Smart Naval Munitions Market Size, Share & Industry Analysis, By Range (Short-Range (<50 km), Medium-Range (50-300 km), and Long-Range (>300 km)), By Guidance Technology (Inertial Navigation Systems (INS), EOIR, Active/Passive Sonar, Autonomous Target Recognition (ATR), and Others), By Launch Platform (Surface Ships, Submarines, Coastal Batteries & Shore-Based Systems, and Unmanned Naval Platforms (USVs and UUVs)), By Type (Missiles, Munitions, Guided Projectiles, Guided Rockets, and Precision Guided Firearms), and Regional Forecast, 2026-2034

Smart Naval Munitions Market Size and Future Outlook

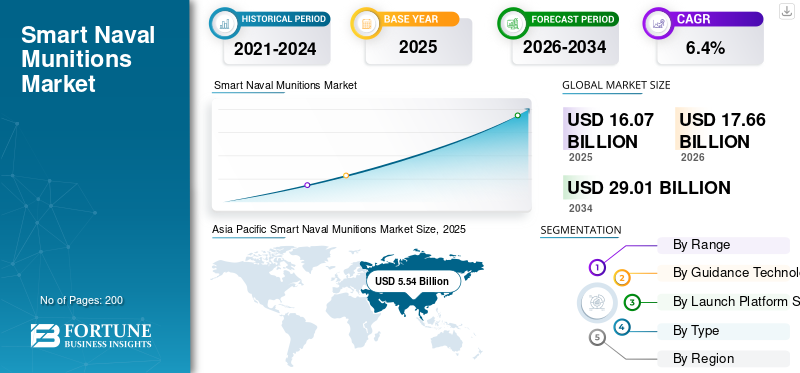

The global smart naval munitions market size was valued at USD 16.07 billion in 2025. The market is projected to grow from USD 17.66 billion in 2026 to USD 29.01 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. Asia Pacific dominated the smart naval munitions market with a market share of 34.47% in 2025.

Smart naval munitions are ship, submarine, or shore-launched weapons designed for naval missions that can guide themselves to a target using onboard navigation and sensors, rather than flying on a purely ballistic or unguided path. Smart naval munitions demand is rising as navies can add lethal reach faster with weapons than with new ships. Bigger defense budgets set the funding base, while Indo-Pacific deterrence, European sea-lane security, and stockpile refills drive orders for longer-range, connected weapons that can work under heavy jamming and still hit moving targets. Buying is also shifting toward coastal batteries, dispersed magazines, and selective fit on unmanned platforms to stretch an opponent’s defenses.

Key industry participants, including BAE Systems, Diehl Defence, Raytheon Technologies, KNDS, Denel Dynamics, Hanwha Aerospace, Roketsan, Safran Electronics & Defense, General Dynamics Ordnance, and Thales are collectively advanced capabilities centered on extended range, improved targeting accuracy, and greater resistance to electronic warfare.

Download Free sample to learn more about this report.

SMART NAVAL MUNITIONS MARKET TRENDS

Advancements in AI-Driven Precision Naval Munitions are Shaping Market Growth

The smart naval munitions market growth is increasingly shifting toward greater integration of artificial intelligence and autonomous systems within precision-guided weapon systems. Naval forces are prioritizing multi-role munitions capable of mid-mission retargeting adjustments and real-time data sharing across fleets, including surface ships, submarines, and unmanned vessels. Emerging hypersonic capabilities and swarm tactics further enhance strike precision in dynamic battlespaces, while collaborative efforts between defense contractors and tech firms accelerate deployment of next-generation systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Escalating Geopolitical Tensions and Naval Modernization to Drive Market Growth

Rising maritime disputes and security threats drive investments in advanced precision-guided munitions to strengthen deterrence and operational effectiveness. Global navies focus on technologies such as improved sensors, guidance systems, and AI for superior accuracy while minimizing collateral damage. Fleet expansions and upgrades further propel adoption of smart weapons in multi-domain strategies. Heightened focus on Indo-Pacific and Arctic regions intensifies procurement of versatile, long-range solutions.

MARKET RESTRAINTS

High Development and Operational Costs to Hinder Market Growth

Elevated expenses for research, production, integration, and maintenance of advanced technologies such as AI and sensors limit adoption, especially for nations with constrained budgets. Personnel training and system upgrades add to financial burdens, creating barriers for smaller navies and slowing broader market penetration in developing regions. Supply chain dependencies on specialized components exacerbate delays and escalate overall lifecycle expenditures.

MARKET OPPORTUNITIES

AI and Autonomous Systems Integration are the Latest Opportunities in the Market

A major opportunity lies in embedding AI for enhanced targeting accuracy, predictive maintenance, and decision-making in naval operations. This enables development of adaptive munitions for unmanned platforms and network-centric warfare, opening new segments for innovation in contested maritime environments. Demand grows from modernization programs seeking interoperable systems that reduce human risk and boost efficiency. Partnerships with emerging tech providers also foster breakthroughs in modular designs compatible across allied forces.

MARKET CHALLENGES

Cybersecurity Threats and Integration Complexities Are Challenging the Market Growth

Smart munitions face vulnerabilities to cyberattacks, jamming, and spoofing due to reliance on digital networks and sensors in contested electromagnetic spaces. Complex integration with existing platforms, stringent regulations, and rapid technological obsolescence demand ongoing investments in security and adaptability. Balancing quantum-resistant encryption with real-time performance remains a persistent hurdle amid evolving threat landscapes.

Segmentation Analysis

By Range

Medium-Range (50–300 km) Segment due to Practical Standoff Reach Needs for Littoral Fights

Based on range, the market is segmented into short-range (<50 km), medium-range (50-300 km), and long-range (>300 km).

The medium-range (50-300 km) segment is anticipated to account for the largest smart naval munitions market share. Medium-range smart naval munitions demand grows as they deliver practical standoff reach for littoral fights and sea denial, fit most ship and coastal launchers, and offer affordable stockpile depth.

The short-range (<50 km) segment is anticipated to rise with a CAGR of 6.8% over the forecast period.

By Guidance Technology

Inertial Navigation Systems (INS) Segment Dominated Due to the Growing Focus on Accuracy

Based on guidance technology, the market is segmented into inertial navigation systems (INS), EOIR, active/passive sonar, autonomous target recognition (ATR), and others.

In 2025, the inertial navigation systems (INS) segment dominated the global market. INS demand stays strong as every smart naval munition needs a reliable navigation backbone. Upgrades focus on accuracy, shock tolerance, and anti-jam integration with GPS, terrain-aiding, and guidance fusion is a key factor driving the segment’s growth.

The autonomous target recognition (ATR) segment is projected to grow at a CAGR of 8.2% over the forecast period.

By Launch Platform

Surface-Ship Segment to Lead due Owing to Increase in Magazine Depth

Based on launch platform, the market is segmented into surface ships, submarines, coastal batteries & shore-based systems, and unmanned naval platforms (USVs and UUVs).

The surface ships segment is anticipated to witness a dominating market share over the forecast period. Surface-ship demand leads as destroyers and frigates carry the most launch cells and mission sets. Navies prioritize layered air defense, anti-ship strike, and land-attack loads to increase magazine depth.

The unmanned naval platforms (USVs and UUVs) segment is projected to be fastest growing at a CAGR of 10.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Missiles Segment Led the Market Due to Longer Reach and Decisive Effects

Based on type, the smart naval munitions market is segmented into missiles, munitions, guided projectiles, guided rockets, and precision guided firearms.

The missiles segment dominated the segmental market share. Missiles dominate demand since they provide the longest reach and decisive effects across anti-ship, strike, and air-defense missions. Buyers want smarter seekers, datalinks, and higher production rates for sustained combat readiness.

The guided projectiles are projected to grow at a CAGR of 7.5% during the study period.

Smart Naval Munitions Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific held the dominant share in 2024, valued at USD 4.94 billion, and also maintained its leading share in 2025, with USD 5.54 billion. The region demand surges as navies seek longer-range sea denial, distributed lethality, and layered air defense. Destroyers, submarines, and shore batteries pull procurement of networked missiles, smart torpedoes, and precision projectiles.

Asia Pacific Smart Naval Munitions Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Japan Smart Naval Munitions Market

The Japanese market in 2026 is estimated at around USD 1.12 billion, accounting for roughly 7.6% of CAGR during the forecast period. Japan demand grows as it strengthens island defense, anti-ship reach, and shipboard missile defense. Investments target longer-range munitions, improved sensors, and integration across destroyers and submarines for credible rapid response.

China Smart Naval Munitions Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 2.19 billion. China demand remains high as the navy expands VLS capacity, long-range strike, and layered air defense. Focus areas include anti-ship salvos, land-attack reach, and smarter targeting to complicate adversary defenses.

India Smart Naval Munitions Market

The Indian market in 2026 is estimated at around USD 0.84 billion. India demand is pulled by Indo-Pacific deterrence, sea-lane protection, and Make-in-India co-production. Priorities include coastal batteries, ship-launched anti-ship missiles across key platforms, and smarter guidance kits that reduce import dependence.

North America

North America is estimated to reach USD 5.50 billion in 2026 and secure the position of second largest region in the market. The region demand rises as navies expand missile-defense, anti-ship, and strike inventories, refill stockpiles, and integrate smarter seekers and datalinks. Buying is driven by Pacific deterrence, homeland defense, and readiness.

U.S. Smart Naval Munitions Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 5.02 Billion in 2026, accounting for roughly 6.3% of global sales. Demand is driven by fleet air-defense, anti-ship, and strike needs, plus stockpile replenishment. Priorities include networked missiles, smarter seekers, and higher production rates to match Pacific credible operational planning.

Europe

Europe is projected to record a growth rate during the forecast period of 6.1%, which is the third-highest among all regions, and reach a valuation of USD 5.08 Billion by 2026. Europe demand accelerates as nations rebuild magazines, deploy coastal and ship-based anti-ship missiles, and strengthen naval air defense. Joint programs and expansion answer lessons from high-intensity conflict and sea-lane security.

U.K. Smart Naval Munitions Market

The U.K. market in 2026 is estimated at around USD 0.81 billion, representing roughly 6.3% CAGR of global sales. U.K. demand focuses on protecting carrier and escort groups, upgrading ship self-defense, and sustaining submarine strike. Spending favors modern anti-ship and air-defense missiles, plus guidance upgrades to better resist jamming.

Germany Smart Naval Munitions Market

Germany’s market is projected to reach approximately USD 0.99 billion in 2026. Germany demand rises with NATO readiness, Baltic and North Sea security, and air-defense modernization. Procurement emphasizes shipboard interceptors, anti-ship missiles, and coastal batteries, supported by local production and European programs.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.64 billion and USD 0.31 billion, respectively, in 2026. Rest of the world demand grows unevenly, led by Gulf security and selective Latin American upgrades. Buyers prioritize coastal defense, frigate refits, and precision munitions with navigation and electronic-warfare tolerance.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Innovations due to Surge in Demand For Stockpile Replenishment

BAE Systems, Diehl Defence, Raytheon Technologies, KNDS Group, Denel Dynamics, Hanwha Aerospace, Roketsan, Safran Electronics & Defense, General Dynamics Ordnance, and Thales Group are collectively driving the smart naval munitions market by accelerating the shift from standalone precision to networked, jam-resistant, and longer-range effects. As a group, they are pushing innovation in multi-mode seekers, hardened guidance and navigation, two-way datalinks, and autonomy-enabled target recognition, while also expanding industrial capacity for propulsion, energetics, and electronics to meet the surge in demand for stockpile replenishment and higher magazine depth.

LIST OF KEY SMART NAVAL MUNITIONS COMPANIES PROFILED IN REPORT

- BAE Systems (U.K.)

- Diehl Defense (Germany)

- Raytheon Technologies (U.S.)

- KNDS Group (Germany)

- Denel Dynamics (South Africa)

- Hanwha Aerospace (South Korea)

- Roketsan (Turkey)

- Safran Electronics & Defense (France)

- General Dynamics Ordnance (U.S.)

- Thales Group (France)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Bharat Electronics Ltd (BEL) and Safran Electronics & Defense entered into a joint-venture agreement to set up a new company in India focused on manufacturing the HAMMER (Highly Agile Modular Munition Extended Range) precision-guided air-to-ground weapon.

- November 2025: Naval Group and LASIGE (the research unit at the University of Lisbon’s Faculty of Sciences) signed an MoU to explore joint R&D collaboration across naval and broader defence technology areas.

- November 2025: India and France progressed their defense cooperation through a fresh arrangement to co-produce the HAMMER precision air-to-ground weapon system in India, supporting India’s push to build indigenous high-tech armaments and reduce reliance on external suppliers.

- July 2025: Raytheon, part of RTX, secured a USD 74 million U.S. Navy contract to deliver new RAM Guided Missile Launching Systems, refurbish existing launchers, and supply upgrade hardware and spares.

- October 2021: Rheinmetall and UVision signed a strategic teaming deal to supply Europe with loitering munitions, making UVision’s combat-proven HERO family available to European customers to meet current and evolving operational needs.

REPORT COVERAGE

The smart naval munitions market report offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Range, By Guidance Technology, By Launch Platform, By Type, and Region |

| By Range |

|

| By Guidance Technology |

|

| By Launch Platform |

|

| By Type |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 16.07 Billion in 2025 and is projected to reach USD 29.01 Billion by 2034.

In 2025, the market value stood at USD 5.54 Billion.

The market is expected to exhibit a CAGR of 6.4% during the forecast period (2026-2034).

By range, the medium-Range (50-300 km) segment is expected to dominate the market.

Escalating geopolitical tensions and naval modernization are the key factors driving market growth.

BAE Systems, Diehl Defense, Raytheon Technologies, KNDS Group, Denel Dynamics, and Hanwha Aerospace are few major players in the global market.

Asia Pacific dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us