Solid Rocket Motor Market Size, Share & Industry Analysis, By Platform (Missiles, Rocket Artillery, Space Launch Vehicle and Boosters and Model & Sounding Rockets), By Stage (Single Stage and Multi Stage), By Component (Propellant, Igniter, Thruster/Nozzle, Motor Casing & Insulation and Others), By End User (Space Agencies, Research Institutes and Defense), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

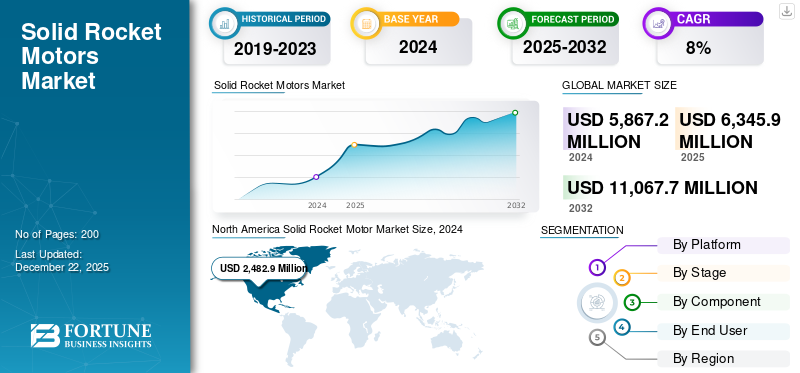

Solid Rocket Motor Market Size and Future Outlook

The solid rocket motor market size was valued at USD 6.35 billion in 2025. The market is projected to grow from USD 6.91 billion in 2026 to USD 12.99 billion by 2034, exhibiting a CAGR of 8.2% during the forecast period. North America dominated the solid rocket motor market with a market share of 42.36% in 2025.

The market is poised for substantial growth, fueled by escalating defense expenditures worldwide, the rapid integration of hypersonic and precision-guided munitions, and surging demand for reliable propulsion in missiles, launch vehicles and space systems. Advanced solid rocket motors, leveraging high-energy composite propellants, lightweight composite casings, and enhanced burn-rate control, deliver superior thrust-to-weight ratios, long shelf-life stability, and performance in extreme conditions. Furthermore, innovations in insensitive munitions and green solid propellants, amid rising geopolitical tensions and space militarization, are propelling market acceleration.

- For instance, in March 2024, Northrop Grumman is announced expansion of its Allegany Ballistics Laboratory in West Virginia with a USD 178 million NAVSEA contract to build a new modular energetics facility to double the solid rocket motor production capacity by fall 2026.

Key players such as Northrop Grumman Corp, Nammo AS, Technologies Inc., Anduril, China Aerospace Science and Technology Corporation and others, are focusing on innovations such as high-energy composite propellants for extended range and reduced weight for enhanced safety across missiles, launch vehicles, and hypersonic systems.

Download Free sample to learn more about this report.

Solid Rocket Motors Market Key Takeaways

- 2025 Market Size: USD 6.35 billion

- 2026 Market Size: USD 6.91 billion

- 2034 Forecast Market Size: USD 12.99 billion

- CAGR: 8.2% from 2026–2034

- North America dominated the market with a 42.36% share in 2025.

- Missiles segment is projected to hold the largest market share with 42.69% in 2026.

- Defense segment is projected to account for 60.98% of the global market share in 2026.

North America

The market reached USD 2.69 billion in 2025, driven by increasing defense spending and missile modernization programs.

Asia Pacific

The market reached USD 1.38 billion in 2025, supported by rising investments in missile and satellite technologies.

Europe

The market reached USD 1.97 billion in 2025, fueled by expanding defense initiatives and space launch activities.

U.S.

The market reached USD 2.42 billion in 2025, driven by defense modernization.

Japan

The market reached USD 0.28 billion in 2025, supported by space and missile programs.

Read More

Impact of Russia Ukraine War

Russia Ukraine War Influences Market Due to High Consumption and Demand

The Russia Ukraine war has significantly accelerated global demand for solid rocket motors, driven by high consumption of rockets and missiles, the need to rebuild depleted inventories, and the shift toward sustained, high-tempo fires. European countries and NATO partners have expanded procurement of air-defense interceptors, guided rockets, artillery rockets and long-range precision munitions. This has spurred domestic manufacturing expansions by major players such as L3Harris, Lockheed Martin partnering with General Dynamics and Anduril Industries.

- For instance, in November 2025, L3Harris Technologies announced a USD 400 million investment in a new 110-acre solid rocket motor production campus in Camden, Arkansas, set to expand large SRM manufacturing capacity. The facility supports U.S. missile defense modernization during surging demand driven by the Russia Ukraine war and Middle East conflicts for SRMs in long-range missiles and air defense.

Nations prioritize SRMs for their high thrust, long shelf life and instant readiness in contested environments. Russia has aggressively scaled up its own SRM production for long-range strikes, reducing dependence on imports amid sanctions. Therefore, the Russia-Ukraine war catalyzes sustained market expansion by driving urgent procurement of reliable SRM-powered missiles.

SOLID ROCKET MOTOR MARKET TRENDS

Technological Innovation and Investment in R&D are Key Market Trends

Ongoing research and development activities and innovative breakthroughs in materials science are driving the solid rocket motor market growth. These advancements are improving the overall performance of SRMs, improving safety mechanisms and promoting environmental sustainability. Scientists are developing new composite materials that can withstand higher stresses and temperatures, making rocket propulsion systems more efficient and reliable. Technological progress in manufacturing processes is also making it possible to produce these motors with greater precision, enhancing their operational safety and efficiency.

- For instance, in December 2023, Northrop Grumman Corporation successfully conducted a full-scale static test fire of a new solid rocket motor developed in less than a year as part of its Solid Motor Annual Rocket Technology Demonstrator (SMART Demo). The company reported that the SMART Demo successfully demonstrated several innovative technologies, alternative manufacturing materials and processes that reduce lead times by 75%.

Furthermore, the market is also focusing on environmentally friendly operations. This ranges from looking for more environmentally friendly propellant alternatives with lower harmful emissions to reducing environmental impact during launches. The fusion of improved performance, stringent safety standards and an environment-friendly approach is shaping the market's future.

Growing Reusable Space Launch Vehicles to Fuel Market Development

The market is experiencing strong growth trends, driven by the growing use of SRMs in reusable space launch vehicles and fast-growing commercial space sector. Organizations recognize that the reliability and performance benefits of SRMs make them well-suited for missions involving multiple launches.

- For instance, in December 2020, ESA announced plans for the maiden flight demonstration of a prototype reusable rocket first stage named Themis in 2023. The Themis program aims to provide valuable insights into the economic worth of reusability for Europe and to develop technologies applicable to future European launchers. Themis is based on decisions made during the European technological breakthroughs in reusability and follows a leaner and cost-conscious development approach. In December 2020, ESA signed a USD 40 million contract with French prime contractor ArianeGroup for the 'Themis Initial Phase'.

- In August 2024, The Wall Street Journal reported that Lockheed Martin and General Dynamics plan to build their rocket motors, seeking to tackle a persistent shortage impacting Ukraine’s defense capabilities and U.S. efforts to deter China. General Dynamics will start production next year at its facility in Arkansas, which would initially produce thousands of SRMs annually exclusively for Lockheed Martin.

These developments growing adoption of SRM in defense & space, promising expanded market opportunities through innovation and supply chain resilience.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Government-Industry Collaborations is Expected to Drive Market Growth

Collaborative contracts and government-industry cooperative agreements drive innovation and expand production capacity. Government across the globe is making direct investments and collaborations with key defense suppliers for the development of advanced solid rocket motors.

- For instance, in January 2026, Department of War (DoW) announced a huge USD 1 billion convertible preferred equity investment directly into L3Harris Technologies' Missile Solutions Business. This first-of-its-kind direct-to-supplier partnership aims to massively expand the U.S. production capacity for solid rocket motors, essential for critical munitions and national security.

These collaborations foster the development of new technologies and approaches and extensively facilitate market access and growth opportunities. By aligning resources and sharing expertise, both sides can commence innovative projects, optimize production processes, and better respond to evolving consumer needs in a rapidly changing market.

Northrop Grumman has continued to advance the CASTOR series by leveraging foundational technology derived from four generations of ballistic missile boosters and with expertise gained from expendable launch vehicle programs. Thus, these government-industry collaborations accelerate innovation in solid rocket motor technology and ensure robust production scaling to meet national security demands.

Increasing Geopolitical Tensions to Boost Market Growth

The increasing geopolitical tensions globally influence market growth positively. The global instability is creating urgent, sustained demand for missile systems that ensure rapid deterrence and response readiness. As countries continue to invest in their defense capabilities due to regional conflicts and strategic threats, the demand for advanced propulsion systems, especially SRMs, is expected to increase.

Nations perceive rising rivalries and conflicts as direct challenges to sovereignty, prompting immediate shifts in defense priorities toward scalable, storable propulsion such as SRMs. Thus, the nations are concentrating on building up their military arsenals, resulting in increased demand for effective and reliable missile, space and defense propulsion technologies. In addition, the continuous arms race and increase in the scope of space research programs are intensifying the need for innovation and global competition in this sector.

Continuous Ongoing Space Exploration Programs Is Expected to Propel Market Growth

Continuous ongoing space exploration programs propel market growth by generating persistent demand for reliable, high-thrust propulsion in launch vehicles and orbital missions. National space agencies such as NASA, ESA and ISRO maintain significant schedules for satellite constellations, crewed missions and deep-space probes, relying on solid rocket motors for their strap-on boosters and upper stages that deliver precise thrust profiles.

- For instance, in August 2025, Northrop Grumman Corporation announced that its GEM 63XL solid rocket boosters, the longest monolithic, single-cast units provided nearly two million pounds of thrust for the first certified flight of United Launch Alliance’s Vulcan Centaur rocket on the U.S. Space Force-106 mission.

Such missions ensure steady contracts for motor suppliers, as programs prioritize proven, cost-effective solid propulsion systems over experimental alternatives. Moreover, the ongoing initiatives such as Artemis or Starship development embed SRM scalability into core architectures, fostering new upgrades in rocket motors. In addition, private ventures such as SpaceX, Blue Origin, and Rocket Lab increase solid rocket motors demand through frequent test flights and shared satellite launches. These companies value solid rocket engines for quick reuse and flexible payloads.

Therefore, the ongoing space exploration programs from agencies such as NASA, ESA, and ISRO, alongside private players such as SpaceX and Northrop Grumman, sustain robust demand for advanced solid rocket motors in launch vehicles and missions, which is expected to drive market growth.

MARKET RESTRAINTS

High Development and Manufacturing Costs to Hamper Market Growth

The complex engineering, specialized materials, and rigorous testing required to ensure the performance, safety, and reliability of SRMs significantly increase development costs. SRM development demands extensive testing of volatile propellants under extreme conditions, requiring specialized facilities and high investment.

These high barriers to entry pose challenges for smaller companies and countries with limited defense budgets, making it difficult to enter or scale within the market. Smaller defense budgets and limited industrial base in some countries restrict their ability to develop or produce SRMs domestically, forcing reliance on imports or partnerships with larger defense contractors.

The high costs also lead to extended program timelines, as SRM qualification requires multiple static-fire tests, environmental trials and repeated inspections before production release. Any modification in propellant formulation, grain geometry, casing material or nozzle design typically requires re-validation, further increasing cost and delaying deliveries. In addition, SRM manufacturing must comply with strict hazardous material handling, storage and transportation regulations, which raises operating costs and thus restricts the growth of the market during the forecast period.

MARKET OPPORTUNITIES

Increasing Spending on Defense Systems to Drive Market Growth Opportunities

Governments elevate defense allocations during global threats, directing funds toward proven SRM-powered weapons such as interceptors and cruise missiles that offer immediate operational readiness. This shift accelerates procurement, providing manufacturers with multi-year contracts.

- For instance, according to the Stockholm International Peace Research Institute (SIPRI), worldwide military expenditure hit USD 2.44 trillion in 2024, up 6.8% from 2023.

Increasing investments by nations globally to modernize military capabilities and procure advanced missile systems powered by solid rocket motors offer market growth opportunities. SRMs are favored for their reliability, high thrust, long shelf life and rapid deployment capabilities in strategic and tactical defense applications.

Rising expenditures target aging stockpiles, funding upgrades to SRMs for enhanced range, accuracy, and survivability in contested environments. Defense forces are focused on modernizing and expanding its SRM manufacturing capabilities with the help of their increased defense budget.

- For instance, in February 2025, defense technology contractor Anduril Industries secured a USD 14.3 million contract from the U.S. Department of Defense to expand SRM production. This initiative reflects the Pentagon’s effort to strengthen domestic manufacturing capabilities amid growing supply chain concerns.

The nations prioritizing upgrading of aging stockpiles to boost SRM range, accuracy and survivability, with expanded budgets supporting market growth.

Rising Demand in Space Exploration to Provide Lucrative Growth Opportunities

Solid rocket motors are used across various aerospace applications and are particularly prominent in heavy-lift launches, satellite deployments and lunar missions. These motor systems are used due to their high reliability and strong thrust output, making them uniquely best suited for deep space missions. There is an increase in design of key space missions and space projects for space exploration which drives the development and adoption of solid rocket motors.

- For instance, April 2025, China National Space Administration (CNSA) announced intensive 2025 missions, such as Tianwen-2 for asteroid sampling, Shenzhou-20/21 crewed flights, and international projects including the China-Europe SMILE probe and China-Italy earthquake satellite.

Such increased launches demand more solid rocket motors for Long March rockets, spurring domestic production and innovation. Moreover, in heavy-lift operations, such as launching commercial satellites or conducting resupply missions to space stations, such motors provide consistent performance and stability, helping ensure that missions meet tight deadlines and targets.

Additionally, in lunar missions, SRMs have been used to enable soft landings and support ascent maneuvers. These functions are essential for the success of missions to study the moon's geology and assess possible resources. As space and private organizations continue to advance the boundaries of exploration, SRMs continue to be favored for their simple design and ease of integration, making them an ideal option for various space exploration operations.

MARKET CHALLENGES

Stringent Regulatory and Safety Standards & Supply Chain Challenges to Limit Market Expansion

Stringent regulatory and safety standards restrain market expansion by imposing rigorous compliance burdens that delay programs and raise operational costs. SRM testing must meet exacting government criteria for propellant stability, blast overpressure and fragment containment.

Compliance with strict aerospace and defense regulations and safety standards requires extensive testing, certifications and approvals. These requirements extend development timelines and add to costs, potentially slowing the introduction of new technologies in the market. Ongoing geopolitical tensions can complicate supply chains and international collaborations, impacting the availability of raw materials and components critical for SRM production.

In addition, procuring specialty materials such as advanced composites and energetic propellants is limited to a few niche suppliers. This concentration can lead to delays, supply chain disruptions and difficulties in scaling up production rapidly to meet the growing needs of military and aerospace, especially amid geopolitical tensions and trade restrictions.

Segmentation Analysis

By Platform

Increasing Defense Spending Amid Geopolitical Tensions to Propel Missiles Segmental Growth

Based on the platform, the market is divided into missiles, rocket artillery, space launch vehicle and boosters and model & sounding rockets.

The Missiles segment is projecteed to dominate the market with a share of 42.69% in 2026. With rising geopolitical tensions and a growing focus on developing missile arsenals, most countries are spending on solid-propelled missile systems. These engines form the core of air-to-air, surface-to-air, and ballistic missile platforms due to their ability to deliver high thrust and rapid response times, strengthening the segment’s leadership.

- For instance, in July 2024, Avio signed a contract with Raytheon, an RTX business, to advance development of critical solid rocket motors for U.S. government and allied defense applications. The rocket motors are expected to be used for defense weapon systems such as tactical missiles.

The space launch vehicle and boosters segment is anticipated to rise with a CAGR of 8.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Stage

Simple Design, Cost Effectiveness and Ease of Production to Propel Single Stage Segmental Growth

By stage, the market is segmented into single stage, and multi stage.

The single stage segment holds the largest share due to wide use of single stage SRMs in short-range missiles, artillery and sounding rockets due to their simple design, low cost, ease of production and maintainability. Their high reliability and quick ignition capabilities make them suitable for tactical battlefield operations, where efficiency and speed are significant. Recent developments reflect a rising demand for miniature propulsion systems.

- For instance, in March 2025, Anduril Industries started working on a lighter solid motor to enhance capacity and efficiency within rocket artillery pods, enabling lightweight single-stage propulsion systems.

The Single Stage segment is expected to lead the market, contributing 65.86% globally in 2026.

By Component

Rise in Demand for High-Performance Thermal Protection Systems and Lightweight Structural Materials Push Motor Casing & Insulation Segment Growth

Based on component, the market is segmented into propellant, igniter, thruster/nozzle, motor casing & insulation, and others.

The Motor Casing & Insulation segment is expected to account for 63.57% of the market in 2026. Motor casing & insulation segment accounts for the largest market share, as there is increasing demand for high-performance thermal protection systems and lightweight structural materials to ensure motor safety under harsh conditions. Insulation shields internal components from high combustion temperatures, and the casing supplies the structural core to house high-pressure gases. Moreover, advances in composite materials such as carbon fiber-reinforced polymers and advanced ablative liners boost durability, reduce weight and enable higher thrust-to-weight ratios, driving segment growth.

- For instance, in December 2024, Aerojet Rocketdyne, a unit of L3Harris, started adding new light composite casings to tactical missile systems to enhance agility and range

The propellant segment is expected to grow with a steady growth rate of CAGR of 8.0% over the forecast period.

By End User

Surge in Global Tensions and Increase in Defense Budget Push Defense Segment Growth

Based on end user, the market is segmented into space agencies, research institutes and defense.

The Defense segment is projecteed to dominate the market with a share of 60.98% in 2026. The segment dominance stems from expanding defense budgets globally, growing geopolitical tensions and upgrading missile and artillery systems. Solid rocket motors are widely employed in short- and medium-range ballistic missiles, tactical rockets, anti-aircraft missiles and interceptor systems. Their quick response, low logistical support and simplicity of deployment make them appropriate for military use.

- For instance, in March 2025, Anduril Industries received a substantial contract from the U.S. Army to develop a next-generation SRM for artillery and tactical missile systems.

The space agency’s segment is fastest growing segment and is expected to grow with a steady growth rate of CAGR of 7.9% over the forecast period.

Solid Rocket Motor Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

North America

North America Solid Rocket Motor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 2.69 billion in 2025, representing 42.36% of total market revenue, and is projected to reach USD 2.93 billion in 2026. North America dominated due to the increasing defense spending and huge investment in the missile defense system. The persistent interest of the U.S. Department of Defense in missile defense systems, tactical rocket and hypersonic weapons development fuels a strong demand for SRMs in military and aerospace applications.

- For instance, in May 2024, Nammo collaborated with Raytheon, a U.S. defense provider, to expand rocket motor production in Perry, Florida.

U.S. Solid Rocket Motor Market

Based on North America’s strong contribution the U.S. market reached at USD 2.42 billion in 2025. The market in U.S. holds largest share in the region due to defense priorities and space innovation. The market is aggressively expanding domestic solid rocket motor production through partnerships such as Raytheon-Avio for missile applications due to severe supply chain constraints.

- For instance, in November 2025, Raytheon (RTX) signed a MoU with Avio to establish a new U.S. based solid rocket motor facility, securing preferred production capacity for critical weapon systems amid surging demand.

Europe

Europe contributed approximately USD 1.97 billion to the global market in 2025, accounting for 31.03% share, and is expected to reach USD 2.13 billion in 2026, which is the second highest among all region. The region market is growing due to coordinated defense initiatives among EU member countries and the expanding commercial and institutional space launch sectors. This growth is also supported by munitions replenishment, air and missile defense expansion and a shift toward multi-year procurement to secure production slots and rebuild stockpiles. Key players are focusing on solid rocket motor production in various European countries which is expected to drive market growth in the region.

- For instance, in November 2025, Lockheed Martin confirmed at the Dubai Airshow plans for further investments in SRM production in Poland, Germany, and the Middle East to meet surging global demand driven by rising conflicts.

U.K. Solid Rocket Motor Market

The U.K. market in 2025 was at USD 0.42 billion, representing roughly 6.6% of global revenues.

France Solid Rocket Motor Market

France market reached USD 0.58 billion in 2025, equivalent to around 9.2% of global sales.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 1.38 billion, representing 21.77% of global demand, and is projected to grow to USD 1.53 billion in 2026. The growth can be attributed to investment in missile technologies and satellite technologies in major countries such as China, India and Japan. The market is growing as institutional missions require large number of solid stages/boosters and solid subsystems which directly helps the market growth. For instance, China launched Orienspace's Gravity-1, in October 2025, from a Yellow Sea barge which uses seven solid rocket motors. Thus, such developments drive the adoption of SRMs in commercial space launch activities.

Japan Solid Rocket Motor Market

The Japan market in 2025 was at USD 0.28 billion, accounting for roughly 4.4% of global revenues.

China Solid Rocket Motor Market

China’s market is projected to be one of the largest worldwide. Its 2025 revenue was USD 0.57 billion, representing roughly 9.0% of global sales.

India Solid Rocket Motor Market

The India market in 2025 reached USD 0.40 billion, accounting for roughly 6.3% of global revenues.

Rest of the World

Rest of the World recorded a market size of USD 0.31 billion in 2025, capturing 4.84% of the global market share, and is projected to reach USD 0.32 billion in 2026, due to expanding air and missile defense procurement, rising demand for precision strike and interception and a strong push for localization of missile-related industrial work. Moreover, increased procurement of interceptor and guided-weapon inventories in the Gulf and broader MEA drives growth of the market in the region. For instance, in 2022, Saudi Arabia’s GAMI approved localization projects with Lockheed Martin to manufacture THAAD interceptor launchers and canisters.

Middle East & Africa Solid Rocket Motor Market

The Middle East & Africa market was at USD 0.19 billion in 2025, representing roughly 3.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Advanced Propellants and Lightweight Casings by Key Players to Propel Market Progress

The global market remains consolidated, led by major players such as Northrop Grumman Corp, L3Harris Technologies, Lockheed Martin, Raytheon Technologies (RTX), and Nammo AS, which command significant shares through innovations in high-thrust composite propellants and modular thrust vectoring systems. These firms drive market growth via strategic contracts from defense agencies and OEM partnerships. This is expected to increase the importance of development of insensitive, high-energy motors for precision missiles, hypersonic weapons and space launch vehicles across air, sea, land and space platforms. Moreover, players prioritize scalable designs with extended shelf life to support rapid replenishment and next-generation strategic.

- For instance, in January 2026, Northrop Grumman secured a USD 94.3 million U.S. Navy contract to develop a 21-inch Second-Stage Solid Rocket Motor (SSRM) for extended-range missiles targeting air, surface and hypersonic threats.

Other prominent players such as Aerojet Rocketdyne and Avio S.p.A focus on 3D-printed casings, green propellants, and digital twin simulations for optimized performance.

LIST OF KEY SOLID ROCKET MOTOR COMPANIES PROFILED

- Northrop Grumman Corp (U.S.)

- Nammo AS (Norway)

- L3Harris Technologies Inc. (U.S.)

- Anduril (U.S.)

- China Aerospace Science and Technology Corporation (China)

- IHI Corporation (Japan)

- Rafael Advanced Defense Systems Ltd (Israeli)

- Avio S.p.A. (Italy)

- Bayern-Chemie (Germany)

- Ursa Major (U.S.)

- Kratos Defense & Security Solutions (U.S.)

- X-Bow (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: L3Harris announced a USD 1 billion Department of War investment in its Missile Solutions business via convertible preferred security, for a 2026 IPO to ramp up solid rocket motor production for missiles such as PAC-3, THAAD, Tomahawk, and Standard Missile.

- December 2025: Northrop Grumman successfully conducted a static fire test of its prototype Mk 72 SRM at its Elkton, Md., facility, validating performance models and digital twin tech for U.S. Navy needs.

- July 2025: L3Harris announced a USD 1 billion Department of War investment in its Missile Solutions business via convertible preferred security, for a 2026 IPO to ramp up solid rocket motor production for missiles such as PAC-3, THAAD, Tomahawk, and Standard Missile.

- June 2025: Saab selected Anduril Rocket Motor Systems to design, develop, qualify, and produce SRMs for the Ground-Launched Small Diameter Bomb (GLSDB) system, partnering with Boeing.

- April 2025: Raytheon awarded contracts to Northrop Grumman and Nammo to verify design specs and scale production of the Mk 72 solid rocket motor for the U.S. Navy's Standard Missile, amid L3Harris supply constraints.

- January 2025: L3Harris announced a USD 1 billion Department of War investment in its Missile Solutions business via convertible preferred security, for a 2026 IPO to ramp up solid rocket motor production for missiles such as PAC-3, THAAD, Tomahawk, and Standard Missile.

- April 2024: L3Harris Technologies entered into an agreement with Orange County, Virginia, to fund the expansion and modernization of the company’s site in the county. The effort is intended to increase solid rocket motor production while growing the company’s presence in the Commonwealth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform, By Stage, By Component, By End User, and Region |

| By Platform |

|

| By Stage |

|

| By Component |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.35 billion in 2025 and is projected to reach USD 12.99 billion by 2034.

In 2025, the North America market value stood at USD 2.69 billion.

The market is expected to exhibit a CAGR of 8.2% during the forecast period of 2026-2034.

By platform, the missiles segment is expected to lead the market.

The increasing geopolitical tensions and continuous space exploration activities are driving market expansion.

Northrop Grumman Corp, Nammo AS, L3Harris Technologies Inc. and among others are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us