Smart Pole Market Size, Share & Industry Analysis, By Component (Hardware and Software & Services), By Installation Type (New Installation and Retrofit Installation), By Application (Highways and Roadways, Public Places, Railways and Harbors, and Others (Commercial & Industrial Zone, etc.)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

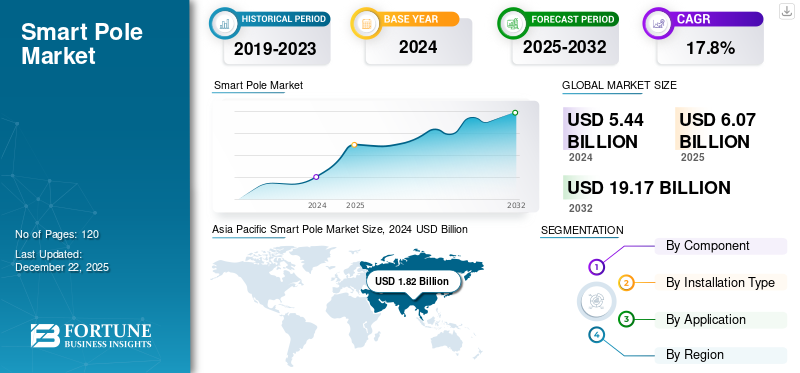

The global smart pole market size was valued at USD 6.07 billion in 2025 and is projected to grow from USD 6.87 billion in 2026 to USD 25.17 billion by 2034, exhibiting a CAGR of 17.60% during the forecast period. Asia Pacific dominated the market with a share of 33.90% in 2025.

Smart Poles represent the next generation of urban infrastructure, integrating advanced technologies such as IoT, 5G, and sensor-based systems to enhance city management and public services. These poles go beyond traditional lighting functions by incorporating surveillance cameras, environmental sensors, EV charging stations, and communication modules to provide real-time data and connectivity across city networks.

This evolution supports municipalities in delivering smart city solutions, improving traffic flow, energy efficiency, public safety, and environmental monitoring through a unified platform.

Major market players such as Signify, Omniflow, Delta Electronics, and Huawei Technologies are innovating continuously to offer scalable, intelligent pole systems. By leveraging artificial intelligence, data analytics, and cloud-based platforms, they aim to transform urban landscapes into more sustainable and connected environments.

Download Free sample to learn more about this report.

IMPACT OF AI

Implementation of AI Capabilities to Fuel Market Growth

AI is increasing the smart pole market growth by turning poles into intelligent decision-making units rather than just passive infrastructure. Instead of simply collecting data, AI enables poles to analyze traffic patterns, detect emergencies, and optimize services, including lighting or signage, in real time.

AI integration also supports predictive maintenance, helping cities identify equipment faults or performance drops before failure occurs, which reduces downtime and long-term costs. For instance,

- In November 2024, Ubicquia launched the UbiCell Utility-Grade Universal (UGU) lighting controller, designed to enhance energy efficiency and asset management for streetlights. The AI-driven controller offers real-time insights and advanced diagnostics, improving network visibility and enabling proactive maintenance.

IMPACT OF RECIPROCAL TARIFF RATES

Reciprocal Tariff Rates to Hamper Market Growth

Reciprocal tariffs, where countries impose equivalent trade duties on each other, can increase the cost of imported intelligent pole components, especially hardware such as sensors, controllers, and LED modules.

Since many pole projects rely on global supply chains, tariff disputes between major economies can disrupt procurement and inflate project costs. A hypothetical instance between the U.S. and China shows this,

- If the U.S. imposes a 25% tariff on Chinese smart controllers, and China retaliates with tariffs on U.S.-made communication chips, a U.S.-based smart technology pole integrator may face a 10–15% cost hike, leading to reduced pole installations or stripped-down feature sets.

This leads to delays in deployment, reduced investment confidence, and, in some cases, cities may scale back or postpone smart infrastructure upgrades.

Smart Pole Market Trends

Integration of Smart Pole with 5G Networks to be a Key Trend in Market

One of the biggest trends in the smart technology pole industry today is their increasing connectivity to 5G networks, where they act as the backbone for next-generation infrastructure. As cities and telecom operators roll out 5G at a faster clip, smart technology poles are being deployed as low-cost platforms to hold small cells and antennas, bypassing the space and zoning issues of cell towers.

Their strategic deployment along roads and public areas allows for tight 5G coverage, especially for mmWave signals at high frequencies that need to have nodes of close proximity. The integration takes a shared infrastructure approach, with municipalities and telcos working together to deploy 5G gear on poles while integrating lighting, sensors, and other smart city applications. For instance,

- In May 2025, O2 Telefónica and 5G Synergiewerk announced plans to roll out 5G streetlights across Germany’s 25 largest cities, starting in 2025, aiming to enhance mobile coverage in busy urban and tourist areas. These smart technology poles replace traditional streetlights, integrate 5G antennas and energy-efficient LED lighting, connected via fiber optics.

MARKET DYNAMICS

Market Drivers

Increasing Urbanization and Smart City Initiatives to Drive Market Growth

The demand for smart poles is driven by growing urbanization and global efforts toward smart city implementation. As cities grow, the need for energy-efficient and networked infrastructure increases, making smart technology poles a central solution. These multi-functional posts transcend the old streetlights by incorporating technologies that increase energy efficiency, connectivity, and public safety.

Governments and cities are actively encouraging smart technology poles as part of urban modernization initiatives, aware of their potential to enhance sustainability objectives, enhance traffic control, and facilitate next-generation wireless networks. As centralized points for lighting, sensors, communication systems, and other smart technology, these poles assist urban centers in minimizing resource duplication while making cities more habitable.

Market Restraints

Technology and Infrastructure Challenges Restrain Adoption of Smart Poles

Rolling out smart technology poles is also presented with a number of key technology and infrastructure issues that limit large-scale implementation. One major setback is grid constraints, as most city power grids are not equipped to handle energy-hungry additions.

Maintenance is also much more complicated than for regular streetlights since smart technology poles integrate electrical, telecom, and computing systems, with specialized technicians needed for maintenance. The multi-purpose functionality of these poles has implications that if one component fails, many services, such as traffic counting or air quality monitoring, are affected. For instance,

- In February 2025, in Visakhapatnam, smart technology poles installed under the 2015 Smart City Mission at a cost of USD 1.7 million are now defunct, which caused public dissatisfaction. Meant to provide early warnings for natural calamities and pollution, the poles are rusted and non-functional.

Market Opportunities

Integration of EV Charging Infrastructure Creates Lucrative Market Opportunities

The convergence of EV charging with smart technology poles is a large market opportunity as urban centers around the world adopt smarter, greener infrastructure. With electric vehicle adoption increasing, cities require easy access to charging that doesn't take up extra space or involve complicated installations. Smart technology poles provide the perfect answer by repurposing current streetlight infrastructure as multi-function hubs that integrate lighting, connectivity, and EV charging. For instance,

- In June 2024, Indonesia’s state electricity company, PLN, announced plans to convert electricity poles into public EV charging stations to boost electric vehicle adoption. Following a successful pilot of three stations in Jakarta, PLN planned to transform 2,000 poles into charging stations in 2024, starting in Jakarta and Bekasi, with future expansion nationwide.

- In May 2024, seven power poles in Sydney’s Northern Beaches will be converted into 22-kilowatt electric vehicle (EV) charging stations as part of the Intellihub EV Streetside Charging project, supported by Northern Beaches Council and ARENA. Located in areas including Manly, Collaroy, and French's Forest, these chargers use 100% GreenPower and cater to the growing EV ownership in the region, with over 3,100 EVs registered.

Such a strategy simultaneously tackles many urban issues. It offers convenient charging points where individuals reside and commute, enhances cleaner transport, and maximizes public space use.

SEGMENTATION ANALYSIS

By Component

Rising Need to Facilitate Automation and Data Flow Management Propels Hardware Segment Growth

Based on component, the market is segmented into hardware and software & services. The hardware segment is subdivided into Lighting lamp, pole bracket & pole body, communication device, controller, cameras, and others (ballast, etc.).

The hardware segment is projected to dominate the market with a share of 71.30% in 2026 due to the fact that it encompasses the physical foundation of the system—smart lighting units, poles, LED fixtures, sensors, cameras, EV chargers, and networking devices. Within these, controller devices account for the majority since they represent the central processing unit that facilitates automation, data flow management, and responsiveness in real time. Controllers control power consumption, light patterns, sensor data, and communicate with city control centres.

Communication Device-4G/5G modules, Wi-Fi routers, LPWAN antennas, and mesh-network devices—is expected to grow at the highest CAGR in the hardware segment. The demand for smooth connectivity, particularly for real-time data transmission, smart surveillance, autonomous traffic management, and public internet access, is driving this growth.

By Installation Type

Growing Focus on Modernizing Existing Street Lighting Infrastructure Boosts Demand for Retrofit Installations

Based on installation type, the market is segmented into new installation and retrofit installation.

Retrofit installations segment is projected to dominate the market with a share of 51.49% in 2026 as they enable cities to retrofit and modernize existing street lighting infrastructure without replacing it entirely. Most urban cities have extensive networks of existing poles, and it is cheaper, less intrusive, and faster to install smart features such as LED lights, IoT sensors, surveillance cameras, and Wi-Fi modules onto them. This strategy assists governments in achieving smart city objectives on tight budgets, particularly in areas where infrastructure is aging, but there isn't much space for new construction.

New installations are expanding at the highest CAGR, driven by the construction of greenfield smart cities, new freeways, special economic zones, and urban development projects in developed as well as emerging economies. These offer the chance to build poles from scratch with modular, future-proofed designs, allowing complete integration of 5G, EV charging, digital signage, and renewable power systems. For instance,

- In May 2025, Telangana CM A. Revanth Reddy ordered smart electric poles with lighting, surveillance, and monitoring features for Hyderabad’s GHMC areas, starting with a pilot at Secretariat, Necklace Road, and KBR Park. The ‘Future City’ will have underground power lines, with high-tension lines relocated.

- In March 2024, the City of Melbourne, in partnership with the state government, is trialing eight smart technology poles in Fishermans Bend’s Turner and Graham streets as part of a 12-month pilot ending April 2025. These poles, part of the “Gateway to GMH” project, feature weather and transport sensors, LoRaWAN connectivity, smart lighting, and pedestrian/bike counters to collect data on transport, noise, air quality, and more.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rise in Smart Pole Installations in Public Places Foster Segment Growth

Based on application, the market is segregated into highway and roadways, public places, railways and harbors, and others.

Smart technology poles in public places (parks, plazas, downtown areas, tourist spots, campuses) segment is projected to dominate the market with a share of 45.35% in 2026. leaders with high-density population, heavy foot traffic, and the pressing requirement of smart surveillance, lighting, and connectivity in urban centers. Municipalities target these zones first as they are public gathering points, where public safety, smart lighting, digital billboards, and Wi-Fi services provide direct civic benefit.

Smart technology pole installation along highways and roadways is expanding at the highest CAGR, stimulated by the increasing need for smart traffic systems, emergency services, accident surveillance, and adaptive lighting along extensive corridors. Governments are incorporating poles to aid connected vehicle infrastructure (V2X), electric vehicle charging, and real-time traffic analysis. For instance,

- In April 2025, EasyStreet Systems received ALDOT approval for its direct-bury composite smart technology poles in highway clear zones, which enable safer and cost-effective telecom and smart city infrastructure. Unlike traditional break-away poles with a 1,000 lb. weight limit, these poles offer a buckling failure mode, reducing installation costs by USD 8,000–USD 10,000 per site.

SMART POLE MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

Asia Pacific

Asia Pacific Smart Pole Market Size, 2025 USD Billion

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 33.90% of the global market in 2025, generating USD 2.06 billion in revenue, and is projected to reach USD 2.36 billion in 2026. infrastructure demand, and forward-looking policy frameworks. Unlike mature Western markets that focus more on upgrading, Asia Pacific nations are undergoing massive greenfield urban development, allowing smart technology pole integration from the ground up. The Japan market is projected to reach USD 0.53 billion by 2026, the China market is projected to reach USD 1.15 billion by 2026, and the India market is projected to reach USD 0.3 billion by 2026.

Countries, including China, India, and Southeast Asia, are building entirely new urban corridors, smart zones, and digital districts where smart lighting, 5G connectivity, and sensor-based city management are built into the urban blueprint. For instance,

- In February 2025, Ranchi's Smart City Corporation installed 1,300 sensor-based LED street lights along two 22-km lanes as part of the Smart Cities Mission. These lights adjust brightness based on traffic density, enhancing visibility and safety while conserving energy. The project was completed by Larsen & Toubro and is now managed by JBVNL.

Additionally, public-private partnerships (PPPs) are more aggressively pursued in Asia Pacific, enabling large-scale deployments with shared financial risk. For instance,

- In December 2024, Kuching launched its first smart technology pole project at the Waterfront as part of efforts to become a smart city. The five poles, funded by USD 44,800 from Malaysia’s federal ministry, feature LED lighting, public Wi-Fi, CCTV, digital signage, and Sarawak cultural designs.

The Chinese government drives the smart pole market growth by actively building smart cities and deploying infrastructure throughout the country. These poles receive special attention as they incorporate 5G connectivity to advance the digital transformation objectives of the nation. Local manufacturers increase their production capacity to fulfil national needs while adding sophisticated sensors and artificial intelligence functions.

Download Free sample to learn more about this report.

North America

North America contributed approximately USD 1.71 billion to the global market in 2025, accounting for 28.10% share, and is expected to reach USD 1.94 billion in 2026. North America is projected to grow at the highest CAGR in the smart technology pole industry due to its strong focus on next-generation urban infrastructure, 5G densification, and intelligent transportation systems. The ongoing rollout of 5G networks is a major accelerator, as telecom operators seek to use smart technology poles for small cell placement, particularly in urban and suburban areas. In addition, North America also benefits from a highly tech-driven urban planning approach and federal infrastructure bills. The U.S. market is projected to reach USD 1.39 billion by 2026. For instance,

- The U.S. Infrastructure Investment and Jobs Act invests USD 350 billion in highway programs over 5 years.

Strong collaboration between municipalities and private tech companies also supports this trend. For instance,

- In March 2025, Hogansville, Georgia, became the first U.S. city to install LG CNS’s smart technology poles, advancing public safety and city infrastructure. Backed by Movere, these poles feature sensors, EV chargers, air quality and flood monitoring, and an emergency button for immediate alerts to dispatchers.

In the U.S., the market is accelerating due to strong federal infrastructure funding, rapid 5G small cell deployment, and rising demand for smart urban mobility. Los Angeles, New York, and Chicago are actively adopting smart technology poles for traffic monitoring, public safety, and connectivity.

South America

South America's market is experiencing gradual but steady growth, largely supported by government-led smart city pilots aimed at enhancing public services, lighting, and digital inclusion.

Cities in Brazil, Argentina, and Peru are adopting smart technology poles to tackle challenges, including urban congestion, crime monitoring, and energy inefficiencies, especially in metro areas.

Europe

In 2025, the Europe market stood at USD 1.43 billion, representing 23.50% of global demand, and is projected to grow to USD 1.6 billion in 2026. Europe’s market is growing significantly due to its strict environmental regulations, emphasis on energy consumption efficiency, and alignment with EU-wide climate goals such as the Green Deal and Fit for 55.

European cities are prioritizing decarbonization and urban digital transformation, with smart technology poles seen as key tools to reduce carbon footprints through LED retrofitting, solar integration, and adaptive lighting. Additionally, smart technology poles support the region’s push toward smart mobility and walkable, sensor-rich cities, which improve traffic safety, air quality monitoring, and public connectivity. The UK market is projected to reach USD 0.41 billion by 2026, while the Germany market is projected to reach USD 0.35 billion by 2026. For instance,

- In March 2024, Virgin Media O2 (VMO2) successfully trialed smart technology poles installed beside existing street broadband cabinets to expand mobile coverage across the U.K. These compact poles, requiring no planning permission, house small cells powered and connected via VMO2’s fibre network using “digital electricity.” This innovation reduces deployment time and cost while supporting future smart city services such as EV charging.

Latin America

Latin America recorded a market size of USD 0.25 billion in 2025, capturing 4.10% of the global market share, and is projected to reach USD 0.27 billion in 2026.

Middle East & Africa

In 2025, Middle East & Africa generated USD 0.63 billion, contributing 10.30% to global market revenue, and is projected to grow to USD 0.7 billion in 2026. The Middle East & Africa region is witnessing steady growth in the market, which is fueled by nation-backed urban transformation projects and the push to develop digitally integrated cities from the ground up. Countries such as Saudi Arabia (NEOM), the UAE (Smart Dubai), and Egypt (New Administrative Capital) are embedding smart technology poles into massive smart city blueprints that emphasize security, sustainability, and real-time urban intelligence. For instance,

- In November 2024, TAWAL and 5SKYE signed a partnership during Connected World KSA to deploy smart technology poles and micro-edge data centers in Saudi Arabia. This initiative, supported by the Ministry of Communications and Information Technology, aims to boost 5G, IoT, and low-latency applications while reducing infrastructure costs.

In Africa, while infrastructure is still developing, key economies such as South Africa, Kenya, and Nigeria are beginning to adopt smart technology pole solutions in central business districts and transport corridors, often supported by international partnerships. For instance,

- In June 2023, Kenya Power piloted a 'smart poles' project to provide affordable internet to public institutions. The company installed unique utility poles in six locations in Nairobi, which were leased to telecom providers to mount their wireless transmission equipment.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Market Players are Constantly Engaging in Strategic Alliances, Mergers, and Acquisitions to Keep Up with Changing Technology

Key players in the market are actively focusing on technological innovation, strategic alliances, and global expansion. With rising demand for connected infrastructure, companies are investing in product development and smart solutions. Mergers, partnerships, and acquisitions remain central to their growth strategies as they aim to strengthen their market position and cater to evolving urban needs.

Major Players in the Smart Pole Market

Signify Holdings, Omniflow, Delta Electronics, Huawei Technologies, Schréder, Wipro Lighting, and Kesslec, among others, are the key players in the market.

Long List of Smart Pole Companies Studied

- Signify Holdings (Netherlands)

- Omniflow (Portugal)

- Delta Electronics (Taiwan)

- Huawei Technologies (China)

- Leica Geosystems (Switzerland)

- Guangzhou DSPPA Audio Co., Ltd. (China)

- Sunna Design (France)

- Schréder (Belgium)

- Wipro Lighting (India)

- Sundrax Digital Ecosystem (India)

- Kesslec (India)

- Ubicquia, Inc. (U.S.)

- iRam Technologies (India)

…and more

KEY INDUSTRY DEVELOPMENTS

- April 2025: Digicomm International acquired EasyStreet Systems, a U.S.-based maker of lightweight, sustainable smart technology poles, to expand its smart city and telecom infrastructure offerings. The move enhances Digicomm’s capabilities in deploying 5G, IoT, EV charging, and connected infrastructure, while supporting rapid and cost-effective rollouts for municipal and telecom clients.

- October 2024: Pegatron 5G and Flexsol partnered to offer Make in India private 5G solutions, with a focus on smart technology pole deployments. The collaboration combines Pegatron’s 5G network gear with Flexsol’s poles and infrastructure to support sectors such as smart cities, factories, and campuses, both in India and globally.

- February 2024: At MWC 2024, Huawei and Unilumin jointly launched the smart technology pole site solution to support smart city transformation. The solution enhances security, sustainability, intelligence, and efficiency in urban infrastructure by integrating IoT sensing, energy-efficient smart lighting, multi-network access, and automated operations.

- June 2023: Srinagar (a city located in India) expanded its smart city infrastructure by installing 50 smart electricity poles equipped with WiFi hubs, EV charging points, LED lights, CCTV cameras, solar panels, and environment sensors. This follows the successful pilot at Zero Bridge, which now sees 4,000 daily connections.

- January 2023: Kaohsiung, Taiwan, signed a USD 1.5 million deal with U.S.-based Iveda to install Utilus Smart Poles as part of its smart city development. These poles will integrate AI-powered video surveillance, real-time traffic monitoring, IoT sensors, and public alert systems for emergencies, including floods or accidents.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The market presents lucrative investment prospects driven by increasing investment in smart cities and government spending initiatives. Increasing demand for connected solutions, including IoT, 5G, and surveillance systems, enhances the market’s appeal. Public-private partnerships and supportive policies further encourage stakeholder participation. Strategic investments in innovation and retrofitting offer long-term growth potential.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, components, installation types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.60% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Installation Type

By Application

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is projected to reach USD 25.17 billion by 2034.

In 2025, the market was valued at USD 6.07 billion.

The market is projected to grow at a CAGR of 17.60% during the forecast period.

The public places segment holds the highest share of the market.

Increasing urbanization and smart city initiatives to drive the market growth.

Signify Holdings, Omniflow, Delta Electronics, and Huawei Technologies are the top players in the market.

Asia Pacific accounts for the highest market share.

By installation type, the new installation segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us