Soil Compaction Machine Market Size, Share & Industry Analysis, By Product Type (Vibratory Rollers, Static Rollers, Pneumatic Rollers, Plate Compactors, and Rammers (Tampers)), By Engine Type (Diesel-powered, Electric-powered, and Hybrid), By Mobility (Walk-behind and Ride-on), By Application (Road Construction, Building & Infrastructure Construction, Mining, Agriculture & Landscaping, and Others (Industrial sites and landfills)), and Regional Forecast, 2026 – 2034

Soil Compaction Machine Market Size and Future Outlook

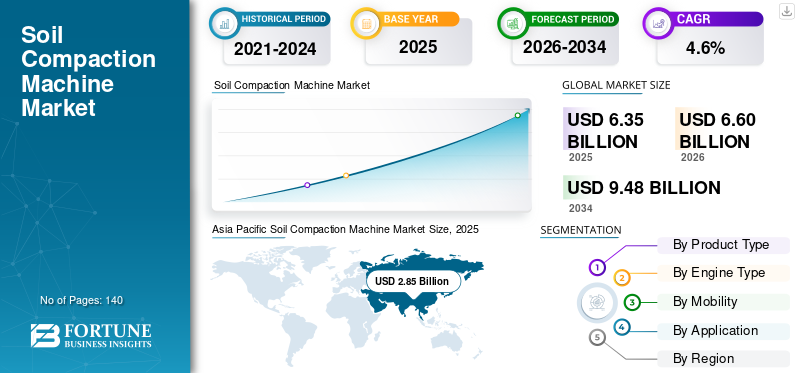

The global soil compaction machine market size was valued at USD 6.35 billion in 2025. The market is projected to grow from USD 6.60 billion in 2026 to USD 9.48 billion by 2034, exhibiting a CAGR of 4.6% during the forecast period. Asia Pacific dominated the soil compaction machine market with a market share of 44.88% in 2025.

Soil compaction machines are equipment used to compress soil and increase its density to improve ground stability and load-bearing capacity. The compaction machine market is witnessing steady growth driven by increasing construction activities and rapid urban development across key regions, including Asia Pacific and Middle East & Africa. These machines are widely used across construction sites to efficiently compact soil and enhance performance in residential commercial and industrial projects. They play a critical role in delivering reliable compaction solutions, ensuring long-term durability of infrastructure such as roads, foundations, and industrial facilities. Current market trends indicate rising adoption of advanced soil compaction equipment, including soil compactors designed for higher efficiency and adaptability across varying soil conditions. Contractors are focusing on optimizing supply chains, reducing rework, and improving productivity across projects. Additionally, the integration of electric and hybrid technologies is gaining traction as companies align with sustainable construction practices. From a regional analysis perspective, growth is supported by infrastructure investments across key regions during the forecast period, while the competitive landscape of key players continues to influence market shares across each market segment.

- For instance, in January 2026, BOMAG GmbH introduced an advanced vibratory roller series equipped with intelligent compaction technology and real-time density monitoring, aimed at improving compaction accuracy and operational efficiency in large-scale infrastructure projects.

BOMAG GmbH, HAMM AG (Wirtgen Group), Ammann Group, Caterpillar Inc., and Volvo Construction Equipment are among the key players holding a significant share of the market. Their competitive positioning is strengthened by strong expertise in compaction technologies, the ability to deliver high-performance and application-specific equipment solutions, extensive global distribution and service networks, and continuous innovation in intelligent compaction and fuel-efficient systems to meet evolving construction requirements.

Download Free sample to learn more about this report.

SOIL COMPACTION MACHINE MARKET TRENDS

Increasing Focus on Rework Reduction and First-Pass Compaction Efficiency is Shaping Equipment Demand

Demand for soil compaction machines is increasingly being influenced by the growing need to minimize rework and achieve required compaction levels within the first few passes across road construction and infrastructure projects. Contractors are placing greater emphasis on operational efficiency, as repeated compaction cycles lead to higher fuel consumption, extended project timelines, and increased equipment wear. This is driving the adoption of compaction equipment with improved vibration control, optimized drum designs, and better machine stability to ensure effective soil densification in fewer passes. The variability of soil conditions across project sites is also pushing operators to rely on equipment that can adapt to different materials such as granular soils, cohesive soils, and mixed subgrades without requiring frequent adjustments. Instead of fully automated systems, there is a growing preference for machines that offer practical operator assistance features, such as adjustable frequency settings and basic feedback indicators, which help improve compaction consistency without adding operational complexity.

- For instance, in March 2025, Caterpillar Inc. introduced an upgraded vibratory roller with enhanced drum design and simplified control settings, aimed at improving first-pass compaction efficiency and reducing fuel consumption in road construction projects.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for High-Quality Infrastructure and Faster Project Execution to Drive Market Growth

The market is witnessing steady growth as construction and infrastructure development activities increasingly focus on achieving higher ground stability, improved load-bearing capacity, and faster project completion. Sectors such as road construction, urban infrastructure, mining, and industrial development are prioritizing efficient compaction processes to ensure long-term durability and structural integrity of projects. The increasing complexity of construction projects, including multi-layer road structures, variable soil conditions, and large-scale earthworks, is driving the need for high-performance compaction equipment capable of delivering consistent and reliable results across different terrains. The growing emphasis on reducing project timelines and operational costs is encouraging the adoption of compaction machines that can achieve required density levels with fewer passes while maintaining uniformity. As infrastructure investments continue to rise, particularly in developing economies, there is increasing demand for equipment that can operate efficiently under high-utilization conditions while ensuring fuel efficiency and minimal downtime. Equipment manufacturers are responding by introducing advanced soil compaction machines with improved vibration systems, enhanced machine stability, and better adaptability to diverse soil conditions, enabling contractors to optimize productivity and achieve consistent compaction outcomes across a wide range of construction applications.

- For instance, in March 2024, HAMM AG (Wirtgen Group) introduced the HD+ 120i V-VIO tandem roller, featuring a combination of vibration and oscillation in a single drum, allowing operators to switch compaction modes based on soil conditions and achieve effective compaction with fewer passes.

MARKET RESTRAINTS

Variability in Soil Conditions and Operator Dependency Continues to Limit Compaction Efficiency

The performance of soil compaction machines is highly dependent on site-specific soil conditions, including moisture content, soil type, and layer thickness, which can vary significantly even within a single project. This variability makes it difficult to achieve consistent compaction results without continuous adjustments, increasing reliance on operator experience and judgment. Unlike automated industrial systems, compaction outcomes are still largely influenced by how effectively the operator selects vibration settings, controls machine speed, and manages pass patterns. In many construction environments, especially in emerging markets, the shortage of skilled operators can lead to inefficient machine utilization, over-compaction, or under-compaction, ultimately affecting project quality. This dependency limits the effectiveness of even advanced equipment, as optimal performance cannot be achieved without proper handling.

MARKET OPPORTUNITIES

Increasing Investment in Road Rehabilitation and Maintenance Creating Sustained Equipment Demand

An emerging opportunity in the soil compaction machine market growth is the increasing focus on road rehabilitation and maintenance across developed and emerging economies. While new infrastructure development remains important, a significant portion of government spending is now being directed toward repairing and upgrading existing road networks, many of which are experiencing early deterioration due to inadequate initial compaction and rising traffic loads. Soil compaction machines play a critical role in these activities by ensuring proper subgrade strengthening, patch repair compaction, and surface preparation for overlays. Unlike large-scale greenfield projects, maintenance and rehabilitation work requires versatile and efficient equipment capable of operating in constrained urban environments and delivering consistent results across smaller work zones. This is driving demand for both compact ride-on rollers and light compaction equipment that can be easily deployed for periodic road repairs, utility reinstatement work, and municipal infrastructure upgrades.

- For instance, in April 2024, Caterpillar Inc. expanded its asphalt compaction portfolio with upgraded tandem vibratory rollers designed to improve compaction performance in road maintenance and urban repair applications.

MARKET CHALLENGES

Achieving Uniform Compaction Across Variable Soil Conditions Remains a Key Operational Challenge

A key challenge in the market is achieving consistent and uniform compaction across varying soil conditions encountered within a single project site. Soil properties such as moisture content, density, and composition can change significantly over short distances, making it difficult to maintain consistent compaction quality without continuous adjustments. This variability directly affects machine performance and increases the risk of under-compaction or over-compaction, both of which can compromise structural integrity and lead to long-term failures. Unlike standardized industrial processes, soil compaction relies heavily on operator skill and real-time judgment to select appropriate vibration settings, machine speed, and pass patterns. Inconsistent operation can result in uneven density distribution, requiring additional passes and increasing fuel consumption, equipment wear, and project timelines. The challenge is further amplified in projects involving mixed soil layers or engineered fill materials, where compaction requirements differ across layers.

Segmentation Analysis

By Product Type

Vibratory Rollers Segment Led as It Represents Most Widely Adopted Equipment across Large-Scale Infrastructure Projects

By product type, the market is segmented into vibratory rollers, static rollers, pneumatic rollers, plate compactors, and rammers (tampers).

Vibratory rollers held the largest soil compaction machine market share as they are extensively deployed across major applications such as road construction, highways, airports, and large infrastructure projects, where achieving deep and uniform soil compaction is critical. These machines utilize vibration mechanisms to transfer energy efficiently into the ground, enabling higher compaction density in fewer passes compared to conventional equipment. Their ability to handle a wide range of soil types, including granular and mixed soils, makes them highly suitable for large-scale and high-load construction environments.

- For instance, in June 2024, BOMAG GmbH introduced an advanced single drum vibratory roller equipped with ECONOMIZER compaction measurement technology, designed to provide real-time feedback to operators and improve compaction efficiency on varying soil conditions.

Plate compactors are the fastest-growing segment and are projected to expand at a CAGR of 5.1% during the forecast period. The growth of this segment is driven by increasing demand for compact and versatile equipment used in urban construction, repair work, and confined job sites such as sidewalks, trenches, and small foundation projects. Plate compactors offer advantages in terms of ease of operation, lower cost, and flexibility, making them highly suitable for small to medium-scale applications.

To know how our report can help streamline your business, Speak to Analyst

By Engine Type

High Power Output, Durability, and Ability to Operate Efficiently Led to Dominance of Diesel-Powered Segment

By engine type, the market is segmented into diesel-powered, electric-powered, and hybrid.

Diesel-powered machines held the largest share of the market, driven by their widespread use in heavy-duty compaction applications such as road construction, highways, mining, and large infrastructure projects. These machines are preferred due to their high power output, durability, and ability to operate efficiently in demanding site conditions where continuous operation and high compaction force are required. Diesel-powered equipment is particularly suitable for large vibratory rollers and heavy compaction machines that require consistent energy delivery to achieve deep soil compaction.

- For instance, in February 2024, Volvo Construction Equipment introduced upgraded diesel-powered soil compactors with improved fuel efficiency and reduced emissions, designed to enhance performance while complying with evolving emission standards in construction projects.

Electric-powered machines are the fastest-growing segment and are projected to expand at a CAGR of 7.0% during the forecast period. The growth of this segment is driven by increasing emphasis on reducing emissions, noise levels, and fuel dependency, particularly in urban construction and indoor applications. Electric compactors are gaining traction in projects such as road maintenance, municipal work, and confined construction environments where environmental regulations and noise restrictions are more stringent.

By Mobility

Ride-on Segment Led as It Supports High-Productivity Compaction in Large-Scale Construction Projects

By mobility, the market is segmented into walk-behind and ride-on.

Ride-on machines held the largest share of the market, driven by their widespread use in large-scale construction activities such as road construction, highways, airports, and industrial infrastructure projects. These machines are designed to deliver high compaction force, wider coverage, and improved operational efficiency, making them highly suitable for projects requiring continuous and high-volume compaction. Ride-on compactors, particularly vibratory rollers, are preferred due to their ability to achieve deeper soil compaction with fewer passes, ensuring uniform density across large surface areas.

Walk-behind machines are the fastest-growing segment and are projected to expand at a CAGR of 5.1% during the forecast period. The growth of this segment is driven by increasing demand for compact and easy-to-operate equipment in urban construction, maintenance work, and confined job sites such as trenches, sidewalks, and residential projects. Walk-behind compactors offer advantages in terms of maneuverability, lower cost, and ease of transportation, making them highly suitable for small to medium-scale applications.

By Application

Road Construction Segment Led as It Represents Largest Demand Center for Soil Compaction Activities

By application, the market is segmented into road construction, building & infrastructure construction, mining, agriculture & landscaping, and others (industrial sites and landfills).

Road construction held the largest share of the market, driven by the critical role of compaction in ensuring the durability and performance of road infrastructure. Soil compaction machines are extensively used in subgrade preparation, base layer compaction, and asphalt compaction processes to achieve required density and load-bearing capacity. The demand is particularly strong due to the need for uniform compaction across long stretches of road networks, where inconsistencies can lead to premature failures such as rutting and surface deformation.

Agriculture & landscaping is the fastest-growing segment and is projected to expand at a CAGR of 5.3% over the forecast period. The growth of this segment is driven by increasing demand for land development, soil preparation, and ground stabilization in agricultural fields, sports grounds, and landscaping projects. Soil compaction machines are increasingly being used to prepare stable surfaces for irrigation systems, pathways, and turf development, where controlled and uniform compaction is essential.

Soil Compaction Machine Market Regional Outlook

By geography, the market is categorized into Asia Pacific, Europe, North America, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Soil Compaction Machine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific remains the fastest-growing soil compaction machine market, and generated revenue of USD 2.85 billion in 2025 globally. The growth is driven by rapid urbanization, large-scale infrastructure development, and expanding road construction activities across key economies such as China, India, Japan, and Southeast Asian countries. The region’s growth is primarily supported by increasing government investments in transportation infrastructure, including highways, expressways, rail corridors, and urban development projects. Additionally, the rising need for durable road networks and improved construction quality is driving demand for efficient soil compaction equipment capable of delivering consistent subgrade performance across varying soil conditions.

China Soil Compaction Machine Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 1.24 billion, representing roughly 18.8% of global sales.

Japan Soil Compaction Machine Market

The Japanese market is estimated at around USD 0.26 billion in 2026, accounting for roughly 3.9% of the global sales.

India Soil Compaction Machine Market

The Indian market is estimated at around USD 0.57 billion in 2026, accounting for roughly 8.7% of global sales.

North America

The North America market accounted for over USD 1.29 billion in revenue in 2025, supported by strong demand across road construction, infrastructure rehabilitation, and urban development activities in the U.S., Canada, and Mexico. Regional demand is closely linked to increasing investments in highway modernization, bridge repair, and municipal infrastructure upgrades, along with a growing focus on improving construction quality and project efficiency. Contractors are increasingly deploying advanced soil compaction machines to achieve consistent subgrade performance, reduce rework, and optimize fuel consumption across large-scale and maintenance projects.

U.S. Soil Compaction Machine Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 1.05 billion in 2026, driven by its extensive road network, aging infrastructure, and continuous investments in transportation and public infrastructure projects. Unlike many regions, U.S.-based contractors place strong emphasis on achieving high compaction standards to ensure long-term durability and reduce lifecycle maintenance costs. The country is witnessing significant investments in road rehabilitation, highway expansion, and urban infrastructure upgrades, which are increasing the demand for high-performance compaction equipment capable of delivering uniform density across varying soil conditions.

Europe

The European market is driven by a strong focus on construction quality, sustainability, and advanced infrastructure development across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for soil compaction machines is closely linked to the region’s emphasis on precision compaction, strict construction standards, and the need to minimize environmental impact during infrastructure development. Contractors and project developers are increasingly adopting compaction equipment that offers improved fuel efficiency, reduced emissions, and better control over compaction performance.

U.K. Soil Compaction Machine Market

The U.K. market is estimated at around USD 0.17 billion in 2026, representing roughly 2.6% of global sales.

Germany Soil Compaction Machine Market

Germany’s market is projected to reach approximately USD 0.25 billion in 2026, equivalent to around 3.8% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in large-scale infrastructure development, urban expansion, and transportation projects across key regions such as GCC countries, South Africa, Israel, and North Africa. Demand for soil compaction machines is closely linked to the region’s focus on improving road connectivity, supporting economic diversification, and developing modern urban infrastructure. Governments across the region are prioritizing projects such as highways, smart cities, industrial zones, and logistics corridors, which require efficient ground preparation and compaction to ensure long-term structural stability. GCC countries are investing heavily in mega infrastructure projects, including new cities, road networks, and tourism developments, creating strong demand for high-capacity compaction equipment capable of operating in large and challenging environments. South Africa’s demand is driven by mining activities and infrastructure development, where soil stabilization and ground preparation are critical for operational efficiency. North Africa is witnessing increasing investments in transportation infrastructure and urban development, further supporting equipment adoption.

GCC Soil Compaction Machine Market

The GCC market is projected to reach around USD 0.27 billion in 2026, representing roughly 4.0% of the global sales.

South America

The South America market is driven by increasing infrastructure development activities, rising focus on improving road connectivity, and gradual adoption of advanced construction equipment across key economies such as Brazil, Argentina, and Chile. Demand for soil compaction machines is primarily supported by expanding road construction projects, growing urban development, and strong mining operations across the region. Contractors are increasingly deploying compaction equipment to improve soil stability, ensure uniform density, and enhance the durability of infrastructure projects while reducing rework and operational costs.

Brazil Soil Compaction Machine Market

The Brazil market is projected to reach around USD 0.30 billion in 2026, representing roughly 4.5% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Compaction Technology Expertise, Equipment Design, and Application-Specific Performance Capabilities

The soil compaction machine market is moderately consolidated, with competitive positioning driven by technological capabilities, application-specific expertise, and the ability to deliver high-performance compaction equipment across diverse construction activities such as road construction, infrastructure development, mining, and urban projects. Leading players such as BOMAG GmbH, HAMM AG (Wirtgen Group), Ammann Group, Caterpillar Inc., and Volvo Construction Equipment maintain strong market positions by offering advanced compaction machines capable of achieving uniform soil density and high operational efficiency under demanding construction conditions.

Competitive differentiation is increasingly shaped by the ability to develop fuel-efficient compaction machines with enhanced vibration performance, improved durability, and optimized operational reliability. As contractors focus on reducing rework, improving compaction consistency, and meeting project timelines, market players are investing in next-generation equipment with improved drum designs, advanced vibration control systems, and operator-friendly features that enhance on-site productivity.

- For instance, in September 2024, Wacker Neuson SE introduced updated vibratory rammers and plate compactors designed to improve compaction performance and operational efficiency in confined and urban construction applications.

LIST OF KEY SOIL COMPACTION MACHINE COMPANIES PROFILED IN REPORT

- BOMAG GmbH (Germany)

- HAMM AG (Wirtgen Group) (Germany)

- Ammann Group (Switzerland)

- Dynapac (Fayat Group) (Sweden)

- Sakai Heavy Industries, Ltd. (Japan)

- Wacker Neuson SE (Germany)

- Caterpillar Inc. (U.S.)

- Volvo Construction Equipment (Sweden)

- CASE Construction Equipment (U.S.)

- JCB Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: BOMAG Americas, Inc. introduced the new BP series vibratory plate compactors, designed to improve durability, reduce maintenance, and enhance compaction performance across soil and asphalt applications.

- June 2024: Ammann Group expanded its e-drive electric compaction equipment solutions for urban and indoor applications, focusing on reduced operating costs and compliance with emission regulations.

- April 2024: BOMAG GmbH presented its electric vibratory plates, tandem rollers, and tampers at INTERMAT 2024, emphasizing energy-efficient and low-emission compaction solutions.

- March 2024: BOMAG GmbH announced new product introductions and showcased electric compaction equipment, including the BW 120 AD e-5 electric tandem roller and BP 18/45 e plate compactor, at World of Asphalt 2024.

- March 2024: BOMAG GmbH highlighted its e-PERFORMANCE electric compaction equipment line, focusing on low-noise and zero-emission operation for urban construction environments at World of Asphalt 2024.

REPORT COVERAGE

The global soil compaction machine market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Engine Type, Mobility, Application and Region |

| By Product Type |

|

| By Engine Type |

|

| By Mobility |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value to stand at USD 6.60 billion in 2026 and is projected to reach USD 9.48 billion by 2034.

In 2025, the North Americas market value stood at USD 1.29 billion.

The market is expected to exhibit a CAGR of 4.6% during the forecast period (2026-2034).

By application, the road construction segment leads the market.

Rising infrastructure development, road construction, urbanization, demand for durability, and efficient compaction drive market growth.

BOMAG GmbH, Wirtgen Group, Ammann Group, Dynapac, and Sakai Heavy Industries, Ltd. are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us