Smart Bullets Market Size, Share & Industry Analysis, By Smart Function (Guided, Programmable and Sensor-fuzed), By Weapon Class (Small arms, Grenade & low-velocity munitions and Medium caliber), By Guidance (Electro-optical/imaging, Laser-based, RF/mmWave and Inertial/GNSS-aided), By Fuzing (Multi-mode smart fuze, Proximity Fuze and Time Fuze), By End User (Land, Naval and Air), and Regional Forecast, 2026-2034

Smart Bullets Market Size and Future Outlook

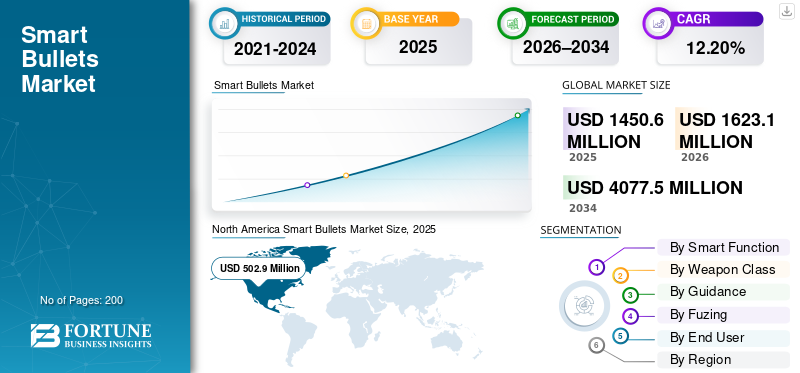

The global smart bullets market size was valued at USD 1,450.6 million in 2025. The market is projected to grow from USD 1,623.1 million in 2026 to USD 4,077.5 million by 2034, exhibiting a CAGR of 12.20% during the forecast period. North America dominated the smart bullets market with a market share of 34.67% in 2025

Smart bullets are precision guided munitions that deviate from standard trajectories by turning, adjusting speed or transmitting data, often using optical sensors, fins, actuators and batteries for real-time steering toward laser-designated targets. They encompass self-guiding, .50-caliber round bullets, laser-tracking projectiles, and inertial systems. These are primarily used in military sniping for hitting, evading targets at long ranges despite wind or cover, enhancing accuracy and troop safety.

Key players operating in the market include Lockheed Martin, Sandia Labs, Northrop Grumman, BAE Systems Plc, Raytheon and others. The major players are focused in developing new technologies, partnerships and among others to gain competitive edge.

Download Free sample to learn more about this report.

SMART BULLETS MARKET TRENDS

Integration of AI is an Emerging Market Trend

Integration of AI into smart bullets represents a pivotal market trend, enabling autonomous adaptation to battlefield dynamics through machine learning algorithms that enhance target recognition, trajectory optimization and real-time decision making for precision strikes. AI facilitates onboard processing for sensor fusion, environmental compensation such as wind or evasive maneuvers, and predictive engagement in complex scenarios, reducing reliance on human input while boosting lethality against threats. This shift supports networked coordination with weapon systems and minimized collateral damage via intelligent threat classification, driving military adoption of edge AI in small caliber guided munitions.

Russia Ukraine War Impact

Russia-Ukraine War Accelerated Demand for Smart Bullets Due to Growing Western Ammunition Shortage

The Russia-Ukraine war significantly accelerated demand for smart bullets and precision-guided munitions, exposing Western ammunition shortages that prompted urgent U.S. and European production ramps for guided artillery shells and small-caliber prototypes. Russia's artillery dominance highlighted the need for trajectory correcting rounds to counter volume fire, driving NATO investments in AI-enhanced bullets despite supply chain strains, while Ukraine adapted by boosting domestic smart munition assembly from foreign kits.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Surging Military Modernization to Drive Market Growth

Surging military modernization drives the smart bullets market growth by prioritizing precision-guided munitions amid escalating geopolitical tensions and evolving warfare paradigms. Global armed forces accelerate upgrades to integrate AI-driven guidance, autonomous targeting, and networked systems into small-caliber rounds, countering asymmetric threats, drones and urban combat challenges while enhancing sniper standoff ranges and reducing collateral risks. This push incorporates commercial innovations such as miniaturized sensors and edge computing into legacy platforms, compressing decision cycles and boosting operational superiority against evasive or concealed adversaries.

MARKET RESTRAINTS

High Development and Production Costs is a Market Restraint

High development and production costs represent a primary market restraint, stemming from the intricate engineering required to miniaturize guidance systems, optical sensors, fin actuators, and onboard processors within small-caliber projectiles. These expenses escalate due to specialized materials for high G tolerance, precision manufacturing tolerances and integration of real-time computing that conventional bullets avoid, limiting scalability for mass deployment. Moreover, reliance on costly R&D programs including DARPA's EXACTO further burdens budgets, while supply chain dependencies for rare components hinder affordability compared to unguided alternatives.

MARKET OPPORTUNITIES

Escalating Global Defense Needs for Precision Munitions Creates New Market Opportunities

Increasing demand for precision munitions create significant market opportunities for smart bullets by addressing demand in asymmetric warfare, urban operations and counter-drone scenarios where conventional rounds lack accuracy against moving or concealed targets. Heightened geopolitical tensions and border disputes drive militaries worldwide to prioritize guided small-caliber projectiles that minimize collateral damage, integrate with unmanned systems, and enable rapid mission success through GPS, laser and AI-enhanced targeting. Modernization programs in major powers favor retrofitting legacy ammunition with smart kits, fostering innovation in high volume production and alliance standardization for export markets.

MARKET CHALLENGES

Complex Miniaturized Architecture Poses Significant Market Challenge

Complex miniaturized architecture poses a significant market challenge for smart bullets, demanding the integration of guidance systems, optical sensors, fin actuators, batteries, and onboard processors into tiny projectiles while enduring extreme G forces during launch, vibration and flight. Engineering hurdles involve shrinking components without sacrificing precision trajectory control or real-time environmental adaptation, such as compensating for crosswinds or target evasion, which complicates design reliability and testing protocols. Manufacturing such intricate systems requires advanced microfabrication techniques and specialized materials resistant to high temperatures and electromagnetic interference, straining current production capabilities and escalating technical risks for scalable deployment.

Segmentation Analysis

By Smart Function

Growth in Military Modernization to Boost the Programmable Segmental Growth

Based on the smart function, the market is segmented into guided, programmable, and sensor-fuzed segments.

The programmable segment is anticipated to account for the largest smart bullets market share. The segment growth is driven by rising defense budgets and the requirement to update current artillery and small-caliber systems with intelligent technologies.

The guided segment is anticipated to rise with a CAGR of 12.82% over the forecast period.

By Weapon Class

High-Demand Platforms to Boost Medium Caliber Segment Growth

Based on weapon class, the market is segmented into small arms, grenade & low-velocity munitions and medium caliber.

In 2025, medium caliber segment dominated the global market. This segment growth is driven by its use in various platforms such as contemporary Infantry Fighting Vehicles (IFVs), Armored Personnel Carriers (APCs), helicopters and naval vessels.

The grenade & low-velocity munitions segment is projected to grow at a CAGR of 12.21% over the forecast period.

By Guidance

High-Bandwidth Capability to Boosts RF/mmWave Segment Growth

Based on the guidance, the market is segmented into Electro-optical/imaging, Laser-based, RF/mmWave and Inertial/GNSS-aided.

The RF/mmWave segment is anticipated to witness a dominating market share over the forecast period. These sensors have bandwidths of up to 7 GHz or higher (e.g., 60GHz and 77GHz bands), which allow them to differentiate between targets that are closely placed and provide specific structural information about the target.

The electro-optical/imaging segment is projected to grow at a high CAGR of 12.65% over the forecast period.

By Fuzing

Increased Precision Capabilities to Boosts Multi-Mode Smart Fuze Segment Growth

Based on the fuzing, the market is segmented into multi-mode smart fuze, proximity fuze and time fuze.

The multi-mode smart fuze segment is anticipated to witness a dominating market share over the forecast period. These fuzes are more effective than traditional fuzes as they can convert from Point Detonation (PD) to Surface Proximity (airburst) to optimize lethality against personnel or soft targets.

The Proximity Fuze segment is projected to grow at a CAGR of 12.32% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Increased Defense Spending & Modernization to boost Land Segment

Based on end user, the market is segmented into land, naval and air.

The land segment dominated the market. Increasing defense spending is driving the purchase of cutting-edge, technologically superior land based weaponry, especially in developing nations such as China and India.

In addition, naval segment is projected to grow at a CAGR of 12.04% during the study period.

Smart Bullets Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Smart Bullets Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 449.1 million, and also maintained the leading share in 2025, with USD 502.9 million. North America leads smart bullets development through major defense contractors such as Lockheed Martin and Raytheon advancing DARPA-funded programs such as EXACTO for self-guided .50-caliber rounds.

U.S Smart Bullets Market

Based on North America’s strong contribution the U.S. market can be analytically approximated at around USD 350.0 million in 2026, accounting for roughly 12.03% of CAGR. The U.S. dominates with sustained DoD investments in guidance kits and trajectory-correcting projectiles, enhancing sniper accuracy against moving targets. Key contracts support Northrop Grumman and RTX in scaling smart shell production for artillery and naval applications.

Europe

Europe is projected to record a steady growth rate during the forecast period of 12.65%, which is the second highest among all regions, and reach a valuation of USD 342.4 million by 2026. Europe focuses on collaborative programs upgrading legacy ammunition with programmable fuzes and sensor fusion to meet NATO interoperability standards.

U.K Smart Bullets Market

The U.K. market in 2026 is estimated at around USD 112.2 million, representing roughly 13.10% CAGR during the study period. The U.K. invests in BAE Systems' 3P programmable ammunition for multi-mode targeting, bolstering land forces' standoff capabilities.

Germany Smart Bullets Market

Germany’s market is projected to reach approximately USD 98.0 million in 2026. Germany advances Rheinmetall's guided 155mm shells and small-caliber prototypes within EU defense initiatives for reduced collateral damage.

Asia Pacific

Asia Pacific region is estimated to reach USD 492.8 million in 2026 and secure a position of third-largest region in the market and fastest growing during the study period. Asia Pacific sees rapid prototyping of indigenous smart bullets amid border tensions, with focus on cost-effective laser-guided systems.

Japan Smart Bullets Market

The Japan market in 2026 is estimated at around USD 113.3 million, accounting for roughly 12.70% of CAGR during the forecast period. Japan develops fin-stabilized smart rounds through Mitsubishi Heavy Industries for maritime defense against swarm attacks.

China Smart Bullets Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 152.9 million. China rapidly scales mass-produced guided small-caliber munitions via Norinco, prioritizing AI autonomy for high-volume fire in contested zones.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. Middle East nations such as Israel and UAE invest in Rafael and local firms for urban counter-terror smart projectiles. The Middle East & Africa and Latin America market is set to reach a valuation of USD 143.9 million and USD 84.0 million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovations Drive Key Player’s Dominance in Market

The Smart Bullets market remains consolidated, with dominant players such as Lockheed Martin, Northrop Grumman, Raytheon (RTX), BAE Systems, and Sandia Labs commanding shares through rise in demand for advanced precision-guided munitions platforms.

Technological innovations accelerate expansion as Lockheed Martin advances DARPA's EXACTO program with self-steering .50-caliber rounds featuring optical guidance for moving targets, Northrop Grumman launches guided 57mm shells with onboard seekers for naval drone defense, and Raytheon develops Mad-Fires projectiles integrating rocket propulsion and radar homing. BAE Systems enhances 3P programmable ammunition for multi-mode targeting, while Sandia Labs prototypes laser-tracking bullets compensating for wind and range. These advancements meet military demands for urban warfare, counter-sniper operations and reduced collateral damage engagements.

LIST OF KEY SMART BULLETS COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- Raytheon Technologies Inc. (U.S.)

- BAE Systems (U.K.)

- Sandia National Labs (U.S.)

- Rheinmetall AG (Germany)

- Norinco (China)

- Nammo (Norway)

- KNDS (Netherlands)

- General Dynamics (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2024: A USD 7.48 billion contract for Joint Direct Attack Munitions, JDAM tail kits, spares, repair, and technical support services has been given to the Boeing defense sector by the U.S. Air Force.

- February 2024: Rheinmetall has received two orders from the German Bundeswehr to produce and deliver 40-mm ammunition for automatic grenade launchers. Ten thousand of programmable 40 mm x 53 Airburst Munition (ABM) DM131 service cartridges will thus be supplied by Rheinmetall. The estimated value of this order is USD 27.47 million.

- February 2024: Munitions India Limited, a Defence Public Sector Enterprise, and the Indian Institute of Technology Madras (IIT Madras) are collaborating to create the country's first 155 Smart Ammunition. This program will aid in the indigenization of a vital defense industry.

- October 2023: Northrop Grumman Corporation has received a development contract from the U.S. Navy for its recently developed 57mm guided high explosive ammunition. The business will test and develop the munition in order to qualify it for use with the Mk110 Naval Gun Mount.

- January 2023: Rheinmetall, a German company, has contracted to deliver 40mm ammunition worth USD 35.99 million to two unidentified European NATO clients.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.20% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Smart Function, Weapon Class, Guidance, Fuzing, End User, and Region |

| By Smart Function |

|

| By Weapon Class |

|

| By Guidance |

|

| By Fuzing |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,450.6 million in 2025 and is projected to reach USD 4,077.5 million by 2034.

In 2025, the market value stood at USD 502.9 million.

The market is expected to grow at a CAGR of 12.20% during the forecast period of 2026-2034.

By smart function, the programmable segment is expected to dominate the market.

Surging military modernization is anticipated to drive market growth.

Lockheed Martin Corporation (US), Northrop Grumman, Raytheon Technologies Inc., BAE Systems, Sandia National Labs, Rheinmetall AG are few key players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us