Smart Personal Safety and Security Device Market Size, Share & Industry Analysis, By Product Type (Wearables, Safety Devices, Phone-tethered Companions, and Others), By End User (Consumers, Defense, Healthcare, Telecommunications, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

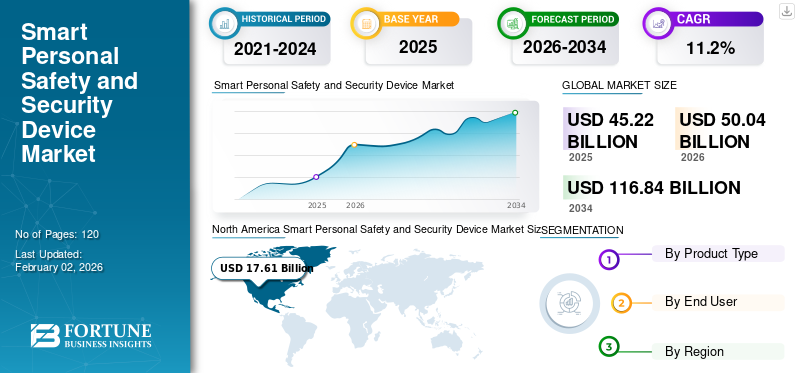

The global smart personal safety and security device market size was valued at USD 45.22 billion in 2025 and is projected to grow from USD 50.04 billion in 2026 to USD 116.84 billion by 2034, exhibiting a CAGR of 11.2% during the forecast period. North America dominated the global market with a share of 38.9% in 2025.

The smart personal safety and security device industry is evolving, centered around smart, portable, and connected devices designed to protect individuals in real time. These devices are integrated with advanced technologies such as IoT, GPS, Bluetooth, and cellular networks. Technological evolution, such as miniaturization, sensors, and connectivity, enables the seamless integration of smart devices into everyday life. Additionally, urbanization and rising crime rates are increasing the demand for personal safety solutions.

Law enforcement agencies are adopting advanced tools, such as smart helmets and wearable cameras integrated with AI features, including facial recognition, thermal imaging, and number plate scanning, to enhance situational awareness and officer safety. This trend is gaining rapid pace, further boosting market growth.

The market is dominated by established key players, such as Apple, Inc., Samsung Electronics Co., Ltd., Honeywell International Inc., ASSA ABLOY AB, and Garmin Ltd. These players focus on partnerships with insurers and telcos to drive adoption. For instance, Honeywell advances its connected worker platforms through collaborations with industrial clients and IoT partners, ensuring compliance and enterprise safety integration.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Growing Demand for Enhanced Security & Incident Response is Fueling Generative AI Adoption in Cyber Defense Applications

Generative AI is revolutionizing cybersecurity applications by automating threat detection, summarizing incident logs, and orchestrating response workflows. The adoption of gen AI plays a significant role in bolstering defensive capabilities. For instance, AI-enhanced Security Operations Centers (AI-SOCs) are delivering faster detection and response, lowering false positives, and improving efficiency. Moreover, manufacturers and platform operators are increasingly embedding GenAI-powered security layers to protect device firmware, secure communication channels, and remotely mitigate evolving cyber threats. For instance,

- In June 2025, according to industry experts, generative AI improves Security Operations Center (SOC) efficiency by 95%.

IMPACT OF RECIPROCAL TARIFF

Reciprocal Tariffs on Electronics Lead to Rising Costs Across Market

Reciprocal tariffs introduced in April 2025, including a baseline 10% levy on most imports and higher rates of 20–54% on goods from China and the European Union (EU), have raised production costs for smart personal safety devices, which rely heavily on global supply chains for electronic components. For smart wearables and IoT-based safety gadgets, which depend on globally sourced components, such as semiconductors, sensors, and batteries, these tariffs have translated into 10–32% increased import costs, particularly from China and Asia. For instance,

- Tech analysts forecast consumer price hikes of approximately 20% for smartphones, 25–50% for vulnerable categories such as hearing aids, and likely similar increases for safety wearables.

MARKET DYNAMICS

Market Drivers

Surge in Integration of Safety Features into Mainstream Wearables is Driving the Market Growth

The rapid adoption of smartwatches, fitness bands, and wearable devices is a key driver for growing adoption of smart personal safety and security devices. Leading consumer electronics brands (Apple, Samsung, and Garmin) are embedding safety functions such as fall detection, crash detection, SOS alerts, heart-rate monitoring, and GPS tracking directly into everyday gadgets. For instance,

- In June 2024, according to an industry survey, global wearable shipments exceeded 534 million to 538 million units.

The integration of personal safety functions into smart personal safety and security devices, already widely used for health and lifestyle monitoring, significantly expands market penetration. This convergence of health, connectivity, and safety positions wearables as the dominant gateway for smart personal security adoption among consumers.

Market Restraints

High Cost of Devices & Subscriptions May Hinder Market Growth

Many smart safety wearables and IoT devices carry premium price tags, such as advanced smartwatches, GPS trackers, and satellite-linked SOS devices. Ongoing subscription fees for services such as Garmin’s inReach SOS or emergency monitoring add to the total cost of ownership, limiting adoption among price-sensitive consumers and in emerging markets.

In emerging economies, awareness about advanced wearable safety devices remains low, and consumers often prioritize affordability over additional features. This creates a slow penetration curve outside North America and Europe, despite growing safety concerns, hindering the smart personal safety and security device market growth.

Market Opportunities

Growing Elderly Population Spurs Integration of Safety Devices into Healthcare Ecosystems

The growing aging population is emerging as a major opportunity for smart personal safety and security devices. By 2030, more than 1.4 billion people worldwide will be aged 60 and above, significantly increasing the demand for fall-detection devices, medical alert systems, and health-monitoring wearables. Seniors face higher risks of chronic illnesses and accidents, creating a natural use case for IoT-enabled safety devices that combine SOS alerts, vital sign tracking, and emergency response features.

At the same time, healthcare systems and insurers are expanding remote patient monitoring (RPM), with U.S. Medicare reimbursements for RPM exceeding USD 500 million in 2024 and growing at over 30% annually. Together, these factors position smart security devices as essential tools in elderly care, bridging consumer electronics and healthcare applications to drive long-term growth in the smart personal safety and security device market.

SMART PERSONAL SAFETY AND SECURITY DEVICE MARKET TRENDS

Rising Demand for Safety Features Embedded into Mainstream Wearables Fuels Market Growth

The rise in demand for the integration of safety features directly into mainstream consumer wearables, such as smartwatches and fitness trackers, is growing among customers. Leading brands in the market are now offering devices with features such as two-way communication with emergency contacts, integration with smart home security systems, wearable panic alarms for children and elderly users, and cloud-based incident reporting for faster coordination with local authorities. This shift has effectively transformed wearables from lifestyle and fitness accessories into multi-functional personal safety tools, appealing to a broader user base.

- For instance, wearable fall detection devices have been shown to reduce emergency response times by up to 50%, enhancing their value in real-world safety contexts.

Moreover, ecosystem integration, such as linking emergency alerts with smartphones, cloud platforms, or insurer programs, further enhances user value. This trend is positioning wearables as the primary gateway for personal safety technology, expanding the market well beyond niche, dedicated devices.

SEGMENTATION Analysis

By Product Type

Rising Personal Safety and Healthcare Concerns Accelerate Growth of Wearables

Based on enterprise type, the market is classified into wearables, safety devices, phone-tethered companions, and others (bodycams/clip-on recorders).

The Wearables segment led the market accounting for 58.34% market share in 2026. Increasing concerns about personal safety, elderly care, women’s and child protection, and health emergencies drive demand for wearables. Additionally, consumers are increasingly looking for multi-functional wearables that combine fitness, health monitoring, and safety into one device, which fuels the segment’s growth.

Phone-tethered companions are anticipated to grow at the highest CAGR during the forecast period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Consumers Segment Dominated due to their Growing Confidence in Safety Devices

Based on end user, the market is categorized into consumers, defense, healthcare, telecommunications, and others (NGOs, insurer-sponsored cohorts, etc.).

The Consumers segment is projected to dominate the market with a share of 59.5% in 2026. Consumers value the confidence and independence that safety devices provide, especially for vulnerable groups. Lightweight, stylish wearables integrate seamlessly into daily life, unlike bulky standalone medical devices. In addition to fitness tracking, a growing number of wearables now integrate AI-driven predictive health alerts, continuous SpO₂ (Peripheral Oxygen Saturation) and ECG (Electrocardiogram) monitoring, and seamless connectivity with emergency response apps expanding the role of everyday devices into comprehensive personal safety tools. For instance,

- According to industry experts, with 534.6 million wearables shipped globally in 2024, safety functions are reaching consumers at scale through devices they already use daily.

The healthcare segment is projected to grow at the highest CAGR during the forecast period.

SMART PERSONAL SAFETY AND SECURITY DEVICE MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Smart Personal Safety and Security Device Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 17.61 billion in 2025, capturing 38.90% of global revenue, and is estimated to reach USD 19.16 billion in 2026. Key factors fostering the dominance of the region include the deployment of safety wearables such as smart helmets in sectors such as law enforcement, defense, and manufacturing. These devices offer features such as facial recognition, thermal imaging, and sensor-driven monitoring, providing critical support for first responders and field personnel. In 2026, the U.S. market is estimated to reach USD 14.1 billion. Increasing crime rates and heightened public awareness are prompting consumers to invest in safety & security devices across the country, thereby industry expansion.

Download Free sample to learn more about this report.

Europe

In 2025, Europe held 24.10% of the global market, reaching a valuation of USD 10.88 billion, and is projected to grow to USD 11.98 billion in 2026. Incidents of violent crime and harassment in urban regions are increasing at approximately 5% annually, motivating widespread demand for portable safety solutions. In 2024, over 60% of women in urban areas reported experiencing harassment, which is propelling demand for smart personal safety and security devices. The UK market is projected to reach USD 2.37 billion by 2026, while the Germany market is projected to reach USD 2.32 billion by 2026. France to record USD 1.74 billion in 2025.

Asia Pacific

The market in Asia Pacific reached USD 11.78 billion in 2025, representing 26.10% of total market revenue, and is projected to reach USD 13.41 billion in 2026. The market is growing rapidly in the region, due to rising urban safety concerns, increasing disposable incomes, and widespread adoption of connected wearables and IoT-enabled safety devices. The Japan market is projected to reach USD 2.65 billion by 2026, the China market is projected to reach USD 2.85 billion by 2026, and the India market is projected to reach USD 2.15 billion by 2026.

South America

Over the forecast period, South America is anticipated to witness a prominent growth in this market. The market is set to record USD 2.14 billion in 2025, as governments across the region are prioritizing public safety investments, ranging from smart city projects to law enforcement technology upgrades, which boost visibility and uptake of personal safety gadgets.

Middle East & Africa

The Middle East & Africa is expected to showcase a significant growth in coming years. In 2025, the Middle East & Africa market stood at USD 2.8 billion, representing 6.20% of global demand, and is projected to grow to USD 3.11 billion in 2026. Several MEA countries have growing concerns around personal security, crime, and public safety, which are increasing the demand for personal safety/security devices. In the Middle East & Africa, GCC is set to attain the value of USD 0.87 billion in 2025.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 2.14 billion in 2025, accounting for 4.70% share, and is expected to reach USD 2.38 billion in 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Industry Participants Focus on Investments to Reinforce their Product Offerings

The global smart personal safety and security device market shows a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and market expansion.

Apple, Inc., Samsung Electronics Co., Ltd., Honeywell International Inc., ASSA ABLOY AB, and Garmin Ltd. are some of the dominating players actively creating advanced solutions to cater to customer demands. Additionally, they focus on collaboration, acquisitions, and partnerships with regional players to maintain dominance across regions.

Apart from this, other prominent players in the market include Oracle Corporation, Infosys Limited, Red Hat, Inc., and others. These companies are undertaking various strategic initiatives such as investments in R&D, geographic expansion, and product launches, to bolster their product offerings.

Long List of Companies Studied

- Apple, Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- Honeywell International Inc. (U.S.)

- ASSA ABLOY AB (Sweden)

- Garmin Ltd. (U.S.)

- ADT Inc. (U.S.)

- Arlo Technologies, Inc. (U.S.)

- Fitbit (Google) (U.S.)

- Buddi Limited (U.K.)

- Revolar Technology Inc. (U.S.)

- Tile Inc. (U.S.)

- Silent Beacon, LLC (U.S.)

- Axon Enterprise, Inc. (U.S.)

- Johnson Controls International plc (U.S.)

- AngelSense (U.S.)

- Huawei Technologies Co. Ltd. (China)

- GreatCall Inc. (Lively) (U.S.)

- Safelet B.V. (Netherlands)

- Schneider Electric SE (France)

- Siemens AG (Germany)

….and more

KEY INDUSTRY DEVELOPMENTS

- September 2025: Garmin launched its Fenix 8 Pro lineup, featuring LTE and satellite connectivity for phone-free emergency messaging via Garmin Messenger, paired with a MicroLED display boasting 4,500 nits of brightness. This release signals a shift toward embedded safety, enhanced connectivity, and recurring SOS services via subscription tiers.

- September 2025: Samsung introduced a home-focused AI system capable of detecting unusual activity, such as monitoring elderly relatives. This system is built on its Knox security platform for enhanced privacy.

- July 2025: Pebblebee upgraded its popular USD 35 Clip Bluetooth tracker with Alert, a free SOS feature enabling users to trigger a siren, strobe lights, and send a location-based text to emergency contacts via multi-press activation. The company also debuted a paid “Alert Live” subscription for live location tracking and silent alerting, aligning privacy-focused gear with personal safety.

- March 2025: Keotech introduced the world’s first personal dashcam, a wearable device combining continuous recording with emergency response capabilities. This launch marks a pivotal step in wearable safety tech, offering individuals a hands-free, proactive safety solution.

- November 2024: Apple extended its Emergency SOS via satellite feature to more international markets, including Austria, Belgium, Italy, Luxembourg, the Netherlands, and Portugal. Additionally, it extended free access for iPhone 14 users for an additional year, boosting safety accessibility globally.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.2% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type · Wearables · Safety Devices · Phone-tethered Companions · Others (Bodycams/Clip-on Recorders) By End User · Consumers · Defense · Healthcare · Telecommunications · Others (NGOs, Insurer-sponsored Cohorts, etc.) By Region · North America (By Product Type, By End User, and By Country) o U.S. o Canada o Mexico · South America (By Product Type, By End User, and By Country) o Brazil o Argentina o Rest of South America · Europe (By Product Type, By End User, and By Country) o U.K. o Germany o France o Italy o Spain o Russia o Benelux o Nordics o Rest of Europe · Middle East & Africa (By Product Type, By End User, and By Country) o Turkey o Israel o GCC o North Africa o South Africa o Rest of Middle East & Africa · Asia Pacific (By Product Type, By End User, and By Country) o China o India o Japan o South Korea o ASEAN o Oceania o Rest of Asia Pacific |

|

Companies Profiled in the Report |

· Apple, Inc. (U.S.) · Samsung Electronics Co., Ltd. (South Korea) · Honeywell International Inc. (U.S.) · ASSA ABLOY AB (Sweden) · Garmin Ltd. (U.S.) · ADT Inc. (U.S.) · Arlo Technologies, Inc. (U.S.) · Fitbit (Google) (U.S.) · Buddi Limited (U.K.) · Revolar Technology Inc. (U.S.) |

Frequently Asked Questions

The market is expected to reach USD 116.84 billion by 2034.

In 2025, the market was valued at USD 45.22 billion.

The market is projected to grow at a CAGR of 11.2% during the forecast period.

By product type, wearables led the market.

Surge in integration of safety features into mainstream wearables is driving market growth.

Apple, Inc., Samsung Electronics Co., Ltd., Honeywell International Inc., ASSA ABLOY AB, Garmin Ltd., ADT Inc., Arlo Technologies, Inc., Fitbit (Google), Buddi Limited, and Revolar Technology Inc. are the top players in the market.

North America held the highest market share.

By end user, the healthcare segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us