Robotics System Integration Services Market Size, Share & Industry Analysis, By Service Type (System Design & Engineering, Robotic Cell Integration, Programming & Simulation Services, Installation & Commissioning, Maintenance and Support Services, and Training & Consulting Services), By Robot Type (Articulated Robots, SCARA Robots, Cartesian Robots, Collaborative Robots, and Delta Robots), By End-Use Industry (Automotive, Electrical & Electronics, Food & Beverage, Pharmaceutical & Healthcare, Metals & Machinery, Logistics & Warehousing, and Others) and Regional Forecast, 2026–2034

Robotics System Integration Services Market Size and Future Outlook

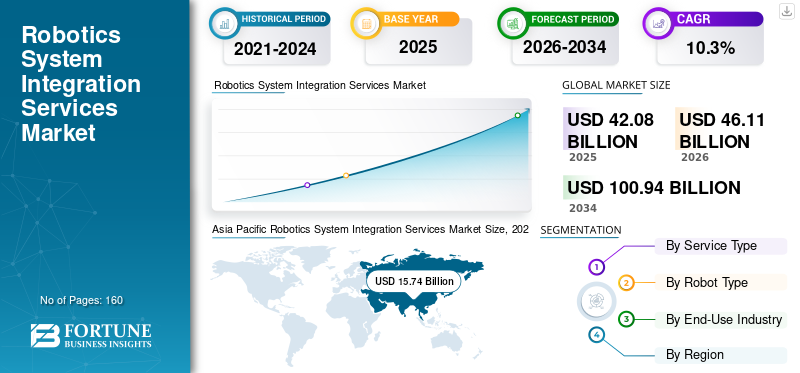

The global robotics system integration services market size was valued at USD 42.08 billion in 2025. The market is projected to grow from USD 46.11 billion in 2026 to USD 100.94 billion by 2034, exhibiting a CAGR of 10.3% during the forecast period.

Rapid adoption of automation, smart factory initiatives, growing need for flexible manufacturing, and the expansion of robotics in new manufacturing facilities are expected to drive market demand. Several government initiatives, rising advanced manufacturing, and e-commerce growth are additional factors that are propelling market growth. Manufacturing companies are heavily investing in smart factories, while Industry 4.0 is driving demand for complex system integration services. Manufacturers are focusing on flexible manufacturing processes that enable low-volume production, creating demand for reprogrammable robotics system integration services. Processes such as welding, assembly, material handling, and inspection are among the prominent application areas driving huge demand for robotics system integration services, thereby supporting overall market growth.

- For instance, in April 2025, Boston Dynamics and Hyundai Motor Group expanded their partnership to deploy tens of thousands of robots across manufacturing facilities.

Key players such as ABB Ltd., FANUC Corporation, and KUKA AG are prominent key players in the market. Collaboration with domestic players, expansion of digital and automation systems, and industry-focused solutions are key strategic moves adopted by these companies. As a result, market players are strengthening their positions and expanding their market share.

However, rising cost components and volatile geopolitical scenarios are contributing to supply chain disruptions across regions. Additionally, increased trade tariffs and a growing focus on local manufacturing might further limit market growth in the short term.

Download Free sample to learn more about this report.

Robotics System Integration Services Market Key Takeaways

- 2025 Market Size: USD 42.08 billion

- 2026 Market Size: USD 46.11 billion

- 2034 Forecast Market Size: USD 100.94 billion

- CAGR: 10.3% from 2026–2034

- Asia Pacific dominated the robotics system integration services market in 2025, supported by its strong manufacturing base and rapid industrial automation adoption.

- The programming & simulation services segment is expected to witness the highest growth rate of approximately 11.6% during the forecast period.

- The collaborative robots segment is projected to record the highest growth of around 11.6%, driven by increasing adoption of human-robot collaboration.

Asia Pacific

Asia Pacific dominated the market in 2025 and is expected to register the fastest growth due to expanding manufacturing activities and increasing automation investments.

North America

North America remains a mature market, supported by strong adoption of industrial automation across the automotive, aerospace, and electronics industries.

Europe

Europe continues to be a key regional market, driven by its well-established automotive, machinery, and aerospace manufacturing sectors.

U.S.

U.S. The market is driven by rising automation adoption across the automotive, aerospace, electronics, and logistics industries.

Japan

Japan The market is supported by the country's advanced robotics ecosystem and continued investments in smart manufacturing and factory automation.

Read More

ROBOTICS SYSTEM INTEGRATION SERVICES MARKET TRENDS

Expansion of Modular Automation Solutions to Bolster Product Demand

Modular and plug-and-play automation systems are gaining huge traction across key industries such as healthcare and pharmaceuticals. Modular robotic solutions are increasingly being integrated for applications such as packaging, palletizing, inspection, laboratory automation, and material handling. System integrators are developing industry-specific modular automation platforms that allow companies to adopt robotics incrementally rather than through large-scale automation investments. This approach reduces deployment risks, shortens implementation timelines, and makes robotic automation more accessible to small and medium-sized enterprises. As demand for flexible manufacturing and cross-industry automation increases, modular integration solutions are expected to play a key role in expanding the adoption of robotic systems integration across diverse industrial environments.

- For example, in October 2025, SoftBank agreed to acquire ABB’s robotics division for approximately USD 5.4 billion as part of its broader strategy to build a global AI-driven robotics ecosystem. The acquisition aims to combine AI infrastructure with industrial robotics capabilities to accelerate automation innovation.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Integration of Advanced Technology in Robotic Automation to Drive Market Growth

Robotics integration plays a crucial role in optimizing manufacturing processes and enhancing production capacity. The integration of advanced technology in robotic automation enables high-precision tasks, including inspection, assembly, and material handling. These systems are capable of real-time defect detection, identification of measurement deviations, and detection of surface, which may be difficult for human operators to achieve consistently. Several end-use industries, such as automotive, electronics, and medical device manufacturing, require high-precision tasks, leading to strong demand for robotics integration in manufacturing setups. Additionally, the integration of real-time data enables manufacturing companies to keep track and optimize the process, boosting the robotics system integration services market growth.

- For instance, in March 2026, ABB partnered with NVIDIA to develop a new generation of AI-enabled autonomous industrial robots integrating ABB’s RobotStudio platform with NVIDIA Omniverse simulation technology.

MARKET RESTRAINTS

High Initial Integration Costs and Implementation Complexity to Deter Market Expansion

Robotics system integration services require capital investment in hardware, controllers, software platforms, sensors, and safety systems. Companies also invest heavily in engineering services, programming, and system validation, further increasing overall project expenses. Due to initial integration costs and complexity, some companies delay or limit the adoption of robotics integration services despite the long-term productivity benefits.

MARKET OPPORTUNITIES

Adoption of Robotics-as-a-Service Model to Present Several Market Opportunities

Robotics-as-a-service (RaaS) model allows companies to access robotics systems based on subscription models or pay-per-use models, making it convenient for small and medium-scale organizations. Under this model, system integrators offer programming, maintenance, and system optimization along with the robotic equipment. The service also includes real-time continuous monitoring, software upgrades, and predictive maintenance for efficient robotic integration. As industries increasingly prioritize operational flexibility and cost optimization, the adoption of RaaS solutions is expected to accelerate, driving sustained demand for robotics system integration services.

MARKET CHALLENGES

Increasing Adoption of Industry 4.0 to Hinder Market Growth

With the increasing adoption of Industry 4.0, IoT-connected robots, and cloud-based automation platforms, robotic systems are becoming more vulnerable to cybersecurity threats. Protecting robotic networks, industrial control systems, and production data from cyberattacks presents a growing challenge for system integrators.

Segmentation Analysis

By Service Type

Robotic Cell Integration Segment Leads the Market Owing to Growing Adoption of Automated Production Line

Based on service type, the market is divided into system design & engineering, robotic cell integration, programming & simulation services, installation & commissioning, maintenance and support services, and training & consulting services.

Robotic cell integration dominates the market as it involves the core deployment of robotic systems within production environments. This service includes integrating robotics with conveyors, sensors, vision systems, safety equipment, and other machinery to create fully functional automated work cells. Industries such as automotive, electronics, and metal manufacturing rely heavily on robotic cells for applications such as welding, assembly, and material handling. The growing adoption of automated production lines and smart factories is driving strong demand for the product.

Programming & simulation services are expected to witness the highest growth rate of about 11.6% as manufacturers increasingly focus on optimizing robotic operations before physical deployment. These services involve robot programming, virtual commissioning, and simulation of production processes using digital tools to test robot performance and workflow efficiency. Simulation helps reduce integration risks, minimize downtime, and shorten implementation timelines. With the rising adoption of digital twins, AI-driven robotics programming, and advanced automation software, demand for these services is rapidly increasing across modern manufacturing environments.

- For instance, in October 2025, EVS completed the acquisitions of Telemetrics (US) and XD Motion (France) and launched a dedicated robotics division called T-Motion. The new division integrates robotics systems for automated media production and camera systems.

By Robot Type

Articulated Robots Segment Dominates the Market Owing to its Wide Industry Application

Based on robot type, the market is segmented into Articulated Robots, SCARA Robots, Cartesian Robots, Collaborative Robots, and Delta Robots.

Articulated robots dominate the market due to their high flexibility, multi-axis movement, and ability to perform complex industrial tasks such as welding, painting, assembly, and material handling. These robots are widely used in automotive, electronics, and heavy manufacturing industries where precision and payload capacity are critical. Continuous technological advancements and the expansion of industrial robot portfolios are strengthening their adoption.

Collaborative robots are expected to witness the highest growth of about 11.6% as manufacturers increasingly adopt human-robot collaboration for flexible and safe automation. Cobots are easier to deploy, cost-efficient, and require minimal safety barriers, making them suitable for SMEs and high-mix production environments. Their ability to work alongside human operators improves productivity and operational efficiency in sectors such as electronics, logistics, and healthcare.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Automotive Segment to Dominate due to Growing Electric Vehicles and Battery Automation

Based on end-use industry, the market is segmented into automotive, electrical & electronics, food & beverage, pharmaceuticals & healthcare, metals & machinery, logistics & warehousing, and others.

The automotive segment is expected to hold the dominant the robotics system integration services market share owing to growing demand for electric vehicles and battery automation. Robotics integration systems cater to varied applications such as welding, painting, assembly, and material handling. Automotive manufacturers rely heavily on robotic production lines to ensure high precision, consistency, and efficiency in large-scale vehicle manufacturing.

Logistics and warehousing are expected to witness the highest growth rate of about 12.6% as companies increasingly adopt automation to manage rising e-commerce demand and complex supply chains. Robotics system integrators are deploying automated sorting systems, robotic picking solutions, and autonomous mobile robots (AMRs) to improve warehouse efficiency and order fulfillment speed. The rapid expansion of large fulfillment centers and smart warehouses is significantly increasing the segment’s growth.

Robotics System Integration Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Robotics System Integration Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America represents a mature market for robotics system integration services, driven by strong adoption of industrial automation across automotive, aerospace, and electronics manufacturing sectors. The region benefits from the presence of major robotics companies, advanced technology infrastructure, and strong investment in Industry 4.0 initiatives. In addition, labor shortages and rising wages in the U.S. and Canada are encouraging manufacturers to adopt robotic automation to maintain productivity.

U.S. Robotics System Integration Services Market

The U.S. market is driven by strong automation adoption across the automotive, aerospace, electronics, and logistics industries. Rising labor costs and workforce shortages are encouraging manufacturers to invest in robotic automation and advanced system integration solutions to improve productivity.

Europe

Europe is a key market for robotics system integration services, supported by its strong industrial base in automotive, machinery, and aerospace manufacturing. Countries such as Germany, Italy, and France are global leaders in advanced manufacturing and industrial automation adoption. The region’s focus on energy-efficient production, digital manufacturing, and sustainability is encouraging companies to adopt robotics integration solutions. Additionally, increasing investments in smart factories and collaborative robotics technologies are driving further market expansion across European industries.

U.K. Robotics System Integration Services Market

The U.K. market will reach a value of USD 1.36 billion by 2026, representing roughly 2.9% of global market revenues.

Germany Robotics System Integration Services Market

Germany’s market will reach USD 2.90 billion by 2026, equivalent to around 6.3% of the global sales.

Asia Pacific

Asia Pacific dominates and is expected to witness the highest growth in the market due to its strong manufacturing base and rapid industrial automation adoption. Countries such as China, Japan, South Korea, and India are major manufacturing hubs with high demand for robotic automation in automotive, electronics, and semiconductor industries. Government-led initiatives supporting smart manufacturing, such as China’s “Made in China 2025” and Japan’s robotics innovation programs, are further accelerating market growth. The presence of major robot manufacturers and increasing investments in factory automation are also strengthening the region’s market leadership.

India Robotics System Integration Services Market

The Indian market, in 2026, will be valued at USD 3.13 billion, accounting for roughly 6.8% of the global market. Supportive government-led startup initiatives and increasing digital consumer base to propel the market growth in India.

China Robotics System Integration Services Market

China’s market is projected to remain dominant in the Asia Pacific region in 2026, with revenues reaching USD 5.50 billion, representing roughly 11.9% of global sales.

ASEAN Robotics System Integration Services Market

The ASEAN market will reach a value of USD 3.31 billion by 2026, accounting for roughly 7.2% of revenue.

South America

The robotics system integration services market in South America is gradually expanding as industries modernize their manufacturing infrastructure. Countries such as Brazil and Argentina are witnessing growing adoption of automation in automotive, food processing, and mining equipment manufacturing. Government initiatives aimed at improving industrial productivity and export competitiveness are encouraging manufacturers to adopt robotics integration solutions. However, economic volatility and limited technological infrastructure in certain countries may slow the pace of automation adoption.

Brazil Robotics System Integration Services Market

The Brazil market will reach USD 1.39 billion in 2026, representing roughly 3.0% of the global market.

Middle East and Africa

The Middle East & Africa region is experiencing increasing demand for robotics integration services as governments focus on industrial diversification and smart manufacturing initiatives. Countries such as the UAE and Saudi Arabia are investing in advanced automation technologies as part of national transformation programs like Vision 2030. Robotics integration is gaining traction in sectors such as logistics, oil & gas equipment manufacturing, and food processing. Additionally, the development of smart logistics hubs and automated warehouses in the Gulf region is contributing to market growth.

GCC Robotics System Integration Services Market

The GCC market will reach USD 0.93 billion in 2026, representing roughly 2.0% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Digital Technology Investment to Propel the Market Penetration

The robotics system integration services market is moderately fragmented, such that there is a large number of regional and specialized system integrators. Many service providers are investing in digital twins, AI-driven robotics programming, machine vision systems, and IoT-enabled automation platforms. System integrators are collaborating with robot manufacturers, AI companies, and software providers to enhance their technological capabilities.

- For instance, in 2024, Rockwell Automation partnered with robotics technology providers to enhance its FactoryTalk automation platform with integrated robotic control and analytics capabilities.

LIST OF KEY ROBOTICS SYSTEM INTEGRATION SERVICES MARKET COMPANIES PROFILED

- ABB Ltd. (Switzerland)

- KUKA AG (Germany)

- FANUC Corporation (Japan)

- Yaskawa Electric Corporation (Japan)

- Rockwell Automation, Inc. (U.S.)

- Siemens AG (Germany)

- ATS Corporation (Canada)

- JR Automation (U.S.)

- Dürr Group (Germany)

- Stäubli International AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: ABB announced an investment of approximately USD 75 million in India to expand its manufacturing and R&D capabilities in industrial automation and robotics. The expansion strengthens ABB’s ability to deliver integrated robotics solutions and automation services across industrial sectors.

- November 2025: ABB expanded its long-standing partnership with Tata Consultancy Services (TCS) to modernize its digital infrastructure using AI-driven IT operations. The collaboration aims to support ABB’s next phase of digital transformation across automation and robotics operations.

- October 2025: EVS completed the acquisitions of Telemetrics (U.S.) and XD Motion (France) and launched a dedicated robotics division called T-Motion. The new division integrates robotics technologies for automated media production and camera systems.

- January 2025: EcoRobotics introduced EcoBot 3000, a robotic automation platform designed for warehouse automation and sustainable operations.

- March 2024: ABB expanded and upgraded its robotics manufacturing and innovation facility in Auburn Hills, Michigan (U.S) with a USD 20 million investment.

REPORT COVERAGE

The global robotics system integration services market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.3% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Robot Type, End-Use Industry, and Region |

| By Service Type |

|

| By Robot Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 42.08 billion in 2025 and is projected to reach USD 100.94 billion by 2034.

In 2025, the market value stood at USD 15.74 billion.

The market is expected to exhibit a CAGR of 10.3% during the forecast period.

By service type, the robotic cell integration segment dominates the market.

Manufacturers’ consistent focus on quality control and precision to drive the market growth.

FANUC Corporation, KUKA AG, Siemens AG, and ABB Ltd. are the major players in the global market.

Asia Pacific dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us