Railway Wiring Harness Market Size, Share & Industry Analysis, By Train Type (Metro, Light Train, High Speed Train/ Bullet Train), By Cable Type (Power Cable, Jumper Cable, Transmission Cable), By Material Type (Copper, Aluminium, Others), By Application Type (HVAC, Brake Harness, Lighting Harness, Traction System Harness) and Regional Forecast, 2026-2034

Railway Wiring Harness Market Future Outlook

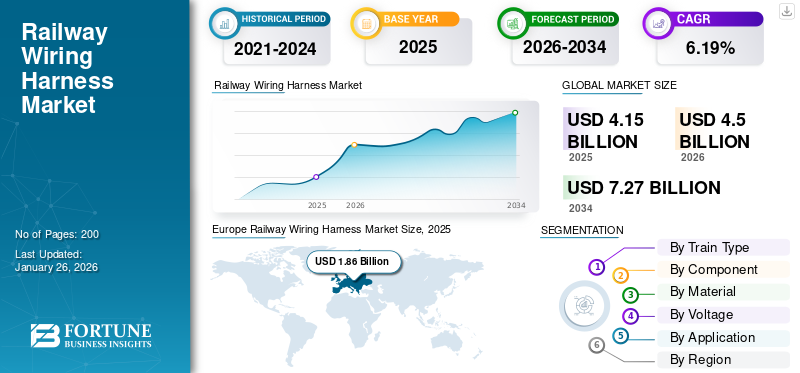

The global railway wiring harness market size was valued at USD 4.15 billion in 2025 and is projected to grow from USD 4.5 billion in 2026 to USD 7.27 billion by 2034, exhibiting a CAGR of 6.19% during the forecast period. Europe dominated the global market with a share of 44.73% in 2025.

A railway wiring harness is an organized assembly of wires, cables, terminals, and connectors that transmit electrical power and signals across various train systems. It ensures efficient and reliable communication between components such as lighting, HVAC, propulsion, and control systems. These harnesses are designed with durability and withstand vibration, temperature extremes, and environmental exposure, contributing to safe and uninterrupted train operations across different types of rolling stock, including locomotives, metros, and high-speed trains.

The market is experiencing significant growth driven by massive investments in expanding and modernizing rail infrastructure, especially metros and high-speed networks, spurred by urbanization and government funding. Electrification of trains and the rising demand for electric/hybrid rolling stock further amplify the harnessing needs. Additionally, the rising integration of digital systems, such as infotainment, smart sensors, and IoT, will boost market demand in the near future.

Key players include major firms such as Hitachi, TE Connectivity, Sumitomo Electric, and Schleuniger. These companies lead through technological investment, strategic acquisitions, and broad geographic presence. Development in material technology, product durability, and tailored offerings further strengthens their market leadership.

Download Free sample to learn more about this report.

Railway Wiring Harness Market Key Takeaways

- 2025 Market Size: USD 4.15 Billion

- 2026 Market Size: USD 4.50 Billion

- 2034 Forecast Market Size: USD 7.27 Billion

- CAGR: 6.19% from 2026–2034

- Europe dominated the railway wiring harness market with a 44.73% share in 2025.

- The others segment (commuter rails, trams, and other train types) is projected to account for 45.60% of the market in 2026.

- The copper segment is expected to hold a 54.05% market share in 2026.

Europe

Europe accounted for USD 1.86 billion in 2025 and is projected to reach USD 2.02 billion in 2026.

North America

North America generated USD 0.75 billion in 2025 and is expected to grow to USD 0.81 billion in 2026.

Asia Pacific

Asia Pacific reached USD 0.96 billion in 2025 and is projected to grow to USD 1.05 billion in 2026.

U.S.

The market is projected to reach USD 0.38 billion by 2026.

Japan

The market is projected to reach USD 0.03 billion by 2026.

Read More

Market Dynamics

Market Drivers

Railway Infrastructure Expansion Drives Market Demand

Railway infrastructure expansion significantly drives the market's growth by increasing the demand for new and upgraded trains equipped with advanced electrical systems. As countries invest in metro, high-speed, and light rail projects to enhance public transport and reduce carbon emissions, there is a parallel rise in the need for complex wiring systems to support power distribution, control units, and passenger amenities. Modern trains increasingly integrate technologies such as communication, surveillance, HVAC, and infotainment systems, all of which rely on reliable and efficient wiring harnesses. Additionally, the electrification of rail networks further amplifies the harness requirements for propulsion and auxiliary systems. Thus, each infrastructure project directly fuels growth in the demand for the market globally. In May 2025, Amtrak spearheaded a sweeping transformation of the U.S. rail system through a USD 50 billion capital investment plan. This includes fleet modernization, such as adding eco-friendly Airo and new Acela trainsets, 125 hybrid locomotives, and station and infrastructure upgrades, including bridges, tunnels, railyard overhauls, and enhanced ADA accessibility.

Market Restraints

Long Replacement Cycles to Restrain Market Growth

Long replacement cycles restrain the market's growth, as these components are built for durability, often lasting 15 to 30 years under harsh operating conditions. Once installed, they require minimal maintenance and infrequent replacement, limiting recurring revenue opportunities for manufacturers. Unlike industries such as automotive or electronics, where upgrades and replacements are frequent, the railway sector operates on extended product life cycles, resulting in slower aftermarket demand. This affects the volume of harnesses sold annually, even in the face of rising new rail infrastructure projects. Additionally, the long intervals between replacements discourage frequent technological upgrades in older rolling stock, further slowing innovation-driven demand in the retrofit market. Thus, the adoption of the global railway wiring harness market strongly depends on the new infrastructure development rather than recurring sales, which hampers the demand for the product in the long run.

Market Opportunities

Smart and Connected Trains to Provide Growth Opportunities for the Market

Smart and connected trains offer significant growth opportunities for the market by integrating advanced digital systems such as IoT, AI, real-time diagnostics, and predictive maintenance. These technologies require reliable and high-speed data transmission across various onboard systems, including sensors, control units, infotainment, surveillance, and communication networks. As a result, there is a rising demand for sophisticated, high-bandwidth wiring harnesses with enhanced EMI shielding, lightweight materials, and modular designs. Additionally, smart train applications also introduce more wiring density and complexity, especially in automated and driverless train systems. This shift drives innovation in cable architecture and fosters long-term partnerships with OEMs and system integrators. These collaborations allow manufacturers to expand their product offerings and play a critical role in shaping the future of intelligent rail systems, driving the global railway wiring harness market growth. In September 2024, CRRC unveiled two pioneering green installing trains at InnoTrans 2024 in Berlin: the CINOVA H2 hydrogen-powered intercity model and autonomous Rail Rapid Transit 2.0. These zero-emission, ultra-long-range, autonomous-capable solutions are expected to cut nearly 730 tons of CO2 per train annually.

Market Challenges

High Complexity in Wiring Architecture to Challenge Market Development

High complexity in wiring architecture presents a significant challenge to the growth of the railway wiring harness market by increasing design, integration, and installation difficulties. Modern trains are equipped with numerous subsystems, such as propulsion, HVAC, infotainment, control, and safety systems, each requiring reliable and interconnected wiring. Designing a harness that supports dense electrical pathways within limited space while ensuring electromagnetic compatibility, fire resistance, and durability is highly complex. Moreover, customization needs for different train types and regional standards further increase engineering effort and time. This leads to longer development cycles, higher production costs, and increased potential for installation errors or maintenance issues, further challenging the growth of the market.

Railway Wiring Harness Market Trends

Electrification of Rail Networks is a Significant Trend in the Market

The electrification of rail networks is a key trend in the market, as countries aim to reduce carbon emissions and improve energy efficiency. Electrified trains require complex and high-performance wiring harnesses to connect components such as traction motors, power converters, pantographs, batteries, and auxiliary systems. This increases the demand for high-voltage, heat-resistant, and flame-retardant cables. As more rail operators transition from diesel to electric locomotives and EMUs, the need for durable and reliable electrical infrastructure grows. Electrification also supports the integration of smart systems such as regenerative braking and onboard monitoring, which further increase wiring complexity and volume. Thus, rail electrification directly boosts the demand for railway wiring harnesses worldwide. In May 2025, Croatia launched its first battery-electric multiple unit (BEMU) on the Zagreb-Bjelovar-Zagreb route. Developed by Koncar, the train operates for up to 18 hours/day, covering 480 km daily, with speeds of 160 km/h on catenary power and 120 km/h in battery mode.

Download Free sample to learn more about this report.

Impact of Tariffs

Rise in Costs and Complications in Sourcing Raw Materials Hampers Market Expansion Due to Tariffs

In June 2025, the U.S. imposed tariffs ranging from 25% to 50% on imports of steel, aluminum, and electrical components, including copper, a critical material for railway wiring harnesses. These tariffs have increased material costs by around 10 to 15%, significantly raising production expenses for wiring harness manufacturers. Higher costs can either reduce profit margins or force price hikes, making the U.S.-made harness less competitive globally. Supply chain disruptions are emerging as companies shift sourcing strategies to lower-cost regions in an effort to avoid tariffs. The uncertainty surrounding trade policies is also causing delays in investment decisions related to railway projects. Although a trend toward shoring is evident in the U.S., establishing local production facilities requires significant capital and time, limiting short-term capacity growth. As a result, these tariffs are driving up costs, complicating sourcing strategies, and impeding market expansion.

Segmentation Analysis

By Train Type

High-Speed Rail/Bullet Rail Segment to Display High Growth Rate due to Expanding Infrastructure

By train type, the market is categorized into metro rail transit/monorail, light rail transit, high-speed rail/bullet rail, and others.

The high-speed rail/bullet rail segment is likely to exhibit the highest growth rate during the forecast period. The growth is fueled by expanding infrastructure in China, India, and Europe, as governments are investing in HSR to provide fast, efficient, and green alternatives to air and road travel. These trains require advanced and high-density wiring harnesses to support propulsion systems, braking, communication, and infotainment technologies. Their complexity and need for high-performance materials create a surge in segmental demand in the forecast period.

In May 2025, Trenitalia, Deutsche Bahn, and OBB announced plans to launch direct Frecciarossa high-speed services from Milan and Rome to Munich in December 2026. These routes extend through Austria and will be expanded to Berlin and Naples by December 2028.

By Component

Wire Segment Led the Market due to Extensive Use in Safety Systems

By component, the market is characterized into wire, connector, terminal, and others.

Connectors are the fastest-growing segment as modularity and plug-and-play systems become the norm in modern rail manufacturing. Rising complexity in railway wiring harness systems and the need for ease of assembly, maintenance, and upgrade are driving the demand for advanced connectors. High-speed data transmission, safety-critical operations, and automated systems in smart and high-speed trains require reliable, EMI-resistant connectors. Moreover, the growth in infotainment, communication systems, and real-time diagnostics also supports the rapid growth of the segment during the forecast period.

In October 2022, at Inno Trans, Staubli unveiled the EvoTrak Lite modular connector, a compact, metal-enclosed solution for medium-power traction chain applications. The connector is rated up to 1,500 V/300-330 A, 1-4 poles, 10-70 sqmm cables, with IP66-67, phase segregation, shielded-cable EMI management, and IP2X safety. Its lightweight design meets EN 50467 and EN 45545-2 standards, offering installation flexibility in confined rail vehicle spaces.

By Material

Superior Electrical Conductivity, Flexibility, and Durability Boosts Copper Segment Growth

By material, the market is divided into copper, aluminum, and others.

Copper remains the dominant material due to its superior electrical conductivity, flexibility, and durability. It is widely used across power, control, and combination systems in all types of rail vehicles. The copper segment will account for 54.05% market share in 2026. Copper’s high thermal resistance and operational efficiency make it well-suited for harsh rail environments. Furthermore, most industry standards and legacy systems are designed around copper solutions, reinforcing its widespread use despite rising material costs. This entrenched adoption surges the growth of the segment over the study period.

Aluminum is gaining traction as a lighter and cost-effective alternative to copper, especially in high-voltage and weight-sensitive applications such as high-speed and electric trains. Advancements in insulation and alloying technologies have improved aluminum’s reliability and conductivity. Its use helps reduce train weight, enhancing energy efficiency and range. As sustainability and cost control become priorities, aluminum is expected to witness significant adoption, particularly in newer and electrified platforms.

By Voltage

Shift toward Electrification of Rail Systems Propels High Voltage Segment Growth

By voltage, the market is divided into low voltage, medium voltage, and high voltage.

The high voltage segment will account for 53.61% market share in 2026. The high voltage segment dominates and is expected to register the fastest CAGR during the forecast period due to the global shift toward the electrification of rail systems. Electric trains, especially in high-speed and long-distance applications, require high-voltage systems for traction, power distribution, and regenerative braking. As railways move away from diesel engines, the demand for high-voltage harnesses will rise significantly over the forecast period.

The medium voltage segment held the second-largest railway wiring harness market share in 2024, supporting auxiliary systems such as HVAC, lighting, and onboard converters, which are used in both electric and hybrid trains, particularly within metro and regional rail networks. Their importance lies in balancing performance and safety across various train systems without the complexity or cost of high-voltage components. As train complexity increases, medium-voltage systems continue to be widely implemented globally over the timeframe.

By Application

To know how our report can help streamline your business, Speak to Analyst

High-Voltage and Complex Wiring Configurations Boost Traction System/Engine Segment Growth

By application, the market is divided into HVAC, brake & lighting, traction system/engine, infotainment, and others.

The traction system/engine segment dominates as it forms the core of power delivery in electric and hybrid trains. Wiring harnesses in this segment are critical for connecting motors, converters, and converter units, requiring high heat and vibration resistance. Engine systems use high-voltage and complex wiring configurations, driving higher material and engineering requirements. The push toward electrified propulsion further increases the demand for robust engine wiring solutions.

Infotainment is the fastest-growing application in the market as modern trains increasingly focus on passenger comfort, convenience, and connectivity. Demand for onboard Wi-Fi, display screens, USB ports, real-time information systems, and surveillance has surged. These systems require advanced wiring to support data and power transmission. Growing expectations from commuters, especially in metro and intercity services, are prompting OEMs and operators to upgrade infotainment capabilities, boosting the demand for wiring harnesses in the segment.

Railway Wiring Harness Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Railway Wiring Harness Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2024 due to its extensive electrified railway network, high-speed rail coverage, and strong environmental regulations. Europe accounted for USD 1.86 billion in 2025, representing 44.73% of the global market share, and is projected to reach USD 2.02 billion in 2026. Countries such as Germany, France, and the U.K. invest heavily in modernizing rolling stock, expanding metro systems, and implementing smart rail technologies such as ETCS and predictive maintenance. Strict regulatory standards such as EN 45545 mandate fire-safe, halogen-free wiring harness, boosting demand for advanced materials. The EU’s Green Deal, favoring a shift from road to rail, supports growth in wiring systems for both passenger and freight applications. Europe’s established OEM base and strong export capability further contribute to its leadership in the market. The UK market is projected to reach USD 0.23 billion by 2026, and the Germany market is projected to reach USD 0.47 billion by 2026.

North America

North America contributed 18.12% to the global market in 2025, with a valuation of USD 0.75 billion, and is projected to reach USD 0.81 billion in 2026. North America held a moderate share of the market in 2024, driven by efforts to modernize aging rail infrastructure and expand urban transit networks. Key investments include the electrification of select corridors and the upgrade of Amtrak services, which are supporting the demand for high-voltage wiring harnesses. Smart technologies such as Positive Train Control (PTC), real-time monitoring, and enhanced transporting and passenger amenities drive the need for complex wiring systems. Growing emphasis on freight rail efficiency, sustainability, and safety compliance further boosts market demand. Additionally, strong government funding and the rise of public-private partnerships across the U.S. and Canada are creating opportunities for suppliers offering advanced, durable, and flame-retardant railway wiring harness systems. The U.S. market is projected to reach USD 0.38 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 0.96 billion in 2025, capturing 23.11% of global revenue, and is estimated to reach USD 1.05 billion in 2026. Asia Pacific was the fastest-growing region in 2025, driven by large-scale railway infrastructure development in China, India, Japan, and Southeast Asia. Rapid urbanization fuels the expansion of metro and suburban rail systems, while ambitious high-speed rail projects such as India’s bullet train and China’s HSR network demand advanced, high-voltage wiring harnesses. Government initiatives promoting rail electrification and public transport modernization are encouraging the adoption of the global railway wiring harnesses across the region. These initiatives support the integration of sophisticated control, safety, and infotainment systems, thereby driving wiring complexity. Cost-effective manufacturing, a rising domestic OEM base, and foreign investment also support regional growth. The demand for lightweight, durable, and scalable harness solutions continues to rise across both new builds and retrofits, which fuels market growth. In May 2025, Proterial’s durable contact wire – GT-SNNSK110, featuring tin-indium alloy and visual wear-groove markers, will deploy on Tokyo’s Keio Line between Chofu and Sengawa. It delivers ≥20% greater tensile strength than pure copper, improves wear resistance, and simplifies maintenance. As Japan’s first private railway adoption of this technology, it reflects the move toward cost-efficient and high-performance electrical infrastructure. The Japan market is projected to reach USD 0.03 billion by 2026, the China market is projected to reach USD 0.52 billion by 2026, and the India market is projected to reach USD 0.13 billion by 2026.

Rest of the World

The Rest of the World region captured 14.03% of the global market in 2025, generating USD 0.58 billion in revenue, and is projected to reach USD 0.62 billion in 2026. The rest of the world held a smaller share in 2024, although it shows steady growth, supported by increased investments in rail in South America, the Middle East, and Africa. Brazil, Saudi Arabia, Egypt, and the UAE are developing metro, commuter, and high-speed rail networks to improve connectivity and reduce urban congestion. These projects often involve imported trains or international technology partnerships, increasing the use of advanced wiring harnesses. Though infrastructure is developing at a slower pace than in other regions, strategic public-private initiatives and smart city development projects are driving gradual market expansion in the region.

Competitive Landscape

Key Market Players

Key Players Focus on Advanced Technologies to Gain Competitive Edge

The global railway wiring harness market exhibits a moderately consolidated competitive landscape, characterized by the presence of multinational giants and regional players. Key companies such as Hitachi, TE Connectivity, Sumitomo Electric, and Schleuniger dominate the market due to their strong R&D capabilities, global supply chains, and long-term contracts with OEMs and transit authorities. These firms focus on product innovation, lightweight materials, fire safety compliance, and modular harness designs to meet evolving regulatory and performance standards. Emerging players in Asia are gaining ground by offering cost-competitive solutions and localized support. Strategic collaborations, mergers, and capacity expansion in high-growth regions further define the competition in the market. Continuous advancements in smart train technologies and electrification are intensifying the race for technological leadership.

List of Key Railway Wiring Harness Companies Profiled

- Proterial, Ltd. (Japan)

- Sumitomo Electric (Japan)

- TE Connectivity (Switzerland)

- Schleuniger (Switzerland)

- RPI Manufacturing (U.S.)

- Schrade Kabeltechnik GmbH (Germany)

- Excel Connection (U.S.)

- Voitas Engineering (Poland)

- Harness Techniques Pvt. Ltd (India)

- Cheers Electronic Technical Ltd. (China)

- Questex LLC (U.S.)

- HUBER+SUHNER - Phoenix Dynamics Limited (U.K.)

- Jeanuvs Pvt Ltd. (India)

- Control Cable, Inc. (U.S.)

- Motherson (India)

Key Industry Developments

- May 2025: Keio Corporation became the first private Japanese railway to introduce Proterial’s durable alloy contact wire (GT-SNNSK110) on sections of the Keio Line. Enhanced with tin and indium, it offers 20% higher tensile strength and better wear resistance than pure copper, featuring wear-grooves for visual maintenance cues. The upgrade aims to reduce labor maintenance costs and boost efficiency.

- August 2024: Cheers Electric, with over 15 years in wire harness manufacturing, introduced an advanced range of cable-processing solutions. Their lineup includes a range of semi-and fully-automatic wire-cut/strip/crimp machines, ultrasonic wire welders, benchtop, and cable lug crimpers. These machines deliver speeds of 1,000-4,500 psc/hour and precision of up to ±0.02 mm. Engineered for industrial scalability, they feature PLCs, touchscreens, quick-change tooling, and comply with CE/RoHS standards.

- May 2024: Motherson Sumi Wiring increased its wiring harness capacity by 10% as two new plants became operational in Q1, targeting ramp-up by Q3-Q4. These facilities serve both ICE and EV customers, aligning with expanding OEM capacities amid India’s rising demand for electrification.

- September 2023: Motherson opened its eighth UAE wiring harness facility in Ras AI Khaimah’s RAKEZ zone. With a EUR 10 million (USD 11.7 million) investment, the 11,000 sqm plant employs 500 staff, producing harnesses for commercial and special purpose vehicles and exporting to Europe.

- October 2022: HUBER+SUHNER acquired U.K.-based Phoenix Dynamics Ltd., rebranding it as HUBER+SUHNER Phoenix Dynamic Ltd. Phoenix Dynamics, a Staffordshire specialist in customized cable assemblies and electro-mechanical connectivity for aerospace, defense, automotive, energy, marine, medical, and rail sectors, brings 25 years of high-end industrial expertise. The acquisition enhanced HUBER+SUHNER’s end-to-end solutions and global engineering capabilities.

Investment Analysis and Opportunities

The global railway wiring harness market presents strong investment opportunities driven by rising rail infrastructure projects, urban transit expansion, and global electrification initiatives. Governments worldwide are allocating significant budgets to modernize and electrify railway networks, especially in Asia Pacific and Europe. Investors can benefit from the demand for advanced, lightweight, and fire-retardant harness solutions as rail operators prioritize safety and energy efficiency. Growth in smart rail systems, including predictive maintenance, infotainment, and real-time diagnostics, opens avenues for innovation in high-speed data and power cabling. Additionally, public-private partnerships and policy support in emerging economies offer a favorable investment climate. Companies investing in automation, localized manufacturing, and sustainable materials stand to gain a competitive benefit and capture long-term growth in this expanding and evolving market.

Report Coverage

The global railway wiring harness market report analyzes the market in depth. It highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, train type, material type, component, voltage, and application. Besides this, the market research report provide insights into the market trends and highlight significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.19% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Train Type

By Component

By Material

By Voltage

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says the global market was valued at USD 4.15 billion in 2025 and is anticipated to reach USD 7.27 billion by 2034.

The market will exhibit a CAGR of 6.19% over the forecast period (2026-2034).

By component, the wire segment held the leading share of the market in 2025.

Railway infrastructure expansion is a key factor driving the market growth.

Key companies such as Hitachi, TE Connectivity, Sumitomo Electric, and Schleuniger are the leading players in the market.

In 2025, the Europe led the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us