental research into more valuable translational and practical tissue-engineering processes. All these factors are expected to drive the market growth in the coming years.

- For instance, in 2025, a review published in npj Biomedical Innovations highlighted that the convergence of materials science, biomedical engineering, and cell biology is advancing wound management and tissue regeneration, with growing demand for biomaterials, growth factors, and cell-based approaches that promote tissue repair. This supports the opportunity for primary cells in scaffold testing, wound healing, and engineered tissue research.

MARKET CHALLENGES

Donor-to-Donor Variability Poses a Prominent Challenge to Market Growth

Variability among donors poses a significant challenge in the market, as cells obtained from various donors may exhibit differing growth rates, gene expression, enzyme activity, immune responses, and functional characteristics. These variations are affected by factors such as donor age, gender, genetics, health condition, disease history, medication background, tissue origin, and collection circumstances. Consequently, researchers frequently must examine various donor lots, confirm each batch, and utilize larger sample sizes to produce consistent results. This raises experiment expenses, prolongs project schedules, and complicates the standardization of primary-cell workflows for drug screening, ADME/toxicity assessments, and translational studies. The challenge is particularly significant for high-value cells such as primary human hepatocytes, PBMCs, endothelial cells, and donor-derived immune cells, as functional performance can differ among lots. As a result, suppliers need to allocate more resources for donor characterization, lot qualification, quality assurance, and uniform cryopreservation methods. All the factors cumulatively affect the market growth.

- For instance, in March 2025, a study published in Stem Cell Reports noted that primary human hepatocytes are a preferred source for liver-function studies, but highlighted donor-to-donor variability as one of the bottlenecks when using primary material.

Segmentation Analysis

By Source

Human Segment Dominated Due to Higher Clinical Relevance and Translational Use

In terms of source, the market is divided into human and animal.

The human segment led the global primary cells market share in 2025. This is due to human-derived primary cells are widely preferred in drug discovery, ADME/toxicity testing, immunology, oncology, respiratory research, and disease modeling. Additionally, rising emphasis on human-relevant in vitro models, reduced dependence on animal testing, and growing use of PBMCs, hepatocytes, airway epithelial cells, renal cells, and donor-specific immune cells are increasing the adoption of human primary cells across pharma, biotech, CRO, and academic research settings.

- For instance, in August 2024, BioIVT acquired ZenBio Inc., expanding its portfolio of skin-based expertise, primary cell and exosome isolation, and blood products for pharmaceutical, diagnostics, and cosmetics

The animal segment is anticipated to rise with a CAGR of 7.50% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Wider Use in Immunology and Cell Therapy Research Led to Hematopoietic Cells Segment Dominance

Based on type, the market is classified into hematopoietic cells, hepatocytes, renal cells, gastrointestinal cells, lung cells, heart cells, dermal cells, musculoskeletal cells, and others.

The hematopoietic cells segment accounted for the dominant market share in 2025. The segment's leadership is due to the wide usage in various applications, and high use of PBMCs, T cells, B cells, monocytes, macrophages, dendritic cells, CD34+ cells, and leukopaks in immune response testing and translational research. Additionally, growing demand for donor-specific immune cells, higher use of leukopaks as cellular starting material, and rising development of cell and gene therapy programs are increasing the adoption of hematopoietic cells. Furthermore, the segment is set to hold 31.3% share in 2026.

- For instance, in May 2025, BioIVT launched VivoSTART Cryopreserved GMP Leukopaks to support improved cell therapy development by providing flexible and regulatory-compliant cellular starting material. Such launches are supporting the growth and dominance of the hematopoietic cells segment.

The lung cells segment is anticipated to rise with a CAGR of 12.17% over the forecast period.

By Application

Wider Use in Routine Biomedical Research Supported Dominance of Basic Cell Biology Research Segment

On the basis of application, the market is divided into basic cell biology research, safety, toxicity, & ADME testing, regenerative medicine/tissue engineering, and others.

In 2025, the market share was primarily led by the basic cell biology research segment. This is due to primary cells are extensively used to study normal cell behavior, tissue-specific functions, cell signaling, immune response, disease mechanisms, and cellular interaction pathways. Additionally, academic institutes, research laboratories, and pharma discovery teams use primary cells across various research applications. Furthermore, the segment is set to hold 36.4% share in 2026.

- For instance, ATCC states that human primary cells are commonly used for preclinical and investigative biological research, including studies of intercellular and intracellular communication, developmental biology, and disease mechanisms in cancer, Parkinson’s disease, and diabetes. Such broad use of primary cells in fundamental biological studies supports the dominance of the segment.

The regenerative medicine/tissue engineering segment is anticipated to rise with a CAGR of 12.25% over the forecast period.

By End User

Pharmaceuticals & Biotechnology Companies Led Demand due to Higher Use in Drug Discovery and Preclinical Testing

Based on end user, the market is segmented into pharmaceuticals & biotechnology companies, academic & research institutes, CROs & CDMOs, and others.

The pharmaceuticals & biotechnology companies segment dominated the market share in 2025. The dominance of the segment is attributed to the fact that these companies are the largest users of primary cells for various applications. Moreover, the growing shift toward biologics, cell therapies, immunotherapies, and advanced in vitro models is further increasing primary cell purchasing across commercial research and development settings. Furthermore, the segment is set to hold 50.2% share in 2026.

- For instance, in February 2025, PHC Corporation and CCRM signed a collaboration agreement to develop primary T-cell expansion culture processes to improve cell and gene therapy manufacturing efficiency and cell quality. Such industry collaborations focused on primary-cell workflows are supporting the dominance of the segment.

CROs & CDMOs are projected to witness a CAGR of 12.69% during the forecast period.

Primary Cells Market Regional Outlook

Based on region, the global market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Primary Cells Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 0.93 billion in 2024 and dominated the global market. In 2025, the region maintained its dominance, with USD 1.00 billion. The regional growth is driven by a strong pharmaceutical and biotechnology R&D base, high use of primary cells in ADME/toxicity testing, and wider adoption of human-relevant in vitro models.

U.S. Primary Cells Market

The U.S. market led the North American region and is projected to be approximately USD 0.96 billion in 2026, representing about 36.6% of global revenues.

Europe

The market in Europe is set to grow at a CAGR of 8.77% during the forecast period. Europe’s growth is supported by strong academic research, biopharma activity, and policy emphasis on alternatives to animal testing.

U.K. Primary Cells Market

The U.K. market in 2026 is estimated at around USD 0.14 billion, representing roughly 5.3% of global revenues.

Germany Primary Cells Market

The German market size is projected to reach approximately USD 0.15 billion in 2026, equivalent to around 5.8% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach USD 0.59 billion in 2026. The region is expected to be the fastest-growing region due to expanding biotechnology R&D, CRO activity, translational research, and pharma outsourcing in China, Japan, India, South Korea, Singapore, and Australia. Moreover, East and Southeast Asia are among the world’s major R&D-performing regions, which also supports the market growth.

Japan Primary Cells Market

The Japan market in 2026 is estimated at around USD 0.13 billion, accounting for roughly 5.1% of global revenues.

China Primary Cells Market

China’s market is projected to reach revenues of around USD 0.21 billion in 2026, representing roughly 8.0% of global sales.

India Primary Cells Market

The Indian market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 2.2% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa markets are anticipated to register moderate growth in the coming years. Prominent factors such as the gradual expansion of biomedical research, hospital-linked translational studies, and increasing investments in healthcare research hubs are anticipated to boost the market growth in these regions. The Latin America market in 2026 is estimated at around USD 0.14 billion.

GCC Primary Cells Market

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.04 billion in 2026, representing about 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Portfolio Expansion and Donor-Specific Cell Solutions to Support Players’ Market Position

The global primary cells market reflects a moderately fragmented market competitiveness, with prominent players such as Thermo Fisher Scientific Inc., Merck KGaA, Lonza, PromoCell, and STEMCELL Technologies accounting for a significant portion of market revenue. The dominance of these companies can be attributed to their broad portfolios across human and animal primary cells, strong geographic presence, and emphasis on strategic initiatives.

- For instance, in February 2025, PHC Corporation and CCRM signed a master collaboration agreement to develop primary T-cell expansion culture processes to improve efficiency and cell quality in cell and gene therapy manufacturing.

Other significant participants include Miaoshun (Shanghai) Biotechnology Co., Ltd., Cell Biologics, Inc., ZenBio, Inc., and ATCC, among others. These firms are also emphasizing donor characterization, cryopreserved cell quality, matched media systems, custom sourcing, and application-specific primary cell workflows to strengthen their competitive position across the forecast period.

LIST OF KEY PRIMARY CELL COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Merck KGaA (Germany)

- Lonza (Switzerland)

- PromoCell (U.S.)

- Miaoshun (Shanghai) Biotechnology Co., Ltd. (China)

- Cell Biologics, Inc. (U.S.)

- STEMCELL Technologies (U.S.)

- ZenBio, Inc. (U.S.)

- ATCC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: MaxCyte launched ExPERT DTx, a high-throughput transfection platform for research and drug discovery applications, enabling transfection of primary cells and cell lines with minimal cellular stress.

- October 2025: Lonza launched TheraPEAK AmpliCell Cytokines and TheraPEAK 293-GT Medium, expanding its GMP solutions for cell and gene therapy workflows.

- September 2025: PromoCell entered the GMP field with custom cell culture media services for cell-based therapy and regenerative medicine applications.

- September 2025: Charles River Laboratories integrated Akadeum’s GMP-grade Human T Cell Leukopak Isolation Kit into its Cell Therapy Flex Program.

- February 2024: iXCells announced the grand opening of its new 30,000 sq. ft. San Diego facility to support demand for disease-relevant cell-based models, including primary cells, iPSC-derived cells, 2D/3D culture models, and organoids.

REPORT COVERAGE

The global primary cells market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of key factors, including technological progress, product innovations, the regulatory environment, and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.95% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Source, Type, Application, End User, and Region |

| By Source |

|

| By Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.43 billion in 2025 and is projected to reach USD 5.59 billion by 2034.

In 2025, the market value in North America stood at USD 1.00 billion.

The market is expected to exhibit a CAGR of 9.95% during the forecast period of 2026-2034.

By source, the human segment led the market in 2025.

Rising demand for human-relevant in vitro models, growth in safety, toxicity, and ADME testing, and expansion of immunology, oncology, and cell therapy research are primarily driving market expansion.

Thermo Fisher Scientific Inc., Merck KGaA, Lonza, and PromoCell are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us