Quick Commerce Market Size, Share & Industry Analysis, By Mode of Payment (Cash on Delivery and Cashless Payments), By Product (Groceries, Beauty & Personal Care, Fresh Food & Beverages, Electronics & Toys, and Others), By Channel Type (Mobile Application and Web Portal), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

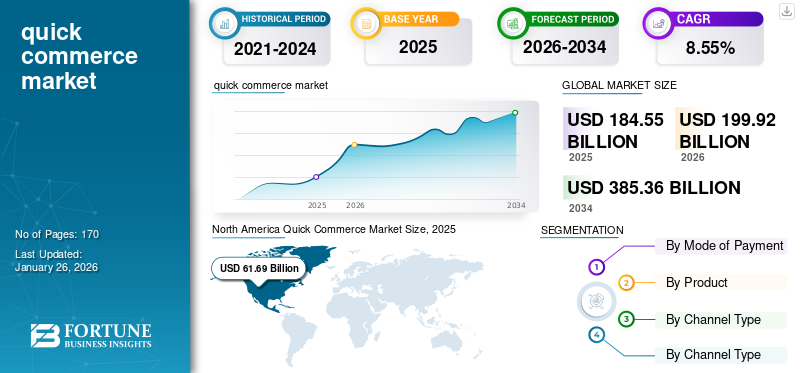

The global quick commerce market size was valued at USD 184.55 billion in 2025 and is projected to grow from USD 199.92 billion in 2026 to USD 385.36 billion by 2034, exhibiting a CAGR of 8.55% over the forecast period. North America dominated the quick commerce market with a market share of 33.43% in 2025. Internationally reputed players, including Getir, Blinkit, GoPuff, Flink, and Swiggy Instamart lead the intensely competitive market. Established players and relatively new players investment in cost-efficient delivery platforms and AI-driven inventory management tools is anticipated to keep the market competitive.

Quick commerce, also known as the Q-commerce, refers to a segment of the e-commerce industry focused on rapid delivery of food and other goods, typically delivered in under 30 minutes. It primarily caters to high-demand, low-involvement products such as groceries, ready-to-eat meals, personal care items, and other household essentials. Q-commerce operates through hyperlocal super fast delivery models, leveraging small warehouses or dark stores located close to customer hubs, along with advanced technology and efficient logistics networks. The market is mainly driven by consumer preferences for convenience and immediacy.

Download Free sample to learn more about this report.

Global Quick Commerce Market Snapshot

Market Size & Forecast:

- 2025 Market Size: USD 184.55 billion

- 2026 Market Size: USD 199.92 billion

- 2034 Forecast Market Size: USD 385.36 billion

- CAGR: 8.55% from 2026–2034

Market Share:

- North America dominated the quick commerce market with a 33.43% share in 2025, driven by the growing demand for ultra-fast deliveries of essentials, high smartphone penetration, and expansion by major players such as Uber Eats, DoorDash, and Instacart.

- By product, Groceries retained the largest market share in 2024, supported by frequent, urgent purchase behavior and high reliance on delivery of everyday essentials like dairy, produce, and pantry items.

Key Country Highlights:

- United States: Rapid digital adoption, venture capital funding, and aggressive expansion by tech-enabled delivery companies make the U.S. the market’s global growth engine.

- India: Rising urbanization, a booming youth population, and expanding startup ecosystem (e.g., Blinkit, Zepto, Swiggy Instamart) drive the fastest growth in Asia.

- Germany: Dense urban centers and a strong focus on eco-friendly delivery (bikes and EVs) foster growth for players like Flink and Getir.

- United Kingdom: Premium delivery expectations and increasing digital payment usage support expansion by local players like Zapp and global entrants.

- Saudi Arabia & UAE: Wealthy, tech-savvy consumers and strong mobile/internet penetration contribute to growing demand for ultra-fast and premium delivery services.

QUICK COMMERCE MARKET TRENDS

Rise of Hyper-Localized Quick Commerce Solutions to Enhance Service Adoption

Q-commerce is witnessing a shift toward hyper-localized services driven by consumer demand for personalized and faster deliveries. Companies in this market space are leveraging micro-warehouses and dark stores strategically placed within urban neighborhoods to ensure delivery within 10-30 minutes. This model enhances efficiency and also caters to local preferences by stocking region-specific products. The integration of AI-driven inventory management and real-time demand forecasting further optimized operational efficiency.

Moreover, partnerships with local vendors are expanding product assortments while supporting community businesses. Sustainability is also gaining traction, with eco-friendly packaging and carbon-neutral delivery. As consumer expectations evolve, hyper-localization is becoming a key differentiator for Q commerce players aiming to build loyalty in a competitive market.

- North America witnessed quick commerce market growth from USD 54.95 Billion in 2023 to USD 57.25 Billion in 2024.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Consumer Need for Convenience and Speed to Fuel Market Growth

The growing preference for on-demand services has made consumers expect faster and more convenient delivery options. Urbanization, busy lifestyles, and the rise of working professionals have further amplified the need for quick access to everyday essentials, fueling the market growth. The primary aim of Q commerce is to satisfy the growing consumer demand for rapid order fulfilment and ease of accessibility, catering to immediate needs such as urgent purchases, last-minute essentials, and grocery replenishment.

Market players in this space leverage technology to streamline operations, from order placement to food delivery, ensuring a seamless and swift customer experience. This model is apt and suitable for the population in urban areas where the density of potential consumers substantiates the investment in infrastructure and technology required to support super fast delivery time. Additionally, quick commerce companies are offering discounts that brick-and-mortar stores struggle to match and are therefore preferred by a large chunk of consumers.

Advancement in Technology and Logistics to Favor Market Expansion

Innovations in technology, such as AI-powered route optimization, real-time inventory management, and mobile apps, have enabled seamless operations in the Q commerce space. Additionally, the development of hyperlocal delivery networks and dark stores has enhanced the efficiency of last-mile logistics, supporting the rapid expansion of this market. Technological advancements, proliferation of smartphones, and the increasing penetration of the internet have boosted the swift growth of this sector.

Market Restraints

High Operational Cost and Low-Profit Margins May Obstruct Market Growth

Quick commerce companies require maintaining robust infrastructure, including dark stores, advanced inventory management systems, and reliable last-mile delivery networks, to fulfill orders within a short timeframe. These factors significantly increase operational expenses. Additionally, the reliance on discounts and promotions to attract customers often reduces profitability, making it challenging for companies to achieve substantial growth.

Market Opportunities

Product Diversification and Sustainability Innovations to Offer Lucrative Growth Opportunities

Established industry participants will likely emphasize product diversification to gain a competitive edge over the forecast timeframe. While groceries dominate the sector globally, electronics & toys, pharmaceuticals, and beauty & personal care categories offer significant potential for expansion. Furthermore, internationally renowned players will target new, underserved markets, notably across Asian countries, to lessen the threat of new players’ entry. At a macro level, sustainability innovations offer significant growth opportunities to both established and new market players. Practices such as employing Electric Vehicles (EVs) for product delivery and adopting sustainable packaging materials help companies make sustainable commitments and build a strong brand reputation.

Impact of COVID-19

COVID-19 Positively Influenced Industry Growth owing to Increased Need for Contactless Deliveries

The COVID-19 pandemic significantly boosted the quick commerce sector, as lockdowns and safety concerns drove consumers toward fast, contactless deliveries. With more people staying indoors, the demand surged for essentials such as groceries, medicine, and hygiene products, fostering growth for online delivery platforms promising delivery within shorter periods. Startups and established players expanded aggressively, utilizing technology and hyperlocal partnerships to meet this demand.

However, the industry also faced certain challenges, including strained supply chains, increased operational costs, and labor shortages. Despite these hurdles, the pandemic cemented Q commerce as a vital part of urban lifestyles, reshaping consumer habits and accelerating digital adoption in retail.

SEGMENTATION ANALYSIS

By Mode of Payment

Increasing Awareness Regarding Benefits to Create Demand for Home Healthcare Services

Based on mode of payment, the market is bifurcated into cash on delivery and cashless payments.

The cashless payment segment is projected to account for 83.16% of the market share in 2026 and is expected to continue its prominent position during the forecast period. Various modes of cashless payments, including credit cards, debit cards, mobile banking, internet banking, and UPI apps, among others, have increased significantly in recent years as a result of coordinated efforts of the government with all stakeholders.

This remarkable growth of digital transactions enabling cashless payments has offered several benefits, such as fostering economic development, promoting financial stability, enhanced transparency in government systems, and valuable data for informed decision-making. This, in turn, is projected to supplement the segmental growth.

The cash on delivery segment is forecast to grow at a steady CAGR between 2025 and 2032. This method of payment is still appealing to the audience that still does not have access to credit/debit cards, is hesitant to make payment online, or is new to a brand.

To know how our report can help streamline your business, Speak to Analyst

By Product

Frequent and Urgent Need to Support Highest Revenue Generation through Groceries Segment

By product, the market is segmented into groceries, beauty & personal care, fresh food & beverages, electronics & toys, and others.

The groceries segment is expected to represent 43.78% of the total market share in 2026, contributing the highest market share. This segment includes products, such as cereals, breakfast & instant food, snacks & munchies, seafood, baked goods, meat and meat alternatives, dairy, vegetables & fruits. Urban consumers prioritize convenience and time savings, relying on quick home delivery for last-minute needs or meal preparation. Additionally, the rise of working professionals, nuclear families, and busy lifestyles amplifies demand, making groceries a core category for Q commerce growth. The grocery segment is anticipated to capture 44% of the revenue share in 2025.

The fresh food and beverages segment held the second-largest share of the market in 2024 and is projected to grow at the fastest CAGR of 9.81% over the forecast period (2025-2032). Food cravings and thirst often trigger impulse buying. The convenience of ordering and receiving these items in minutes aligns perfectly with this behavior. Additionally, people in urban centers often lack time and energy to cook or dine out due to their fast-paced lifestyle. The instant delivery of ready-to-eat meals or beverages fills this gap efficiently, supporting the segment growth.

By Channel Type Analysis

Deeper Penetration and High Adoption of Smartphones to Boost Growth of Mobile Applications

Based on the channel type, the market is segmented into mobile application and web portal.

The mobile application segment dominated the global quick commerce market with a market share of 93.58% in 2026 due to the high penetration of smartphones and easy accessibility of internet access. A significant portion of the market’s target audience prefers mobile-first solutions owing to their lifestyle and reliance on smartphones for daily activities. Furthermore, apps can integrate with device-specific features, such as GPS for precise location-based delivery, cameras for QR code scanning, and mobile wallets for quick payments. GPS integration in Q commerce ensures faster, hyper-local delivery, boosting the segment growth. The mobile application segment is likely to hold 93% of the market share in 2025.

The web portal segment is expected to grow considerably and holds notable preference among certain user segments. Factors driving the growth of the segment include the ease of use of larger screens with better viewing experience and detailed search, ease of input for complex orders, secure environment, and perceived professionalism, along with no constraint for app storage. The web portal segment is forecasted to display a strong CAGR of 3.93% during the forecast period.

Quick Commerce Market Regional Outlook

Geographically, the market is divided into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

North America

North America Quick Commerce Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market value of USD 57.25 billion in 2024, and USD 54.95 billion in 2023. The Q commerce market in North America is a fast-evolving sector that caters to the growing demand for ultra-fast delivery of groceries, household essentials, and convenience items. Key features of the Q commerce market in the region include an emphasis on urban areas, a wide array of product categories, technology integration, and strategically located dark stores. Uber Eats, DoorDash, and Instacart are key players in the region. Large retailers such as Amazon and Walmart have ventured into the space, leveraging their vast logistics networks to offer ultra-fast delivery. The U.S. market is projected to reach USD 55.68 billion by 2026. In 2025, North America represented USD 61.69 billion, accounting for 33.43% of the worldwide market, and is projected to grow to USD 66.64 billion in 2026.

The U.S. market is estimated to hit USD 51.60 billion in 2025. The demand for Q commerce in the U.S. market has been growing exponentially due to the tech-savvy population, changing consumer habits, and accelerated online shopping trends. Further, venture capital and acquisitions have increased in the U.S. market, enabling players to scale and improve service offerings.

Europe

Europe to be anticipated the second-largest market with USD 58.96 billion in 2025, recording the second-largest CAGR of 9.28% during the forecast period. The Europe quick commerce market is projected to expand significantly behind Asia Pacific over the forecast years. Consumers in the region increasingly value convenience and time savings, especially in densely populated city centers, making Europe a prime market for on-demand delivery. The players in the market focus on environmentally friendly delivery methods, such as bicycles or electric vehicles. Some of the prominent players in the European market include Gorillas, Getir, Flink, and Deliveroo. The UK market is projected to reach USD 8.6 billion by 2026, while the Germany market is projected to reach USD 11.61 billion by 2026. The Europe market generated USD 58.96 billion in 2025, representing 31.95% of the global market landscape, and is expected to reach USD 64.03 billion in 2026.

The Germany’s market size is foreseen to be valued at USD 10.69 billion and France’s likely to be USD 5.98 billion in 2025.

Asia Pacific

Asia Pacific region is to be anticipated the third-largest market with USD 48.54 billion in 2025. The Asia Pacific market is expected to register the highest CAGR during the projection period owing to high population density, increasing urbanization, and evolving consumer behavior. High smartphone penetration and the widespread use of digital wallets have created a robust foundation for Q commerce adoption. With its youth population and booming startup ecosystem, India has emerged as a key growth driver in the region. Quick commerce is transforming the e-commerce sector in India by offering ultra-fast day delivery. Meanwhile, developed markets such as South Korea, Japan, and Australia emphasize quality, speed, and sustainability in Q commerce offerings. The Japan market is projected to reach USD 5.44 billion by 2026, the China market is projected to reach USD 14.77 billion by 2026, and the India market is projected to reach USD 13.56 billion by 2026. Asia Pacific contributed 26.30% to the global market in 2025, with a valuation of USD 48.54 billion, and is projected to reach USD 52.95 billion in 2026.

Middle East & Africa

The Middle East & Africa market was valued at USD 5.52 billion in 2025, capturing 2.99% of global revenue, and is estimated to reach USD 5.83 billion in 2026.

South America

The South America region captured 5.33% of the global market in 2025, generating USD 9.83 billion in revenue, and is projected to reach USD 10.47 billion in 2026.

Rest of the World

With nearly 70-90% of the population in the GCC countries having internet access, the Middle East boasts a tech-savvy audience. Wealthier demographics in the GCC countries have driven the demand for premium services such as fast delivery. Local startups such as Jahez in Saudi Arabia and global delivery platforms such as Talabat and Careem dominate the market. In contrast, international players, such as Deliveroo and Zapp, are expanding their reach further, boosting global quick commerce market growth. The UAE market is expected to hit USD 0.56 billion in 2025.

South America is expected to be the fourth-largest market with a value of USD 9.83 billion in 2025.

Competitive Landscape

Key Market Players

Prominent Industry Participants Focus on Mergers & Acquisitions to Enhance Reach

Numerous domestic and international players characterize the market’s intense competition. In recent years, mergers and acquistions have been the most prominent competitive strategies employed by industry participants. For instance, in June 2022, Zomato Ltd, an Indian food delivery company, acquired Blink Commerce Private Limited, an Indian e-commerce agency, marking Zomato Ltd’s foray into the quick commerce sector.

LIST OF KEY QUICK COMMERCE COMPANIES PROFILED IN THE REPORT:

- Getir (Turkey)

- Blinkit (India)

- GoPuff (U.S.)

- Flink (Germany)

- Swiggy Instamart (India)

- Zapp (U.K.)

- Dunzo (India)

- Glovo (Spain)

- Zepto (India)

- JOKR (U.S.)

Key Industry Developments

- June 2024: Zepto, an Indian quick-commerce company, garnered USD 665 million in the funding round, taking its valuation to USD 3.6 billion. With this funding, the company aims to double its dark-store count to 700, bolstering its position in India’s rapidly growing quick-commerce sector.

- March 2024: Swiggy, a major industry player, merged its premium grocery vertical InsanelyGood with its quick commerce vertical Instamart.

- November 2023: Getir, an ultra-fast grocery delivery services company based out of Turkey, announced the acquisition of online grocery company FreshDirect to expand its footprint in the U.S. This acquisition would lead to significant collaborations between the two companies wherein FreshDirect will retain its brand name and will continue to operate out of its facility in New York City and will leverage Getir’s technology and operational footprint to serve its customer base. On the other hand, FreshDirect will enable Getir to enhance further the breadth and quality of its product line, particularly its fresh products range, making it even more appealing to its New York customers.

- December 2022: Getir announced the acquisition of Gorillas, a German ultrafast grocery delivery services company, in a deal worth USD 1.2 billion.

- July 2021: Jokr, a start-up that delivers grocery, secured USD 170 million in funding to expand its business operations into more markets on both sides of the Atlantic. The company is already active in nine cities across Europe and the Americas, and several more launch cities are planned in the future.

Investment Analysis and Opportunities

Technology Integration Achieving Faster Last-Mile Delivery to Create Numerous Growth Opportunities

The market has grown significantly over the last few years, driven by high demand resilience, recurring revenue models, and tech-driven efficiency. Essentials such as groceries and medicine sustain demand even during economic downturns. Investing in Micro-Fulfillment Centers (MFCs) technology to streamline inventory and enable faster deliveries or developing platforms for route optimization, inventory prediction, and last-mile delivery coordination provides investors with an opportunity.

Moreover, diversifying product offerings into high-margin categories such as pharmaceuticals and beauty products is another lucrative growth opportunity. Additionally, expanding into high-growth regions such as Southeast Asia, Latin America, and the Middle East is a potential opportunity for investors.

REPORT COVERAGE

The market research report provides a detailed analysis of the market and focuses on key aspects such as the competitive landscape, services, and leading product types. It also offers global market trends and insights and highlights key industry developments. In addition to the aforementioned factors, the report on the global market outlook has several factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 8.55% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Mode of Payment

|

|

By Product

|

|

|

By Channel Type

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global Quick Commerce market was valued at USD 170.80 billion in 2024 and is projected to reach USD 385.36 billion by 2034, growing at a CAGR of 8.55% during the forecast period.

The market is anticipated to grow at a CAGR of 8.55% during the forecast period (2026-2034).

Quick Commerce, or Q-commerce, refers to a segment of e-commerce focused on delivering groceries, ready-to-eat meals, personal care items, and essentials typically within 30 minutes using hyperlocal warehouses or dark stores close to customers.

The growth is fueled by urbanization, busy lifestyles, and rising consumer demand for speed and convenience. Advances in AI-driven inventory management, route optimization, and expansion of hyperlocal delivery networks also significantly contribute.

North America leads the Quick Commerce market with a 33.43% share in 2025, supported by tech-savvy consumers, strong urban demand, and investments from major players like Amazon, Uber Eats, and DoorDash.

Technological innovations such as AI powered route optimization, real-time inventory tracking, mobile apps, and hyperlocal dark stores have optimized operations and enabled ultra-fast delivery, making Q-commerce more efficient and customer friendly.

High operational costs due to infrastructure needs, low-profit margins from frequent discounts, supply chain complexities, and labor shortages pose significant challenges to sustainable growth in the Q-commerce sector.

Groceries hold the largest share due to frequent and urgent needs, followed by fresh food and beverages, which are growing rapidly. Other emerging categories include beauty & personal care, electronics, and pharmaceuticals.

- 2021-2034

- 2025

- 2021-2024

- 170

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us