Quicklime Market Size, Share & Industry Analysis, By Type (High Calcium Quicklime, Dolomitic Quicklime, and Others), By Application (Mining & Metallurgy, Building & Construction, Water Treatment, Chemical, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

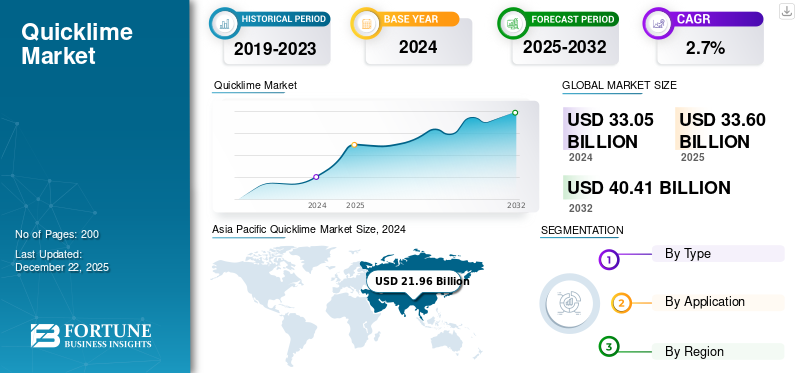

The global quicklime market size was valued at USD 33.6 billion in 2025 and is projected to grow from USD 34.18 billion in 2026 to USD 42.6 billion by 2034, exhibiting a CAGR of 2.7% during the forecast period. Asia Pacific dominated the quicklime market with a market share of 66% in 2025.

The global market is witnessing steady growth opportunities driven by applications such as, steel manufacturing, construction material processing, water purification, and chemical synthesis. Quicklime, also known as calcium oxide or burnt lime, is a chemical compound produced by the thermal decomposition of limestone or dolomite in a lime kiln. Also known as calcium oxide, it appears as a white, caustic, alkaline crystalline solid at room temperature. The product is widely utilized in various industries due to its reactivity with water and acids, forming hydrated lime or calcium hydroxide. Additionally, burnt lime is a critical material for adjusting pH levels, removing impurities, and stabilizing soil in construction. Rising demand from sustainable water treatment technologies and infrastructure development will significantly drive the growth of the industry.

The main players working in the market include Carmeuse, Lhoist Group, Graymont Limited, United States Lime & Minerals, Inc., and Sigma Minerals Ltd.

Download Free sample to learn more about this report.

QUICKLIME MARKET TRENDS

Increased Use of Quicklime in Recycling and Waste Management Boosts Market Growth

The burnt lime is increasingly applied in waste treatment and recycling, supporting global sustainability goals. It is widely used to treat industrial sludge, neutralize acidic waste, and control odors in landfill sites. Additionally, in metal recovery and e-waste processing, it facilitates separation and detoxification steps. This growing trend is particularly prominent in regions where environmental regulations are tightening and companies are under pressure to reduce landfill disposal. With more cities and industries moving toward circular economy models, burnt lime’s role as a treatment and neutralization agent is being reconsidered and repurposed.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand from Steel and Metallurgical Industries is Fueling the Market Growth

The steel and metallurgical industries are among the largest consumers of the product globally, and their continued growth fuels product demand. Burnt lime is vital in removing sulfur, silica, and phosphorus impurities during the steelmaking process. As countries invest in modern infrastructure, smart cities, and green building projects, the need for steel is surging, thereby boosting the consumption of the product. Moreover, the burnt lime is essential for non-ferrous metallurgy, including aluminum and copper processing. The ongoing modernization of the steel industry and the rising focus on high-grade steel products position it as an important growth driver in the market.

MARKET RESTRAINTS

Environmental and Regulatory Challenges could limit Market Growth

Environmental concerns and regulatory pressures pose significant restraints on the market, especially in regions committed to carbon neutrality and sustainable industry practices. The production of burnt lime releases a substantial amount of carbon dioxide, not only from fuel combustion but also from the chemical decomposition of limestone itself. This dual-source emission profile makes it difficult for manufacturers to meet low-emission targets without major technological upgrades. Smaller manufacturers, in particular, struggle to meet these standards due to limited access to green technologies and funding. Furthermore, the need for continuous monitoring, advanced pollution control systems, and sustainability certifications is restricting industry growth.

MARKET OPPORTUNITIES

Rising Demand from Flue Gas Treatment in Power Plants Poses a Strong Opportunity for the Market

The increasing focus on reducing air pollution has created substantial opportunities for quicklime in flue gas desulfurization systems used in thermal power plants and industrial boilers. The product effectively removes sulfur dioxide and other acidic pollutants from flue gases, making it a preferred material in emission control systems. Its availability and efficiency make it a reliable option for large-scale pollution mitigation projects. Retrofitting existing coal-based power plants and establishing new industrial facilities are expected to drive significant consumption.

- According to UNICEF, in 2021, many people were facing chronic health issues globally due to air pollution. The need for the product to reduce air pollution from thermal plant systems is a major factor driving quicklime market growth.

MARKET CHALLENGE

Carbon Emission Control & Environmental Regulations Pose a Major Challenge to the Market

One of the major challenges facing by quicklime industry is the persistent issue of carbon emissions during production. The calcination of limestone naturally releases CO₂, not just from fuel combustion but also as a by-product of the chemical reaction. This unavoidable process makes achieving carbon neutrality extremely difficult with current technologies. Moreover, global regulations aimed at reducing greenhouse gases are intensifying, placing additional pressure on lime producers to develop cleaner alternatives or improve process efficiency.

TRADE PROTECTIONISM

Trade protectionism is increasingly affecting the market, particularly regarding tariffs, import restrictions, and local sourcing mandates. Several countries have imposed duties on lime imports to protect domestic manufacturers, often citing dumping practices or strategic resource control. While such measures support local industries, they disrupt global supply chains and raise prices for end users in construction, mining, and water treatment sectors.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Growing Adoption of High Calcium Quicklime in Various End-Use Industries Boosts Segment Growth

Based on type, the market is classified into high calcium quicklime, dolomitic quicklime, and others.

The high calcium quicklime segment holds the dominant quicklime market share as it is widely used in industrial sectors for its strong alkalinity and reactivity. The calcination of pure limestone produces this type of lime and finds application in steel manufacturing, flue gas desulfurization, chemical production, and soil stabilization. It plays a vital role in metallurgical processes by removing impurities and enhancing thermal reactions. It is also used for wastewater treatment and neutralizing acidic conditions in the environmental sector. Additionally, the increasing focus on eco-friendly building materials drives their use in the construction industry as a binding and drying material.

Dolomitic quicklime, derived from dolomite rock, contains calcium oxide (CaO) and magnesium oxide (MgO), giving it unique properties compared to high-calcium type. It is particularly valued in applications that benefit from the dual alkalinity of calcium and magnesium, such as the steel and refractory industries. In steelmaking, it helps improve slag properties, enhancing the removal of impurities such as sulfur and phosphorus. It also finds increasing use in glass manufacturing, chemical processing, and soil treatment, where the magnesium content is advantageous.

By Application

Mining & Metallurgy Segment Dominates due to Its Efficiency in Removing Impurities

Based on application, the market is classified into mining & metallurgy, building & construction, water treatment, chemical, and others.

Mining & metallurgy holds the largest share of the market, due to its efficiency in impurity removal, metal recovery, and pH regulation. In metallurgy, it is used in steelmaking processes to eliminate impurities such as silica, phosphorus, and sulfur from molten metal. It acts as a flux, promoting better slag formation and improving the quality of finished metal products. In mining, it is used in ore concentration processes such as flotation, where it adjusts pH levels to optimize mineral separation. Its ability to improve operational efficiency and reduce environmental risks makes it a key input in metal and mineral extraction activities.

The building and construction sector extensively utilizes burnt lime due to its binding, drying, and stabilizing properties. It is employed in producing lime-based mortars and plasters that offer high durability and resistance to environmental conditions. It is also essential for soil stabilization, especially in road construction, where it improves load-bearing capacity and prevents soil swelling and shrinkage. The trend toward eco-friendly construction practices has further promoted the use of quicklime, as it helps reduce carbon footprints when combined with supplementary cement materials.

Quicklime is a widely adopted chemical in the water treatment industry due to its effective pH adjustment and impurity removal capabilities. It is commonly used in municipal and industrial water treatment plants to neutralize acidic waters and precipitate heavy metals. Its ability to react quickly with contaminants makes it valuable in drinking water purification and wastewater treatment. Additionally, it is used in treating sludge and biosolids, making disposal safer and more compliant with environmental norms.

Quicklime Market Regional Outlook

By geography, the market is categorized into Asia Pacific, North America, Europe, and the Rest of the World.

Asia Pacific

Asia Pacific Quicklime Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 22.28 billion, contributing 66.00% to global market revenue, and is projected to grow to USD 22.62 billion in 2026, fueled by rapid industrialization, infrastructure expansion, and large-scale metallurgy operations. China, India, and Japan are key contributors, driven by massive steel production and growing construction activity. It is widely used for its cost-effectiveness and availability across diverse applications such as mining, cement, chemicals, and water treatment. In countries such as China and India, government-led infrastructure development and industrial projects create continuous demand for lime-based materials.

North America

The North America region captured 9.00% of the global market in 2025, generating USD 2.93 billion in revenue, and is projected to reach USD 2.98 billion in 2026. North America is one of the prominent regions in the market, driven by its well-established industrial base and strong demand across steel, construction, and environmental applications. The U.S. and Canada lead the region with advanced mining and metallurgical operations, where it is critical in impurity removal and pH control. Infrastructure upgrades and government investments in construction further support consistent demand for lime in cement and soil stabilization.

Europe

Europe maintained a strong presence in the global market, reaching USD 5.22 billion in 2025, accounting for 16.00% share, and is expected to reach USD 5.33 billion in 2026. Stringent environmental norms, energy-efficient manufacturing goals, and sustainable infrastructure initiatives drive Europe's quicklime market. Countries such as Germany, the U.K., and France dominate the region with strong consumption in steel production, water treatment, and advanced construction materials. The European Union’s focus on reducing carbon emissions and promoting green energy has encouraged the use of burnt lime in environmental applications, including flue gas treatment and hazardous waste stabilization.

Latin America

The Latin America market generated USD 1.66 billion in 2025, representing 4.90% of the global market landscape, and is expected to reach USD 1.7 billion in 2026. Latin America is witnessing growing demand for the product due to expanding industries such as mining, construction, and chemicals. Countries such as Brazil and other major countries are key contributors, where it is widely used in metal extraction, soil improvement, and water treatment. The region's strong mining sector, particularly copper and gold, supports substantial consumption of burnt lime for pH regulation and ore flotation.

Middle East & Africa

Middle East & Africa recorded a market size of USD 1.5 billion in 2025, capturing 5.00% of the global market share, and is projected to reach USD 1.55 billion in 2026. The Middle East and Africa region is gradually emerging as a notable market for quicklime, backed by infrastructure development, resource exploration, and environmental remediation projects. Countries such as Saudi Arabia and South Africa are leading in demand due to their growing construction, mining, and water treatment industries. The Gulf countries' construction boom drives cement usage, soil stabilization, and road building.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Development and Introduction of New Products by Key Companies Resulted in Their Dominating Position in the Market

The market is highly competitive, with major players focusing on capacity expansion, sustainability, and mergers & acquisitions to strengthen their market presence. Key global companies include Carmeuse, Lhoist Group, Graymont Limited, United States Lime & Minerals, Inc., and Sigma Minerals Ltd. These companies compete based on product innovation, cost-efficiency, and regional dominance. While global leaders dominate in developed markets, regional players are expanding aggressively in emerging economies, intensifying competition in the industry.

LIST OF KEY QUICKLIME COMPANIES PROFILED

- Carmeuse (Belgium)

- Cheney Lime & Cement Company (U.S.)

- Lhoist Group (Belgium)

- Graymont Limited (Canada)

- Mississippi Lime Company d/b/a MLC. (U.S.)

- United States Lime & Minerals, Inc. (U.S.)

- Pete Lien & Sons, Inc. (U.S.)

- Sigma Minerals Ltd. (India)

- Cornish Lime (U.K.)

- Greer Lime Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2024: Mississippi Lime Company (MLC), a leading global supplier of lime products and technical solutions, would invest in constructing a state-of-the-art, sustainable kiln at its newly acquired lime operation in Bonne Terre, Mo. The construction began in early 2024, and commissioning will be completed by 2026.

- September 2023: Graymont Limited plans to expand its business in Southeast Asia. The company acquired Compact Energy, a major lime processing facility in Malaysia. Through this move, the company is expected to produce 600,000 tons of quicklime and 170,000 tons of hydrated lime annually.

- September 2022: Mississippi Lime Company completed its acquisition of Valley Minerals, a single-site dolomitic quicklime producer based in Bonne Terre, Missouri. The acquisition would help Mississippi Lime expand on its commitment to better serve the growing next-generation steel production base.

- April 2025: Graymont has announced that they are making an investment to expand its lime production in Victoria, Australia, to meet the needs of its growing customer base. The company has acquired land for expansion and has also built a Logistics Terminal in Melbourne to expand its supply network.

- May 2024: The Lhoist Group announced that they are aiming to produce the first low-carbon dolime at its Dolomies de Marche-les-Dames site. The project is called GLOBE, it is a part pf Lhoist's commitment to an ambitious policy of decarbonizing its activities.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.7% from 2026-2034 |

|

Unit |

Value (USD Billion) & Volume (Million Ton) |

|

Segmentation |

By Type · High Calcium Quicklime · Dolomitic Quicklime · Others |

|

By Application · Mining & Metallurgy · Building & Construction · Water Treatment · Chemical · Others |

|

|

By Geography North America (By Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Type, Application, and Country/Sub-region) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Type, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Type, Application, and Country/Sub-region) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Type, Application, and Country/Sub-region) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 34.18 billion in 2026 and is projected to reach USD 42.6 billion by 2034.

In 2025, the market value stood at USD 22.28 billion.

The market is expected to exhibit a CAGR of 2.7% during the forecast period (2026-2034).

High calcium quicklime type leads the market by type.

Growing demand from the steel and metallurgical industries is the key factor driving the market.

Carmeuse, Lhoist Group, Graymont Limited, United States Lime & Minerals, Inc., and Sigma Minerals Ltd. are some of the leading players in the market.

Asia Pacific dominates the market.

The growing usage of steel in infrastructure and construction development will likely drive the product's adoption in the forthcoming years.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us