Pultrusion Market Size, Share & Industry Analysis, By Type (Glass Fiber, Carbon Fiber, and Others), By Application (Industrial, Housing, Consumers, and Others), and Regional Forecast, 2026-2034

Pultrusion Market Size and Future Outlook

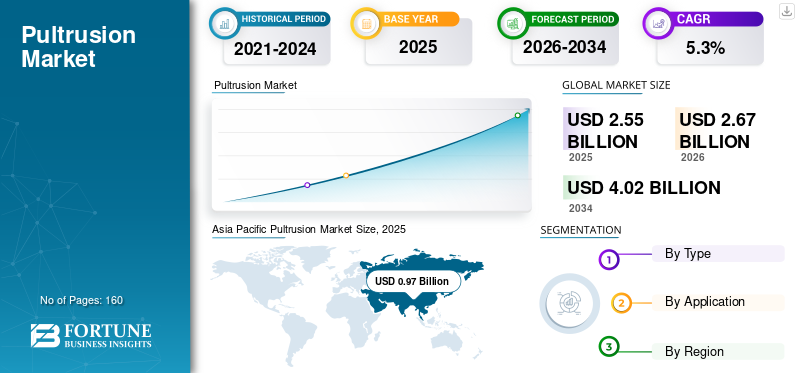

The global pultrusion market size was valued at USD 2.55 billion in 2025. The market is projected to grow from USD 2.67 billion in 2026 to USD 4.02 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. Asia Pacific dominated the global pultrusion market with a market share of 38.04% in 2025.

Pultrusion is a continuous, automated manufacturing process used to produce fiber-reinforced polymer (FRP) profiles with a constant cross-section by pulling reinforcement through a heated die filled with resin. Pultruded profiles are widely used where designers require corrosion resistance, electrical insulation, or transparency to electromagnetic waves, high specific strength, dimensional consistency, and low maintenance over extended service lives.

Market growth is driven by increasing demand for lightweight materials and a substantial increase in demand for durable products for harsh environments. Additionally, technological advancements are expected to increase efficiency and production, thereby boosting market growth.

Furthermore, the market comprises several major players, including BASF, Creative Composites Group, Strongwell, Exel Composites, and Reliance Industries Ltd. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

PULTRUSION MARKET TRENDS

Standardization, Infrastructure Codes, and Grid Modernization are Significant Market Trends

Pultruded profiles are moving from specialty composite use cases into more mainstream infrastructure specifications as standards and design guidance mature. In Europe, EN 13706 provides specifications for pultruded profiles, while newer design guidance for fiber-polymer composite structures (CEN/TS 19101) support broader engineering adoption in buildings, bridges, and civil works. At the same time, power-grid upgrades and higher conductor performance targets are accelerating demand for pultruded composite conductor cores and structural elements that combine strength, low sag, and corrosion resistance. Alongside this, producers are emphasizing recyclability pathways and lower-carbon resin systems to meet customer and regulatory expectations on materials circularity and embodied carbon.

- For instance, industrial-scale adoption of composite conductor cores is being supported by multi-year supply agreements and localized manufacturing footprints, reflecting transmission and distribution investment cycles.

MARKET DYNAMICS

MARKET DRIVERS

Infrastructure Durability Needs and Grid Modernization are Accelerating Adoption of Pultruded Composites

Pultruded FRP is increasingly selected where long service life and reduced maintenance offset higher upfront material costs. In the construction and civil infrastructure sectors, corrosion-driven lifecycle costs are prompting designers to adopt GFRP rebar, FRP bridge components, and structural profiles in aggressive environments. In parallel, electric utilities are specifying pultruded crossarms, poles, and hardware components to enhance reliability, reduce installation weight, and provide electrical insulation where required. Ongoing standardization (e.g., structural profile specifications and GFRP reinforcement codes) reduces technical risk for asset owners and supports broader adoption of procurement.

- For instance, ACMA conference materials on pultruded fiberglass rebar highlight increasing adoption tied to ASTM D7957 qualification and expanding DOT use cases for bridge and highway structures.

MARKET RESTRAINTS

Design-Code Familiarity Gaps and Feedstock Cost Volatility Can Restrict Market Expansion

Despite strong performance advantages, adoption can be slowed by conservative specification practices, limited familiarity among civil engineers, and qualification requirements that add time and cost for new profiles. Pultrusion economics are also sensitive to glass and carbon fiber pricing and resin costs, while tooling (dies) and product-specific testing requirements create upfront investment barriers for smaller programs. Additionally, recycling complexity remains a structural restraint for thermoset-based pultruded products, contributing to scrutiny in regions with tightening waste and landfill policies. This is expected to hinder the pultrusion market growth in the coming years.

MARKET OPPORTUNITIES

Low-Carbon Infrastructure Programs and Circularity Solutions to Create Lucrative Growth Opportunities

Public infrastructure investment and decarbonization strategies can favor pultruded composites when lifecycle emissions and maintenance impacts are evaluated. Opportunities are expanding in corrosion-prone structures (such as those exposed to coastal and de-icing salts), renewable energy (including wind-blade carbon pultrusion), and transportation, where lightweighting can improve energy efficiency. In terms of sustainability, emerging circularity routes, such as co-processing in cement clinker production and mechanical size reduction for reuse, are being scaled up as practical pathways for end-of-life composites.

- For example, EPTA highlights co-processing and mechanical size reduction as practical circularity routes currently being developed and tested by the industry.

MARKET CHALLENGES

Competition from Metals and Thermoplastic Extrusions, Plus Fire-Performance Requirements, to Hamper Market Growth

Aluminum, steel, and thermoplastic extrusions remain strong substitutes in applications where commodity pricing, established standards, and well-understood failure modes dominate procurement decisions. In building and transportation interiors, fire, smoke, and toxicity requirements can necessitate higher-cost resin systems and qualification work, raising barriers in price-sensitive tenders. Finally, the need to deliver consistent dimensional tolerances, surface finish, and long-term durability across different climates increases the importance of process control and robust QA/QC.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Glass Fiber Segment Led Market as It Offers a Strong Cost-to-Performance Balance

Based on type, the market is segmented into glass fiber, carbon fiber, and others.

The glass fiber segment accounted for the largest pultrusion market share in 2025. The segment is growing as it offers a strong cost-to-performance balance for structural profiles used on a large scale. Demand is lifted by corrosion-resistant requirements in utilities, chemicals, water infrastructure, and coastal environments where steel protection is costly. The higher adoption of non-conductive components supports their use in electrical enclosures, ladder rails, and cable management. Furthermore, the segment held 88.6% share in 2025.

The carbon fiber segment is projected to grow at a CAGR of 5.1% during the study period. The segment growth is driven by the need for lightweighting and increased stiffness in transportation, renewable energy, and high-performance industrial equipment. Manufacturers adopt carbon pultruded parts where deflection control, dimensional stability, and fatigue life are critical, such as robotic arms, booms, rollers, and structural reinforcements.

By Application

To know how our report can help streamline your business, Speak to Analyst

Industrial Segment Dominated Market Due to Extensive Use of the Product

In terms of application, the market is categorized into industrial, housing, consumers, and others.

The industrial segment accounted for a 42.8% share in 2025. Demand rises as steel and aluminum are replaced in corrosive or electrically sensitive environments. Process plants, wastewater treatment facilities, marine structures, and utilities are adopting FRP gratings, handrails, walkways, cable trays, and ladder systems to reduce maintenance, minimize downtime, and enhance safety. Higher investment in grid modernization, renewable energy assets, and industrial automation increases the need for lightweight, modular structural components.

The housing segment is also expected to grow favorably over the projected period. The segment's growth is driven by durable, low-maintenance building components that resist moisture, rot, and corrosion. Pultruded profiles are used in window/door reinforcement, framing elements, railing systems, decking substructures, and architectural trims where dimensional stability supports tighter tolerances. The segment is expected to grow at a CAGR of 4.7% over the forecast period.

The consumer segment is expected to experience favorable growth throughout the forecast period, driven by demand for durable products with low maintenance requirements and the ability to integrate colors, surface finishes, and UV-stable resins. As design teams prioritize repeatable performance and scalable manufacturing, pultruded composites become attractive for mid-volume consumer categories.

Pultrusion Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Pultrusion Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 0.97 billion, and is expected to maintain its leading share in 2026, valued at USD 1.02 billion. The market’s growth is supported by expanding wind supply chains, infrastructure build-out in coastal and industrial zones, and the scale-up of regional composite manufacturing capacity. China remains the largest consumption base for FRP products, while India and Southeast Asia are gaining momentum in wind and electric utility upgrades. Large-volume production programs favour pultrusion as it delivers repeatable quality at high output rates.

China Pultrusion Market

In 2025, the Chinese market was valued at USD 0.49 billion. China’s market demand is driven by wind energy components, cable management systems, industrial platforms, and corrosion-resistant infrastructure in coastal and chemical-industry environments. The market also benefits from a large domestic supply base for glass fiber and thermoset resins, which enables the production of cost-competitive pultruded profiles for the construction and utilities sectors.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, estimated to reach USD 0.57 billion by 2026, driven by strong penetration in electric utility crossarms and structural shapes, as well as the growing adoption of GFRP reinforcement in corrosion-prone infrastructure. The region benefits from established producers with large machine fleets and in-house design support. For example, Strongwell reports more than 65 pultrusion machines across four North American facilities, indicating substantial installed capacity to serve utility and infrastructure demand.

U.S. Pultrusion Market

In 2025, the U.S. market was valued at USD 0.46 billion. In the U.S., grid reliability programs and replacement of aging utility structures are supporting demand for pultruded crossarms and poles. Infrastructure applications are increasingly supported by formal codes for GFRP reinforcement, reducing adoption friction for state DOTs and bridge owners.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at 5.3% and reach a valuation of USD 0.64 billion in 2026. The region's growth is driven by a well-established structural profile ecosystem and increasing attention to standardization (EN 13706) and Eurocode-aligned composite design methods.

U.K. Pultrusion Market

The U.K. market in 2025 was valued at USD 0.08 billion, representing approximately 4.5% of the global market revenue.

Germany Pultrusion Market

Germany’s market was valued at USD 0.14 billion in 2025, equivalent to around 5.7% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 0.20 billion. The region is growing from a smaller base, with opportunities in electric utility structures, corrosion-resistant industrial walkways, and selective infrastructure upgrades. Adoption is often project-driven, with procurement influenced by import availability and local fabrication capability.

Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by project-based demand in industrial facilities, desalination, and water infrastructure, as well as coastal construction, where corrosion resistance is highly valued. Limited local pultrusion capacity in several countries can lead to increased dependence on imported profiles and systems.

GCC Pultrusion Market

The GCC market was valued at USD 0.11 billion in 2025, accounting for approximately 4.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Adopting Business Expansion Strategies to Maintain Their Market Positions

The market includes a mix of dedicated manufacturers, vertically integrated composite groups, and wind-focused carbon pultrusion specialists. Competition is shaped by tooling and design capability, QA/QC maturity, customer qualification track record, and the ability to supply large, consistent volumes. Some of the key market players include BASF, Creative Composites Group, Strongwell, Exel Composites, and Reliance Industries Ltd. Companies are focusing on capacity investments near large end-use hubs (notably wind), resin system upgrades for fire and weather performance, and deeper co-development with OEMs to lock in long-duration supply agreements.

LIST OF KEY PULTRUSION COMPANIES PROFILED

- Creative Composites Group (U.S.)

- Strongwell (U.S.)

- Exel Composites (Finland)

- Fiberline Composites (Denmark)

- Bedford Reinforced Plastics (U.S.)

- Pultron Composites (New Zealand)

- Gurit (Switzerland)

- BASF (Germany)

- Reliance Industries Ltd. (India)

- EPP Composites Pvt. Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Exel Composites received a purchase order for carbon planks for wind turbine spar caps from a major wind turbine manufacturer, signaling conversion of wind-customer engagement into repeatable pultrusion supply for large-scale blade structures.

- December 2024: Exel Composites’ JV (KECI) confirmed its new manufacturing site in India is operational (completed on time; lines commissioned), building dedicated pultrusion capacity optimized for wind power components with deliveries planned from early 2025.

- May 2024: Fiberline Building Profiles and KRAFTON announced a strategic merger, aimed at expanding the offering of pultruded structural profiles and planks and improving delivery performance across Europe—supportive for construction-sector penetration.

- July 2023: Exel Composites provided a wind-program progress update and announced factory expansion in India, indicating active scale-up of carbon and glass pultrusion qualification/testing for wind customers and a push to localize high-volume production.

- December 2022: Exel Composites signed a multi-year agreement to supply pultrusion products to a wind power industry customer, reinforcing wind energy as a major demand engine for pultruded composites and supporting longer-term capacity planning.

- June 2022: Owens Corning and Pultron formed a JV to manufacture fiberglass rebar, aiming to expand capacity and accelerate global adoption of pultrusion-based rebar as a corrosion-resistant alternative to steel in concrete reinforcement.

- October 2021: Exel Composites and Kineco Group announced a joint venture in India to expand the Indian market, strengthening their local manufacturing presence and targeting demand in wind power, transportation, and telecom sectors with pultruded composite solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.3% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Type, Application, and Region |

|

By Type |

· Glass Fiber · Carbon Fiber · Others |

|

By Application |

· Industrial · Housing · Consumers · Others |

|

By Geography |

· North America (By Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Type, Application, and Country/Sub-region) o Germany (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) · Asia Pacific (By Type, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Type, Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Type, Application, and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.55 billion in 2025 and is projected to reach USD 4.02 billion by 2034.

Recording a CAGR of 5.3%, the market is slated to exhibit steady growth during the forecast period.

The industrial application segment led in 2025.

Asia Pacific held the highest market share in 2025.

BASF, Creative Composites Group, Strongwell, Exel Composites, and Reliance Industries Ltd. are some of the prominent players in the market.

The need for infrastructure durability and grid modernization is accelerating the adoption of pultruded composites.

The major factors expected to favor product adoption in the market are a strong strength-to-weight ratio and corrosion and chemical resistance.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us