Smart Orthopedic Implants Market Size, Share & Industry Analysis, By Product (Smart Joint Implant, Smart Spine Implant, and Others), By Procedure (Total Joint Replacement, Partial Joint Replacement, and Spinal Fusion & Stabilization Procedures), By Application (Intraoperative Implant Optimization, Post-Operative Implant Performance Monitoring, and Rehabilitation & Recovery Tracking), By End-user (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Smart Orthopedic Implants Market Size and Future Outlook

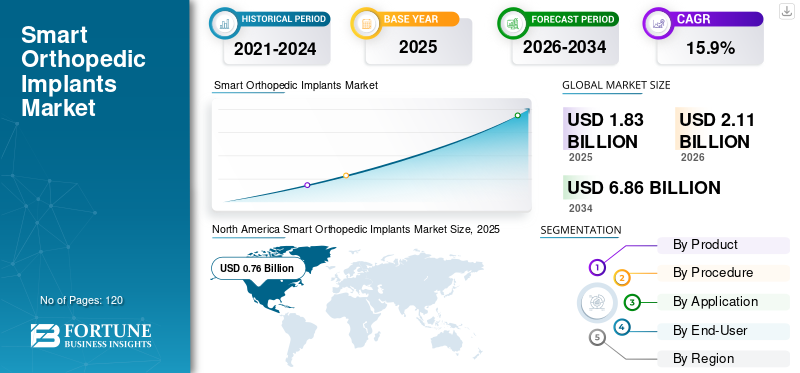

The global smart orthopedic implants market size was valued at USD 1.83 billion in 2025. The market is projected to grow from USD 2.11 billion in 2026 to USD 6.86 billion by 2034, exhibiting a CAGR of 15.9% during the forecast period. North America dominated the smart orthopedic implants market with a market share of 41.53% in 2025.

Smart orthopedic implants are advanced joint or bone implants that include small sensors or connected features to monitor movement, pressure, or healing inside the body. These implants help doctors understand how a joint is performing after surgery and whether recovery is on track. The market growth is attributed to the rising number of joint replacement surgeries, the aging population, and the growing prevalence of orthopedic conditions. In addition, rising sports injuries along with technological advancements are also projected to accelerate market growth during the forecast period.

- For instance, in December 2025, MedStar Health became one of the hospitals in the U.S. that started using smart knee technology for total knee replacement procedures. The hospital adopted Persona IQ technology for tracking knee motion post-surgery.

Furthermore, many key industry players, such as Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Stryker Corporation, Johnson & Johnson, and Medtronic plc, operating in the market, are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

Smart Orthopedic Implants Market Key Takeaways

- 2025 Market Size: USD 1.83 billion

- 2026 Market Size: USD 2.11 billion

- 2034 Forecast Market Size: USD 6.86 billion

- CAGR: 15.9% from 2026-2034

- North America dominated the smart orthopedic implants market with a 41.53% share in 2025.

- The smart spine implant segment is projected to grow at a CAGR of 15.8% during the forecast period.

- The spinal fusion & stabilization procedures segment is anticipated to expand at a CAGR of 15.6% during the forecast period.

North America

North America held the leading position in 2025, reaching USD 0.76 billion in market value.

Europe

Europe is projected to grow at a CAGR of 15.4% and is expected to reach USD 1.98 billion by 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 0.46 billion in 2026, securing the third-largest regional market position.

U.S.

The market is estimated at USD 0.76 billion in 2026, accounting for approximately 36.2% of global sales.

Japan

The market is estimated at USD 0.08 billion in 2026, representing around 3.7% of global revenues.

Read More

SMART ORTHOPEDIC IMPLANTS MARKET TRENDS

Rising Emphasis on Integration of Implants with Digital Health Platforms Boosts Market Trend

The market is currently witnessing a rising emphasis on the integration of digital health platforms in implants for better monitoring. This integration helps healthcare professionals track the recovery of patients. Moreover, hospitals are seeing more patients with severe leg circulation problems, especially those linked to diabetes, and this is pushing companies to develop devices specifically designed for smaller, harder-to-treat vessels. In addition, continual collaborative research and development activities are also projected to support this trend during the forecast period.

- For instance, in October 2025, a group of researchers at the University of Pittsburgh announced the development of a wireless spinal implant that enables remote monitoring of patients after surgery.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Substantial Rise in Joint Replacement Surgeries to Boost Market Growth

Joint replacement procedures are increasing worldwide due to aging populations and rising cases of arthritis and joint injuries, driving smart orthopedic implants market growth. Moreover, many patients require hip or knee replacements to restore mobility and reduce pain. Hospitals are performing more of these surgeries every year, which increases demand for implants. In addition, there is a considerable adoption of smart implants as they add value by giving doctors information about how the joint is performing after surgery.

- For instance, according to data published in the Journal of Bone and Joint Surgery, Inc., the number of total knee arthroplasty procedures in the U.S. is expected to reach 3.48 million per year by 2030.

MARKET RESTRAINTS

Higher Cost of Smart Implants as Compared to Traditional Implants Hamper the Market Development

Smart orthopedic implants are more expensive than standard implants because they include sensors, connectivity features, and advanced materials. Many hospitals and patients still choose conventional implants due to lower costs and familiarity. In addition, insurance coverage and reimbursement for smart implants are also not consistent across all regions. This makes adoption slower, especially in cost-sensitive markets. While the benefits are clear, some hospitals wait for stronger long-term evidence and better pricing before adopting smart implant technologies widely.

MARKET OPPORTUNITIES

Growth of Personalized and Data-driven Treatment is Projected to Offer Market Opportunities

Healthcare is moving toward personalized care, where treatment is based on each patient’s condition and recovery pattern. Smart implants support this approach by providing real-time or long-term data about joint performance. In addition, healthcare professionals can use this information to adjust rehabilitation plans and detect problems early. This creates strong opportunities for companies that offer connected implant solutions.

MARKET CHALLENGES

Long-term Reliability and Data Management to Pose a Critical Market Challenge

Smart implants must work reliably inside the body for many years. Any failure can lead to additional surgery or complications. This makes product development and testing more complex. Hospitals also need systems to manage the data generated by these implants. Storing, analyzing, and protecting patient data requires a secure digital infrastructure. Training doctors and staff to use these systems adds another layer of difficulty.

Segmentation Analysis

By Product

Superior Treatment by Smart Joint Implant to Drive Segmental Growth

Based on the product, the market is divided into smart joint implants, smart spine implants, and others.

The smart joint implant segment is anticipated to account for the largest smart orthopedic implants market share. The segment growth is attributed to a substantial number of hip and replacement procedures. These implants directly replace damaged joints, making them ideal for adding smart monitoring features. In addition, hospitals and surgeons are more willing to adopt smart technology in these high-volume procedures. Smart knee and hip implants help track patient activity and recovery, improving long-term results.

- For instance, in July 2025, Zimmer Biomet announced its plan to acquire Monogram Technologies to consolidate its presence in surgical robotic systems.

The smart spine implant segment is anticipated to rise with a CAGR of 15.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Procedure

Substantial Volume of Total Joint Replacement Procedures to Accelerate Segment Growth

Based on procedure, the market is segmented into total joint replacement, partial joint replacement, and spinal fusion & stabilization procedures.

In 2025, the total joint replacement segment dominated the global market. The global smart orthopedic implants market is attributed to the substantial volume of total joint replacement procedures. Patients undergoing full joint replacement require careful monitoring during recovery. Smart implants help doctors understand joint performance after surgery and make adjustments if needed. Moreover, a growing number of product approvals and new introductions are also estimated to accelerate segment growth during the forecast period.

- For instance, in December 2024, OrthAlign, Inc. announced the first clinical utilization of its Lantern Hip, a total hip replacement technology.

The spinal fusion & stabilization procedures segment is anticipated to rise with a CAGR of 15.6% over the forecast period.

By Application

Rising Usage of Smart Technologies During Surgery Leads to Intraoperative Implant Optimization Segmental Dominance

Based on application, the market is segmented into intraoperative implant optimization, post-operative implant performance monitoring, and rehabilitation & recovery tracking.

In 2025, the intraoperative implant optimization segment accounted for the largest share of the global market. Intraoperative implant optimization refers to using smart technologies during surgery to ensure proper implant placement and alignment. This application holds a high share because correct positioning is critical for long-term success. Smart systems help surgeons make better decisions during the operation, reducing the risk of complications or revision surgeries.

The rehabilitation & recovery tracking segment is anticipated to rise with a CAGR of 16.0% over the forecast period.

By End-User

Higher Volume of Joint Replacement Surgeries to Boost Hospitals Segment Growth

Based on end-user, the market is segmented into hospitals, specialty clinics, and others.

In 2025, the hospitals segment held the highest market share as most joint replacement surgeries take place in hospital operating rooms. Smart implants require specialized surgical teams, equipment, and post-surgery monitoring, which hospitals can provide. Large hospitals also handle higher patient volumes, increasing implant usage. They are more likely to invest in advanced technologies that improve patient outcomes and reduce readmissions. Furthermore, the segment is set to hold 69.7% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 16.8% during the forecast period.

Smart Orthopedic Implants Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Smart Orthopedic Implants Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 0.67 billion, and also maintained the leading share in 2025, with USD 0.76 billion. The market in North America is expected to increase due to a higher number of orthopedic surgical procedures and technological advancements.

U.S Smart Orthopedic Implants Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.76 billion in 2026, accounting for roughly 36.2% of global sales.

Europe

Europe is projected to record a growth rate of 15.4% in the coming years and expected to reach a valuation of USD 1.98 billion by 2026. The region is estimated to witness considerable market growth due to rising investments for new product development and the growing incidence of sports injuries.

U.K. Smart Orthopedic Implants Market

The U.K. market in 2026 is estimated at around USD 0.10 billion, representing roughly 4.8% of global revenues.

Germany Smart Orthopedic Implants Market

Germany’s market is projected to reach approximately USD 0.14 billion in 2026, equivalent to around 6.6% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.46 billion in 2026 and secure the position of the third-largest region in the market. Improving healthcare infrastructure, coupled with the introduction of advanced products, will accelerate regional growth.

Japan Smart Orthopedic Implants Market

The Japanese market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 3.7% of global revenues.

China Smart Orthopedic Implants Market

China’s market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.15 billion, representing roughly 7.2% of global sales.

India Smart Orthopedic Implants Market

The Indian market in 2026 is estimated at around USD 0.10 billion, accounting for roughly 4.8% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.11 billion in 2026. In the Middle East & Africa, the GCC is set to reach USD 0.01 billion in 2026.

South Africa Smart Orthopedic Implants Market

The South African market is projected to reach around USD 0.004 billion in 2026, representing roughly 0.21% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Product Approvals by Market Players to Boost Market Progress

The global smart orthopedic implants market holds a semi-consolidated market structure, constituting prominent players such as Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Stryker Corporation, Johnson & Johnson, and Medtronic plc. The significant global market share of these companies is due to numerous strategic activities, including massive investments and product approvals.

- For instance, in August 2024, Zimmer Biomet highlighted the use of its Persona IQ smart knee implant, which includes an embedded sensor to remotely monitor patient recovery data such as motion and walking patterns.

Other notable players in the global market include Globus Medical, Inc., Corin Group plc, Exactech, Inc., OrthoSensor, Inc., Canary Medical, Inc. These companies are expected to prioritize collaborations to increase their global market share during the forecast period.

LIST OF KEY SMART ORTHOPEDIC IMPLANTS COMPANIES PROFILED

- Zimmer Biomet Holdings, Inc. (U.S.)

- Smith & Nephew plc (U.K.)

- Stryker Corporation (U.S.)

- Johnson & Johnson (U.S.)

- Medtronic plc (Ireland)

- Globus Medical, Inc. (U.S.)

- Corin Group plc (U.K.)

- Exactech, Inc. (U.S.)

- OrthoSensor, Inc. (U.S.)

- Canary Medical, Inc. (Canada)

- SpineGuard S.A. (France)

- Centinel Spine, LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Zimmer Biomet received FDA clearance for an enhanced ROSA Knee robotic system designed to support personalized implant positioning during total knee replacement surgery.

- June 2025: Johnson & Johnson MedTech announced the launch of its KINCISE 2 surgical automated system for knee replacement

- October 2024: VISIE Inc. successfully conducted a demonstration of its continuous anatomic auto-tracking for knee surgery.

- June 2024: Smith+Nephew launched CORIOGRAPH pre-operative planning and modeling services to personalize robotic-assisted orthopedic surgeries.

- February 2024: Smith+Nephew showcased AI-driven robotic-assisted orthopedic solutions for personalized joint reconstruction at the AAOS annual meeting.

REPORT COVERAGE

The global smart orthopedic implants market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Procedure, Application, End-User, and Region |

| By Product |

|

| By Procedure |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.83 billion in 2025 and is projected to reach USD 6.86 billion by 2034.

In 2025, the market value stood at USD 0.76 billion.

The market is expected to exhibit a CAGR of 15.9% during the forecast period of 2026-2034.

By product, the smart joint implant segment is expected to lead the market.

The increasing prevalence of orthopedic conditions and technological advancements are driving market expansion.

Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Stryker Corporation, Johnson & Johnson, and Medtronic plc are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us