Skateboard Chassis Market Size, Share & Industry Analysis, By Platform Architecture (Single Motor Platform (2WD), Dual Motor Platform (AWD), and Multi-Motor Performance Platforms (3-4 motors)), By Chassis Material (Aluminum Skateboard Chassis, Steel Skateboard Chassis, Mixed Material Platforms, and Composite / Carbon Fiber Platforms), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Component Integration Level (Basic Skateboard Platforms, Integrated Skateboard Platforms, and Highly Integrated Platforms), and Regional Forecast, 2026-2034

Skateboard Chassis Market Size and Future Outlook

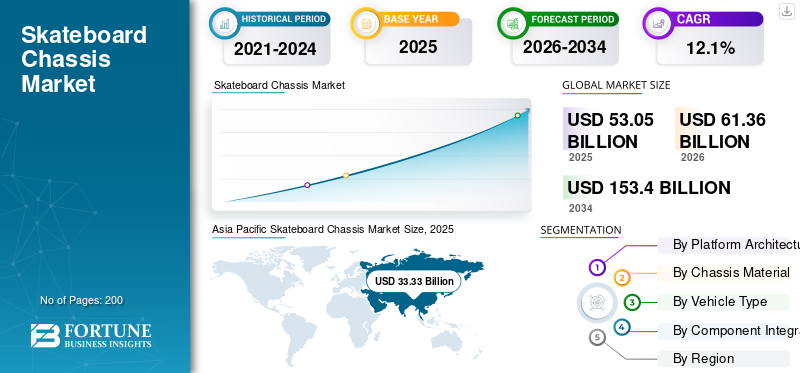

The global skateboard chassis market size was valued at USD 53.05 billion in 2025. The market is projected to grow from USD 61.36 billion in 2026 to USD 153.42 billion by 2034, with a CAGR of 12.1% over the forecast period. Asia Pacific dominated the skateboard chassis market with a market share of 62.83% in 2025.

A skateboard chassis is a flat, modular electric-vehicle platform that integrates the battery pack, e-drive system, suspension mounting points, steering, and structural underbody into one base. It enables multiple body styles to be built on the same platform, improving packaging efficiency, scalability, interior space, and manufacturing flexibility. The market is driven by rising EV production, growing use of dedicated electric platforms, demand for modular design vehicle architectures, and the shift toward larger battery packs with better space utilization. Automakers are also adopting skateboard chassis to reduce development time, support multiple vehicle types, improve structural integration, and enhance range, safety, and manufacturing efficiency across passenger and commercial EV programs.

Major players include Tesla, Volkswagen, BYD, Hyundai Motor Group, General Motors, Geely, Stellantis, Magna International, Foxconn, and REE Automotive. The key trend is movement toward highly integrated, scalable EV platforms with mixed-material structures, cell-to-pack or cell-to-chassis designs, and broader use across SUVs, vans, pickups, and commercial electric vehicles.

Download Free sample to learn more about this report.

Skateboard Chassis Market Key Takeaways

- 2025 Market Size: USD 53.05 billion

- 2026 Market Size: USD 61.36 billion

- 2034 Forecast Market Size: USD 153.42 billion

- CAGR: 12.1% from 2026–2034

- Asia Pacific dominated the skateboard chassis market with a 62.83% share in 2025.

- Single-motor platforms held the leading share due to cost efficiency and mass-market EV adoption.

- Steel skateboard chassis dominated due to durability, affordability, and large-scale manufacturing suitability.

Asia Pacific

Asia Pacific dominated with USD 33.33 billion revenue in 2025, driven by strong EV manufacturing.

North America

North America growth is supported by EV adoption and electric SUV demand.

Europe

Europe benefits from emission regulations and dedicated EV platform development.

U.S.

Market reached USD 5.30 billion in 2026, driven by EV investments.

Japan

Market reached USD 1.59 billion in 2026, supported by EV innovation.

Read More

SKATEBOARD CHASSIS MARKET TRENDS

Rapid Shift toward Dedicated EV Platforms Accelerates Skateboard Chassis Adoption

Automakers worldwide are increasingly transitioning from modified internal combustion engine (ICE) architectures to dedicated electric vehicle (EV) platforms, significantly boosting demand for the skateboard chassis segment. These platforms enable flexible vehicle design, improved battery placement, and optimized weight distribution, making them ideal for next-generation EV production. The modular nature allows OEMs to develop multiple vehicle models, sedans, SUVs, and commercial vehicles on a single platform, reducing development time and cost. This shift is particularly strong in China, Japan, Europe, and North America, where EV penetration is accelerating. As OEMs scale production and standardize EV architectures, skateboard chassis are becoming the foundational design approach for mass electrification.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing EV Production and Platform Standardization Drives Market Growth

The continuous rise in global electric vehicle production is a primary driver for the skateboard chassis market growth. As governments push for decarbonization and stricter emissions regulations, automakers are expanding their EV portfolios, requiring scalable, cost-efficient platform solutions. Skateboard chassis enable high-volume production through standardization, allowing OEMs to reduce engineering complexity and achieve economies of scale. Additionally, the growing demand for electric SUVs, pickup trucks, and commercial fleets further underscores the need for robust, adaptable chassis platforms. This trend is reinforced by investments in gigafactories and EV manufacturing ecosystems, ensuring sustained demand for skateboard-based architectures across both passenger and commercial vehicle segments.

MARKET RESTRAINTS

High Initial Development Costs and Platform Transition Complexity Limit Adoption

Despite strong growth potential, the skateboard chassis market challenges are related to high upfront investment and engineering complexity. Developing a dedicated EV platform requires significant capital expenditure in R&D, tooling, and manufacturing reconfiguration. Automakers transitioning from legacy ICE platforms must also redesign supply chains and retrain engineering teams, which can slow adoption. Smaller OEMs and emerging manufacturers may find it difficult to justify these investments without guaranteed production volumes. Additionally, integrating advanced battery systems and ensuring structural safety further complicates the development process. These factors can delay platform rollouts and limit rapid adoption, especially in cost-sensitive or emerging automotive markets.

MARKET OPPORTUNITIES

Expansion of Electric Commercial Vehicles Creates New Growth Opportunities

The electrification of commercial vehicles presents a significant opportunity to adopt a skateboard chassis. Electric vans, buses, and trucks benefit greatly from flat, modular platforms that maximize cargo space and support larger battery capacities. Fleet operators are increasingly adopting EVs to reduce operating costs and meet sustainability targets, driving demand for scalable chassis solutions. Skateboard platforms also enable customized body designs, allowing manufacturers to tailor vehicles for logistics, public transport, and last-mile delivery. As urbanization and e-commerce continue to grow, the need for efficient electric commercial fleets will expand, creating strong opportunities for skateboard chassis providers to diversify beyond passenger vehicle applications.

MARKET CHALLENGES

Balancing Integration Complexity with Cost Efficiency Remains a Key Challenge

As skateboard chassis evolve toward greater integration, such as cell-to-pack and cell-to-chassis designs, manufacturers face the challenge of balancing performance gains with cost control. Highly integrated platforms improve energy density, reduce weight, and enhance vehicle efficiency, however they also increase design complexity and reduce modularity. This can make repairs, upgrades, and platform reuse more difficult. Additionally, achieving the right balance between lightweight materials and structural strength without significantly increasing costs is a persistent challenge. Automakers must carefully optimize integration levels to ensure scalability, affordability, and long-term platform flexibility while maintaining competitive performance and safety standards.

Segmentation Analysis

By Platform Architecture

Cost-Efficient Mass-Market EV Deployment Sustains Single Motor Platform Dominance

Based on platform architecture, the market is segmented into single-motor platform (2WD), dual-motor platform (AWD), and multi-motor performance platforms (3-4 motors). Single motor platforms dominate due to their cost efficiency, simpler design, and suitability for high-volume EV production, particularly in compact and mid-range vehicles. These platforms enable automakers to achieve affordability and scalability, especially in emerging and price-sensitive markets. Their energy efficiency and lower component complexity further support widespread adoption.

The multi-motor performance platforms segment is projected to grow at a 19.7% CAGR over the forecast period.

By Chassis Material

Cost-Effective Structural Strength Maintains Steel Chassis Leadership

Based on chassis material, the market is segmented into aluminum skateboard chassis, steel skateboard chassis, mixed-material platforms, and composite/carbon fiber platforms.

Steel skateboard chassis dominate due to their lower cost, high durability, and ease of large-scale manufacturing. They are widely used in mass-market EVs and commercial vehicles where structural strength and cost control are critical. Advanced high-strength steel grades also help reduce weight while maintaining safety.

The composite/carbon fiber platforms segment is projected to grow at a 18.5% CAGR over the forecast period.

By Vehicle Type

Rising Consumer Preference for Larger Vehicles Drives SUV Segment Leadership

Based on vehicle type, the market segmentation is as hatchback/sedan, SUV, LCV, and HCV.

SUVs dominate the market and acquired the skateboard chassis market share due to increasing global consumer preference for larger, versatile vehicles with higher ground clearance and longer driving range. These vehicles require larger battery packs and more robust chassis structures, thereby increasing the skateboard platform’s value per unit. Automakers are heavily focusing on electric SUV launches to capture demand across developed and emerging markets.

The HCV segment is projected to grow at a 16.5% CAGR over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component Integration Level

Platform Standardization and Efficiency Gains Propel Integrated Chassis Adoption

Based on component integration level, the market is segmented into basic skateboard platforms, integrated skateboard platforms, and highly integrated platforms.

Integrated skateboard platforms dominate as they balance performance, cost, and manufacturability by combining key systems such as battery, drive units, and thermal management into a unified chassis layouts structure. This improves packaging efficiency and reduces component redundancy, enabling scalable EV production. Automakers increasingly prefer integrated platforms for multi-model flexibility and cost optimization.

The highly integrated platforms segment is projected to grow at a 21.9% CAGR over the forecast period.

SKATEBOARD CHASSIS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

ASIA PACIFIC

Asia Pacific Skateboard Chassis Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market due to its large EV production base, strong battery ecosystem, and rapid adoption of dedicated EV platforms. The region benefits from cost-efficient manufacturing, high domestic demand, and strong government support for electrification. Increasing penetration of SUVs and commercial EVs further boosts demand for scalable skateboard architectures. China’s dominance, along with growing contributions from India and steady progress in Japan, ensures sustained regional leadership.

CHINA SKATEBOARD CHASSIS MARKET

China leads the global market in EV production and sales with an anticipated market share of 83.27% in 2026, supported by strong domestic OEMs and battery manufacturers. The country has rapidly adopted dedicated skateboard platforms and advanced integration technologies. High demand for SUVs and commercial EVs, along with government incentives and export growth, continues to strengthen China’s dominance.

JAPAN SKATEBOARD CHASSIS MARKET

Japan’s market, with an estimated valuation of USD 1.59 billion for 2026, showcases gradual growth, driven by steady EV adoption and strong engineering capabilities. The market focuses on compact, efficient vehicle platforms, with a slower transition to full electrification than in China. However, increasing OEM investments in dedicated EV architectures are expected to boost demand in the coming years.

INDIA SKATEBOARD CHASSIS MARKET

India is an emerging market with a CAGR of 20.8% and strong growth potential, driven by rising EV adoption and supportive government policies. Demand is concentrated in cost-sensitive segments, particularly compact cars and light commercial vehicles. Increasing localization of manufacturing and expansion of EV infrastructure are expected to accelerate the adoption of skateboard chassis platforms.

NORTH AMERICA

North America is growing steadily due to increasing EV adoption, especially in the U.S., and rising demand for larger vehicles such as SUVs and electric pickup trucks. The region benefits from higher-value skateboard chassis due to larger battery packs and advanced integration. Expanding EV manufacturing capacity and localizing the supply chain are further supporting the shift toward dedicated EV platforms.

U.S. SKATEBOARD CHASSIS MARKET

The U.S. will account for USD 5.30 billion in 2026, driven by high EV adoption and the strong presence of leading OEMs. The market is driven by demand for SUVs and electric pickup trucks, which require larger and more complex skateboard platforms. Increasing investments in EV manufacturing and platform innovation continue to support market growth.

EUROPE

Europe remains a key market, supported by strict emission regulations and a strong push toward electrification. The region is characterized by rapid transition to dedicated EV platforms and the increasing adoption of lightweight, mixed-raw materials chassis. Although EV growth has moderated in some countries, regulatory pressure and OEM commitments continue to sustain demand for advanced skateboard chassis systems.

GERMANY SKATEBOARD CHASSIS MARKET

Germany will lead the European market in 2026 with USD 4.18 billion, driven by its strong automotive manufacturing base and presence of major OEMs. The country is at the forefront of EV platform development and production. The growing focus on premium EVs and SUVs is driving demand for advanced, high-value skateboard chassis solutions.

U.K. SKATEBOARD CHASSIS MARKET

The U.K. market, exhibiting a CAGR of 11.7% CAGR over the forecast period, is driven by rising EV adoption and regulatory support for electrification. A growing mix of SUVs and compact EVs supports demand. The country is transitioning toward dedicated EV platforms, with increasing investments in EV production and infrastructure, supporting long-term growth in skateboard-chassis demand.

REST OF THE WORLD

The rest of the world is gradually expanding, driven by increasing EV adoption in Latin America and the Middle East & Africa. Growth is supported by urbanization, fuel cost pressures, and government initiatives promoting electrification. Although starting from a smaller base, improvements in infrastructure and the growing availability of affordable EV models are enabling steady growth in skateboard-chassis demand. Markets in Latin America, Southeast Asia, and the Middle East are witnessing gradual EV adoption, driving early-stage demand for skateboard chassis. Growth is focused on affordable passenger EVs and light commercial vehicles. Expanding infrastructure, government incentives, and increasing availability of EV models are expected to support long-term market development in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Platform Standardization, Vertical Integration, and Strategic Partnerships Shape Market Competitiveness

Rapid advancements in dedicated EV platform engineering, battery integration technologies, and strong collaboration between automakers and suppliers characterize the global skateboard chassis market trends. Leading players such as Tesla, Volkswagen, BYD, Hyundai Motor Group, General Motors, Stellantis, Geely, Magna International, Foxconn, and REE Automotive compete through scalable modular platforms, cell-to-pack or cell-to-chassis integration, and flexible architectures supporting multiple vehicle types. Companies are strengthening competitiveness by investing in vertically integrated supply chains, expanding EV manufacturing capacity, optimizing costs through platform standardization, and forming strategic alliances with battery manufacturers and technology partners. The focus is also shifting toward lightweight mixed-material structures and highly integrated traditional chassis systems to improve efficiency and range.

- In March 2024, General Motors expanded its Ultium platform strategy to support a wider range of electric SUVs, trucks, and commercial vehicles, reinforcing the adoption of its scalable skateboard architecture across global markets.

LIST OF KEY SKATEBOARD CHASSIS COMPANIES PROFILED

- Tesla, Inc. (U.S.)

- Volkswagen AG (Germany)

- Hyundai Motor Group (South Korea)

- Toyota Motor Corporation (Japan)

- Geely Holding Group (China)

- General Motors Company (U.S.)

- Rivian Automotive, Inc. (U.S.)

- Lucid Group, Inc. (U.S.)

- XPeng Inc. (China)

- Foxconn / Foxtron Vehicle Technologies (Taiwan)

- Magna International Inc. (Canada)

- REE Automotive Ltd. (Israel)

- Canoo Inc. (U.S.)

- BYD Company Ltd. (China)

- Stellantis N.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Watt Electric Vehicle Company and Donut Lab showcased a new modular skateboard platform at CES featuring integrated in-wheel drive skateboard chassis technology. The platform enables flexible vehicle design, improved interior space, and simplified drivetrain architecture, highlighting advancements in compact, highly integrated electric chassis systems.

- January 2026: Toyota revealed its intention to reinvent EV skateboard chassis design to enhance passenger safety and interior space efficiency. The company is focusing on structural redesign and improved battery placement to increase crash performance and cabin room, reflecting ongoing innovation in next-generation electric vehicle platform engineering.

- December 2025: REE Automotive said Cascadia Motion, a BorgWarner subsidiary, would manufacture and commercialize compact electric drive units integrating REEcorner technology for global OEM programs. This is highly relevant to skateboard chassis competition because REE’s corner-based architecture pushes platform modularity further, combining drive, steering, braking, and suspension functions close to each wheel.

- October 2025: Hyundai unveiled the ELEXIO electric SUV with Beijing Hyundai and said it was built on the E-GMP platform, positioning the model as the foundation for Hyundai’s long-term NEV strategy in China. For skateboard chassis suppliers, this matters because E-GMP is a dedicated EV platform with integrated battery-underfloor packaging and scalable architecture.

- September 2025: BYD launched e-Bus Platform 3.0 and the first C11 electric bus based on it. The release is important for skateboard chassis analysis as it reportedly combines a 1,000-volt architecture with cell-to-chassis battery integration, demonstrating how commercial EV underbodies are evolving toward greater structural integration, improved safety performance, and higher platform efficiency.

REPORT COVERAGE

The global skateboard chassis market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market dynamics and trends expected to drive the market during the forecast period. It offers information on rapid technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The forecast provides a comprehensive competitive landscape, including the most significant global market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform Architecture, Chassis Material, Vehicle Type, Component Integration Level, and Region |

| By Platform Architecture |

|

| By Chassis Material |

|

| By Component Integration Level |

|

| By Vehicle Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 53.05 billion in 2025 and is projected to reach USD 153.42 billion by 2034.

In 2025, Asia Pacifics market value stood at USD 33.33 billion.

The market is expected to grow at a CAGR of 12.1% from 2026 to 2034.

The single motor platform (2WD) segment led the market share.

Demand for modular vehicle architectures and the shift toward larger battery packs with better space utilization are driving market momentum.

Key market players include Tesla, Volkswagen, BYD, Hyundai Motor Group, General Motors, Geely, Stellantis, and Magna.

Asia Pacific region accounted for the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us