Smoke Grenade Market Size, Share & Industry Analysis, By Function (Multispectral/IR-Obscurant, Low-tox Training Smokes, Screening/Obscuration (Visible), and Signaling/Marking (Color)), By Delivery Mode (Vehicle-Launched (66–80 mm), 40 mm Launched, Hand-Thrown, and Shipboard Launchers), By Composition (Advanced Multispectral, Red-Phosphorus & Clean-Burn Blends, Engineered Training, and Legacy HC/Chlorinated), By Platform (Ground Combat & Engineers, UAS/Robotics Adjacent, & Others), By End User (Army/Marine Ground Forces, Navy/Coast Guard, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

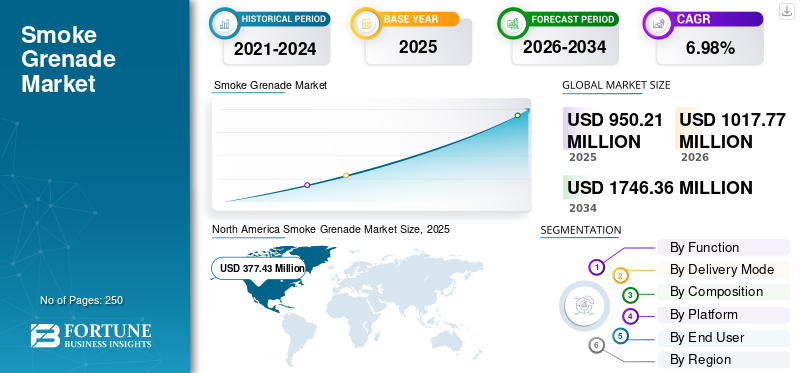

The global smoke grenade market size was valued at USD 950.21 million in 2025. The market is projected to grow from USD 1017.77 million in 2026 to USD 1746.36 million by 2034, exhibiting a CAGR of 6.98% during the forecast period. North America dominated the global market with a share of 39.72% in 2025.

Smoke grenades are battlefield tools that throw up a quick, thick cloud to mask movement, mark landing zones, mislead observers, and obstruct electro-optical or infrared sightlines. They appear as hand-thrown canisters for training exercises and close-in concealment; 40 mm rounds fired from underslung or stand-alone launchers; vehicle-fired 66–80 mm grenades that cast multispectral screens around armored platforms; and shipboard launchers that protect vessels during boarding or harbor maneuvers. Field kits often include a single-color wire-pull grenade for simple, fast signaling where color identification matters. Units also use a high-output burst smoke grenade when they need an immediate, dense wall to break optical sensors, laser rangefinders, and target-tracking systems. For training near personnel or in tighter spaces, cold-burn wire-pull grenades provide visible screening with reduced heat and residue while maintaining safety.

Key players include Rheinmetall (ROSY/ROSY_VL multispectral launchers; DM45 hand smoke), American Rheinmetall Munitions (66 mm IR vehicle smoke), Lacroix Defense (GALIX soft-kill launchers), Chemring (hand and 40 mm military smoke; naval screening), Nammo (40 mm smoke families), Primetake (high-output and cold-burn smokes), Centanex (wire-pull and training smokes), Eurenco (energetic bases and clean-burn formulations), Diehl Defence (vehicle protection smoke and launcher integration), and NonLethal Technologies (operational and training smokes). These players are advancing cleaner, IR-effective obscurants, faster-build canisters, and integrated launcher kits.

Download Free sample to learn more about this report.

Smoke Grenade Market KEY TAKEAWAYS

- 2025 Market Size: USD 950.21 million

- 2026 Market Size: USD 1,017.77 million

- 2034 Forecast Market Size: USD 1,746.36 million

- CAGR: 6.98% from 2026–2034

- North America dominated the smoke grenade market with a 39.72% share in 2025.

- The low-tox training smokes segment is expected to register the highest CAGR of 7.20% during the forecast period.

- The 40 mm launched segment is expected to grow at the highest CAGR of 7.17% over the forecast period.

North America

Valued at USD 377.43 million in 2025, supported by rising military training, armored vehicle upgrades, and clean-burn smoke technologies.

Europe

Projected to reach USD 195.26 million by 2026, driven by increasing defense procurement and military modernization.

Asia Pacific

Expected to witness the fastest growth, driven by expanding defense modernization and localized smoke grenade production.

U.S.

Projected to reach USD 243.67 million by 2026, supported by rising military and law enforcement spending.

Japan

Projected to reach USD 42.64 million by 2026, driven by growing defense modernization and training activities.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Expanding Use of Small Drones Accelerates Smoke Grenade Demand

The market is accelerating as the use of small drones and networked electro-optical and infrared cameras expands across modern battlefields. This growth increases the need for rapid, multispectral smoke to disrupt detection and targeting cycles. At the same time, platform retrofit programs are installing 66 to 80 mm launchers on new and legacy infantry fighting vehicles, creating a larger installed base and predictable resupply requirements. Together, these factors lead to larger annual orders, multi-year contracts, and stronger local production partnerships and sustained investment in cleaner, qualified formulations that can be deployed in complex urban and littoral environments.

MARKET RESTRAINTS

Stringent Regulations Are a Major Cause of Market Restraint

Stringent regulatory frameworks covering safety, environmental impact, and potential misuse slow the growth and adoption of smoke grenades, especially outside defense in civilian or commercial settings. Compliance demands drive reformulation, extended testing, and certification cycles, raising costs and delaying product launches. For new entrants, meeting hazardous-goods, storage, and disposal rules is a high barrier to entry. Regulations also vary by region, with North America and Europe generally enforcing stricter standards, which fragment specifications, complicate approvals, and limit cross-border trade and distribution. The net effect is fewer approved variants, longer time-to-market, and higher total ownership costs for buyers and suppliers.

MARKET OPPORTUNITIES

Integration with Advanced Tactical Gear to Create New Market Opportunities

The increasing need for sophisticated, adaptable tactical tools in defense operations is driving demand for dependable, contemporary smoke grenades for crowd management and control, signaling, screening and obscuration, riot control, and hiding. Linking smoke grenades with modern tactical gear turns a single consumable into a full capability. Modular MOLLE pouches and quick-release carriers speed deployment under attack. Night-vision-readable labels and glove-positive pins lower user error and shorten training time. Radio and battle-management interfaces can cue timing and salvo sequences so smoke effects align with movement and fires. Vendors that certify gear compatibility and provide simple playbooks can win kit contracts and generate steady unit-level replenishment.

SMOKE GRENADE MARKET TRENDS

Integration of Smart Technologies is Emerging as a Defining Market Trend

Smoke grenades are moving from purely mechanical consumables to connected ordnance. Smart tags and QR codes link each canister to lot history, storage conditions, and shelf life, enabling first in first-in-first-out discipline and faster recalls. Passive temperature and humidity sensors embedded in pouches record exposure so quality teams can quarantine risky stock. Programmable firing modules coordinate timing and salvo patterns with battle management systems, turning smoke into a synchronized effect. On weapon health checks, validate continuity and igniter status before use, reducing misfires.

MARKET CHALLENGES

Failures During Ignition to Challenge Market Growth

Unapproved look-alike products are entering supply chains and creating public safety and reliability risks. Failures during ignition or burn lead to injuries, range closures, and emergency recalls, which erode user confidence in legitimate brands. Tamper-evident packaging, forensic composition testing, and post-delivery audits become mandatory, increasing compliance workloads for both buyers and suppliers. Training units may suspend use until authenticity is verified, depressing burn rates and disrupting readiness plans. Rebuilding trust requires visible quality assurance, a clear chain of custody, and rapid incident response.

Russia-Ukraine War Impact

The Russia-Ukraine war has sharply increased global demand for smoke grenades. Both military and civilian sectors have boosted purchases, using them for concealment, signaling, and tactical maneuvers. Defense contractors in Europe and the U.S. have ramped up production, while supply chains for chemicals and casings face consistent strain. Rising battlefield needs have also drawn attention to improved designs and safety standards. However, smaller suppliers struggle with export restrictions and elevated raw material costs. Overall, the conflict has turned a niche defense product into a symbol of modern battlefield adaptation and industrial urgency.

Download Free sample to learn more about this report.

Segmentation Analysis

By Function

Countering Thermal/IR Detection Boosted Multispectral/IR-Obscurant Segment Growth

On the basis of function, the market is classified into multispectral/IR-obscurant, low-tox training smokes, screening/obscuration (visible), and signaling/marking (color).

The multispectral/IR-Obscurant segment accounted for a significant market share in 2025. The growth in the segment is driven by the need to defeat thermal and infrared detection in modern warfare and persistent surveillance.

The low-tox training smokes segment is expected to grow at a CAGR of 7.20% over the forecast period.

By Delivery Mode

Growing Need for Multi-Tube Launcher Banks Encouraged Vehicle-Launched (66–80 mm) Segment Growth

In terms of delivery mode, the market is categorized into Vehicle-Launched (66–80 mm), 40 mm launched, hand-thrown, and shipboard launchers.

The vehicle-launched (66–80 mm) segment captured the largest share of the market in 2025. The vehicle-launched segment is expanding as new and legacy armored platforms add multi-tube launcher banks.

The 40 mm launched segment is expected to grow at the highest CAGR of 7.17% over the forecast period.

By Composition

Advanced Multispectral Segment Dominated the Market, Driven by Engineered Particles

Based on composition, the market is segmented into advanced multispectral, red-phosphorus & clean-burn blends, engineered “low-signature” training, and Legacy HC/Chlorinated.

The advanced multispectral segment held the dominating position in 2025. The development of sophisticated multispectral formulations in smoke grenades is accelerated by engineered particles, which provide tunable physical characteristics such as size, shape, and composition that allow for efficient obscuration across a broad spectrum of electromagnetic radiation, including visible light, infrared (IR), and millimeter waves (MMW).

The red-phosphorus & clean-burn blends segment is set to grow at a CAGR of 7.16% throughout the forecast period.

By Platform

Robust Use for Short Protected Moves Boosted Combat & Engineers Segment Demand

Based on platform, the market is segmented into ground combat & engineers, UAS/Robotics adjacent, Maritime/Littoral, and aviation-adjacent.

The ground combat & engineers segment held the dominating position in 2025. Ground combat and engineer units drive demand through frequent use for breaching, deception, and short protected moves.

The segment of UAS / Robotics Adjacent will witness a growth rate of 7.14% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Inventions in Technology Propelled the Army/Marine Ground Forces Segment Growth

Based on end user, the market is segmented into army/marine ground forces, navy/coast guard, SOF commands, training & T&E RANGES, and regulators/agencies/consortia.

The army/marine ground forces segment held the dominating position in 2025. The growth is driven by innovations in technology (eco-friendly and multispectral smokes), shifting military needs (force protection and large-scale combat scenarios), and their vital role in tactical operations, both historical and contemporary (concealment, signaling, and deception).

The segment of the navy/coast guard adjacent will witness a growth rate of 7.08% growth across the forecast period.

Smoke Grenade Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Smoke Grenade Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 353.54 million, and maintained its leading share in 2025 with USD 377.43 million. North America leads the global smoke grenade market. Regional growth is backed by counter-UAS training needs, armored-vehicle retrofit cycles that expand launcher banks, and a shift to clean-burn formulas that pass stricter environmental rules without cutting training days. The U.S. market for smoke grenades is expanding significantly due to rising military and law enforcement spending and the growth of both commercial and recreational applications. In 2026, the U.S. market is estimated to reach USD 243.67 million.

Europe and Asia Pacific

Europe and Asia Pacific are anticipated to witness a notable smoke grenade market share in the coming years. During the forecast period, the smoke grenade market in Asia Pacific is projected to record a growth rate of 7.69%, which is the highest amongst all the regions. Asia Pacific is the fastest-growing region, backed by amphibious and coastal operations that demand fast-build, corrosion-resistant smokes, plus localization and licensed filling that cut lead times, meet offset goals, and support sustained training cadence. Backed by these factors, countries including China are anticipated to record the valuation of USD 90.34 million, Japan to record USD 42.64 million, and India to record USD 71.15 million in 2026. After Asia Pacific, the market in Europe is estimated to reach USD 195.26 million in 2026. In the region, the U.K. and Germany are both estimated to reach USD 64.30 million and 53.85 million, respectively, in 2026.

Middle East & Africa and Latin America

The Middle East & Africa and Latin America regions would witness a moderate growth during the study period in this market, owing to a rise in defense budgets and procurement activities. The market in the Middle East & Africa in 2026 is set to record USD 88.59 million in valuation, while Latin America is set to attain the value of USD 63.23 million in 2026.

COMPETITIVE LANDSCAPE

Key Players

Product Upgrades and Strategic Partnerships to define the Competitive Landscape

This market is moderately consolidated, with a few primes and strong regional specialists. Major players include Rheinmetall and American Rheinmetall Munitions, Lacroix Defense, Chemring, Nammo, Centanex, and Eurenco. They prioritize R&D in low-flash ignition, cleaner multispectral plumes, recyclable casings, and IR attenuation across NIR, MWIR, and LWIR. Companies partner with armored vehicle makers and naval integrators to certify kit-level solutions and shorten trials. They pursue framework and IDIQ awards to secure recurring volumes. Licensed local filling with government arsenals improves surge capacity and lead times. Digital sustainment with QR serialization, tracking, and dashboards strengthens after-sales support.

LIST OF KEY SMOKE GRENADE COMPANIES PROFILED

- Rheinmetall AG (Germany)

- Lacroix Defense France)

- Alsetex (France)

- Chemring Group (U.K.)

- Nammo AS (Norway)

- EURENCO (France)

- Primetake Ltd (U.K.)

- NonLethal Technologies (U.S.)

- Diehl Defence (Germany)

- ST Engineering (Singapore)

KEY INDUSTRY DEVELOPMENTS

- January 2025: The British Army selected ISTEC Services Limited, a defense company specializing in weapon integration and smoke discharger systems (SDS), to provide the SDS for the improved M270 MLRS A2.

- September 2024: A firm-fixed-price contract of USD 99.25 million was given to American Rheinmetall Munitions Inc. of Stafford, Virginia, for grenades launched by 66 mm infrared smoke screening vehicles.

- May 2024- Rheinmetall received a USD 77 million contract from the Bundeswehr to supply about one million DM45 smoke hand grenades. The framework arrangement, which is valid until 2027, permits a flexible annual call-off of ammunition in accordance with the forces' determined needs.

- June 2024: Rheinmetall unveiled the ROSY_VL Rapid Obscuring System Vertical Launch, the first vertically launched smoke protection system, at Eurosatory 2024. This unit makes use of the tried-and-true ROSY Mod launcher modules arranged vertically.

- May 2024- A Prior Information Notice (PIN) released by the UK Ministry of Defence (MOD) started pre-market engagement for the competitive procurement of 40mm grenades, which are estimated to be worth USD 197 million.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.98% from 2026-2034 |

|

Unit |

Value (USD Million ) |

|

Segmentation |

By Function, Delivery Mode, Composition, Platform, End User, and Region |

|

By Function |

· Multispectral/IR-Obscurant · Low-tox Training Smokes · Screening/Obscuration (Visible) · Signaling/Marking (Color) |

|

By Delivery Mode |

· Vehicle-Launched (66–80 mm) · 40 mm Launched · Hand-Thrown · Shipboard Launchers |

|

By Composition |

· Advanced Multispectral · Red-Phosphorus & Clean-Burn Blends · Engineered “Low-Signature” Training · Legacy HC/Chlorinated |

|

By Platform |

· Ground Combat & Engineers · UAS/Robotics Adjacent · Maritime/Littoral · Aviation-Adjacent |

|

By End User |

· Army/Marine Ground Forces · Navy/Coast Guard · SOF Commands · Training & T&E Ranges · Regulators/Agencies/Consortia |

|

By Geography |

· North America (By Function, Delivery Mode, Composition, Platform, End User, and Country) o U.S. o Canada · Europe (By Function, Delivery Mode, Composition, Platform, End User, and Country/Sub-region) o U.K. o Germany o France o Russia o Rest of the Europe · Asia Pacific (By Function, Delivery Mode, Composition, Platform, End User, and Country/Sub-region) o China o Japan o India o South Korea o Rest of the Asia Pacific · Rest of the World (By Function, Delivery Mode, Composition, Platform, End User, and Country/Sub-region) o Middle East and Africa o Latin America |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 950.21 Million in 2025 and is projected to reach USD 1746.36 Million by 2034.

In 2024, the market value stood at USD 377.43 Million.

The market is expected to exhibit a CAGR of 6.98% during the forecast period of 2026-2034.

The multispectral/IR-Obscurant segment led the market by Function.

Expanding use of small drones is a key factor driving product demand.

Rheinmetall and American Rheinmetall Munitions, Lacroix Defense, Chemring, Nammo, Centanex, and Eurenco are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us