Silicon Tetrachloride Market Size, Share & Industry Analysis, By Grade (Technical Grade and Electronic Grade), By Application (Fumed Silica, Poly Silicon, Optical Fiber, Chemical Intermediate, and Others), By End-Use Industry (Semiconductors & Electronics, Solar, Telecommunications, Silicon Chemicals, and Others), and Regional Forecast, 2026-2034

Silicon Tetrachloride Market Size and Future Outlook

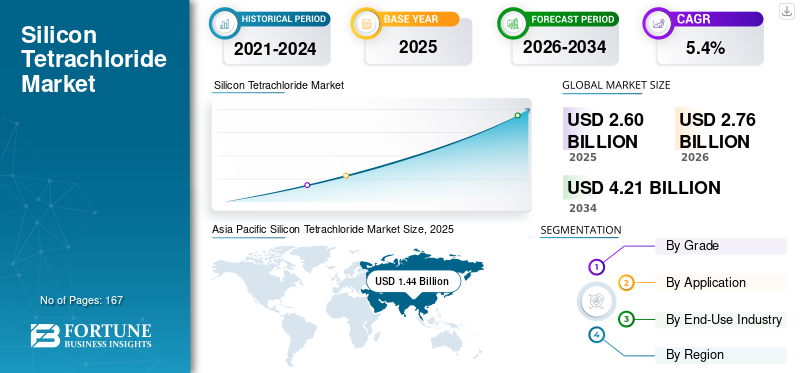

The global silicon tetrachloride market size was valued at USD 2.60 billion in 2025. The market is projected to grow from USD 2.76 billion in 2026 to USD 4.21 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the silicon tetrachloride market with a market share of 55.38% in 2025.

Silicon tetrachloride (SiCl4) is a chlorosilane compound utilized as a crucial intermediary in the production of fumed silica, optical fiber preforms, synthetic quartz glass, semiconductor-related silicon materials, and selected silicon chemical intermediates. It is also produced during chlorosilane-based polysilicon manufacturing; however, a substantial portion of this volume is typically recovered and reconverted to trichlorosilane within integrated process loops.

The market is bolstered by increasing demand for high-purity silicon materials across semiconductor manufacturing, telecommunications infrastructure, and downstream silicon chemicals. The World Semiconductor Trade Statistics organization forecasted that the global semiconductor market will attain USD 700.9 billion in 2025. Additionally, Tokuyama’s fiscal year 2025 business briefing emphasized that demand for optical fiber is driven by cables connecting servers within and between AI data centers, where high-purity silicon tetrachloride remains a crucial precursor.

The market is dominated by several major players, including Tokuyama Corporation, PCC Group, Evonik Industries AG, Hemlock Semiconductor, Wacker Chemie AG, Merck KGaA, and OCI, which are at the forefront of the industry. Strong positions in high-purity chlorosilanes, specialty silicon chemicals, optical-fiber materials, and semiconductor-related silicon intermediates have substantiated their global market presence.

Download Free sample to learn more about this report.

SILICON TETRACHLORIDE MARKET TRENDS

High-Purity and Application-Specific Grades are Reshaping Market Growth

A notable trend in the market is the shift from general industrial chlorosilane applications to more specialized, high-purity grades for optical fibers, semiconductor materials, and advanced silicon chemistry. Tokuyama specifically markets SiCl4 for synthetic quartz glass, optical fiber, and silica-related applications. In contrast, Merck offers SiCl4 as part of its semiconductor-focused range, emphasizing its role as an intermediate in the production of hyper-pure polysilicon. This shift indicates that market growth now hinges not only on chemical volume but also on purity levels, distillation techniques, and the preservation of quality in high-specification applications.

Investment activities in semiconductor-grade silicon materials further support the trend. Wacker inaugurated a new production line for ultra-pure semiconductor-grade polysilicon at Burghausen in 2025 and announced that its long-term capacity for the highest semiconductor-grade quality will increase by more than 50%. As SiCl4 remains a significant intermediate in chlorosilane-based silicon purification, these investments indirectly enhance demand for higher-purity SiCl4 and support technologies across the entire value chain.

The demand for optical fibers is emerging as a significant avenue for the silicon tetrachloride market growth. Tokuyama’s Fiscal Year 2025 business briefing indicates that optical fiber, predominantly manufactured from high-purity silicon tetrachloride, is experiencing increased demand driven by applications such as AI data center interconnections. Consequently, the market is becoming progressively more specialized, with value increasingly oriented toward quality-sensitive, technology-intensive end-use applications rather than solely toward bulk industrial trade.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Semiconductor and Optical-Fiber Growth is Increasing Demand for High-Purity SiCl4

Silicon tetrachloride is gaining increasing significance in semiconductor-related silicon processing and optical fiber manufacturing, where high purity, impurity control, and process reliability are paramount. Merck recognizes SiCl4 as an intermediate in the production of ultra-pure polysilicon, whereas Tokuyama explicitly associates it with synthetic quartz and optical fiber applications. These applications are elevating the importance of SiCl4 as a material dictated by specific specifications.

Macro demand signals support this trajectory. The World Semiconductor Trade Statistics forecast indicates continued growth in the global semiconductor market in 2025, while Wacker’s expansion in semiconductor-grade polysilicon highlights stronger demand for ultra-pure silicon feedstocks used in next-generation chips and AI-related applications. Consequently, demand for SiCl4 is positively impacted by both increasing semiconductor production and higher material requirements in premium-grade silicon applications.

Meanwhile, the optical-fiber supply chain is emerging as a significant growth catalyst. Tokuyama’s fiscal year 2025 business materials indicate that optical fiber, predominantly manufactured from high-purity silicon tetrachloride, is experiencing increased demand driven by AI and data center infrastructure. Consequently, the market is sustained by the expansion of electronics and broader investments in digital communications networks.

MARKET RESTRAINTS

Captive Recycling in Polysilicon Production Limits External Volume

A significant market constraint is that a substantial portion of the compound produced during chlorosilane-based polysilicon manufacturing is not marketed externally; instead, it is recovered and reconverted into trichlorosilane. Hemlock Semiconductor explicitly states that silicon tetrachloride is recovered and reconverted to trichlorosilane, which serves as the primary raw material in the process, while Wacker also details highly integrated material loops in polysilicon production. This internal recycling pattern markedly restricts the scale of the externally traded market.

Consequently, the overall process throughput for SiCl4 significantly exceeds that of the market. This limitation hampers the expansion of the primary market, especially within the solar and polysilicon value chain, where material circulation is substantial but external commercial sales are comparatively constrained. Therefore, growth within the sector is more heavily reliant on downstream applications such as fumed silica, optical fiber, synthetic quartz, and semiconductor materials, rather than on total polysilicon production alone.

SiCl4 is highly reactive with moisture and therefore requires specialized handling, storage, and transportation procedures. According to CAMEO Chemicals, the substance decomposes upon contact with water, producing hydrochloric acid and heat. This reactivity can limit logistical flexibility and impose additional compliance requirements on both suppliers and end users.

MARKET OPPORTUNITIES

AI Infrastructure, Fiber Optics, and Semiconductor Purity Upgrades are Expanding Premium Use Cases

A significant opportunity arises in the use of high-purity silicon tetrachloride across the optical fiber, quartz, and advanced semiconductor value chains. Tokuyama’s fiscal year 2025 business briefing indicates that optical fiber production chiefly relies on high-purity SiCl4, and it notes the rising demand for cables connecting servers and data centers. This scenario offers promising prospects for suppliers who can ensure superior impurity control, maintain consistent purification standards, and deliver higher-performance grades.

The semiconductor industry is additionally establishing new premium demand channels. Wacker’s expansion in semiconductor-grade polysilicon and Merck’s positioning in silicon materials tailored for semiconductors suggest that future growth is likely to be concentrated in higher-value, specification-sensitive demand rather than in broad commodity-like sales. This development enhances the market outlook for suppliers possessing robust purification capabilities and advanced customer support.

Producers with downstream integration into specialty silica, optical fiber materials, and semiconductor-grade silicon chemistry are well positioned to capture additional value. Tokuyama’s business materials, for instance, link its silica and optical-material operations to broader semiconductor and information-electronics demand, demonstrating the strategic importance of SiCl4 within higher-value downstream material ecosystems.

MARKET CHALLENGES

Purity Control, Hazard Management, and Qualification Requirements Continue to Raise Execution Complexity

The market faces persistent challenges in maintaining exceptionally high purity while handling a chemically aggressive substance. Given that this compound is utilized in optical fiber production, silicon processing for semiconductor applications, and synthetic quartz manufacturing, contamination control remains paramount. Both Tokuyama and Merck categorize SiCl4 in the high-purity materials sector, where the quality of distillation, trace impurity management, and batch consistency directly impact subsequent performance.

Simultaneously, the hazardous properties of SiCl4 increase operational complexity. The substance exhibits vigorous reactivity with moisture and can emit corrosive hydrochloric acid, thereby elevating containment, transportation, and safe process integration standards. These restrictions result in heightened supplier expenses and diminish the pool of qualified market participants capable of serving sensitive end-use applications.

Furthermore, qualification cycles can be challenging in optical-fiber and semiconductor-related applications, where long-term purity stability, process compatibility, and reproducibility are critical. Suppliers must, therefore, compete not solely on price but also on technical capability, purification standards, and customer qualification support. This situation elevates barriers to entry and consolidates market dominance among established high-purity entities.

Segmentation Analysis

By Grade

Technical Grade Segment Led Market Due to Its Extensive Use in Fumed Silica Manufacturing

Based on grade, the market is segmented into technical grade and electronic grade.

The technical grade segment held the largest market share in 2025, driven by its extensive use in fumed silica manufacturing, specialty silicon chemicals, and intermediate silicon processing methods. PCC explicitly designates SiCl4 as the primary raw material for fumed silica production and as a precursor in silicon-based industrial procedures, thereby reinforcing the predominant role of technical-grade material in the trade.

The electronic grade segment is anticipated to attain the highest CAGR throughout the forecast period. This expansion is driven by increasing demand for semiconductor materials, optical fiber preforms, and high-purity polysilicon, where impurity control and process quality are paramount. Merck’s semiconductor-oriented SiCl4 product and Tokuyama’s strategic positioning in optical fiber and quartz industries bolster more robust long-term growth prospects for electronic-grade and specialty-purity SiCl4.

By Application

Increased SiCl4 Usage for Fumed Silica Production Boosted Segment Growth

Based on application, the market is segmented into fumed silica, optical fiber, poly silicon, chemical intermediate, and others.

The fumed silica segment accounted for the largest market share in 2025, supported by the direct use of SiCl4 as a primary feedstock in the production of pyrogenic silica. PCC Group explicitly states that SiCl4 is the principal raw material employed in the manufacturing of fumed silica. At the same time, Tokuyama designates it as a raw material for REOLOSIL and related silica products.

The optical fiber segment is expected to grow significantly during the forecast period. This growth is driven by the increasing deployment of optical interconnects in artificial intelligence (AI) data centers, cloud infrastructure, and telecommunications networks. Tokuyama’s fiscal year 2025 business briefing explicitly highlights that optical fiber is predominantly manufactured from high-purity SiCl4, and that demand for cables is increasing in AI infrastructure applications.

The poly silicon segment continues to hold strategic importance; however, it accounts for a relatively small share of the market compared to its significance in the process. Both Hemlock and Wacker have indicated that SiCl4 is extensively recovered and reused in chlorosilane-based polysilicon manufacturing, thereby reducing the volume available for external trade. As a result, polysilicon remains highly pertinent from a process-flow perspective, yet its market dominance is comparatively lower.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Silicon Chemicals Led Market Driven by Extensive Use of SiCl4

In terms of end-use industry, the market is categorized into semiconductors & electronics, solar, telecommunications, silicon chemicals, and others.

The silicon chemicals segment accounted for the largest silicon tetrachloride market share in 2025, driven by the extensive use of SiCl4 in the manufacturing of fumed silica, synthetic quartz, and other downstream silicon intermediates. PCC and Tokuyama both explicitly associate SiCl4 with these applications, thereby affirming that specialty silicon chemicals remain the primary external demand sector in the market.

The semiconductors & electronics segment is projected to achieve the highest compound annual growth rate (CAGR) throughout the forecast period. Merck designates SiCl4 for use in semiconductor materials and hyper-pure polysilicon processing. In contrast, Wacker’s expansion of semiconductor-grade polysilicon exemplifies ongoing investments in ultra-pure silicon feedstocks for advanced chip manufacturing and artificial intelligence (AI)-related electronics.

The telecommunications sector sustains a significant market share owing to its utilization of silicon tetrachloride in the manufacturing of optical fibers and preforms, where high-purity chlorosilanes are critical for optimal material performance. The solar sector holds a comparatively small share of the market, primarily as a considerable portion of the SiCl4 produced during polysilicon manufacturing is recycled internally rather than sold externally.

Silicon Tetrachloride Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Silicon Tetrachloride Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the dominant share, valued at USD 1.33 billion, and continued to lead in 2025, with a valuation of USD 1.44 billion. The region remains the primary demand center, supported by its concentration of optical-fiber manufacturing, semiconductor materials processing, specialty silicon chemicals, and integrated chlorosilane value chains. Tokuyama’s direct involvement in optical fiber, quartz, and silica applications, along with the extensive presence of semiconductor and silicon materials supply chains in Japan, China, South Korea, and Malaysia, has fortified the region’s market standing. By 2026, the Chinese market is projected to reach USD 0.43 billion.

China Silicon Tetrachloride Market

China is among the largest demand hubs within the Asia Pacific region, propelled by its extensive electronics manufacturing infrastructure, specialized silicon processing capabilities, and comprehensive photovoltaic and semiconductor ecosystems. Although a significant portion of silicon tetrachloride remains confined within integrated polysilicon loops, China continues to wield considerable influence over overall market dynamics due to its scale in silicon-related supply chains. The IEA PVPS reports that China exceeded one terawatt of cumulative photovoltaic capacity in 2024, highlighting its pivotal role within silicon material ecosystems.

To know how our report can help streamline your business, Speak to Analyst

Japan Silicon Tetrachloride Market

The Japan market in 2026 is estimated to be around USD 0.53 billion, accounting for roughly 19.3% of the global revenues.

India Silicon Tetrachloride Market

The India market in 2026 is estimated at around USD 0.04 billion, accounting for roughly 1.4% of global revenues.

Europe

Europe is expected to experience steady market growth over the forecast period. The region benefits from a robust foundation in specialty chemicals, high-purity silicon materials, and semiconductor-grade polysilicon. Germany serves as the primary regional hub, with Wacker and Merck strategically positioned in the high-purity semiconductor and polysilicon supply chains. During the forecast period, the European region is projected to grow at a 3.5% rate and reach a valuation of USD 0.67 billion in 2026.

U.K. Silicon Tetrachloride Market

The U.K. market in 2026 is estimated at around USD 0.05 billion, accounting for roughly 2.0% of global revenues.

Germany Silicon Tetrachloride Market

Germany’s market in 2026 is estimated at around USD 0.44 billion, accounting for roughly 15.8% of global revenues.

North America

The North American market is anticipated to expand steadily throughout the forecast period. North America is recognized as a key technological market, underpinned by semiconductor manufacturing, substantial demand for high-purity materials, and specific applications of silicon chemicals. Hemlock Semiconductor is a principal entity in the region, supplying SiCl4 to semiconductor and fiber-optic clients while concurrently engaging in substantial internal recycling. Projections indicate that by 2026, the U.S. market will reach USD 0.43 billion.

U.S. Silicon Tetrachloride Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 0.43 billion in 2026, accounting for roughly 15.6% of global sales.

Latin America and Middle East & Africa

Throughout the forecast period, the Latin America and Middle East & Africa regions are anticipated to experience moderate growth within this market. While these regions are relatively smaller, they are witnessing a gradual increase in demand driven by imported silicon chemicals, industrial processing applications, and specific telecommunications and specialty-material uses. Compared with Asia Pacific, Europe, and North America, these regions remain less integrated into the high-purity silicon value chain. The Latin America market is projected to reach USD 0.04 billion by 2026.

GCC Silicon Tetrachloride Market

The GCC market in 2026 is estimated at USD 0.02 billion, accounting for approximately 0.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

High-Purity Processing, Downstream Integration, and Application Support are Core Differentiators

The market demonstrates a moderate level of concentration, with competition influenced by factors such as purity capability, downstream integration, and application-specific technical support. Competitive advantage is founded on expertise in distillation and purification processes, reliability in supplying high-purity chlorosilanes, and engagement in downstream value chains, including fumed silica, optical fiber, semiconductor materials, and polysilicon-related silicon chemistry. Notable market participants include Tokuyama Corporation, PCC Group, Evonik Industries AG, Hemlock Semiconductor, Wacker Chemie AG, Merck KGaA, and OCI.

The market continues to be distinguished by suppliers' ability to ensure safe handling, maintain specification consistency, and achieve long-term customer qualification. Major established companies with direct involvement in optical-fiber preforms, specialty silica, semiconductor-grade polysilicon, or semiconductor materials generally maintain more robust positions compared to suppliers restricted to small-volume catalog sales. Consequently, strategic significance in this market is not solely predicated on bulk tonnage but also on active engagement in high-value, purity-sensitive applications.

LIST OF KEY SILICON TETRACHLORIDE COMPANIES PROFILED

- Tokuyama Corporation (Japan)

- PCC Group (Poland)

- Evonik Industries AG (Germany)

- Hemlock Semiconductor (U.S.)

- Wacker Chemie AG (Germany)

- Merck KGaA (Germany)

- OCI Company Ltd. (South Korea )

- American Elements (U.S.)

- TCI Chemicals (Japan)

- Gelest Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Wacker commissioned Etching Line Next at Burghausen for ultra-pure semiconductor-grade polysilicon, stating that long-term capacity for its highest semiconductor-grade quality will increase by more than 50%.

- July 2025: Tokuyama announced the establishment of OCI Tokuyama Semiconductor Materials Sdn. Bhd. (OTSM) in Malaysia to produce and sell semiconductor-grade polycrystalline silicon semi-finished products using clean energy.

- October 2024: Merck completed the Unity-SC acquisition, further expanding its semiconductor-related technology portfolio and sharpening the strategic focus of its electronics business.

- July 2024: Merck announced its planned acquisition of Unity-SC, strengthening its offering for AI-enabled semiconductors and deepening its semiconductor materials ecosystem.

- December 2023: Tokuyama and OCI formalized and advanced their joint venture for semiconductor-grade polysilicon in Malaysia, with an initial planned capacity of approximately 8,000 tons per year and a future expansion target of 10,000 tons per year.

REPORT COVERAGE

The global silicon tetrachloride market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.4% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Grade, Application, End-Use Industry, and Region |

| By Grade |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.60 million in 2025 and is projected to reach USD 4.21 million by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The silicon chemicals segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Semiconductor and optical-fiber growth is accelerating market expansion.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us