Ship Energy Efficiency Systems Market Size, Share & Industry Analysis, By System Type (Propulsion Efficiency Systems, Energy Management Systems (EMS), Waste Heat Recovery Systems, Air Lubrication Systems, Hull Efficiency Systems, and Others), By Ship Type (Container Ships, Bulk Carriers, Tankers, Passenger Ships, Offshore Vessels, Naval Ships, and Others), By Technology (Hardware-Based Systems, Software & Digital Solutions, Hybrid Systems, and Others), Regional Forecast, 2026-2034

Ship Energy Efficiency Systems Market Size and Future Outlook

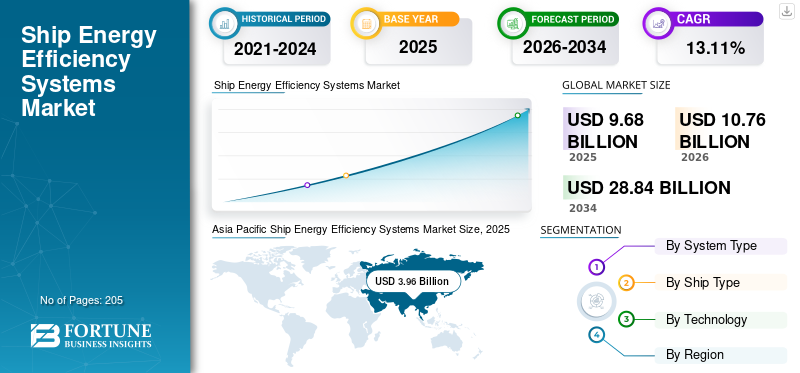

The global ship energy efficiency systems market size was valued at USD 9.68 billion in 2025. The market is projected to grow from USD 10.76 billion in 2026 to USD 28.84 billion by 2034, exhibiting a CAGR of 13.11% during the forecast period. Asia pacific dominated the ship energy efficiency systems market with a market share of 40.90% in 2025.

Ship energy-efficiency systems encompass a range of onboard technologies and digital solutions that optimize fuel consumption, improve propulsion performance, and reduce operational emissions in real time across maritime vessels. These systems include propulsion optimization devices, air lubrication technologies, waste heat recovery units, and advanced energy management platforms that continuously monitor and adjust vessel performance in real time. Their adoption has accelerated as shipowners increasingly shift from purely compliance-driven upgrades to performance-oriented investments that directly impact voyage economics.

The market share is driven by tightening regulatory frameworks, such as the International Maritime Organization’s Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII), which require measurable improvements in vessel efficiency. Additionally, rising fuel costs and volatility in bunker prices have made energy savings a critical lever for cost control, particularly for bulk carriers and container fleets operating on thin margins. The growing availability of retrofit-friendly technologies and digital optimization tools has further enabled operators to achieve efficiency gains without major structural modifications, supporting wider adoption across aging global fleets.

- For instance, in March 2023, Wärtsilä Corporation secured a contract to supply its energy efficiency optimization solutions, including advanced energy management systems and propulsion upgrades, for a fleet of container vessels operated by a European shipping company. The project focused on improving fuel efficiency and ensuring compliance with IMO’s EEXI and CII regulations. By integrating real-time performance monitoring and voyage optimization tools, the vessels are expected to achieve significant reductions in fuel consumption and operational emissions.

Some of the leading companies operating in the global industry include Wärtsilä Corporation, MAN Energy Solutions, Alfa Laval AB, Becker Marine Systems GmbH, and others. Wärtsilä Corporation is a leading provider of integrated vessel energy efficiency solutions, offering technologies such as propulsion optimization, hybrid power systems, and advanced energy management platforms. The company focuses on enhancing vessel performance through digital analytics and real-time monitoring, enabling shipowners to reduce fuel consumption and meet evolving emission regulations.

Download Free sample to learn more about this report.

SHIP ENERGY EFFICIENCY SYSTEMS MARKET TRENDS

Shift Toward Integrated Digital Energy Optimization Systems is the Key Market Trend

The ship energy efficiency systems market growth is driven by the transition from standalone mechanical upgrades to integrated digital optimization platforms that combine hardware with real-time analytics. Shipowners are increasingly adopting solutions that connect propulsion systems, onboard sensors, weather data, and voyage planning tools into a unified energy management framework. This allows continuous monitoring of fuel consumption, hull performance, and engine efficiency under varying operating conditions, rather than relying on periodic manual assessments.

In addition, the growing preference for modular retrofit solutions, in which operators implement incremental upgrades such as air lubrication or voyage-optimization software based on vessel age and trade-route economics. This phased approach reduces upfront capital burden while still delivering measurable efficiency gains. Additionally, wind-assisted propulsion technologies, including rotor sails, are gaining traction on long-haul routes where fuel savings justify installation costs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Regulatory Convergence with Commercial Performance Metrics is the Key Market Driver

A major driver accelerating the adoption of ship energy efficiency systems is the increasing alignment between regulatory compliance frameworks and commercial performance benchmarks. Instead of treating efficiency upgrades as standalone compliance measures, shipowners are now integrating them into charter competitiveness and fleet utilization strategies. For instance, vessels with better Carbon Intensity Indicator (CII) ratings are gaining preference in charter markets, directly influencing revenue potential and asset valuation.

Another key driver is the growing emphasis on data transparency and reporting requirements, particularly from cargo owners and financial institutions. Shipping companies are increasingly required to disclose emissions intensity and operational efficiency metrics as part of ESG-linked financing and contractual obligations. This is pushing operators to deploy verifiable energy efficiency systems that can generate auditable performance data. These factors are anticipated to drive the compound annual growth rate (CAGR) during the forecast period.

MARKET RESTRAINTS

High Retrofit Complexity and Operational Disruptions to Hamper the Market Demand

A key restraint in the ship energy efficiency systems market is the technical complexity associated with retrofitting existing vessels, particularly older ships with limited design flexibility. Many efficiency solutions, such as air lubrication systems or waste heat recovery units—require structural modifications, drydocking, and integration with legacy onboard systems. This leads to extended vessel downtime, which directly impacts revenue generation for operators, especially in high-utilization segments like container shipping.

Another constraint is the uncertainty in performance outcomes across different operating conditions. The effectiveness of certain technologies, such as wind-assisted propulsion or hull optimization systems, can vary significantly depending on route patterns, vessel load, and weather conditions. This variability makes it difficult for shipowners to accurately forecast return on investment, slowing decision-making.

MARKET OPPORTUNITIES

Expansion of Digital Twin and Predictive Performance Modeling Curates Market Opportunities

A significant opportunity in the ship energy efficiency systems market lies in the adoption of digital twin technology and predictive performance modeling. Shipowners are increasingly leveraging virtual replicas of vessels to simulate real-world operating conditions, enabling precise optimization of fuel consumption, maintenance schedules, and system performance. These models allow operators to test multiple efficiency scenarios, such as route changes, speed variations, or equipment upgrades, before actual implementation, reducing operational risks.

In addition, the integration of energy-efficiency systems with alternative-fuel transition strategies. As vessels shift toward LNG, methanol, and ammonia-based propulsion, there is growing demand for systems that can optimize energy usage across hybrid fuel configurations. This creates scope for advanced control systems and energy management platforms that can dynamically balance fuel inputs and improve overall efficiency.

MARKET CHALLENGES

Fragmented Technology Integration and Vendor Ecosystem Creates Market Challenge

A key challenge in the ship energy efficiency systems market is the fragmented nature of technologies and solution providers, which complicates seamless system integration onboard vessels. Ships often deploy multiple systems from different vendors, such as propulsion upgrades, digital monitoring tools, and auxiliary efficiency solutions that may not be inherently compatible. This leads to integration issues, data silos, and suboptimal performance, as systems operate independently rather than as part of a unified energy optimization framework.

Another challenge is the limited standardization in data architecture and communication protocols across the maritime industries. Inconsistent data formats and interoperability issues hinder the effective use of advanced analytics and real-time optimization tools, thereby reducing the overall impact of digital efficiency solutions.

Segmentation Analysis

By System Type

Propulsion Efficiency Systems Dominate Due to Measurable Reduction in Fuel Consumption

Based on the system type, the market is classified into propulsion efficiency systems, Energy Management Systems (EMS), waste heat recovery systems, air lubrication systems, hull efficiency systems, and others.

In 2025, the propulsion efficiency systems dominated the market share because they deliver immediate and measurable reductions in fuel consumption, which remains the highest operating cost for most vessels. Technologies such as optimized propellers, rudder bulbs, and propulsion control upgrades directly enhance thrust efficiency and reduce energy losses during sailing. Unlike auxiliary systems, propulsion improvements impact the vessel continuously across all operating conditions, making their payback period more predictable.

The Energy Management Systems (EMS) segment is experiencing the highest growth and is expected to grow at a CAGR of 15.38% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Ship Type

Container Ships Dominated the Market Due to High Operational Intensity and Sailing Schedules

Based on the ship type, the market is classified into container ships, bulk carriers, tankers, passenger ships, offshore vessels, naval ships, and others.

In 2025, the container ships segment dominated the global market. This is due to their high operational intensity and continuous sailing schedules, which make fuel efficiency a critical cost factor. These vessels operate on fixed routes with tight delivery timelines, leaving limited flexibility for speed reductions, thereby increasing reliance on technological efficiency improvements. Their large engine sizes and high fuel consumption create strong economic incentives for adopting propulsion optimization, energy management systems, and digital voyage planning tools.

The passenger ships segment is expected to grow at a CAGR of 13.93% during the forecast period.

By Technology

Hardware-Based Systems Dominated Due to Their Impact on Vessel Performance and Fuel Consumption

On the basis of technology, the market is classified into hardware-based systems, software & digital solutions, hybrid systems, and others.

In 2025, the hardware-based systems segment dominated the global market due to its proven, measurable impact on vessel performance and fuel consumption. Technologies such as air lubrication systems, waste heat recovery units, optimized propellers, and hull modifications deliver direct efficiency improvements that can be physically verified during operations. Shipowners often prioritize these systems because they provide consistent performance regardless of data quality or digital infrastructure, unlike software solutions that depend on integration and analytics.

The software & digital solutions segment is expected to grow at a CAGR of 14.49% during the forecast period.

Ship Energy Efficiency Systems Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Ship Energy Efficiency Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market in 2025 was valued at USD 1.47 billion, and also expected to hold a share in 2026 with USD 1.63 billion.

North America’s market is strongly driven by EPA emission regulations and regional compliance frameworks that require measurable reductions in vessel fuel intensity, particularly in coastal and inland waterways. Additionally, the presence of large retrofit-ready fleets in the U.S. is accelerating demand for propulsion upgrades and digital monitoring systems.

U.S. Ship Energy Efficiency Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.17 billion in 2025, accounting for roughly 12.14% of the global market size.

Europe

Europe is projected to record a growth rate of 12.59% in the coming years, which is the second-highest among all regions, and reached a valuation of USD 2.72 billion in 2025. Adoption in Europe is primarily driven by the inclusion of maritime transport emissions under the EU ETS, which directly links carbon costs to vessel efficiency performance. Additionally, strict enforcement of MRV (Monitoring, Reporting, Verification) regulations is pushing operators to deploy systems that provide accurate fuel and emissions data. The region also benefits from strong policy support for green shipping corridors, encouraging early adoption of advanced efficiency technologies across key trade routes.

Germany Ship Energy Efficiency Systems Market

The German market in 2025 reached a value of USD 0.67 billion in 2025 and is estimated at around USD 0.74 billion by 2026, representing roughly 6.95% of the global ship energy efficiency systems revenues. Germany’s adoption is driven by its strong marine engineering ecosystem and presence of leading technology providers, enabling rapid deployment of advanced propulsion and waste heat recovery systems. Additionally, demand is supported by export-oriented shipping operators focusing on efficiency upgrades to remain competitive under EU emission regulations.

Asia Pacific

The Asia Pacific region reached USD 3.96 billion in 2025, leading as the largest market share globally. Adoption in Asia Pacific is driven by the region’s dominance in global shipbuilding, where energy efficiency systems are increasingly integrated into new-build vessels in China, South Korea, and Japan. Additionally, rising pressure from international trade partners and emission compliance requirements is accelerating retrofit demand across existing fleets.

India Ship Energy Efficiency Systems Market

The Indian market in 2025 reached at USD 0.51 billion, accounting for roughly 5.27% of global revenues.

Adoption in India is driven by port modernization initiatives and stricter compliance with IMO efficiency regulations, particularly for coastal and inland vessels. Additionally, increasing focus on cost optimization in domestic shipping operations is encouraging the uptake of retrofit-based energy efficiency solutions.

China Ship Energy Efficiency Systems Market

China’s market is projected to be significant worldwide, with 2025 revenues around USD 1.31 billion, representing roughly 13.50% of the global revenues.

Japan Ship Energy Efficiency Systems Market

The Japanese market in 2025 valued at USD 0.71 billion, accounting for roughly 7.35% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space in the long term. The Latin America market is set to reach a valuation of USD 0.96 billion in 2025.

Adoption in Latin America is driven by fuel cost sensitivity in bulk and commodity export routes, pushing operators to invest in propulsion and voyage optimization systems.

Brazil Ship Energy Efficiency Systems Market

Brazil's market reached a value of USD 0.46 billion in 2025, representing roughly 4.78% of the market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market is set to reach a valuation of USD 0.57 billion in 2025.

Adoption in the Middle East & Africa is driven by high fuel consumption in long-haul oil and gas shipping routes, encouraging investment in propulsion and efficiency optimization systems. Additionally, expanding port infrastructure and regional trade corridors are supporting the gradual uptake of retrofit and digital energy management solutions.

GCC Ship Energy Efficiency Systems Market

The GCC market reached a value of USD 0.30 billion in 2025, representing roughly 3.05% of the global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players are Actively Expanding their Share Via Partnerships, Business Expansion, and Technological Advancements

The global ship energy efficiency systems market holds a consolidated market structure, constituting prominent players such as Wärtsilä Corporation, MAN Energy Solutions, Alfa Laval AB, and others. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in February 2023, MAN Energy Solutions introduced an upgraded waste heat recovery (WHR) system for large container vessels, designed to convert exhaust heat into usable energy. The system improves engine efficiency and reduces auxiliary fuel consumption. This deployment supports shipowners in meeting EEXI compliance targets while lowering overall energy demand during long-haul operations.

Other key players in the global market include Becker Marine Systems GmbH, Kongsberg Gruppen, Siemens Energy, ABB Ltd., and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY SHIP ENERGY EFFICIENCY SYSTEMS COMPANIES PROFILED

- Wärtsilä Corporation (Finland)

- MAN Energy Solutions (Germany)

- Alfa Laval AB (Sweden)

- Becker Marine Systems GmbH (Germany)

- Kongsberg Gruppen (Norway)

- Siemens Energy (Germany)

- ABB Ltd. (Switzerland)

- Caterpillar Inc. (U.S)

- Norsepower Oy Ltd. (Finland)

- Hyundai Heavy Industries (South Korea)

KEY INDUSTRY DEVELOPMENTS

- November 2023: Kongsberg Maritime deployed its Vessel Energy Management System (VEMS) on offshore support vessels, integrating automation, propulsion control, and energy monitoring. The system enables real-time optimization of power distribution and fuel consumption based on operational demands. This initiative supports improved efficiency in dynamic positioning operations and reduces unnecessary energy usage.

- April 2023: Becker Marine Systems implemented its Becker Mewis Duct® propulsion efficiency device on bulk carriers operating in Asia-Europe routes. The technology improves propeller inflow and reduces energy losses, leading to measurable fuel savings. The deployment was focused on achieving compliance with EEXI regulations while enhancing propulsion performance without major structural changes.

- March 2023: ABB installed its Azipod® electric propulsion system on a series of cruise vessels, enhancing propulsion efficiency and maneuverability. The system reduces fuel consumption by optimizing thrust and minimizing hydrodynamic losses. This initiative supports shipowners in achieving long-term goals.

- January 2023: Siemens Energy partnered with a European shipowner to provide integrated electric propulsion and energy storage systems for hybrid ferries. The solution combines battery systems with onboard power management to optimize fuel usage during varying load conditions. The project focused on reducing emissions and improving operational efficiency in short-sea shipping routes.

- September 2022: Alfa Laval delivered its E-PowerPack waste heat recovery solution for a fleet of tankers, enabling the conversion of excess heat into electrical power. The system reduces reliance on auxiliary engines and enhances overall energy efficiency. This initiative was part of a broader effort to optimize onboard energy utilization and reduce fuel consumption in high-load operating conditions, term efficiency improvements while complying with tightening environmental regulations.

REPORT COVERAGE

The global ship energy efficiency systems market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.11% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By System Type, Ship Type, Technology, and Region |

| By System Type |

|

| By Ship Type |

|

| By Technology |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.68 billion in 2025 and is projected to reach USD 28.84 billion by 2034.

In 2025, the market value of Asia Pacific stood at USD 3.96 billion.

The market is expected to exhibit a CAGR of 13.11% during the forecast period?

The propulsion efficiency systems segment led the market by system type.

Stringent IMO regulations, rising fuel cost pressures, and increasing demand for data-driven vessel performance optimization are the key factors driving the market.

Wärtsilä Corporation, MAN Energy Solutions, and Alfa Laval AB are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Regulatory compliance requirements, charter competitiveness linked to efficiency ratings, and availability of retrofit-friendly technologies are expected to favor the adoption of ship energy efficiency systems.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us