Robotic Refueling System Market Size, Share & Industry Analysis, By Fuel Pumped (Gasoline, Natural Gas, and Petrochemicals), By Payload-carrying capacity (Up to 50 kg, 50–100 kg, and above 100kg), By Application (Automotive & Commercial Vehicle Fleets, Mining & Construction Equipment, Oil & Gas, Aviation, and Others), and Regional Forecast, 2026 – 2034

KEY MARKET INSIGHTS

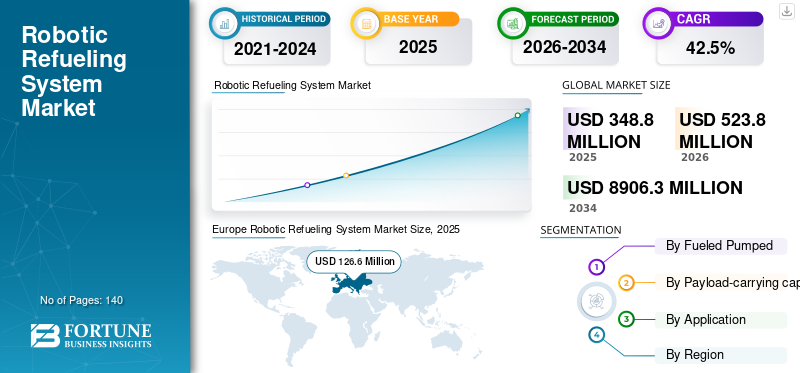

The global robotic refueling system market size was valued at USD 348.8 million in 2025. The market is projected to grow from USD 523.8 million in 2026 to USD 8,906.3 million by 2034, exhibiting a CAGR of 42.5% during the forecast period. Europe dominated the global robotic refueling system market with a market share of 36.29% in 2025.

Robotic refueling comprises automated and semi-autonomous systems designed to perform refueling operations without direct human intervention, primarily across industrial, commercial, mining, aviation, and fleet applications.

The global market is witnessing steady growth, driven by rising automation across industrial operations, increasing emphasis on workforce safety, and the need to minimize downtime in high-value assets. Robotic refueling systems are gaining traction in environments where manual refueling is risky, time-consuming, or operationally inefficient, such as mining sites, oil & gas facilities, and large vehicle fleets.

Moreover, companies like ABB Ltd., KUKA AG, FANUC Corporation, and Sandvik AB are putting more and more emphasis on robotics, automation, and autonomous operations which can support or be integrated into refueling-related tasks within large automated ecosystems. By investing in industrial robotics and autonomous systems, they are expected to support the growth of the market both indirectly and directly.

- To give an example, in May 2024, Sandvik AB increased and enriched its AutoMine automation portfolio with the focus on completely autonomous mining operations where automated service functions, like fueling and maintenance, are becoming more important for non-stop operations.

Download Free sample to learn more about this report.

ROBOTIC REFUELING SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 348.8 million

- 2026 Market Size: USD 523.8 million

- 2034 Forecast Market Size: USD 8,906.3 million

- CAGR: 42.50% from 2026–2034

- Asia Pacific dominated the global market with a share of 32.82% in 2025.

- The natural gas segment is expected to grow at the highest CAGR of 44.9% over the forecast period.

- The above 100 kg segment is projected to register the highest CAGR of 46.3%.

North America

North America represents a significant share of the global market due to early adoption of automation technologies across mining, oil & gas, aviation, and commercial fleet operations.

Europe

Europe holds the highest global robotic refueling market share due to strong industrial automation adoption, advanced manufacturing capabilities.

Asia Pacific

Asia Pacific is expected to register the highest CAGR during the forecast period, driven by rapid industrialization.

U.S.

The U.S. market is estimated to bet around USD 99.2 million in 2026

Japan

Japan’s market is projected to reach USD 29.0 million in 2026, driven by advanced robotics adoption, strong focus on autonomous systems, and continuous innovation in industrial automation technologies.

Read More

ROBOTIC REFUELING SYSTEM MARKET TRENDS

Increasing Adoption of Autonomous Operations in Hazardous Environments is a Key Market Trend

Industries operating in hazardous and remote environments are increasingly adopting autonomous and robotic solutions to improve efficiency and safety. Mining, oil & gas, and heavy industrial sectors are deploying automation to reduce human exposure to flammable fuels, extreme temperatures, and unsafe terrain, creating a favorable environment for robotic refueling systems.

In addition, the growing integration of robotic refueling within broader autonomous ecosystems such as unmanned vehicles, automated depots, and smart mining operations—is strengthening demand. These systems enable continuous operations, reduce downtime, and support centralized control of refueling processes, particularly in large-scale industrial sites.

- For instance, ABB Ltd. projected that the need for autonomous robotic solutions in heavy industries such as mining and energy would rise significantly in 2025 thus, facilitating greater use of robotic service systems in extreme conditions by introducing the demand of such solutions as a segment of its industrial automation strategy.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Focus on Workforce Safety and Operational Automation to Drive Market Growth

Growing emphasis on workforce safety is a major driver for the robotic refueling market growth. Manual refueling activities expose workers to fire hazards, fuel leaks, toxic fumes, and mechanical risks, particularly in mining and industrial environments. Robotic refueling systems significantly reduce these risks by minimizing direct human involvement.

Additionally, industries are adopting automation to improve asset utilization and reduce labor dependency. Automated refueling supports round-the-clock operations, ensures consistent fueling accuracy, and aligns with the broader shift toward autonomous industrial workflows, thereby accelerating market adoption.

- To illustrate, the International Council on Mining and Metals (ICMM) in 2024, listed automation as the top facilitator in terms of safety and productivity enhancement across mining operations, thereby endorsing the rise in use of robotic service systems.

MARKET RESTRAINTS

High Capital Investment and System Integration Complexity to Restrict Market Growth

High initial capital costs associated with robotic refueling systems remain a key restraint, particularly for small and mid-sized operators. These systems require advanced robotics, precision sensors, control software, and compatibility with existing fuel infrastructure, resulting in significant upfront expenditure.

Moreover, integrating robotic refueling system with legacy equipment and diverse fuel standards can be technically complex. Customization requirements, extended commissioning timelines, and the need for skilled personnel may slow the adoption in cost-sensitive or technologically constrained environments.

- To illustrate, McKinsey & Company stated in 2024 that heavy industries are facing the significant barrier of high initial costs as well as the difficulties of integration which hinder the adoption of industrial robotics.

MARKET OPPORTUNITIES

Expansion of Autonomous Fleets and Alternative Fuel Adoption to Create Market Opportunities

As human intervention is reduced in autonomous environments, automated fueling solutions become essential to maintain uninterrupted operations. The rapid expansion of autonomous vehicle fleets across logistics, mining, and industrial operations presents significant growth opportunities for robotic refueling systems.

Furthermore, increasing adoption of alternative fuels such as natural gas and hydrogen is creating demand for specialized robotic refueling technologies. These fuels often require stricter handling and safety protocols, making robotic systems an attractive solution for fleet operators transitioning to cleaner energy sources.

- For instance, in 2025, logistics operators in Europe made public trials of totally self-driving and less pollutant vehicle fleets, thus underlining the increasing demand for refueling infrastructure that operates on its own.

Segmentation Analysis

By Fuel Pumped

High Demand from Existing Fuel Infrastructure Drives Gasoline Segment’s Dominance

Based on fuel pumped, the market is segmented into gasoline, natural gas, and petrochemicals.

The gasoline segment holds the highest market share, driven by its widespread use across automotive and commercial vehicle fleets. Existing fueling infrastructure and high fleet penetration support the strong demand for robotic refueling system which are compatible with gasoline operations.

- For instance, European logistics hubs continue to prioritize automation in conventional fueling operations, supporting gasoline-based robotic refueling deployments.

The natural gas segment is expected to grow at the highest CAGR of 44.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Payload-Carrying Capacity

Requirement for Precision Handling Drives The Leadership of Up to 50 kg Segment

Based on payload-carrying capacity, the market is segmented into up to 50 kg, 50–100 kg, and above 100 kg.

Up to 50 kg segment is taking the lead, since the majority of refueling robots are made for precision handling instead of heavy lifting. These systems are used at fleet depots, in various industries, and in restricted operational areas.

- For instance, industrial robotics suppliers such as FANUC and KUKA continue to expand lightweight robotic platforms, supporting high adoption of lower-payload refueling systems.

The above 100 kg segment is projected to register the highest CAGR of 46.3%.

By Application

High Fleet Density and Refueling Frequency Strengthens the Automotive & Commercial Vehicle Fleets’ Dominance

Based on application, the market is segmented into automotive & commercial vehicle fleets, mining & construction equipment, oil & gas, aviation, and others.

The automotive & commercial vehicle fleets segment holds the highest market share, driven by high refueling frequency, centralized depot operations, and growing automation in logistics and transportation.

- For instance, in 2024, European commercial fleet operators increased investments in automated depot technologies, indirectly supporting robotic refueling adoption.

The mining & construction equipment segment is projected to grow at the highest CAGR of 45.3%.

Robotic Refueling System Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and Middle East & Africa.

Europe

Europe Robotic Refueling System Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe holds the highest global robotic refueling market share due to strong industrial automation adoption, advanced manufacturing capabilities, and early deployment of autonomous solutions across logistics, mining, and industrial operations. The region benefits from stringent workplace safety regulations and sustainability initiatives, which are encouraging the replacement of manual fueling with automated systems. Additionally, Europe’s leadership in industrial robotics and autonomous vehicle testing environments supports early commercialization of robotic refueling technologies for multiple applications.

U.K. Robotic Refueling System Market

The U.K. market in 2026 is estimated to be around USD 34.3 million, representing approximately 6.5% of global market revenues. Market growth is supported by increasing automation in logistics fleets, infrastructure projects, and mining-related operations, along with rising focus on workforce safety and operational efficiency.

Germany Robotic Refueling System Market

Germany’s market in 2026 is estimated at around USD 37.1 million, accounting for approximately 7.1% of global revenues, driven by strong industrial robotics penetration, automotive automation leadership, and investments in autonomous industrial systems.

North America

North America represents a significant share of the global market due to early adoption of automation technologies across mining, oil & gas, aviation, and commercial fleet operations. The region is characterized by strong investments in autonomous vehicles, industrial robotics, and digital infrastructure aimed at improving productivity and safety. Growing labor shortages and increasing regulatory emphasis on workplace safety further support adoption of robotic-refueling systems across industrial and fleet-based applications.

U.S. Robotic Refueling System Market

The U.S. market is estimated to bet around USD 99.2 million in 2026, accounting for approximately 18.9% of global revenues. Growth is driven by automation in mining and oil & gas operations, increasing deployment of autonomous commercial fleets, and strong presence of industrial robotics and automation solution providers.

Asia Pacific

Asia Pacific is expected to register the highest CAGR during the forecast period, driven by rapid industrialization, large-scale infrastructure development, and expanding mining and construction activities. Governments and industries across the region have increasingly adopted automation to improve safety, productivity, and operational continuity in hazardous environments. Rising investments and smart industrial facilities further strengthen demand for robotic refueling solutions.

Japan Robotic Refueling System Market

Japan’s market is projected to reach USD 29.0 million in 2026, driven by advanced robotics adoption, strong focus on autonomous systems, and continuous innovation in industrial automation technologies.

China Robotic Refueling System Market

China’s market in 2026 is estimated at around USD 66.9 million, representing approximately 12.8% of global revenues, supported by large-scale industrial automation, mining expansion, and logistics modernization initiatives.

India Robotic Refueling System Market

The India market in 2026 is estimated at around USD 31.4 million, accounting for approximately 6.0% of global revenues. Growth is supported by infrastructure development, mining expansion, and increasing adoption of automation technologies across construction and industrial sectors.

South America and Middle East & Africa

South America and the Middle East & Africa are expected to witness moderate growth during the forecast period. In these regions, expanding mining activities, oil & gas investments, and gradual adoption of industrial automation are supporting market development. Safety concerns in hazardous operational environments and increasing interest in autonomous operations are encouraging adoption of robotic service systems, including refueling solutions, particularly in large-scale industrial projects.

GCC Robotic Refueling System Market

The GCC market in 2026 is estimated at around USD 14.4 million, representing approximately 2.7% of global revenues. Market growth is driven by automation adoption across oil & gas operations, mining activities, and large infrastructure projects, along with rising emphasis on workforce safety and operational efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Expansion of Industrial Robotics and Autonomous Systems Strengthens Competitive Positioning

The global robotic-refueling system market is characterized by a developing competitive landscape, with major robotics and automation players focusing on autonomous operations, industrial safety, research and development and smart service robotics. Companies are leveraging expertise in industrial robotics, AI, and system integration to address emerging refueling automation needs.

- For instance, in 2024, KUKA AG emphasized expansion of robotic automation solutions for heavy-industry and logistics applications, supporting downstream adoption of robotic service systems.

LIST OF KEY ROBOTIC REFUELING SYSTEM COMPANIES PROFILED

- ABB Ltd. (Switzerland)

- KUKA AG (Germany)

- FANUC Corporation (Japan)

- Sandvik AB (Sweden)

- Komatsu Ltd. (Japan)

- Hitachi Construction Machinery (Japan)

- Airbus SE (Netherlands)

- Rotec Engineering B.V. (Netherlands)

- Fuelmatics AB (Sweden)

- Liebherr Group (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Sandvik AB made the announcement of their continued incorporation of AutoMine solutions into mines that use heavy machinery. These mining practices will be fully autonomous, with the service functions like fueling and maintenance being automatically performed more and more in order to keep the operations going without interruption.

- January 2025: Komatsu Ltd. mining companies already using the company’s Autonomous Haulage System (AHS) will have the possibility of integrating the robotic refueling, that are required for large-scale mining. At the same time, there will be an end-to-end automation of heavy equipment operations to the point that it is referred to as demand for the automated support systems.

- October 2024: Liebherr Group showcased advanced autonomous and semi-autonomous construction and mining equipment solutions at major international industry exhibitions, highlighting the growing role of automation in equipment servicing and fuel handling in heavy-duty applications.

- July 2024: ABB Ltd. revealed plans to invest USD 170 million in the expansion of its U.S. manufacturing and automation. This expansion is aimed at increasing the production capacity for the robotics, electrification, and industrial automation technologies supporting autonomous industrial operations that the company has chosen to focus on.

- March 2024: KUKA AG introduced new heavy-payload industrial robotic systems designed for harsh and outdoor industrial environments, supporting increased use of robotic solutions for servicing tasks including refueling in logistics, construction, and industrial operations.

REPORT COVERAGE

The global robotic refueling system market analysis includes a comprehensive study of market size & forecast across all key segments included in the report. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence physiotherapy equipment market growth over the forecast period. The report also covers technological advancements, product innovation, regulatory considerations, and key strategic developments such as partnerships and acquisitions. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 42.5% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Fuel Pumped, Product, Payload-carrying capacity, Application, and Region |

|

By Fuel Pumped |

· Gasoline · Natural Gas · Petrochemicals |

|

By Payload-carrying capacity |

· Up to 50 kg · 50–100 kg · Above 100kg |

|

By Application |

· Automotive & Commercial Vehicle Fleets · Mining & Construction Equipment · Oil & Gas · Aviation · Others |

|

By Region |

· North America (By Fuel Pumped, Product, Payload-carrying capacity, Application and Country) o U.S. (By Fuel Pumped) o Canada (By Fuel Pumped) o Mexico (By Fuel Pumped) · Europe (By Fuel Pumped, Product, Payload-carrying capacity, Application and Country) o Germany (By Fuel Pumped) o U.K. (By Fuel Pumped) o France (By Fuel Pumped) o Italy (By Fuel Pumped) o Spain (By Fuel Pumped) o Rest of Europe · Asia Pacific (By Fuel Pumped, Product, Payload-carrying capacity, Application and Country) o China (By Fuel Pumped) o Japan (By Fuel Pumped) o India (By Fuel Pumped) o South Korea (By Fuel Pumped) o Rest of Asia Pacific · South America (By Fuel Pumped, Product, Payload-carrying capacity, Application and Country) o Brazil (By Fuel Pumped) o Argentina (By Fuel Pumped) o Rest of South America · Middle East & Africa (By Product, Application, End User, and Country) o GCC (By Fuel Pumped) o South Africa (By Fuel Pumped) o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 348.8 million in 2025 and is projected to reach USD 8,906.3 million by 2034.

In 2025, the market value stood at USD 126.6 million.

The market is expected to exhibit a CAGR of 42.5% during the forecast period.

By application, the automotive & commercial vehicle fleets segment is expected to lead the market.

Rising focus on workforce safety and operational automation is a key factor driving the market growth.

ABB Ltd., KUKA AG, FANUC Corporation, Sandvik AB, and Komatsu Ltd. are among the major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us