Satellite Ocean Surveillance Market Size, Share & Industry Analysis, By Orbit (LEO, MEO , GEO, and Others), By Satellite Payload (SAR (Synthetic Aperture Radar), Electro-Optical (EO) / Multispectral, Thermal IR, RF Detection / RF Geolocation Payloads, Oceanography / Met-Ocean Payloads, and Others), By Constellation Architecture (Single Satellite, Small Constellation, Medium Constellation, and Large Constellation), By Satellite Class (Nanosat (<10 kg), Microsat (10–100 kg), Smallsat (100–500 kg), Medium (500–1,000 kg), and Large (>1,000 kg)), By End User, and Regional Forecast, 2026-2034

Satellite Ocean Surveillance Market Size and Future Outlook

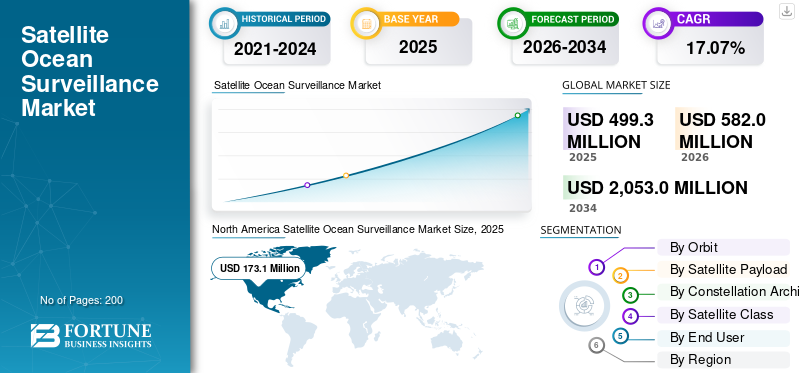

The global satellite ocean surveillance market size was valued at USD 499.3 million in 2025. The market is projected to grow from USD 582.0 million in 2026 to USD 2,053.0 million by 2034, exhibiting a CAGR of 17.07% during the forecast period. North America dominated the satellite ocean surveillance market with a market share of 34.66% in 2025.

Satellite ocean surveillance involves using satellites equipped with Synthetic Aperture Radar (SAR), optical imagers, and other sensors to monitor ocean surfaces for vessel detection, sea ice, oil spills, currents, and environmental changes, providing wide-area, all-weather coverage. It encompasses ship tracking (including dark vessels without AIS transponders), illegal fishing prevention, maritime security, navigation safety, pollution detection, and climate monitoring. Application areas include military domain awareness, coast guard operations, and environmental protection by agencies such as EMSA and ESA, and commercial shipping route planning. Driving factors include rising geopolitical tensions that are boosting security needs, technological advances in high resolution SAR constellations for real time imaging, and others.

Key players include ICEYE, Planet Labs, Maxar, Spire Global, and others. These companies operate X-band SAR satellites for vessel and dark ship detection, provide daily PlanetScope imagery for AI-driven maritime awareness, and deliver high-res analytics via Maritime Sentry for ocean tracking.

Download Free sample to learn more about this report.

SATELLITE OCEAN SURVEILLANCE MARKET TRENDS

Expansion of SAR Micro and Nano-Satellite Constellations is a Key Market Trend

Expansion of SAR micro and nano-satellite constellations represents a pivotal trend, enabling persistent global ocean surveillance through frequent revisits and all-weather imaging. ICEYE launched four new SAR satellites in January 2025 through SpaceX Transporter-12, followed by five more in November 2025, pushing its constellation beyond 44 units and enabling 25 cm resolution for vessel movement detection. This shift supports real-time applications such as dark tracking vessels, IUU fishing enforcement, and maritime security amid rising geopolitical tensions, while AI powered integration automates data processing to deliver actionable insights.

RUSSIA UKRAINE WAR IMPACT

The Russia-Ukraine war accelerated demand for satellite ocean surveillance by exposing shadow tanker fleets evading sanctions through ship-to-ship transfers in the Black Sea and Baltic approaches. European Maritime Safety Agency (EMSA), which provides satellite based services such as CleanSeaNet for oil spill detection and SafeSeaNet for vessel traffic monitoring systems across European waters. It ramped up SAR flights to detect illicit oil movements, while NATO integrated commercial feeds for real-time Russian naval tracking beyond the reach of jammed AIS signals. Geopolitical ripple effects spurred European procurement of persistent LEO constellations to monitor Arctic routes against hybrid threats.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Escalating Geopolitical Tensions and Maritime Security Threats to Drive Market Growth

Escalating geopolitical tensions and maritime security threats drive satellite ocean surveillance market growth by requiring continuous monitoring of contested waters, including the South China Sea, the Red Sea, and the Arctic. Conflicts such as Russia Ukraine highlight the need to detect sanctioned oil trades via ship-to-ship transfers, while illegal fishing and piracy underscore the need for wide-area awareness to protect global trade routes. Hybrid warfare risks, including unmanned vessel swarms and undersea cable sabotage, necessitate constellations' persistent stare to deter aggression and secure checkpoints. This spurs adoption by defense forces and agencies such as the European Maritime Safety Agency (EMSA).

MARKET RESTRAINTS

Technical Limitations Hinder the Market Growth

Technical limitations constrain the market by limiting observations to surface level phenomena, preventing penetration into water to detect subsurface threats such as submarines or underwater infrastructure. SAR imaging struggles with clutter discrimination at sea, misidentifying waves as vessels, while atmospheric interference and ionospheric effects corrupt altimetry data near coasts. Furthermore, Cloud cover blocks optical sensors entirely, and revisit gaps in non-constellation setups delay real time vessel monitoring.

MARKET OPPORTUNITIES

Rise in Additive Manufacturing Creates New Market Opportunities

Expanding LEO constellations creates market opportunities by enabling frequent revisits over remote areas. Low Earth orbits deliver sharper radar images of ships and spills in any weather, filling gaps for navies tracking dark vessels or agencies spotting illegal fishing far offshore. Moreover, faster data relay supports live alerts for pirates or oil leaks, while covering new routes such as the Arctic as ice melts.

MARKET CHALLENGES

Difficulty in Ground Processing Present a Major Market Challenge

Difficulty in ground processing creates a market challenge for satellite ocean surveillance as huge data streams from radar satellites flood stations during short flyovers, overwhelming storage buffers before full download. Raw images need complex fixes for distortions, noise, and wave clutter, slowing turnaround from hours to days without fast computers. Spotting ships amid ocean mess or fusing radar with ship signals demands expert tweaks, while legal rules and regulations require proven data chains that ground teams struggle to document.

Segmentation Analysis

By Orbit

High-Resolution Imaging and Data Quality to Boost the LEO Segmental Growth

Based on the orbit, the market is segmented into LEO, MEO, GEO, and others.

The LEO segment accounted for the largest market share in 2025. The segmental growth is primarily driven by the need for real-time, high resolution data for environmental, defense, and maritime monitoring.

The GEO segment is anticipated to rise with a CAGR of 17.02% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Satellite Payload

Enhanced Operational Capability to Boost SAR (Synthetic Aperture Radar) Segment Growth

Based on satellite payload, the market is segmented into SAR (Synthetic Aperture Radar), Electro-Optical (EO) / multispectral, thermal IR, RF detection / RF geolocation payloads, oceanography / met-ocean payloads and others.

In 2025, the SAR (Synthetic Aperture Radar) segment dominated the global market. The segmental growth is primarily driven by its day and night, all weather imaging capabilities. For marine surveillance, border security, and environmental monitoring, SAR is essential, as it provides reliable, high-resolution, and almost real-time data, unlike optical satellites, which are constrained by clouds, darkness, or haze.

The RF detection / RF geolocation payloads segment is projected to grow at a CAGR of 17.20% over the forecast period.

By Constellation Architecture

Balanced Redundancy and Continuous Coverage Drives Medium Constellation Segment Growth

Based on the constellation architecture, the market is segmented into single satellite, small constellation, medium constellation, large constellation.

The medium constellation segment is anticipated to witness a dominating market share over the forecast period. The growth of this segment is driven by its enhanced reliability from balanced redundancy and optimized revisit frequencies. They ensure continuous coverage over key maritime zones despite individual satellite outages, outperforming sparse large-sat setups or unproven mega-constellations.

The large constellation segment is projected to grow at the highest CAGR of 17.49% over the forecast period.

By Satellite Class

Enhanced Payload and Power Capabilities Boosts Smallsat (100-500kg) Segment Growth

Based on the satellite class, the market is segmented into Nanosat (<10 kg), Microsat (10–100 kg), Smallsat (100–500 kg), Medium (500–1,000 kg) and Large (>1,000 kg).

The smallsat (100–500 kg) segment is anticipated to witness a dominating market share over the forecast period. The growth of this segment is driven by the higher payload capacity, greater onboard power, and improved data handling provided by 100–500 kilogram satellites, which are necessary for sophisticated radar and imaging.

The microsat (10–100 kg) segment is projected to grow at the highest CAGR of 17.71% over the forecast period.

By End User

High Costs and Long Term Investment to boost the Civil space agencies Segment

Based on end user, the market is segmented into civil space agencies, defense ministries, SIGINT authorities, coast guard, fisheries authorities, commercial EO operators.

The civil space agencies segment dominated with the largest market share. This growth is driven by agencies such as NASA, ESA, and ISRO, which are equipped for the massive upfront investments and the decades-long, stable data requirements necessary for climate monitoring, ocean surveillance, and maritime domain awareness.

In addition, SIGINT authorities segment is projected to grow at the highest CAGR of 17.63% during the forecast period.

Satellite Ocean Surveillance Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Satellite Ocean Surveillance Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 148.1 million, and also maintained the leading share in 2025, with USD 173.1 million. North America dominates the market through substantial defense investments focused on Pacific and Arctic maritime domains, where agencies integrate commercial SAR feeds for persistent threat monitoring against adversarial naval activities.

U.S. Satellite Ocean Surveillance Market

Based on North America’s strong contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 122.8 million in 2026, with a roughly 16.89% CAGR over the forecast period. U.S. market growth stems from defense priorities that secure extensive coastlines, with federal agencies funding software defined radars and multi-sensor fusion to counter dark fleets and hybrid threats.

Europe

Europe is projected to record a steady growth rate of 17.54% during the forecast period, which is the second highest among all regions, and to reach a valuation of USD 122.8 million by 2026. Europe advances through collaborative ESA frameworks that pool SAR resources across member states for unified EEZ surveillance, and enhance pollution response and fisheries enforcement through shared data platforms.

U.K. Satellite Ocean Surveillance Market

The U.K. market in 2026 is estimated at around USD 42.6 million, with a CAGR of roughly 17.92% during the forecast period. The U.K. market expansion arises from sovereign needs post-Brexit, emphasizing North Sea and Channel monitoring with imported SAR capabilities integrated into national defense networks for fisheries protection and migrant interdiction.

Germany Satellite Ocean Surveillance Market

Germany’s market is projected to reach approximately USD 37.4 million in 2026.The growth stems from strategic Deutsches Zentrum für Luft- und Raumfahrt (DLR) investments in TerraSAR-X tandem operations providing reliable Baltic Sea coverage, where national security demands counter Russian submarine activities and shadow fleet tracking.

Asia Pacific

Asia Pacific region is estimated to reach USD 176.7 million in 2026 and secure the position of the third-largest region in the market during the forecast period. Asia Pacific surges amid territorial disputes, spurring indigenous SAR fleets for South China Sea vigilance.

Japan Satellite Ocean Surveillance Market

The Japanese market is estimated at around USD 28.8 million in 2026, with a CAGR of 17.55% during the forecast period. Japan propels progress through defense space strategy, emphasizing high-frequency imaging over island chains.

China Satellite Ocean Surveillance Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 61.3 million. China advances through military-civil fusion integrating ocean radars with navigation networks for comprehensive surveillance.

India Satellite Ocean Surveillance Market

The Indian market in 2026 is estimated at around USD 53.8 million. India drives expansion with dedicated coastal missions monitoring exclusive economic zones against poaching and smuggling.

Rest of the World

The rest of the world include the Middle East & Africa and Latin America. Latin America advances satellite ocean surveillance through equatorial launch advantages, enabling frequent coastal passes over Amazon River approaches and offshore oil platforms, with national agencies developing radar missions for ecosystem monitoring and smuggling interdiction. Middle East & Africa focuses on strait chokepoint vigilance using imported SAR paired with ground radars, to support energy export security amid regional conflicts. The Middle East & Africa and Latin America markets are set to reach valuations of USD 50.9 million and USD 30.8 million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Development Fuel Satellite Ocean Surveillance Market Expansion

The satellite ocean surveillance competitive landscape features established players such as ICEYE, Planet Labs, Maxar, and Spire Global, dominating through specialized SAR and multi-sensor capabilities tailored for maritime domain awareness.

Key players advance through AI-powered vessel classification algorithms that automatically distinguish ships from ocean clutter in SAR imagery, alongside software-defined radar payloads enabling dynamic resolution adjustments for small craft detection. Developments include multi sensor data fusion platforms combining radar, optical, and AIS signals for real-time anomaly alerts, plus deployable antenna technologies extending spotlight modes over chokepoints.

LIST OF KEY SATELLITE OCEAN SURVEILLANCE COMPANIES PROFILED

- ICEYE (Finland)

- Planet Labs (U.S.)

- Maxar Technologies (U.S.)

- Spire Global (U.S.)

- Capella Space (U.S.)

- Airbus Defence and Space (France)

- Ursa Space Systems (U.S.)

- BlackSky Technology (U.S.)

- Umbra (Canada)

- CLS Group (France)

KEY INDUSTRY DEVELOPMENTS

- October 2025: The U.S. Navy awarded Planet Labs PBC, through its subsidiary Planet Labs Federal, a USD 7.5 million contract renewal for vessel detection and monitoring across strategic areas of interest across the Pacific.

- October 2025: The National Geospatial-Intelligence Agency (NGA) awarded Planet Labs a USD 12.8 million contract to provide marine data and analytics for the Asia Pacific region.

- July 2025: Under the SBS-III initiative, the Indian government has authorized the quick deployment of 52 surveillance satellites to improve national security through cutting-edge border satellite monitoring.

- June 2025: With AI-powered analytics and high-resolution satellite data, Maxar Intelligence has introduced Maritime Sentry. This revolutionary maritime surveillance system enables real-time observation of vessel activities in port and across vast ocean areas.

- November 2024: An agreement has been reached between Kongsberg Defence & Aerospace (KDA), Norway, and ESA's General Support Technology Programme (GSTP) to construct the Arctic Ocean Surveillance precursor (AOS-p) mission.

REPORT COVERAGE

The global satellite ocean surveillance industry analysis includes a comprehensive study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, Porter’s Five Forces analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers, and acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.07% from 2026-2034 |

| Unit | Value (USD Million) |

| By Orbit |

|

| By Satellite Payload |

|

| By Constellation Architecture |

|

| By Satellite Class |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 499.3 million in 2025 and is projected to reach USD 2,053.0 million by 2034.

In 2025, the North American market value stood at USD 173.1 million.

The market is expected to grow a CAGR of 17.07% during the forecast period.

By orbit, the LEO segment dominated the market in 2025.

Escalating geopolitical tensions and maritime security threats are the key factors driving market growth.

ICEYE (Finland), Planet Labs (US), Maxar Technologies (US), Spire Global US), Capella Space (US), Airbus Defence and Space (France) are few key players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us