Rigid Box Market Size, Share & Industry Analysis, By Material (Paper & Paperboard, Wood, Plastic, and Others), By Product Type (Slotted Box, Die Cut Box, Telescope Box, Folder Box, and Others), By End Use (Food & Beverages, Personal Care & Cosmetics, Electronics & Electricals, Healthcare, and Others), and Regional Forecast, 2026-2034

Rigid Box Market Size and Future Outlook

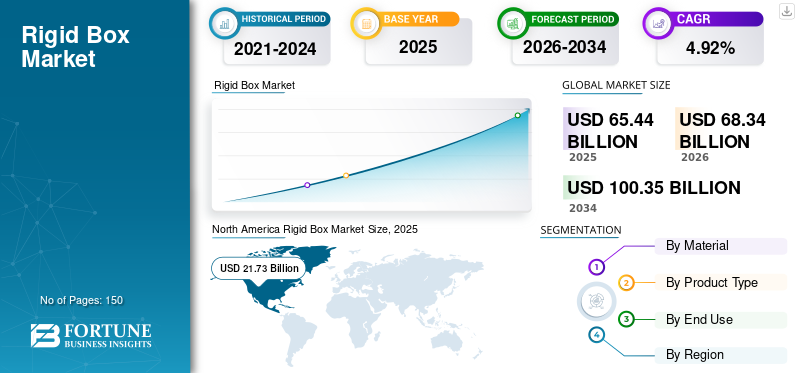

The rigid box market size was valued at USD 65.44 billion in 2025. The market is projected to grow from USD 68.34 billion in 2026 to USD 100.35 billion by 2034, exhibiting a CAGR of 4.92% during the forecast period. North America dominated the rigid box market with a market share of 33.21% in 2025.

The market represents the sector that produces and distributes high-quality, non-collapsible packaging solutions. These are generally made from thick chipboard and used for luxury items, electronics, cosmetics, confectionery, and gift packaging, owing to their robustness and premium aesthetic. The increasing demand for high-quality, sustainable packaging in the luxury, cosmetics, and electronics industries is driving market growth. Brands are increasingly using rigid boxes to enhance product display, protect products, and improve overall consumer experience.

Furthermore, many key industry players, such as Smurfit Kappa, DS Smith, and International Paper, operating in the market, are focusing on developing innovative products and conducting R&D activities.

Download Free sample to learn more about this report.

RIGID BOX MARKET TRENDS

Premiumization and Sustainable Packaging Integration Are Prominent Market Trends

A significant trend influencing the market is the inclusion of premiumization with sustainability. Brands are increasingly using rigid boxes crafted from recycled paperboard, biodegradable materials, and environmental friendly inks, while preserving a luxurious aesthetic appeal. Furthermore, innovations in digital printing and embossing technologies are facilitating enhanced customization and shorter production runs. This trend is further strengthened by increasing consumer awareness of environmental impacts, encouraging manufacturers to reconcile structural strength with reduced material consumption and enhanced recyclability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth in Luxury and Gift Packaging Demand is Driving Market Growth

The growing demand for luxury products and high-end gifting options significantly propels the rigid box market growth. Prominent brands across industries including fashion, jewelry, electronics, and gourmet foods rely on rigid boxes to strengthen brand identity and enhance the unboxing experience. The swift expansion of e-commerce and direct-to-consumer channels has further heightened the importance of sturdy, aesthetically pleasing packaging. As consumers increasingly associate packaging quality with product value, rigid boxes are emerging as a favored option for differentiation and brand positioning.

MARKET RESTRAINTS

High Production and Material Costs Hampers Market Expansion

One of the main limitations in the market is high cost associated with production and raw materials. In contrast, flexible or folding carton packaging results in increased manufacturing costs and extended production schedules. Small and medium-sized enterprises may struggle to implement rigid packaging due to financial constraints. Moreover, variations in raw material costs, especially for paperboard and adhesives, can further affect profitability and pricing strategies, hindering widespread adoption of the product.

MARKET OPPORTUNITIES

Expansion in E-commerce and Direct-to-Consumer Channels Offers Potential Growth Opportunities

The swift growth of e-commerce and direct-to-consumer (D2C) business models offers considerable prospects for the market. Companies are placing greater emphasis on providing a remarkable unboxing experience to enhance customer engagement and foster brand loyalty. Subscription box services, product launches driven by influencers, and packaging formats exclusive to online sales are additional factors driving product demand. Moreover, improvements in logistics and packaging optimization are facilitating the creation of lighter, more cost-effective rigid boxes, thereby increasing their suitability for online retail across various product categories.

MARKET CHALLENGES

Balancing Sustainability with Cost and Performance Poses a Critical Challenge to Market Growth

A significant challenge limiting market is balancing sustainability goals with the demands of cost efficiency and performance. Although there is considerable pressure from both regulators and consumers to use eco-friendly materials, sustainable options often entail higher costs or may compromise structural integrity. Manufacturers are required to invest in research and development to devise innovative solutions that comply with environmental standards while maintaining durability and aesthetics. Additionally, securing a consistent supply of certified sustainable raw materials can be challenging, particularly in developing regions. This issue requires ongoing innovation, supply chain optimization, and collaboration among stakeholders to ensure long-term market competitiveness.

Segmentation Analysis

By Material

Sustainability, Cost Efficiency, and Structural Strength of Paper & Paperboard Segment Drives its Dominance

Based on the material, the market is divided into paper & paperboard, wood, plastic, and others.

The paper & paperboard segment is expected to account for the largest rigid box market share over the forecast period. These materials are readily accessible, recyclable, and increasingly sourced from certified sustainable forestry, in line with rising environmental regulations and consumer preferences. Furthermore, paperboard offers excellent printability and finishing options, enabling high-quality branding through techniques such as embossing, foiling, and lamination. Compared to other materials, it also enables greater customization and scalability in manufacturing, making it the preferred option in luxury, retail, and e-commerce packaging.

The wood segment is expected to grow at a CAGR of 4.98% over the forecast period.

By Product Type

Design Simplicity, Material Efficiency, and Operational Convenience Leads to Slotted Box Segment Growth

Based on product type, the market is segmented into slotted box, die cut box, telescope box, folder box, and others.

In 2025, the slotted box segment dominated the global market. This is due to its simple design, efficient material use, and ease of production. Its structure facilitates rapid assembly, compatibility with automated packaging systems, and efficient flat storage, which reduces logistics expenses. Additionally, slotted boxes offer sizing flexibility and can hold a diverse array of products, making them suitable for sectors including e-commerce, retail, and industrial packaging. This blend of cost efficiency and operational effectiveness underpins their global prevalence.

The die cut box segment is projected to grow at a CAGR of 5.02% over the forecast period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

High Consumption Volume, Gifting Culture, and Premium Packaging Needs Drive the Dominance of the Food & Beverages Segment

Based on the end use, the market is segmented into food & beverages, personal care & cosmetics, electronics & electricals, healthcare, and others.

The food & beverages segment is expected to hold a dominant market share over the forecast period. This is primarily due to its large consumer base and strong demand for attractive, product protection. The seasonal demand, influenced by festivals, corporate gifting, and special events, further boosts usage, particularly for high-end and customized packaging options. Moreover, the growing consumer preference for premium, hygienic packaging has prompted brands to embrace rigid boxes. Their capacity to enhance branding, guarantee product safety, and deliver an improved unboxing experience, strengthening their widespread use in this sector.

The personal care & cosmetics segment is projected to grow at a CAGR of 4.48% over the forecast period.

Rigid Box Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Rigid Box Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 20.82 billion, and maintained its leading position in 2025, at USD 21.73 billion. In North America, the market is driven by robust demand for high-quality packaging for luxury goods, cosmetics, and electronics. The well-established e-commerce landscape underscores the importance of durable, visually appealing packaging to enhance unboxing experiences, while sustainability regulations encourage the use of recyclable, responsibly sourced paperboard.

U.S Rigid Box Market

Based on North America's strong contribution, the U.S. market reached USD 17.45 billion in 2025, accounting for 26.67% of global sales. The market benefits from sophisticated retail networks, robust brand competition, and heightened consumer demand for packaging quality. Businesses are increasingly allocating resources to innovative, sustainable rigid packaging solutions to improve brand differentiation, especially in subscription services, electronics, and premium food sectors.

Europe

Europe is projected to grow at 4.50% over the coming years, the third-highest among regions, and reached a valuation of USD 11.71 billion in 2025. Stringent environmental regulations and heightened consumer awareness of sustainable packaging influence the market in Europe. The robust luxury goods industry in the region, especially in cosmetics, fashion, and confectionery, drives demand for high-quality, recyclable rigid boxes as brands emphasize minimalist yet premium packaging designs.

U.K Rigid Box Market

The U.K. market in 2025 was at USD 2.12 billion, representing 3.23% of global revenues.

Germany Rigid Box Market

Germany's market reached approximately USD 2.48 billion in 2025, equivalent to 3.79% of global sales.

Asia Pacific

Asia Pacific is reached USD 18.61 billion in 2025 and secured second place in the market. The Asia Pacific market growth is driven by rising disposable incomes, a burgeoning middle class, and heightened demand for premium packaged products. Nations including China and India are experiencing significant growth in e-commerce and a culture of gifting, driving demand for affordable yet aesthetically pleasing rigid packaging options.

Japan Rigid Box Market

The Japanese market in 2025 was at USD 3.54 billion, accounting for 5.41% of global revenues. Japan's market growth is propelled by its deep-rooted culture of premium gifting and stringent packaging standards. A keen focus on detail, product presentation, and quality drives demand for aesthetically pleasing, structurally sound rigid boxes, especially in the confectionery, electronics, and traditional gift sectors.

China Rigid Box Market

China's market is growing rapidly with 2025 revenue at USD 5.99 billion, representing 9.15% of global sales.

India Rigid Box Market

The Indian market in 2025 was at USD 5.03 billion, accounting for 7.68% of global revenue.

Latin America

The Latin America region is expected to witness moderate growth during the forecast period. The market reached a valuation of USD 7.14 billion in 2025. The rise in urbanization and the growth of organized retail are driving demand for rigid boxes, especially in food, beverages, and personal care sector across the region. The growing interest in premium packaging for gifting and branding is driving a gradual market expansion.

Middle East & Africa

In the Middle East & Africa, South Africa reached USD 1.78 billion in 2025. The growth of the Middle East & Africa market is driven by rising luxury consumption, particularly in Gulf nations, with the development of contemporary retail infrastructure. There is substantial demand for upscale packaging across perfumes, confectionery, and gifting sector, while the rise in tourism and premium retail experiences also fosters the adoption of rigid boxes.

Saudi Arabia Rigid Box Market

The Saudi Arabian market reached USD 2.01 billion in 2025, accounting for 3.07% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Competition

The global market has a semi-consolidated structure, with prominent players including Smurfit Kappa, DS Smith, and International Paper operating in it. The significant market shares of these packaging companies are due to their numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in February 2026, Smurfit Kappa announced the expansion of its premium rigid packaging portfolio with the introduction of a new collection of fully recyclable rigid gift boxes aimed at luxury retail and e-commerce brands. The company has incorporated advanced water-based coatings and plastic-free lamination technologies to improve sustainability while preserving a high-quality finish.

Other notable players in the market include Mondi, Stora Enso, and Packaging Corporation of America. These companies are expected to prioritize new product launches, strategic partnerships, and collaborations to increase their global market shares during the forecast period.

LIST OF KEY RIGID BOX COMPANIES PROFILED

- Smurfit Kappa (Ireland)

- DS Smith (U.K.)

- International Paper (U.S.)

- Mondi (U.K.)

- Stora Enso (Finland)

- Packaging Corporation of America (U.S.)

- Graphic Packaging International, LLC (U.S.)

- The Pack America Corp. (U.S.)

- Robinson Plc (U.K.)

- Wynalda Packaging (U.S.)

- Infinity Packaging Solutions (UAE)

- Max Bright Packaging Ltd. (China)

- Refine Packaging (U.S.)

- Polipak (Poland)

- TPC Packaging (Australia)

KEY INDUSTRY DEVELOPMENTS

- October 2025: DS Smith has launched a new range of circular-ready rigid packaging solutions tailored for high-value consumer goods and e-commerce uses. The company has prioritized optimizing material use while maintaining structural integrity, enabling brands to minimize packaging waste without sacrificing durability.

- July 2025: Mondi has enhanced its premium packaging operations in Eastern Europe by modernizing its converting facilities to incorporate rigid box manufacturing capabilities. This investment is intended to meet the increasing regional demand for luxury packaging in the cosmetics, confectionery, and personal care industries.

- March 2025: Stora Enso has introduced a groundbreaking rigid packaging solution utilizing its renewable fiber-based materials, aimed at the luxury and electronics packaging sectors. This product highlights reduced carbon footprint and recyclability, while preserving the structural integrity required for rigid boxes. Additionally, the company has partnered with high-end brands to develop packaging designs aligned with sustainability objectives jointly.

- November 2024: International Paper enhanced its premium packaging capabilities by making a strategic investment in converting technologies focused on rigid and specialty boxes. The company improved certain North American facilities to accommodate higher-value packaging formats, such as gift and presentation boxes.

- June 2024: Graphic Packaging International has introduced a new range of rigid paperboard packaging solutions, aimed at replacing plastic-based premium packaging. These solutions emphasize recyclability, lightweight design, and superior print finishes, catering to industries such as food, beverages, and personal care.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, along with their prevalence by region. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.92% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, Product Type, End Use, and Region |

| By Material |

|

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 65.44 billion in 2025 and is projected to reach USD 100.35 billion by 2034.

In 2025, the North America market value stood at USD 21.73 billion.

The market is expected to grow at a CAGR of 4.92% over the forecast period of 2026-2034.

By material, the paper and paperboard segment is expected to lead the market.

Growth in luxury and gift packaging demand is driving market growth.

Smurfit Kappa, DS Smith, and International Paper are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us