Sleep Apnea Implants Market Size, Share & Industry Analysis, By Implant Type (Hypoglossal Neurostimulation Devices, Transvenous Phrenic Nerve Stimulation, Palatal Implants, and Others), By Indication (Obstructive Sleep Apnea and Central Sleep Apnea), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Sleep Apnea Implants Market Size and Future Outlook

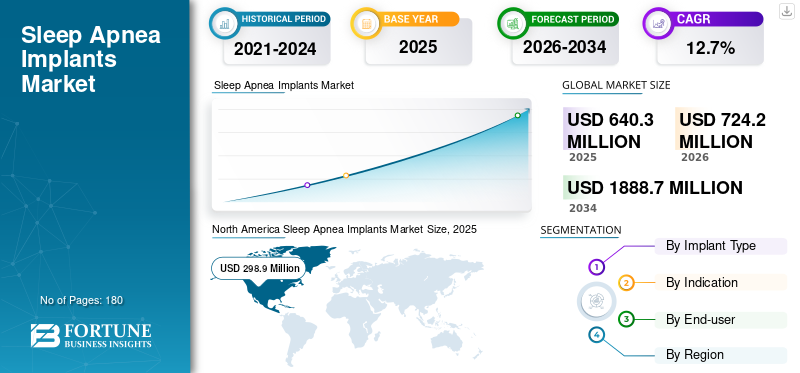

The global sleep apnea implants market size was valued at USD 640.3 million in 2025. The market is projected to grow from USD 724.2 million in 2026 to USD 1,888.7 million by 2034, exhibiting a CAGR of 12.7% during the forecast period. North America dominated the global sleep apnea implants market with a market share of 46.68% in 2025.

Sleep apnea implants are surgically placed devices that help keep the airway open during sleep, mainly for people with Obstructive Sleep Apnea (OSA) in whom Continous Positive Airway Pressure (CPAP) therapy has failed. The market is growing due to rising sleep apnea diagnosis rates, large number of sleep centers and ENT surgeons offering implant pathways, and device manufacturers improving systems to simplify surgery and make follow-up easier.

Furthermore, Medtronic, Inspire Medical Systems, and ZOLL Medical Corporation held the majority of the market share due to strong their brand presence and strategic expansion.

Download Free sample to learn more about this report.

SLEEP APNEA IMPLANTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 640.3 million

- 2026 Market Size: USD 724.2 million

- 2034 Forecast Market Size: USD 1,888.7 million

- CAGR: 12.7% from 2026–2034

- North America dominated the sleep apnea implants market with a 46.68% share in 2025.

- Hypoglossal neurostimulation devices accounted for the largest implant type segment share in 2025.

- Obstructive sleep apnea held the leading indication segment and is estimated to account for 85.7% of the market in 2026.

North America

North America remained the leading regional market, supported by strong adoption of implant therapies and the presence of major industry participants.

Europe

Europe is projected to grow at a CAGR of 12.7% through 2034, driven by advanced healthcare infrastructure and increasing treatment accessibility.

Asia Pacific

Asia Pacific is emerging as a high-potential market due to its large sleep apnea patient population and expanding product availability across key countries.

U.S.

The market is projected to reach USD 318.3 million in 2026, representing approximately 44.0% of global revenue and maintaining its leadership position worldwide.

Japan

The market is expected to generate USD 31.0 million in revenue by 2026, supported by growing awareness, diagnosis rates, and adoption of advanced sleep apnea therapies.

Read More

SLEEP APNEA IMPLANTS MARKET TRENDS

Expanding Usage Beyond Standard OSA Profiles to Emerge as a Key Trend

Currently, there is an increasing shift towards broader patient segments and new clinical evidence that supports use of these implants across different sleep positions and anatomical patterns. This also includes label expansions and trial programs for subgroups that were more difficult to treat under the earlier Breakthrough Device Designation for Genio bilateral hypoglossal (HGNS).

- For instance, in September 2021, Nyxoah received an FDA Breakthrough Device Designation for the Genio bilateral hypoglossal nerve stimulation system for OSA patients with Complete Concentric Collapse (CCC).

MARKET DYNAMICS

MARKET DRIVERS

Increasing Prevalence of OSA & CSA to Fuel the Market Expansion

In recent years, there has been an increasing prevalence of obstructive sleep apnea and central sleep apnea. In these conditions, patients often struggle with CPAP comfort or long-term adherence, which is expected to drive the demand for alternatives that work without a mask. In such a scenario, implant therapies fit properly, which is anticipated to drive the global sleep apnea implants market growth.

- For instance, according to data published by the Journal of Respiratory Medicine in November 2025, approximately 83.7 million adults in the U.S. had OSA in 2024.

MARKET RESTRAINTS

High Upfront Costs and Limited Accessibility in Some Regions to Restrict Market Growth

Sleep apnea implants require surgery and a structured workup, such as a sleep study, ENT evaluation, and, often, drug-induced sleep endoscopy, which decreases eligibility for many patients.

Moreover, the high upfront costs of devices and procedures are also expected to limit accessibility and adoption in certain regions, thereby hindering market growth in the forthcoming years.

MARKET OPPORTUNITIES

Emergence of Next-Generation Systems to Simplify Surgery and Monitoring

In recent years, innovations in sleep apnea implants have enabled hospitals and ASCs to offer the procedure more efficiently. These newer systems are expected to reduce the number of surgical steps, improve sensing or stimulation performance, and add connected tools for patient management, creating significant growth opportunities for key players in the market.

- For instance, in October 2025, Inspire Medical Systems published clinical data on its next-generation Inspire V system at the ISSS and AAO-HNS meetings, highlighting 100% successful implant rates in Singapore and U.S. limited-market-release studies. The key results of these studies showcased a 20.0% reduction in surgical procedure time and statistically significant improvements in obstructive sleep apnea severity.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Shortage of Trained Professionals in Some Regions to Challenge Market Expansion

Despite growing usage of sleep apnea implants, their adoption is often limited due to the scarcity of surgeons in low-and middle-income countries. This shortage is delaying the accessibility and number of procedures performed, as key players are facing challenges expanding in such regions due to limited adoption.

- For instance, according to the data published by Manipal Hospitals in January 2025, more than 90.0% of Indians lack timely access to safe and affordable surgical care.

Segmentation Analysis

By Implant Type

Established Usage in OSA Treatment to Boost the Segment’s Growth of Hypoglossal Neurostimulation Devices

Based on implant type, the market is segmented into hypoglossal neurostimulation devices, transvenous phrenic nerve stimulation, palatal implants, and others.

The hypoglossal neurostimulation devices segment accounted for the largest global sleep apnea implants market share in 2025. These devices directly address the mechanism of airway collapse by stimulating airway muscles during sleep. Also, they have the most established commercial footprint in developed regions, which is expected to drive the segment and overall market growth.

Additionally, the transvenous phrenic nerve stimulation segment is projected to grow at a CAGR of 13.0% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Indication

High Prevelance of OSA Is Driving the Dominance of OSA Segment

By indication, the market is segmented into obstructive sleep apnea and central sleep apnea.

The obstructive sleep apnea segment accounted for the largest market share in 2025. The growth of the segment is attributed to the higher prevalence of obstructive sleep apnea compared to central sleep apnea. As a result, implant therapies are primarily designed and clinically studied for moderate-to-severe OSA. Moreover, the segment is estimated to hold an 85.7% share in 2026.

- For instance, in October 2023, ScienceDirect reported that Obstructive Sleep Apnea (OSA) affects between 9.0% and 38.0% of adults globally.

Additionally, the central sleep apnea segment is anticipated to grow at a CAGR of 13.0% over the forecast period.

By End-user

Rising Number of Hospitals & ASCs Globally to Boost the Segment’s Growth

On the basis of end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

In 2025, hospitals & ASCs dominated the market as end users. The segment’s growth is attributed to the increasing number of hospitals & ASCs, which are contributing to a higher volume of implantation procedures being performed in these settings. Moreover, the availability of high resources and expertise in these settings is additionally favoring the adoption of sleep apnea implants. Furthermore, the segment is set to hold a 72.6% share in 2026.

- For instance, according to MedPAC data, in 2023 the number of ASCs grew, with Medicare-certified facilities increasing by 2.5% from 2022 to reach 6,308.

In addition, the specialty clinics segment is projected to grow at a 13.2% CAGR over the forecast period.

Sleep Apnea Implants Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Sleep Apnea Implants Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 260.7 million, and reached USD 298.9 million by 2025. The growth is attributed to the strong market presence of established players and to increasing implant treatment rates following the failure of CPAP therapies in the region.

U.S. Sleep Apnea Implants Market

In 2026, the U.S. is projected to reach USD 318.3 million, accounting for approximately 44.0% of the global market.

Europe

Europe is projected to record a 12.7% growth rate during the projection period, the second-highest globally, reaching USD 175.6 million by 2026. The region’s growth is attributed to its well-organized healthcare infrastructure, which supports higher implant treatment rates for sleep apnea.

U.K Sleep Apnea Implants Market

The U.K. market is expected to reach USD 26.6 million by 2026, accounting for roughly 3.7% of global revenues.

Germany Sleep Apnea Implants Market

Germany's market is projected to reach USD 39.8 million by 2026, accounting for approximately 5.5% of global revenue.

Asia Pacific

By 2026, the Asia Pacific's market is expected to reach USD 157.9 million, ranking third globally. The large patient pool for OSA and CSA in key countries such as China, India, Japan, and South Korea is prompting key players to expand their product offerings in this region, driving the regional market growth.

- For instance, a 2023 study published by the European Respiratory Society found that OSA was highly prevalent in India, at around 32.5%.

Japan Sleep Apnea Implants Market

Japan is projected to generate USD 31.0 million in revenue by 2026, accounting for approximately 4.3% of the global market.

China Sleep Apnea Implants Market

China’s market is expected to reach nearly USD 58.3 million by 2026, accounting for 8.1% of global revenues.

India Sleep Apnea Implants Market

India’s market is projected to reach USD 24.9 million by 2026, accounting for around 3.4% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are expected to showcase moderate growth, with the Latin America market predicted to reach USD 33.2 million by 2026. The growth of these regions is expected to be driven by increasing awareness of implantation treatment for sleep apnea and key market players entering these regions.

GCC Sleep Apnea Implants Market

By 2026, the GCC market is expected to reach USD 10.6 million, accounting for 1.5% of total market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Brand Reputation and Diversified Portfolios to Reinforce the Market Positions of Significant Players

In 2025, Medtronic, Inspire Medical Systems, and ZOLL Medical Corporation held the majority of the global sleep apnea implants market share. This share is attributed to their strong footprints in the developed markets and their focus on geographic expansions.

Moreover, other prominent players are implementing strategic initiatives, such as new trials, advancements, collaborations, and partnerships to strengthen their market share in the coming years.

LIST OF KEY SLEEP APNEA IMPLANTS MARKET COMPANIES PROFILED

- Inspire Medical Systems (U.S.)

- LivaNova PLC (U.K.)

- Nyxoah (Belgium)

- ZOLL Medical Corporation (U.S.)

- Siesta Medical, Inc. (U.S.)

- Medtronic (Ireland)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Nyxoah received FDA Approvable Letter for its Genio system PMA application, confirming it meets requirements substantially with no further clinical or biocompatibility questions.

- March 2025: LivaNova PLC published its 12-month data from the OSPREY trial of its aura6000 System for moderate-to-severe OSA, showing a 65.0% responder rate and a median reduction of 68% in AHI and ODI.

- November 2024: LivaNova PLC announced that its OSPREY clinical trial for the aura6000 System met primary safety and efficacy endpoints in treating obstructive sleep apnea via targeted hypoglossal nerve stimulation.

- August 2024: Inspire Medical Systems announced FDA approval of its Inspire V therapy system, featuring a next-generation neurostimulator with Bluetooth-enabled patient remote and physician programmer for obstructive sleep apnea treatment.

- July 2024: Nyxoah submitted the fourth and final module of its PMA application for the Genio system to the U.S. FDA, completing its filing for hypoglossal nerve stimulation therapy in obstructive sleep apnea patients.

- July 2022: Nyxoah has secured FDA IDE approval to launch the ACCCESS clinical trial, assessing the Genio system for treating adults with moderate-to-severe obstructive sleep apnea (OSA) who exhibit complete concentric collapse (CCC) of the soft palate.

- June 2021: Nyxoah announced that its BETTER SLEEP trial achieved primary safety and performance endpoints, evaluating the Genio bilateral hypoglossal nerve stimulation system in 42 OSA patients with and without complete concentric collapse (CCC) of the soft palate.

REPORT COVERAGE

The sleep apnea implants market report provides detailed analysis across all market segments, including drivers, trends, opportunities, restraints, and challenges influencing the landscape. It also offers key insights into technological advancements, the prevalence of sleep apnea, industry developments, market share analysis, and detailed company profiles.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.7% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Implant Type, Indication, End-user, and Region |

| By Implant Type |

|

| By Indication |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 640.3 million in 2025 and is projected to reach USD 1,888.7 million by 2034.

In 2025, the market value stood at USD 298.9 million.

The market is expected to grow at a CAGR of 12.7% over the forecast period.

The hypoglossal neurostimulation devices segment led the market, by implant type.

The key factor driving the market is the rising prevalence of OSA and CSA.

Medtronic and Inspire Medical Systems are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us