Pumped Hydro Storage (PHS) Market Size, Share & Industry Analysis, By Type (Open Loop and Closed Loop), By Capacity (Below 500 MW, 500-1000 MW, and Above 1000 MW), and Regional Forecast, 2026-2034

Pumped Hydro Storage (PHS) Market Size and Future Outlook

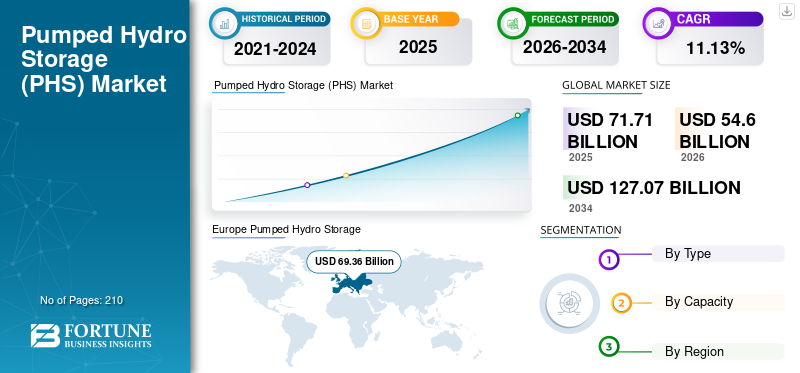

The global Pumped Hydro Storage (PHS) market size was valued at USD 71.71 billion in 2025 and is projected to grow from USD 54.6 billion in 2026 to USD 127.07 billion by 2034, recording a CAGR of 11.13% during the forecast period.

A Pumped Hydro Storage (PHS) or Pumped Storage Hydropower (PSH) plant pumps water to an upper reservoir when power and electricity prices are low and releases the water back to the lower reservoir through a turbine when loads are high and electricity prices are higher. PHS is a flexible form of energy storage technology that contributes to balancing the supply and demand in the grid system and helps integrate a wide range of renewable energy sources, such as wind and solar.

The impact of the COVID-19 pandemic on the market was moderate as it hampered all the industries related to power generation and distribution. The pandemic-induced labor and raw material shortages delayed construction timelines, leading to project delays and cost overruns. The economic downturn impacted investments in pumped hydro storage projects, and the shift in demand dynamics affected the business of these projects, potentially leading to a reevaluation of the project’s viability. Thus, COVID-19 negatively impacted the global PHS market.

Download Free sample to learn more about this report.

PUMPED HYDRO STORAGE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 71.71 billion

- 2026 Market Size: USD 54.6 billion

- 2034 Forecast Market Size: USD 127.07 billion

- CAGR: 11.13% from 2026–2034

- The open-loop segment is expected to acquire 85.88% of the market share in 2026.

- Closed loop PHS plants segment is projected to display a CAGR of 16.07% during the forecast period.

- The above 1000 MW PHS plant is the leading segment in the market by capacity owing to massive energy storage capacity requirements for mega energy projects globally.

North America

The North America market generated USD 71.71 billion in 2025, and is expected to reach USD 54.6 billion in 2026.

Europe

Europe contributed the global market with a valuation of USD 69.36 billion, and is projected to reach USD 70.78 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 116.66 billion in 2025, and is projected to reach USD 128.14 billion in 2026.

U.S.

The U.S. market is estimated to be USD 11.93 billion in 2025.

Japan

Japan is projected to hit USD 6.60 billion in 2025.

Read More

Pumped Hydro Storage (PHS) Market Trends

Modernization of Existing PHS Plants to Improve Efficiency is Current Market Trend

Current trends in the global market include modernizing the hydraulic infrastructures, tapping the hidden hydroelectric energy storage potential in existing facilities, increasing the flexibility and resilience to climate change, and implementing digital & mitigation measures. Pumped hydro storage is being utilized to complement the operation of existing reservoirs and lakes to enhance water management. Novel methods are under investigation to integrate other energy technologies into hydropower plants, such as hydrogen generation, floating photovoltaics on hydropower reservoirs, hybridization with batteries, and waste-heat recovery. Ocean (tidal and wave) power plants use turbines adapted from the hydropower sector.

Moreover, new developments are helping optimize pumped storage hydropower processes, while investments and environmental permits are helping get new projects off the ground. In February 2023, Hitachi Energy completed the world's first static frequency converter solution to use modular multi-level technology in a pumped hydro storage application. This newly developed technology was handed over to Austrian power generator Verbund, which enables the 45-year-old PHS plant to switch its two pump-turbine units from traditional fixed-speed to variable-speed operation. These pump turbines adjust their speed automatically as per grid conditions and reservoir water levels, which improves the efficiency of the PHS process and helps balance the Austrian power grid.

Download Free sample to learn more about this report.

Pumped Hydro Storage (PHS) Market Growth Factors

Increasing Requirement for Grid Stability and Resilience in Intermittent Power Supply Systems

Requirements for new phases in the power sector have increased to maintain a balance in power generation and consumption within an electrical grid. For a power grid system to remain stable, it must respond to volatility in voltage and frequency disturbances with increasing power demand globally. The International Energy Agency (IEA) projected that the global electricity demand will increase by 60 % by the end of 2040, with developing countries accounting for a significant share. Asia Pacific is projected to consume 46% of the global energy. In developed countries, the demand is projected to increase by about 30% by 2040 due to the rising use of digital and data technologies by various businesses. Electricity generation markets are particularly vulnerable to the demand brought in by technological innovations, such as growing digitization of the economy and rise of Electric Vehicles (EVs).

Grid operators and governments continue to seek alternatives to balance a variable supply with fluctuating demands. New concepts and developments from grid operators are vital to ensuring a consistent and steady balance of electricity sources and supply. Pumped hydro storage is a flexible resource that helps balance demand and supply in the power grid and integrates different renewable energy sources, such as wind and solar power systems. Due to their high level of operational flexibility, PHS units provide many of these ancillary services to support grid operations.

Energy Transition Policies Paired With Technological Advancements for PHS

In a significant move to accelerate the global renewable energy capacity, governments across nations have introduced several initiatives to expedite pumped hydro storage project commissioning. Several vital measures have been implemented through collaborative efforts. For instance, in December 2022, the European Commission approved state aid worth USD 27.5 million for the development of a 75MW/530MWh Pumped Hydro Energy Storage (PHES) in Finland. It is the latest energy storage system aid from the EU for a PHS plant.

The government of China has a longstanding commitment to expanding the nation's hydropower capacity. The 13th five-year plan had a target of 380 GW of hydropower capacity by the end of 2020 and 470 GW of hydropower capacity by 2025, which includes PHS. In Asia Pacific, pumped hydropower is witnessing rapid expansion owing to the potential of this technology to meet peak loads and improve the integration of solar and wind power into electric grids. In 2021, the National Energy Administration (NEA) issued a Medium & Long-term Development Plan for pumped hydro storage till 2035 to double its pumped hydro storage capacity to 62 GW by 2025 and reach 120 GW by 2030. Moreover, in 2024, the U.S. Department of Energy's (DOE) Water Power Technologies Office (WPTO) started technical assistance for hydropower developers, system operators, utilities, and other stakeholders for the development of hydropower hybrids and PHS. This technical assistance by DOE's national laboratories is aimed at supporting stakeholders' decisions regarding potential projects.

In terms of technological advancements and scientific publications, Europe comes second in hydropower knowledge production after China. The EU and the U.S. each host about 28% of the world’s most innovative hydropower companies. The EU held 33% of all high-value inventions globally till 2020, with Germany, France, and Poland being the main contributors. Although China is the primary patent leader, the EU, Japan, and South Korea are performing similarly and slightly better than the U.S. These research studies and government support are prompting key players to invest in PHS, which is driving the Pumped Hydro Storage (PHS) market share.

RESTRAINING FACTORS

High Installation Cost and Limited Land Availability for Reservoir is Hampering Market

The development of pumped hydro storage is a challenging and complex process, which is tailored specifically for each project. Maintaining a PHS facility is relatively cost-effective for the long term, whereas pumped storage projects have high installation costs. Similar to other sizable low-carbon infrastructure, much of the lifetime cost of PHS is incurred during construction with high upfront capital. Owing to this, investors are unwilling to invest even if the technology is highly cost-effective and sustainable. Governments developed earlier PHS plants, businesses, or vertically integrated utilities for long-term returns and energy generation. But now, it is difficult for investors to consider what sources of revenue will be available over the long lifetime of PHS assets. Very few organizations or private investors agree to finance such long-term projects due to licensing timeframe uncertainties or long payback periods.

Moreover, suitable land that is large enough and has the right topography for the reservoir, the facility, and all the other requirements can present a challenge in meeting large-scale electricity demand. In the present context, the extensive submergence, together with the land acquisition, has become a significant constraint for constructing land-intensive projects. All PHS projects essentially require two reservoirs, the upper reservoir and the lower reservoir, and this fact entails that various innovative combinations are also considered for installing a pumped storage project. Specific to PHS, though, it becomes difficult to forecast revenues derived from energy arbitrage accurately, and a lot of the ancillary services provided are still not adequately reimbursed, if at all, in many markets. This can restrict the ability of developers to secure additional revenue streams. These factors are expected to hamper the Pumped Hydro Storage (PHS) market growth over the forecast period.

Pumped Hydro Storage (PHS) Market Segmentation Analysis

By Type Analysis

Open Loop Dominates Market Owing to Low Cost and Easy Installation Process

Based on type, the global market is segmented into open loop and closed loop.

The open-loop segment accounts for a major share of the market as significant projects in both developed and developing countries are open-loop. The segment is expected to acquire 85.88% of the market share in 2026. Moreover, these projects incur low costs and offer an easy installation process. Open loop PHS projects have either an upper or lower reservoir, which is continuously connected to a naturally flowing water feature. In such cases, electricity can be generated without the requirement for pumping, as seen in a storage hydropower facility without the pumping feature. Current open-loop systems can also go beyond 100 GWh in energy storage, such as the Vilarinho das Furnas project in Portugal. The 3,600 MW Fengning pumped storage project under construction in China will be the largest in the world once completed in 2025.

Closed loop PHS plants have reservoirs that are not connected all the time to a naturally flowing water feature, such as a river or lake. The segment is projected to display a CAGR of 16.07% during the forecast period. Closed-loop plants allow more siting flexibility, and an essential advantage of closed-loop PHS is that its environmental impact is generally lower. The number of these plants is projected to rise over the forecast period as numerous closed-loop pumped hydro plants are under planning and development. The closed-loop system will be benefited by using the electricity generated by the nearby solar project to pump water uphill during the day before dispatching firm and flexible energy at periods of peak demand.

By Capacity Analysis

Above 1,000 MW Capacity Dominates Market Owing to Higher Energy Storage Capabilities

Based on capacity, the global market is segmented into below 500 MW, 500-1000 MW, and above 1000 MW.

The above 1000 MW PHS plant is the leading segment in the market by capacity owing to massive energy storage capacity requirements for mega energy projects globally. Pumped hydro storage plants with capacities above 1,000 MW offer higher energy storage capabilities and enable them to play a vital role in providing grid stability and meeting peak demand requirements. These plants are well-suited for providing essential grid balancing services and integration of intermittent renewable energy sources, such as solar and wind into the grid system. While the upfront capital costs of large-scale PHS projects are significant, they can often achieve economies of scale, resulting in lower costs per unit of stored energy compared to smaller installations. This can make them more cost-effective in the long run, especially for meeting the energy storage needs of significant utility-scale projects. The above 1000 segment is anticipated to hold a dominant market share of 46.60% in 2026.

The below 500 MW capacity segment holds the second-highest share of the market owing to site availability and the economic feasibility of installing and maintaining a PHS plant. The segment held 44.27% of the market share in 2024. Building large-scale pumped hydro storage plants requires considerable investment and suitable geographic conditions. Projects below 500 MW are often more economically viable to develop compared to larger installations. Identifying suitable sites for PHS plants involves specific geographic requirements, such as access to water sources, elevation differences, and land availability. Sites that meet these criteria and can accommodate larger capacities are limited.

The 500-1000 MW segment offers larger energy storage capacity compared to smaller installations. Increasing energy demand across the world is driving the growth of this segment. The increased capacity of plants allows the storage and release of greater amounts of energy, providing more significant grid stability and reliability. Moreover, plants with this capacity range can provide essential grid support services, such as frequency regulation, voltage control, and black start capabilities. These eventually play a crucial role in balancing supply and demand fluctuations, especially in large-scale power systems.

To know how our report can help streamline your business, Speak to Analyst

REGIONAL INSIGHTS

The Pumped Hydro Storage (PHS) market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe Pumped Hydro Storage (PHS) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North American

The North America market generated USD 71.71 billion in 2025, and is expected to reach USD 54.6 billion in 2026. North American countries are significant markets for PHS, particularly the U.S. The region has several existing pumped hydro facilities and is investing in new projects to enhance grid stability and support renewable energy integration. The region is expected to be the third-largest market with a value of USD 12.06 billion in 2025. The U.S. market is estimated to be USD 11.93 billion in 2025.

Europe

Europe contributed the global market with a valuation of USD 69.36 billion, and is projected to reach USD 70.78 billion in 2026. Europe has a long history of pumped hydro storage, with Norway, Switzerland, and Austria establishing mega projects with substantial capacities. Moreover, many countries in the region are investing in upgrading the existing facilities and building new ones to support the transition to renewable energy sources. The regional market value increased from USD 69.36 billion in 2025 and is projected to reach USD 70.78 billion in 2026, continuing to lead the region.Asia Pacific, led by China, Japan, and Australia, is experiencing rapid growth in the market.

Asia Pacific

Asia Pacific accounted for USD 116.66 billion in 2025, and is projected to reach USD 128.14 billion in 2026. China, in particular, has been investing significantly in pumped hydro projects as part of its renewable energy expansion plans. Some of the most significant PHS projects in the world are focused in China for the coming year. The market size for China is likely to be USD 14.01 billion in 2025. Meanwhile, India is expected to be USD 1.95 billion and Japan is projected to hit USD 6.60 billion in 2025.

Latin America

Latin America contributed approximately USD 41.11 billion to the global market in 2025, and is expected to reach USD 43.5 billion in 2026. In Latin America, Brazil and Chile are also exploring pumped hydro storage to integrate renewable energy into their grids and enhance energy security. The Latin America region is anticipated to be USD 2.60 billion in 2025, as the fourth-largest market.

Middle East & Africa

In 2025, Middle East & Africa reaching a valuation of USD 5.48 billion, and is projected to grow to USD 5.58 billion in 2026. In the Middle East & Africa, the PHS market is relatively smaller as compared to others, and there is growing interest in leveraging pumped hydro technology to support renewable energy deployment and address power access challenges. South Africa is likely to be USD 0.64 billion in 2025.

KEY INDUSTRY PLAYERS

Competitive Landscape is Dominated by Large Scale Companies and Infrastructure Players

The global pumped hydro storage market’s competitive landscape is highly fragmented, with large and some medium-scale regional players delivering a wide range of products at local and country levels across the value chain. Companies are focusing on increasing R&D for innovations in PHS to improve the efficiency of plants and meet the future requirements of growing energy demands.

List of Top Pumped Hydro Storage (PHS) Companies:

- ANDRITZ AG (Austria)

- Siemens AG (Germany)

- Enel SpA (Italy)

- Duke Energy Co. (U.S.)

- Voith GmbH & Co. KGaA (Germany)

- GE Vernova (U.S.)

- Power Construction Corporation of China (China)

- Torrent Power (India)

- ITC Holdings (U.S.)

- NextEra Energy, Inc. (U.S.)

- China Energy Engineering Corporation (China)

KEY INDUSTRY DEVELOPMENTS:

- April 2024: ANDRITZ announced plans to upgrade the Cruachan pumped storage power plant in Scotland. The company will supply two new generating units comprising pump turbines and motor generators, along with essential main inlet valves. The objective of this modernization project is to increase the power output by 40 MW and bring it to a total of 480 MW. In 2026, the global pumped hydro storage industry witnessed rising adoption of closed-loop and off-river pumped storage systems due to their lower environmental impact, higher flexibility, and improved efficiency for renewable energy balancing.

- April 2023: Ignitis Gamyba hired Voith Hydro to expand the Kruonis pumped storage plant in Lithuania. The agreement signed was worth USD 162 million for the installation of the highly flexible pump-turbine unit with an output of 110 MW.

- September 2022: Greenko MP01 IREP Private Limited brought ANDRITZ onboard for electromechanical works at the 1,440 MW-Gandhi Sagar pumped storage project in Madhya Pradesh, India. The agreement included the design, manufacture, supply, testing, and commissioning of seven reversible pump units (five 240-MW units and two 120-MW units), main inlet valves, and associated auxiliaries. China continued expanding its leadership in pumped hydro storage capacity, led by mega projects such as the Fengning Pumped Storage Power Station, which supports large-scale wind and solar power integration.

- May 2022: Voith Hydro installed the world's first 600 r/min pumped storage unit for commercial operation at China's Changlongshan station. Six units were installed at the 2.1 GW station, with the rated speed of units 1 through 4 being 500 r/min.

- July 2021: Voith Hydro completed the modernization work on the Drakensberg power station, which is the second-largest pumped storage facility in South Africa. The company received an order for the design, installation, and commissioning of old generators at the Drakensberg pumped storage power plant.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on crucial aspects, such as major key players, product types, and leading applications of the product. Besides, it offers insights into the market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.13% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (GW) |

|

Segmentation |

By Type

|

|

By Capacity

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 71.71 billion in 2025.

The market is likely to record a CAGR of 13.06% over the forecast period of 2026-2034.

By type, the open loop segment is expected to lead the market.

The market size of Europe was valued at USD 27.00 billion in 2025.

Increasing requirement for grid stability and energy transition policies along with technological advancements are the key factors driving the market growth.

Some of the top players in the market are ANDRITZ AG, Siemens AG, Enel SpA, Duke Energy Co., and Voith GmbH & Co. KGaA.

The global market size is expected to reach a valuation of USD 127.07 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us