Silicon-Carbon Battery Market Size, Share & Industry Analysis, By Battery Type (Lithium-ion Si-C Batteries, Lithium Polymer Si-C Batteries, Solid-State Si-C Batteries, and Others), By Capacity Range (Below 3,000 mAh, 3,000–10,000 mAh, 10,000–50,000 mAh, Above 50,000 mAh, and Others), By Application (Consumer Electronics, Electric Vehicles (EVs), Energy Storage Systems, Industrial (Drones, Tools), and Others), By End User (Electronics Industry, Automotive, Energy & Utilities, Industrial Manufacturing, and Others), and Regional Forecast, 2026-2034

Silicon-Carbon Battery Market Size and Future Outlook

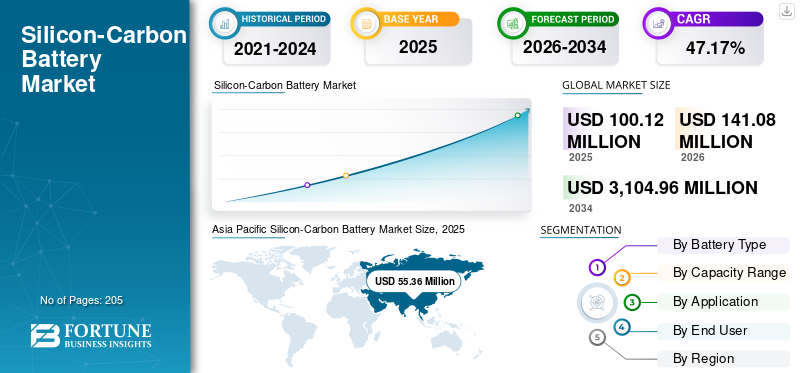

The global silicon-carbon battery market size was valued at USD 100.12 million in 2025. The market is projected to grow from USD 141.08 million in 2026 to USD 3,104.96 million by 2034, exhibiting a CAGR of 47.17% during the forecast period. Asia Pacific dominated the silicon-carbon battery market with a market share of 55.29% in 2025.

Silicon-carbon (Si-C) batteries are an advanced variant of lithium ion batteries that incorporate silicon within the anode structure (typically blended with graphite) to significantly enhance energy storage capacity. Unlike conventional graphite anodes, silicon enables higher lithium-ion uptake, resulting in 20–50% higher energy density and improved fast-charging performance, making it particularly attractive for electric vehicles and high-end consumer electronics.

The primary drivers for Si-C battery adoption include the increasing demand for extended EV driving range, where high energy density batteries directly translates to fewer charging cycles, and the need for the fast charging batteries in smartphone wearables with longer battery life. Additionally, OEMs are actively integrating silicon-based anodes to meet stringent performance benchmarks without increasing battery size, while ongoing advancements in material engineering are improving cycle stability. Rising investments by battery manufacturers and partnerships across the EV value chain are further accelerating the commercialization of Si-C technology.

- For instance, in March 2024, Group14 Technologies announced the expansion of its silicon-carbon battery material production facility in Washington, U.S., to meet rising demand from electric vehicle and consumer electronics manufacturers. The company scaled up production of its proprietary SCC55 silicon-carbon composite anode material, which enables higher energy density and faster charging compared to traditional graphite. This expansion reflects increasing commercialization momentum of silicon-carbon batteries and growing adoption by OEMs seeking performance improvements in next-generation lithium-ion batteries.

Some of the leading companies operating in the industry include Sila Nanotechnologies, Group14 Technologies, Amprius Technologies, CATL, and others. Sila Nanotechnologies is a leading U.S.-based advanced battery materials company specializing in silicon-carbon anode technology for next-generation lithium-ion batteries. The company develops high-performance silicon-based materials that replace traditional graphite anodes, enabling higher energy density and faster charging. Sila is actively partnering with automotive OEMs and electronics manufacturers to commercialize silicon-carbon batteries at scale.

Download Free sample to learn more about this report.

Silicon-Carbon Battery Market KEY TAKEAWAYS

- 2025 Market Size: USD 100.12 million

- 2026 Market Size: USD 141.08 million

- 2034 Forecast Market Size: USD 3,104.96 million

- CAGR: 47.17% from 2026–2034

- Asia Pacific dominated the silicon-carbon battery market with a 55.29% share in 2025.

- The advanced solid-state Si-C batteries segment is projected to grow at a CAGR of 50.70% during the forecast period.

- The above 50,000 mAh segment is anticipated to grow at a CAGR of 49.87% during the forecast period.

Asia Pacific

Asia Pacific reached USD 55.36 million in 2025, driven by strong battery manufacturing capacity and rapid EV adoption.

North America

North America reached USD 21.35 million in 2025, supported by leading silicon anode developers and advanced battery R&D.

Europe

Europe reached USD 19.33 million in 2025, driven by battery localization initiatives and expanding EV manufacturing.

U.S.

The market reached USD 18.65 million in 2025, supported by increasing commercialization of silicon-anode battery technologies.

Japan

The market reached USD 8.07 million in 2025, supported by strong battery innovation and advanced electronics manufacturing.

Read More

SILICON-CARBON BATTERY MARKET TRENDS

Rising Integration of Silicon-Dominant Anodes in High-Performance Battery Applications is the Key Market Trend

The market is witnessing a clear shift from low-percentage silicon blending toward higher silicon-content anodes, particularly in applications demanding superior energy density and fast-charging capabilities. Battery manufacturers are increasingly moving from conventional ~5% silicon incorporation to 10–20% silicon blends, driven by the need to enhance performance without significantly altering existing lithium-ion manufacturing infrastructure. This trend is most evident in premium smartphones and electric vehicles, where OEMs are prioritizing longer battery life and reduced charging time as key differentiators.

Additionally, companies are focusing on engineered silicon-carbon composites (such as SiOx and porous silicon structures) to mitigate expansion-related degradation, enabling gradual commercialization at scale. Strategic partnerships between silicon anode battery market developers and major cell manufacturers are accelerating this transition, with pilot deployments already visible in select EV models and high-end consumer devices. Furthermore, advancements in binder chemistry and electrolyte formulations are supporting higher silicon loading, making the technology more viable for mass-market applications. This evolving material innovation landscape is expected to redefine battery performance benchmarks over the next decade.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for High-Energy-Density and Fast-Charging Battery Solutions Across Consumer Electronics is the Key Market Driver

The silicon-carbon battery market growth is primarily driven by demand for compact electric vehicles, increasing performance gap between conventional graphite-based lithium-ion batteries and next-generation energy storage requirements, particularly in electric vehicles (EVs) and premium consumer electronics. As EV manufacturers aim to extend driving range without increasing battery pack size or weight, Si-C anodes offer a practical pathway by delivering higher gravimetric energy density, directly improving vehicle efficiency. Additionally, the demand for ultra-fast charging capabilities is accelerating the adoption of silicon-based materials, as they enable faster lithium-ion diffusion compared to graphite.

In the consumer electronics segment, OEMs are under pressure to deliver longer battery life within compact form factors, especially in high-end smartphones and laptops, where Si-C technology allows capacity enhancement without increasing device thickness. Furthermore, advancements in silicon stabilization techniques (such as nano-structuring and composite engineering) are reducing degradation issues, making the technology more commercially viable. Strategic investments and long-term supply agreements between silicon anode developers and battery manufacturers are also supporting scale-up, reinforcing the transition toward silicon-carbon batteries across high-performance applications. These factors are anticipated to drive the CAGR during the forecast period.

MARKET RESTRAINTS

Technical Challenges Related to Silicon Expansion and Cycle Life Degradation to Hamper Market Demand

The growth of the silicon-carbon (Si-C) battery market is constrained by intrinsic material limitations associated with silicon anode battery technology, particularly their significant volume expansion (up to ~300%) during charge-discharge cycles. This expansion leads to mechanical stress, particle fracture, and loss of electrical contact, ultimately resulting in rapid capacity fade and reduced battery lifespan. Despite advancements in silicon-carbon composite structures and nano-engineering techniques, maintaining long-term cycle stability at higher silicon content remains a critical challenge.

Additionally, the integration of silicon into existing lithium-ion battery architectures requires specialized binders, electrolytes, and electrode designs, increasing manufacturing complexity and cost. These technical barriers limit large-scale commercialization, especially in applications such as electric vehicles, where long cycle life and reliability are essential.

MARKET OPPORTUNITIES

Emerging Opportunities in Supply Chain Localization and Silicon Anode Material Scaling Drive Demand

The market is creating new opportunities through the localization of battery supply chains and scaling of advanced anode material production, particularly in regions aiming to reduce dependence on graphite imports. Governments and OEMs are increasingly investing in domestic silicon anode manufacturing capabilities, supported by incentives and funding programs targeting next-generation battery materials. This shift is encouraging the development of dedicated silicon processing facilities and integrated production ecosystems, especially in North America and Europe.

Additionally, the transition toward silicon-based anodes is enabling new entrants and material startups to capture value within the battery value chain, which has traditionally been dominated by established graphite suppliers. As production processes mature and economies of scale improve, companies focusing on proprietary silicon-carbon composites and manufacturing techniques are well-positioned to secure long-term supply agreements.

MARKET CHALLENGES

Scalability and Cost Constraints in Commercializing Silicon-Carbon Anode Materials

One of the key challenges in the market is the difficulty in scaling production of high-quality silicon anode materials while maintaining cost competitiveness with conventional graphite. Manufacturing Si-C anodes requires precise material engineering, specialized coatings, and advanced processing techniques, which increase production complexity and limit large-scale output. Additionally, ensuring uniform performance across batches remains challenging, particularly when increasing silicon content.

Another critical issue is the lack of established large-scale supply chains for silicon anode materials, leading to dependency on a limited number of specialized suppliers. This creates bottlenecks in meeting growing demand from EV and electronics manufacturers.

Segmentation Analysis

By Battery Type

Lithium-ion Si-C Batteries Dominate Due to Existing Li-Ion Infrastructure Compatibility

Based on the segmentation of battery type, the market is classified into lithium-ion Si-C batteries, lithium polymer Si-C batteries, solid-state Si-C batteries, and others.

In 2025, the lithium-ion Si-C batteries dominated the silicon-carbon battery market share as they can be seamlessly integrated into existing lithium-ion manufacturing lines, avoiding the need for major infrastructure changes. Battery manufacturers prefer this approach due to lower transition costs and faster commercialization. Additionally, these batteries offer incremental performance improvements such as higher energy density and faster charging, making them suitable for immediate deployment across consumer electronics and electric vehicles without significant redesign.

The advanced solid-state Si-C batteries segment is experiencing the highest growth and is expected to grow at a CAGR of 50.70% over the study period.

To know how our report can help streamline your business, Speak to Analyst

By Capacity Range

3,000–10,000 mAh Dominates Due to Large-Scale Energy Demand

Based on the segmentation of the capacity range, the market is classified into below 3,000 mAh, 3,000–10,000 mAh, 10,000–50,000 mAh, above 50,000 mAh, and others.

In 2025, the 3,000–10,000 mAh segment dominated the global market. This growth is primarily due to its widespread use in smartphones, tablets, and portable consumer electronics, where demand volumes are highest. OEMs are increasingly adopting Si-C technology in this range to deliver longer battery life and faster charging without increasing device size. This segment benefits from rapid product cycles and early technology integration compared to larger-capacity applications such as EVs.

The above 50,000 mAh segment is expected to grow at a CAGR of 49.87% over the study period.

By Application

Consumer Electronics Segment Dominates Due to Short Product Cycles and High Performance

Based on the segmentation of the application, the market is classified into consumer electronics, Electric Vehicles (EVs), energy storage systems, industrial (drones, tools), and others.

In 2025, the consumer electronics segment dominated the global market. Consumer electronics dominate the market as they are the first application segment to adopt emerging battery technologies at scale, driven by shorter product cycles and high performance requirements. Smartphone and laptop manufacturers are integrating Si-C anodes to achieve higher energy density and faster charging without increasing device size, making this segment the primary commercialization pathway before large-scale EV adoption.

The Electric Vehicles (EVs) segment is expected to grow at a CAGR of 49.86% over the study period.

By End User

Electronics Industry is Dominant Due to High-Volume Device Manufacturing

On the basis of the segmentation of the end user, the market is classified into electronics industry, automotive, energy & utilities, industrial manufacturing, and others.

In 2025, the electronics industry segment dominated the global market due to its large-scale production of smartphones, laptops, and portable devices, which require continuous improvements in battery performance. Manufacturers are rapidly integrating Si-C technology to achieve higher energy density and compact designs. The industry’s fast innovation cycles and ability to absorb new technologies earlier than other sectors further strengthen its leading position.

The automotive segment is expected to grow at a CAGR of 48.77% over the study period.

Silicon-Carbon Battery Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Silicon-Carbon Battery Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached USD 55.36 million in 2025 and secured the largest share of the market. Asia Pacific leads the market due to its dominance in battery manufacturing capacity, particularly in China, South Korea, and Japan, where major players are actively integrating silicon-based anodes. The region also benefits from a well-established supply chain for battery materials and large-scale EV production, accelerating early adoption and commercialization of Si-C technology.

India Silicon-Carbon Battery Market

The India market size in 2025 is estimated at around USD 3.57 million, accounting for roughly 3.56% of global revenues.

India is emerging in the Si-C battery market due to increasing investments in domestic battery manufacturing under PLI schemes and a growing focus on advanced cell chemistries. Additionally, rising EV adoption and localization efforts are encouraging early-stage integration of silicon-based anode technologies.

China Silicon-Carbon Battery Market

China’s market is projected to be significant worldwide, with 2025 revenues recorded at around USD 26.87 million, representing roughly 26.84% of the global market.

Japan Silicon-Carbon Battery Market

The Japan market in 2025 was valued at around USD 8.07 million, accounting for roughly 8.06% of global revenues.

North America

North America held the second-highest share in 2025, valued at USD 21.35 million, and is also expected to take a significant share in 2026 with USD 29.83 million.

North America market’s growth is due to its strong concentration of silicon anode technology developers and early-stage commercialization activities. The region is home to key players such as Sila Nanotechnologies, Group14 Technologies, and Amprius, which are actively scaling production and securing supply agreements with automotive and consumer electronics OEMs. Additionally, the presence of advanced R&D infrastructure and national laboratories supports continuous innovation in silicon-based materials.

U.S. Silicon-Carbon Battery Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 18.65 million in 2025, accounting for roughly 18.63% of the global market size.

Europe

Europe is projected to record a growth rate of 50.06% in the coming years, which is the third-highest among all regions, and reached a valuation of USD 19.33 million in 2025. The market in Europe is primarily driven by the region’s aggressive push to localize the battery value chain, particularly reducing reliance on imported graphite and critical materials. The European Union is actively supporting next-generation anode material development, including silicon-based technologies, through initiatives such as the European Battery Alliance and IPCEI projects. Additionally, the rapid expansion of EV manufacturing hubs in Germany and France is creating demand for higher energy density batteries to meet performance and regulatory requirements.

Germany Silicon-Carbon Battery Market

The Germany market in 2025 was valued at around USD 6.63 million 2025 and is estimated at around USD 9.63 million in 2026, representing roughly 6.62% of the global revenues. Germany is a key driver in the market due to its strong automotive OEM base (Volkswagen, BMW, Mercedes-Benz) actively seeking higher energy density solutions for next-generation EV platforms. Additionally, increasing investments in gigafactories and collaborations with advanced battery material companies are accelerating the integration of silicon-based anodes within domestic battery supply chains.

Rest of the World

The rest of the world is expected to witness moderate growth in this market space during the forecast period. The rest of the world market reached a valuation of USD 4.08 million in 2025.

The rest of the world market is gradually adopting Si-C batteries, driven by growing EV penetration in Latin America and the Middle East, along with increasing interest in advanced energy storage solutions. However, adoption remains limited due to a lack of local manufacturing infrastructure and dependence on imports for advanced battery technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Actively Expanding Market Share via Partnerships, Business Expansion, and Technological Advancements

The global silicon-carbon battery market holds a consolidated market structure, constituting prominent players such as Sila Nanotechnologies, Group14 Technologies, Amprius Technologies, and CATL, among others. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in January 2024, Sila Nanotechnologies announced the commencement of construction for its large-scale silicon anode manufacturing facility in Moses Lake, Washington. The facility is designed to produce silicon-carbon materials for electric vehicle batteries on a commercial scale. This development marks a critical step toward mass adoption, as Sila aims to supply next-generation anode materials to automotive OEMs, enabling higher energy density and improved battery performance.

Other key players in the global market include Panasonic Corporation, LG Energy Solution, Samsung SDI, and Enovix Corporation, among others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY SILICON-CARBON BATTERY COMPANIES PROFILED

- Sila Nanotechnologies (U.S.)

- Group14 Technologies (U.S.)

- Amprius Technologies (U.S.)

- CATL (China)

- Panasonic Corporation (Japan)

- LG Energy Solution (South Korea)

- Samsung SDI (South Korea)

- Enovix Corporation (U.S.)

- Enevate Corporation (U.S.)

- Nexeon Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Nexeon Limited announced progress in scaling its silicon anode materials for electric vehicle applications through partnerships with global battery manufacturers. The company focused on improving cycle life and energy density using engineered silicon-carbon composites. This development highlights increasing collaboration between material innovators and cell manufacturers to accelerate the commercialization of silicon-based anode technologies in next-generation lithium-ion batteries.

- February 2024: LG Energy Solution announced ongoing development of silicon-based anode technologies aimed at enhancing energy density in electric vehicle batteries. The company is working on increasing silicon content while addressing cycle life challenges through material optimization. This initiative reflects major battery manufacturers’ commitment to incorporating silicon-carbon advancements into next-generation EV battery platforms.

- October 2023: Samsung SDI announced ongoing research and development efforts focused on increasing silicon content in lithium-ion battery anodes for electric vehicles. The company is working to enhance battery capacity while maintaining stability through advanced material engineering. This initiative underscores the commitment of leading battery manufacturers to incorporate silicon-carbon technologies into future battery platforms.

- September 2023: Enovix Corporation began scaling production of its silicon-based battery cells at its manufacturing facility, targeting consumer electronics and wearable devices. The company’s architecture incorporates silicon-dominant anodes to improve energy density while maintaining compact form factors. This milestone highlights increasing industry focus on integrating silicon-carbon technologies into commercial battery products.

- June 2023: Amprius Technologies announced the shipment of its high-energy-density silicon anode batteries to customers in the aviation and defense sectors. These batteries utilize advanced silicon-carbon structures to deliver significantly higher energy density compared to traditional lithium-ion cells. The development demonstrates early adoption of silicon-based anodes in specialized high-performance applications, paving the way for broader commercialization.

REPORT COVERAGE

The global silicon-carbon battery market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 47.17% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Battery Type, Capacity Range, Application, End User, and Region |

| By Battery Type |

|

| By Capacity Range |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 100.12 million in 2025 and is projected to reach USD 3,104.96 million by 2034.

In 2025, the market value stood at USD 55.36 million.

The market is expected to exhibit a CAGR of 47.17% during the forecast period.

The lithium-ion Si-C batteries segment led the market by battery type.

The increasing demand for high energy density and fast-charging batteries in electric vehicles and advanced consumer electronics is driving the market.

Sila Nanotechnologies, Group14 Technologies, Amprius Technologies, and CATL are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Advancements in silicon anode stabilization, rising EV range requirements, and OEM integration of high-performance battery materials are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us