Quantum Communication Market Size, Share & Industry Analysis, By Architecture (Space-to-Ground QKD, Inter-Satellite QKD/Entanglement, Airborne Relay QKD, Fiber Metro/Long-Haul QKD, Maritime Free-Space QKD), By Product (Terminals (Space/Air/Sea/Ground), Photonic Components, PAT & Control, Security Stack, Test & Assurance), By Service (Secure Link-as-a-Service, Sovereign Ground/Key Services, Integration & MRO, Validation & Accreditation, Training & Ops Support), By End User (Defense Ministries & Armed Forces, Space Agencies & Sat Operators, & Others) and Regional Forecast, 2026-2034

Quantum Communication Market Size and Future Outlook

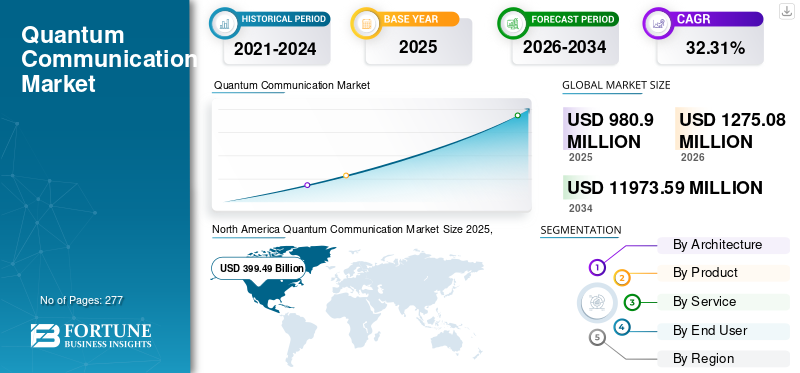

The global quantum communication market size was valued at USD 980.90 million in 2025. The market is projected to grow from USD 1275.08 million in 2026 to USD 11973.59 million by 2034, exhibiting a CAGR of 32.31% during the forecast period. North America dominated the quantum communication market with a market share of 40.72% in 2025.

Quantum communication for aerospace and defense secures networks by distributing encryption keys with quantum states, mainly quantum key distribution (QKD), so any interception is detectable and keys can be refreshed automatically. The market includes space and ground optical terminals, optical ground stations, photon sources and detectors, pointing, acquisition, tracking units, rugged airborne, shipboard pods, quantum random number generators, and crypto-agile key management (KMS/HSM) with orchestration software. It is widely used for sovereign command-and-control, ISR backhaul, embassy and defense cloud connections, coalition gateways, and hardened links across satellites, aircraft, ships, and others.

Key players include Toshiba, ID Quantique (QKD systems, QRNG/HSM), QuantumCTek (national backbones), SES and Thales Alenia Space (EAGLE-1, SAGA missions), Airbus and Honeywell (payloads/terminals), TESAT (space optical terminals), Raytheon and Thales (integration, accreditation). These players are creating secure quantum key distribution (QKD) systems for various industry verticals.

Download Free sample to learn more about this report.

Quantum Communication Market Key Takeaways

- 2025 Market Size: USD 980.90 million

- 2026 Market Size: USD 1,275.08 million

- 2034 Forecast Market Size: USD 11,973.59 million

- CAGR: 32.31% from 2026–2034

- North America dominated the quantum communication market with a 40.72% share in 2025.

- The Fiber Metro/Long-Haul QKD segment accounted for the largest market share in 2025.

- The Security Stack segment accounted for the largest market share in 2025.

North America

North America held a 40.72% share in 2025, valued at USD 399.49 million.

Asia Pacific

Asia Pacific is projected to be the fastest-growing regional market, expanding at a CAGR of 33.25% during the forecast period.

Europe

Europe is projected to reach USD 233.13 million by 2026, supported by strong investments in quantum-secure communications and sovereign cybersecurity initiatives.

U.S.

The market projected to reach USD 213.56 million by 2026.

Japan

The market projected to reach USD 61.48 million by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Sovereign Secure Communications Demand is Anticipated to Drive Market Growth

Defense programs are moving from demonstrations to structured deployments to ensure confidentiality, integrity, and provenance of mission traffic under classical and post-quantum threat models. Procurement priorities include sovereign custody of cryptographic material, crypto-agile key management aligned with PQC standards, and assured interoperability across coalition environments. Funding is directed to national backbones, space-to-ground links, and mission gateways, with defined service levels and audit requirements. This translates into sustained demand for quantum key establishment systems, high-reliability detectors, pointing and tracking assemblies, certified random number generation, and integration with accredited KMS/HSM infrastructures, all of which are supported under formal accreditation pathways.

MARKET RESTRAINTS

Export controls and sovereignty clauses are anticipated to restrain market growth.

Cross-border deliveries face licensing, content origin rules, and sovereign key custody requirements. These policies fragment designs by country, slow approvals, and force vendors to maintain separate product baselines. Components, including detectors, cryo modules, and precision optical components, may require special permits or local finishing, extending lead times and increasing costs. Association projects also struggle to align accreditation and data-handling policies, which delays multinational trials. The impact is fewer common parts, more documentation, and cautious scheduling.

MARKET OPPORTUNITIES

Coalition Interoperability and Defense Cloud Hardening are Anticipated to Create Opportunity

Coalition operations require assured exchange of cryptographic material under heterogeneous sovereignty and accreditation policies. This drives demand for interoperable gateway nodes, policy-aware key orchestration, and audited interfaces that integrate with national key infrastructures. In addition, defense cloud environments are adopting quantum-safe key pipelines, certified random sources at the edge, and compliance-ready services. Vendors offering validated interoperability, clear certification pathways, and structured lifecycle support are positioned to secure framework contracts and recurring operations revenue.

QUANTUM COMMUNICATION MARKET TRENDS

Increasing Hybrid Architectures and Miniaturization Lead to New Market Trends

Two key developments propelling the practical advancement and commercialization of quantum communication are hybrid architectures and downsizing. By addressing important issues such as scalability, deployment, and integration with current infrastructure, these trends help bring quantum technology beyond the lab to practical uses. Solutions that easily integrate with existing classical networks are becoming increasingly popular in the industry. This entails combining edge, cloud, and on-premises systems to take advantage of each platform's advantages. Moreover, bulky experimental setups are being replaced by chip-scale platforms.

MARKET CHALLENGES

Integration, Scaling, and Supply Are Anticipated to Challenge the Market Growth

Mission deployment depends on reliable integration with existing key management infrastructures, zero-trust architectures, and network operations workflows. Achieving multi-vendor interoperability beyond laboratory conditions requires common control planes, standardized telemetry, and validated procedures. Scaling introduces practical constraints, qualified ground sites, trained personnel, spares positioning, and environmental hardening. Airborne and maritime use cases introduce additional stabilization and maintenance requirements, which increase sustainment complexity. Supply chains for detectors, cryogenic assemblies, and precision optics remain capacity-constrained, generating lead-time variability and cost pressure. Without controlled program management, these factors defer milestones and dilute return on early capital outlays.

U.S. Tariff Impact

The market for quantum communication is adversely affected by US tariffs, which raise the price of specialized parts, interfere with supply chains, and impede R&D. Tariffs on high-tech components, such as photonic chips and detectors, increase production costs for businesses, cause procurement delays, and impede the development of important breakthroughs. Furthermore, U.S. tariffs hit quantum-communication supply chains in three places. First, Section 301 duties on China target strategic inputs (e.g., wafers, tungsten, polysilicon), lifting costs for photonics, detectors, and precision opto-mechanics inside terminals and ground stations. Second, Section 232 steel/aluminum tariffs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Architecture

Government Network Hardening to Accelerate Fiber Metro/Long-Haul QKD Growth

Based on the segmentation of architecture, the market is classified into Space-to-Ground QKD, Inter-Satellite QKD/Entanglement, Airborne Relay QKD, Fiber Metro/Long-Haul QKD, and Maritime Free-Space QKD.

The Fiber Metro/Long-Haul QKD segment accounted for a significant market share in 2025. The growth in the segment is because ministries are mandating sovereign, tamper-evident keying between data centers and command posts, operators are extending metro rings and long-haul corridors

The Space-to-Ground QKD segment is expected to grow at a CAGR of 32.55% over the forecast period.

By Product

Crypto-Agility Mandates Are Anticipated to Support the Security Stack Segmental Growth

In terms of product, the market is categorized into Terminals (Space/Air/Sea/Ground), Photonic Components, PAT & Control, Security Stack, Test & Assurance.

The security stack segment captured the largest share of the market in 2025. As PQC rollouts collide with QKD pilots, CISOs need QRNG, KMS/HSM, and policy orchestration to unify keys and provenance. This integration pressure drives upgrades from stand-alone boxes to enterprise-grade, audit-ready data security stacks.

The Terminals (Space/Air/Sea/Ground) segment is expected to grow at the highest CAGR of 32.79% over the forecast period.

By Service

Platform Complexity is Anticipated to Accelerate the Integration & MRO Segmental Growth

Based on service, the market is segmented into Secure Link-as-a-Service, Sovereign Ground/Key Services, Integration & MRO, Validation & Accreditation, Training & Ops Support.

The Integration & MRO segment held the dominating position in 2025. Rugged terminals, PAT loops, and cryo detectors raise lifecycle risk; to sustain availability, buyers fund integration kits, accreditation, spares, and condition-based maintenance, shifting spend toward recurring MRO contracts.

The segment of Secure Link-as-a-Service is set to flourish and is growing at a CAGR of 32.75% growth across the forecast period.

By End User

Mission Assurance Requirements are Anticipated to Support the Defense Ministries & Armed Forces Segmental Growth

Based on end user, the market is segmented into defense ministries & armed forces, space agencies & sat operators, primes & tier-1s, intelligence & foreign affairs, critical-infra (dual-use).

The Defense Ministries & Armed Forces segment held the dominating position in 2025. Growth in the segment is because C2ISR links must remain trusted under contested conditions, Ministries of Defense (MoDs) prioritize quantum-secure keying in multi-theater programs, and this doctrine translates into fleet deployments, training pipelines, and long-tail sustainment.

The segment of Primes & Tier-1s will witness a growth rate of 32.58% growth across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Quantum Communication Market Regional Outlook

By regional, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

The North America held the dominant share in 2024 valuing at USD 310.27 Million and also took the leading share in 2025, with USD 399.49 Million. North America leads the global Quantum Communication market. Growth is anchored by federally funded testbeds and defense programs that prioritize sovereign key custody and interoperability with existing communication security (COMSEC). In 2026, the United States market is estimated to reach USD 213.56 Million. In the US, quantum communications solutions are expanding significantly because of government initiatives and the growing demand for secure communication in the defense and BFSI industries.

North America Quantum Communication Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe & Asia Pacific

Other regions, such as Europe and the Asia Pacific, are anticipated to witness a notable Quantum Communication Market growth in the coming years. During the forecast period, Asia Pacific Quantum Communication market is projected to record a growth rate of 33.25%, which is the highest amongst all the regions. Asia Pacific is the fastest-growing region, propelled by substantial government support, a strong emphasis on cybersecurity using post quantum cryptography, and quick developments in research and hardware. With significant government projects and deployments, including China's quantum satellite and India's quantum mission programs, China and India are in the lead. Backed by these factors, countries including China anticipates to record the valuation of USD 140.09 Million, Japan to record USD 61.48 Million, and India to record USD 91.99 Million in 2026. After Asia Pacific, the market in Europe is estimated to reach USD 233.13 Million in 2026. In the region, the U.K and Germany both are estimated to reach USD 88.35 Million and 57.21 Million by 2026.

Rest of the World

Over the forecast period, Middle East & Africa, and Latin America regions would witness a moderate growth in this marketspace. The Middle East and Africa market in 2026 is set to record USD 98.28 Million as its valuation. Latin America is set to attain the value of USD 64.62 Million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Increase in R&D Activities, New Product Development, and Partnerships Define the Competitive Landscape

This market is highly consolidated, led by Toshiba, ID Quantique, QuantumCTek, SES, Thales Alenia Space, Airbus Defence and Space, Honeywell, TESAT, QNu Labs, and BT Group. These players are investing in new product development (miniaturized terminals, faster key rates, improved detectors/PAT, QRNG, and crypto-agile KMS/HSM) and pursuing partnerships with defense ministries, space agencies, and carriers to convert pilots into national backbones. Co-development and joint demos remain the fastest path to qualification and multi-year awards. Companies are also localizing manufacturing, building second sources, and shifting toward service models.

LIST OF KEY QUANTUM COMMUNICATIONS COMPANIES PROFILED

- Toshiba (Japan)

- ID Quantique (Switzerland)

- QuantumCTek (China)

- SES (Luxembourg)

- Thales Alenia Space (France)

- Airbus Defence and Space (France)

- Honeywell (U.S.)

- TESAT (Germany)

- QNu Labs (India)

- BT Group (U.K.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: The European Space Agency (ESA) and Thales Alenia Space have inked a contract for the SAGA (Secure and cryptoGraphic) mission. For governmental usage, the contract includes the quantum communication systems description and initial design of a fully European end-to-end Quantum Key Distribution (QKD) system.

- May 2023: The Quantum Key Distribution (QKD) payload for the EAGLE-1 satellite is being developed and integrated by TESAT, a new primary partner announced by EAGLE-1 consortium lead SES. The next major milestone in developing and executing Europe's ground-breaking quantum secure communications project, EAGLE-1, is what the SES and TESAT alliance aims to accomplish.

- September 2024- Toshiba, Equinix, and BT Group announced that they will offer quantum secure connectivity at two prestigious Equinix colocation data centers in Slough and Canary Wharf, London.

- August 2025: sky perfect JSAT is participating in a research and development initiative headed by Japan's National Institute of Information and Communications Technology (NICT) to demonstrate satellite-based quantum key distribution (QKD).

- June 2023- The Indian Navy and QNu Labs have partnered to acquire and implement technologies based on Quantum Key Distribution (QKD). According to a release, this partnership marks a significant turning point and makes the Indian Navy the nation's first organization to acquire extensive quantum-based encryption technology.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key Quantum Communication industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 32.31% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Architecture, Product, Service, End User, and Region |

| By Architecture |

|

| By Product |

|

| By Service |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 980.90 Million in 2025 and is projected to reach USD 11973.59 Million by 2034.

In 2024, the market value stood at USD 399.49 Million.

The market is expected to exhibit a CAGR of 32.31% during the forecast period of 2026-2034.

The Fiber Metro/Long-Haul QKD segment led the market by Architecture.

Sovereign Secure Communications Demand is Anticipated to Drive Market Growth

Toshiba (Japan), ID Quantique (Switzerland), QuantumCTek (China), SES (Luxembourg), Thales Alenia Space (France), and Airbus Defence and Space (France) are some of the prominent players in the market.

North America dominated the quantum communication market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 277

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us