Remote Deposit Capture Market Size, Share & Industry Analysis, By Type (Hardware, Software, and Services), By Deployment Mode (On-Premise and Cloud-Based), End User (Financial Institutions and Businesses), and Regional Forecast, 2026 – 2034

Remote Deposit Capture Market Size and Future Outlook

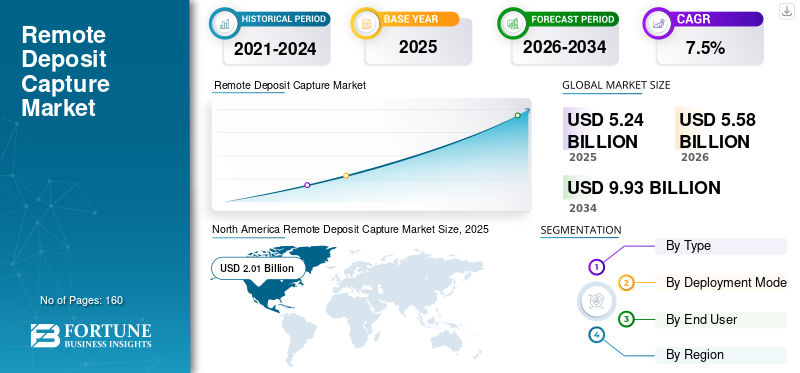

The global remote deposit capture market size was valued at USD 5.24 billion in 2025. The market is projected to grow from USD 5.58 billion in 2026 to USD 9.93 billion by 2034, exhibiting CAGR of 7.5% during the forecast period. North America dominated the remote deposit capture market with a market share of 38.36% in 2025.

Remote deposit capture market is an infrastructure-driven fintech market focused on digitizing check-based transactions. RDC allows business to convert physical checks to electronic images, making the process faster and efficient. Regular check-based payments, stringent regulatory standards, and minimal dependency on physical branches to drive the market demand for remote deposit capture. Increasing count of check frauds, and duplicate check deposits are driving the market demand for advanced image –based validation. Features such as mobile banking, banking at doorstep, digital payment adoption are all surging the market growth during the forecast period. Growing demand for SME banking services, further backed by regulatory policies to boost the market growth of remote deposit capture.

- For instance, in August 2024, Alogent partnered with Mitek to integrate its Check Fraud Defender into Alogent’s Unify platform.

Key players such as Fiserv, Inc., Fidelity National Information Services, Jack Henry & Associates, Inc., Mitek Systems Inc., are few of the key players in the market. Key players are focusing on mobile-first capture solutions, portable remote capture deposit, and adoption of cloud based deployment, to penetrate and gain market share.

Unprecedented geopolitical scenarios such as tariffs, volatile markets, etc. are all slightly impacting the hardware market of remote deposit capture. However, the market is subjected to witness strong growth during the forecast period owing to increasing number of small and medium scale enterprises

Download Free sample to learn more about this report.

REMOTE DEPOSIT CAPTURE MARKET TRENDS

Expansion of Merchant RDC and SME Business to Drive Market Demand

Small and medium sized enterprises are growing across emerging and mature economies. RDC adoption is diversifying across the small and medium enterprises owing to evolution of cloud-based platforms, mobile capture solutions, driving the demand for the market. RDC enables faster cash flow management, further increasing operational efficiency for the banks enabling the market demand for remote deposit capture solutions. Overall, this trend is transforming RDC from a high-value, low-volume enterprise solution into a scalable, volume-driven market, where growth is increasingly fueled by the long tail of SMEs rather than a few large corporate users.

- For example, in the U.S., small businesses account for over 40–50% of total check deposits in certain banking segments, prompting banks to expand merchant RDC offerings tailored to SMEs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Check Frauds and Secure Image-based Processing to Drive Market Growth

Check fraud has been resurging globally, particularly in the U.S., where checks remain widely used in B2B and institutional payments. Fraud risks in RDC environments include duplicate deposits (same check deposited multiple times), altered check amounts, forged signatures, and counterfeit checks. Since RDC relies on digital images rather than physical verification, banks must ensure that these images are authentic, unaltered, and compliant with regulatory standards. Additionally, regulatory bodies and banking associations have been urging institutions to strengthen controls around remote deposits, further driving demand for secure RDC solutions.

- For instance, in 2023, Mitek introduced advanced AI-powered mobile check deposit verification tools aimed at reducing fraud and improving image accuracy.

MARKET RESTRAINTS

Large Legacy Systems and Banking Infrastructure to Limit Market Growth

The high dependency on legacy banking infrastructure is a key restraint in the remote deposit capture market growth as these solutions must tightly integrate with existing bank systems such as core banking platforms, check clearing networks, and compliance frameworks. Many banks, especially in developed markets, still operate on decades-old IT systems that are complex, rigid, and difficult to modify. Integrating RDC into such environments requires significant customization, long deployment cycles, and high implementation costs.

MARKET OPPORTUNITIES

Expansion and Penetration into Emerging Market to Bring Huge Market Opportunities

Many emerging economies have a large base of SMEs and informal businesses, which are underserved by traditional banking but increasingly adopting digital tools. RDC can be positioned as part of a broader financial inclusion strategy, allowing these businesses to access faster deposit services without needing full-scale infrastructure. A relevant example is seen in Kenya and India, where banks and fintechs are integrating RDC-like capabilities within mobile banking platforms to complement existing payment systems. Although digital payments dominate, RDC serves as a bridge solution for transitioning legacy check-based processes into digital workflows.

MARKET CHALLENGES

Reducing Check Volumes Might Pose a Challenge for Market Growth

While check usage is gradually decreasing due to the rise of digital payments, it has not disappeared entirely, especially in sectors including B2B transactions, insurance, and government payments. This means banks still require RDC infrastructure to support existing workflows. However, vendors must continue investing in technology upgrades, security enhancements, and platform modernization, even though the long-term growth potential of the market is limited. This creates uncertainty around Return On Investment (ROI), as future demand may not justify continuous high spending.

Segmentation Analysis

By Type

Software Segment Dominated Market Owing to Adoption of Digital Banking Solutions

Based on type, the market is divided into hardware, software, and services. Hardware is further segmented into check scanners and portable scanners. Based on software, the market is further categorized into capture software, image recognition, fraud detection, deposit processing, and others.

The software segment dominated the remote deposit capture market share in 2025. As it forms the core functional layer enabling check digitization, validation, and processing. Solutions such as mobile capture software, image recognition, fraud detection, and deposit processing platforms are essential for banks to operationalize RDC services. With the increasing adoption of mobile banking and digital channels, financial institutions are investing heavily in software capabilities to enhance user experience, improve processing accuracy, and ensure regulatory compliance. As banks continue to modernize their digital infrastructure, software remains the primary revenue contributor and strategic focus area for RDC vendors.

The services segment is expected to witness the highest growth of about 8.5% CAGR during the forecast period, driven by the increasing need for implementation, integration, and managed services among financial institutions. As RDC solutions become more complex and cloud-based, banks require ongoing support for system deployment, customization, maintenance, and regulatory compliance, fueling demand for service offerings.

- For instance, in 2024, Finastra partnered with fintech providers to embed RDC functionality into its open banking platform. The strategy enables banks to deploy RDC faster via APIs, supporting digital ecosystem expansion.

To know how our report can help streamline your business, Speak to Analyst

By Deployment Mode

On-Premise Deployment Mode Dominate Market Owing to Huge Demand for In-house Infrastructure

Based on deployment mode, the market is segmented into on-premise and cloud-based.

The on-premise segment dominates the market as many financial institutions, particularly large banks, continue to rely on in-house infrastructure for greater control, security, and compliance management. RDC solutions involve sensitive financial data and image-based transactions, prompting banks to prefer on-premise deployments where they can directly manage data storage, fraud controls, and system access. Additionally, legacy banking environments are deeply integrated with existing on-premise systems, making it easier and more cost-effective to extend RDC capabilities within the same infrastructure rather than migrate to new platforms.

The cloud-based segment is expected to witness the highest growth rate of about 7.8% in the RDC market, driven by the increasing adoption of digital banking and scalable, cost-efficient deployment models. Cloud-based RDC solutions enable banks to reduce upfront infrastructure investments while benefiting from faster implementation, flexibility, and automatic updates.

By End User

Financial Institutions being the Primary Purchaser Dominates the Remote Deposit Capture Market

Based on end user, the market is segmented into financial institutions and businesses. Financial institutions are further categorized as commercial banks, retail banks, credit unions, and others. Businesses are further categorized as large corporations and SMEs.

The financial institutions segment dominates the market as banks, credit unions, and other financial entities are the primary purchasers and deployers of RDC solutions. These institutions invest heavily in RDC platforms, mobile capture software, fraud detection systems, and integration services to enable remote deposit capabilities for both retail and business customers. The dominance of this segment is driven by the need to enhance customer experience, reduce branch dependency, and optimize operational costs associated with manual check processing.

The businesses segment is expected to witness the highest growth of about 8.1% CAGR during the projected period, driven by increasing adoption among Small and Medium Enterprises (SMEs) and distributed business networks. The growing availability of low-cost, mobile-based RDC solutions and simplified merchant portals has significantly lowered the entry barriers, enabling wider adoption among smaller businesses.

Remote Deposit Capture Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Remote Deposit Capture Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the RDC market, primarily driven by the continued high usage of checks, especially in the U.S., for B2B, insurance, and government payments. The presence of enabling regulations, including the Check 21 Act, has created a mature ecosystem for image-based check processing. Banks in this region are heavily investing in advanced RDC software, mobile capture, and AI-driven fraud detection, making it the most technologically evolved market. The region is also witnessing increased focus on enhancing security and reducing fraud risks, further driving innovation. Overall, North America represents a mature, innovation-led market with high software penetration.

U.S. Remote Deposit Capture Market

The U.S. represents the dominant market in the North America region. The U.S. market will reach a value of USD 1.73 billion in 2026, representing roughly 31% of global revenues. The U.S. banks have extensively deployed mobile RDC and merchant RDC solutions, making remote deposit a standard feature across retail and business banking platforms.

Europe

The Europe market is relatively moderate compared to North America due to lower reliance on checks and higher adoption of digital payment methods such as SEPA and instant transfers. However, demand persists in specific sectors including corporate banking and cross-border transactions, where checks are still used. A key driver in this region is the push toward digital banking transformation and regulatory compliance, encouraging banks to adopt RDC as part of broader digital solutions. Europe is also witnessing a strong trend toward cloud-based deployments and fintech integration, particularly in the U.K. and Germany.

U.K. Remote Deposit Capture Market

The U.K. market will reach a value of USD 0.30 billion in 2026, representing roughly 5.4% of global market revenues.

Germany Remote Deposit Capture Market

Germany’s market will reach USD 0.32 billion in 2026, equivalent to around 5.8% of the global sales.

Asia Pacific

Asia Pacific is the fastest-growing RDC market, driven by rapid banking digitization, SME expansion, and increasing financial inclusion initiatives. Although check usage is lower in some countries due to the dominance of digital payments, RDC is gaining traction in enterprise transactions and government-related payments. The region presents significant opportunities due to its large base of underserved SMEs, which are increasingly adopting mobile-based and low-cost RDC solutions. A key trend is the emergence of hybrid banking models, where RDC complements mobile and agent banking systems. India and ASEAN nations are witnessing growth through mobile-first deployments, reducing reliance on physical scanners.

India Remote Deposit Capture Market

The Indian market will be valued at USD 0.21 billion in 2026, accounting for roughly 3.8% of the global market. Supportive government-led startup initiatives and increasing digital consumer base to propel the market growth in India.

China Remote Deposit Capture Market

China’s market is projected to remain dominant in the Asia Pacific region in 2026 with revenues reaching USD 0.50 billion, representing roughly 8.9% of global sales.

Japan Remote Deposit Capture Market

The Japan market will reach a value of USD 0.26 billion in 2026, accounting for roughly 4.6% of revenue.

South America

The South America market is driven by growing fintech ecosystems, increasing SME activity, and gradual banking digitization, particularly in Brazil. While digital payments are expanding, checks continue to play a role in business and institutional transactions, sustaining demand for RDC solutions. A key driver is the need for operational efficiency and faster cash flow management among businesses, especially SMEs. The region is witnessing a trend toward mobile-based RDC adoption and simplified merchant solutions, as cost sensitivity limits large-scale hardware deployment.

Brazil Remote Deposit Capture Market

The Brazil market will reach USD 0.24 billion in 2026, representing roughly 4.4% of the global market

Middle East & Africa

The Middle East & Africa market is an emerging stage, characterized by gradual adoption of digital banking and ongoing financial infrastructure development. Key growth drivers include government-led digitization initiatives, increasing banking penetration, and SME growth. The GCC countries, in particular, are leading adoption due to their advanced banking systems and enterprise activity. A notable trend is the integration of RDC with mobile and agent banking models, allowing banks to extend services to remote areas. However, adoption remains constrained by price sensitivity and limited check usage in certain regions.

GCC Remote Deposit Capture Market

The GCC market will reach USD 0.14 billion in 2026, representing roughly 2.5% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Mobile Capture Technology to Propel Market Penetration

Key players in the market are embedding RDC into digital banking platforms, enhancing mobile capture technology, and platform-based revenue models. Rising demand for fraud prevention and detection to further boost the market demand across emerging market including small and medium sized enterprises. Key players are targeting SMEs to diversify their revenue generation through partnerships and collaborations.

- For instance, in 2024, ProgressSoft expanded RDC deployments across Middle Eastern banks, integrating check digitization with national payment systems.

LIST OF KEY REMOTE DEPOSIT CAPTURE MARKET COMPANIES PROFILED IN REPORT

- Fiserv, Inc. (U.S.)

- Fidelity National Information Services (FIS) (U.S.)

- Jack Henry & Associates, Inc. (U.S.)

- Mitek Systems, Inc. (U.S.)

- NCR Corporation (U.S.)

- Bottomline Technologies (U.S.)

- Panini S.p.A. (Italy)

- Digital Check Corp. (U.S.)

- Canon Inc. (Japan)

- Finastra (U.K.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Corporate One Federal Credit Union released updated RDC operational guidance and risk frameworks for credit unions, emphasizing fraud mitigation and audit controls.

- August 2025: First Bank implemented a major RDC software upgrade across its commercial banking platform, including scanner compatibility and system performance enhancements.

- July 2025: Oregon State Treasury expanded the use of RDC systems for public sector financial operations, enabling agencies to digitize check deposits via secure scanning infrastructure.

- May 2024: Apiture enhanced its digital banking platform with improved RDC features, including faster funds availability and advanced fraud analytics.

- September 2023: Ingo Money partnered with banks and fintech platforms to enable instant check cashing via RDC-enabled mobile applications.

REPORT COVERAGE

The global remote deposit capture market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Deployment Mode, End User, and Region |

| By Type |

|

| By Deployment Mode |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value to stand at USD 5.58 billion in 2026 and is projected to reach USD 9.93 billion by 2034.

In 2025, the North Americas market value stood at USD 2.01 billion.

The market is expected to exhibit a CAGR of 7.5% during the forecast period of 2026-2034.

By type, the software segment leads the market.

Rising check frauds and secure image-based processing are driving the market growth.

Fiserv Inc., Jack Henry & Associates, and Mitek Systems, Inc., are the top players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us