Rapid Prototyping Materials Market Size, Share & Industry Analysis, By Material (Thermoplastics, Metal & Alloys, Ceramics, and Others), By Application (Construction & Manufacturing, Electronics & Consumer Goods, Automotive, Medical & Healthcare, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

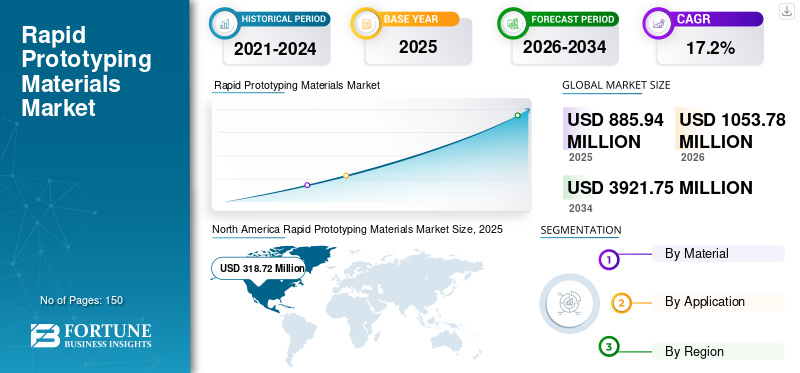

The global rapid prototyping materials market size was USD 885.94 million in 2025 and is projected to grow from USD 1053.78 million in 2026 to USD 3921.75 million by 2034 at a CAGR of 17.2% during the forecast period (2026 - 2034). North America dominated the rapid prototyping materials market with a market share of 36% in 2025.

Prior to mass production, rapid prototyping technology is often used to test the capability of materials in terms of their physical properties. On the basis of rapid prototyping material properties, the design engineers are able to produce quality products by saving time, energy, and material. Different types of rapid prototyping technologies are stereolithography (SLA), selective laser sintering (SLS), fused deposition modeling (FDM), selective laser melting (SLM), laminated object manufacturing (LOM), and others. A suitable material is used in respective technology; for instance, among different SLS rapid prototyping materials, polyamide 12 is the most popular.

Rapid prototyping is an excellent process for fabricating a physical part or model using 3D printing technology. The technology assists in creating a prototype of the idea, which assists in validating the design decisions early in the R&D phase. Efficacy in offering accelerated product development and preventing loss in mass production in the later final stages of the product will drive the demand for rapid prototyping technology.

The adoption of additive manufacturing in industrial production is growing, which is creating the demand for customized materials to match their application requirements. In response to this, various companies are investing in R&D to widen the bandwidth of their product portfolios. Growing demand from various industrial applications and heightened R&D investment will act as a catalyst for the global rapid prototyping materials market growth during the forecast period.

The progression of the COVID-19 pandemic completely or partially stopped the operation of rapid prototyping end-user in almost all key countries. Production halt in most industries, along with the shortage of thermoplastics, alloys, and other prototyping material, led to the decline in the growth of the global market.

Download Free sample to learn more about this report.

GLOBAL RAPID PROTOTYPING MATERIALS MARKET OVERVIEW

Market Size & Forecast:

- 2025 Market Size: USD 885.94 million

- 2026 Market Size: USD 1053.78 million

- 2034 Forecast Market Size: USD 3921.75 million

- CAGR: 17.2% from 2026–2034

Market Share:

- North America led in 2025 with a 36% share, rising from USD 318.72 million in 2025 to USD 373.33 million in 2026, driven by industrial 3D printing and automotive applications.

- By material: Thermoplastics dominated due to versatility, durability, and widespread adoption in prototyping.

- By application: Electronics & consumer goods held the largest share, followed by automotive and aerospace & defense.

- By innovation: Recycled and sustainable prototyping materials gaining traction.

Key Country Highlights:

- United States: High adoption in automotive, aerospace, and electronics sectors.

- China, Japan, South Korea: Rapid industrialization and availability of cost-effective raw materials driving growth.

- Germany, U.K., France, Italy: Strong prototyping services network supporting automotive, consumer goods, and aerospace applications.

- Brazil, Saudi Arabia, South Africa: Emerging markets benefiting from industrial growth and public-private investments.

Rapid Prototyping Materials Market Trends

Developing Recycled Material for Rapid Prototyping to Fuel the Trend in Market

Thermoplastics are the largest material used for rapid prototyping. Thus, with the increasing consumption of thermoplastics, the challenge of plastic waste management will become critical. The increasing concern about plastic pollution has led the key leaders to adopt recycled plastics for rapid prototyping. For instance, in March 2021, Covestro, in association with Polymaker, developed a polycarbonate filament suitable for 3D printing technology by waste bottles received from China-based Nongfu Spring. The resultant product showed lesser carbon footprints and is compatible with industry standards. The product was strategically launched for the manufacturers, who are focusing on establishing a sustainable supply chain in accordance with advanced 3D printing & rapid prototyping technologies. In a similar manner, other plastic materials, such as PE, PET, PP, and PS, can be recycled for rapid prototyping product development. North America witnessed a rapid prototyping materials market growth from USD 318.72 million in 2025 to USD 373.33 million in 2026.

Download Free sample to learn more about this report.

Rapid Prototyping Materials Market Growth Factors

Multiple Advantages Such as Designing of Rapid Prototyping to Drive Market

Rapid prototyping technology offers distinct advantages to the designers, developers, and engineers. Cost and time-efficiency attributes of rapid prototyping could give an edge over the traditional prototyping techniques. On account of the technological advancements in rapid prototyping, the prototype can be developed & tested within hours. For the same prototype, the typical CNC machining or sheet metal fabrication could take weeks due to a critical set of operations & testing. Wide range of materials, geometries, and designs can be tested to achieve the desired end product properties. Easy evaluation & testing allows designers to construct a well-defined roadmap for product refining. This, in turn, significantly reduces the flaws and risks during mass production. The unique combination of cost-effectiveness, functionality, and aesthetics can be achieved with the help of rapid prototyping. Thus, rapid prototyping and materials are gaining popularity, especially in the manufacturing sector.

Growing Demand from Automotive Industry to Boost Sales Revenue

3D printing technology has been an essential part of the automotive industry in producing fast prototyping. However, the transition from fast prototyping to producing more automotive parts and ending with producing nearly whole cars has led to a significant demand for rapid prototyping materials in the automotive industry. The ready-cast products produced through 3D printing exclude the usage of welding of pipes, elbows, and flanges, offering more accurate and efficient solutions.

Leading automotive manufacturers such as Volkswagen, BMW, and Ford are already using this technology to produce various automotive parts. BMW has used 3D printing technology to produce parts of DTM race cars, the Rolls-Royce Phantom, the BMW i8 Roadster, and others. The growing adoption of additive manufacturing technology is a surge in producing more complex and larger parts of cars, trucks, and vehicles, which is set to boost the sales of rapid prototyping materials over the forecast period.

RESTRAINING FACTORS

High Material & Process Cost to Challenge Market Growth

The initial set-up cost of rapid prototyping tools is high. Different factors, including prototype type, material, end properties, and cause & nature of prototype design define the rate or cost of rapid prototyping. Some advanced technologies could cost even USD 100,000. Rapid prototyping ceramic materials and rapid prototyping smart materials are costly in comparison with thermoplastics. The requirement of skilled manpower and technologies increases the overall cost of the operation. In addition, certain disadvantages, such as lag in accuracy & surface finishing, inadequacy in complex designs, and user-designer confusion in terms of objectives, are also restraining the global rapid prototyping materials market growth.

Rapid Prototyping Materials Market Segmentation Analysis

By Material Analysis

To know how our report can help streamline your business, Speak to Analyst

Thermoplastic Segment to Dominate Global Market owing to its Diversified Properties

On the basis of material, the market is categorized into thermoplastics, metal & alloys, ceramics, and others. Thermoplastics are the most adopted prototyping materials, owing to their diversified properties such as high strength, functionality, and durability. The thermoplastics segment led the market accounting for 60.28% market share in 2026. Thermoplastics are cheaper and available in wide & suitable range. PA, PE, PEEK, ABS, PC, and PET are a few examples of thermoplastics used to develop prototypes. Bulk availability and continuous technological development in plastic production are expected to drive the segment growth in future. Metal & alloys are also widely used to design industrial & medical prototypes. Aluminum, stainless steel and titanium are commonly used to obtain prototypes with high strength, heat resistance, chemical resistance, and other desired properties. Low quantity OEM ceramic prototypes can be produced with Lithography-based Ceramics Manufacturing (LCM). The others segment includes materials such as composites, paper, and plaster. These materials are consumed in very few quantities and occupy less share in the overall market. The metal & alloys segment is expected to hold a 24.2% share in 2023.

By Application Analysis

Electronics & Consumer Goods Segment Dominated the Market in 2023 owing to Rising Use of High-tech Gadgets

Based on application, the market is divided into construction & manufacturing, electronics & consumer goods, automotive, medical & healthcare, aerospace & defense, and others. In 2026, the electronics & consumer goods segment is projected to lead the market with a 23.3% share. With rapid digitization, the adoption of high-tech gadgets & consumer electronic products has increased. Rapid prototyping is used to develop & test wide range of electronic & consumer goods products, from PCB’s to household consumer goods, such as sporting goods. The construction & manufacturing segment is projected to grow at the slowest rate due to sluggish but steady growth of the global construction & manufacturing sector across the world. Automotive and aerospace & defense segments hold a considerably larger share of the market. Rapid prototyping is widely used thoroughly to test the functionality of automotive & aerospace parts before mass production. Increasing research & development activities to produce next-gen vehicles & aircraft are set to drive the growth of these segments. On account of the rapid adoption of rapid prototyping in developing surgical tools & medical device parts, the medical & healthcare segment is expected to indicate the fastest growth in the global market. Moreover, increasing investment in developing advanced healthcare facilities is boosting the demand for advanced rapid prototyping technologies in the healthcare industry. Others segment includes applications such as prototype developments for academics & arts. Others segment held the least share in the market and this trend is projected to remain the same in the forecast period.

REGIONAL INSIGHTS

North America

North America Rapid Prototyping Materials Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 36.00% of the global market in 2025, generating USD 318.72 million in revenue, and is expected to reach USD 373.33 million in 2026. North America is expected to dominate the global market due to well-established 3D printing technologies and larger number of service providers in the region. The U.S. is the largest consumer of rapid prototyping technologies across all major end-use industries. Advanced industrial sector, along with massive urbanization, is the main driving factor for the growth of the market. Moreover, the aerospace & medical sector is flourishing in the U.S., which is further expected to grow demand for prototyping materials in the near future. The U.S. market is projected to reach USD 353.09 million by 2026.

- In U.S., the metal & alloys segment is estimated to hold a 25.2% market share in 2023.

Asia Pacific

In 2025, Asia Pacific generated USD 262.53 million, contributing 29.60% to global market revenue, and is expected to reach USD 319.19 million in 2026. On the back of rapid industrialization in the developing economies of Asia, the region held the second largest share in the global market. China, Japan, and South Korea hold a larger portion of the market. The bulk availability of raw material at a considerably cheaper price is favoring manufacturers to simulate & iterate a variety of materials to build functional prototypes for different applications. Also, companies are significantly investing in developing resilient service centers so that the consumers can avail the one-stop solution under one roof. The Japan market is projected to reach USD 83.64 million by 2026, the China market is projected to reach USD 130.27 million by 2026, and the India market is projected to reach USD 29.34 million by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 250.37 million in 2025, accounting for 28.30% share, and is expected to reach USD 296.06 million in 2026. In Europe, Germany is the key contributor to the market growth backed by increasing demand for rapid prototyping across automotive, electronics, consumer goods, and aerospace & military applications. A strong network of advanced prototyping service providers is the key driving factor for the growth of the Germany market. The country is also projected to register the fastest growth during the foreseeable period. Other countries, such as the U.K., France, and Italy, hold a prominent share of the market. Shifting consumer preference from traditional prototyping methods toward latest rapid prototyping services is estimated to increase the consumption of thermoplastics, metals, and composites in Europe. The UK market is projected to reach USD 52.35 million by 2026, while the Germany market is projected to reach USD 91.29 million by 2026.

Latin America and Middle East & Africa

The markets in Latin America and Middle East & Africa are at a preliminary stage and together hold the smallest share in the global market. However, with changing government policies & increasing public-private investment, the overall industrial & manufacturing sector is growing at faster rate. This, in turn, is projected to create lucrative growth opportunities for rapid prototyping materials in these regions. Brazil, Saudi Arabia, and South Africa are expected to indicate significant growth in the coming years.

Rest of World

Rest of World recorded a market size of USD 54.31 million in 2025, capturing 6.10% of the global market share, and is projected to reach USD 65.20 million in 2026.

To know how our report can help streamline your business, Speak to Analyst

List of Key Companies in Rapid Prototyping Materials Market

Leading Entities in the Industry are Developing New Material and Acquiring Smaller Companies

Key operating leaders are mainly investing in the development of advanced materials, which can be more efficiently used for rapid prototyping. Major players, such as 3D Systems Corporation, Arkema, Covestro, and Tethon 3D, are focusing on introducing next generation thermoplastics suitable for additive manufacturing, 3D printing and rapid prototyping.

Leading companies such as 3D Systems Corporation, Arkema, and Covestro are organically expanding their business by launching various innovative materials. A range of thermoplastics are being deployed by these companies, including PA6-66, polyurethane, and other formulations, to align their product portfolio with the expanding demand for advanced polymer resins for 3D printing technology. Such strategic activities are extending company’s expertise in rapid prototyping technology and consecutively impacting the market growth.

LIST OF KEY COMPANIES PROFILED

- Arkema S.A. (France)

- Stratasys, Ltd. (Israel)

- 3D Systems Corporation (U.S.)

- Covestro A.G. (Germany)

- EOS GmbH (Germany)

- CRP Technology S.r.l. (Italy)

- Oxford Performance Materials (U.S.)

- Materialise NV (Belgium)

- Tethon 3D (U.S.)

- 3DCeram (France)

- Nexa3D (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2022 – Stratasys Ltd., a polymer 3D printing solutions provider, launched 16 new materials for three different 3D printing technologies. The product portfolio was done to meet the growing demand from the use cases of 3D printing technologies.

- November 2021 – Covestro launched four new advanced materials for various 3D printing technologies: two materials for Fused Deposition Modeling and Fused Filament Fabrication (FDM/FFF) and Selective Laser Sintering (SLS), respectively, and two other materials for SLS and High-Speed Sintering (HSS).

- November 2021 – Arkema showcased custom UV-curable formulations for 3D printing technology at Formnext 2021 Exhibition held in Germany. The product portfolio includes formulations such as N3D-TOUGH 784, HT-511, DMT-303, IC-163, and LF-053. These formulations are strategically developed to meet the growing requirement of advanced polymer resins for 3D printing technology.

- September 2021 – 3D Systems Corporation expanded its material portfolio with the launch of certified Scalmalloy (A) and M789 (A). These materials will be used to develop high strength parts for energy, mold making, automotive, electronics, aerospace, and defense applications. Also, the consumers can use company’s Direct Metal Printing platform to develop parts with the help of Scalmalloy (A) and M789 (A).

- February 2021 - 3D Systems Corporation announced plans to develop its headquarter in South Carolina with advanced material development laboratories, training centers, customer centers and also advanced metal & polymer manufacturing facility.

REPORT COVERAGE

The global market research report provides both qualitative & quantitative insights of the market across the world. Quantitative insights include market sizing in terms of value (USD million) across each segment, sub-segment, and region profiled in the scope of study. Also, it provides market analysis and growth rates of segment, sub-segment, and key counties across each region. Qualitative insight covers elaborative analysis of key market drivers, restraints, growth opportunities, and global industry trends related to the market. Competitive landscape section covers detailed company profiling of the key players operating in the industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.2% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Material

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1053.78 million in 2026 and is projected to reach USD 3921.75 million by 2034.

Growing at a CAGR of 17.2%, the market will exhibit steady growth over the forecast period.

Thermoplastics segment is the leading material in the market.

Rapid product adoption in medical & aerospace industries is fueling the demand for rapid prototyping materials.

North America held the highest market share in 2026.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us