Sovereign Cloud Market Size, Share & Industry Analysis, By Enterprise Type (Small & Medium Enterprises (SMEs) and Large Enterprises), By Application (Data Sovereignty, Operational Sovereignty, and Digital Sovereignty), By Industry (BFSI, Healthcare, Government & Public Sector, Manufacturing, and Others), and Regional Forecast, 2026 – 2034

(Offer valid till 15th Aug 2026)

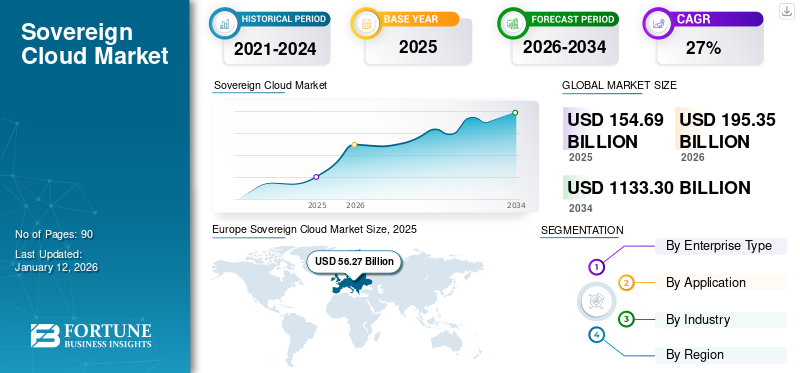

SOVEREIGN CLOUD MARKET SIZE AND FUTURE OUTLOOK

The global sovereign cloud market size was valued at USD 154.69 billion in 2025. The market is projected to grow from USD 195.35 billion in 2026 to USD 1,318.57 billion by 2034, exhibiting a CAGR of 27.0% during the forecast period. Europe dominated the sovereign cloud market with a market share of 36.37% in 2025.

Sovereign cloud refers to cloud services that are offered and provided completely within a specific country's geographical boundaries in order to meet the requirements of local laws governing data privacy and sovereignty. The growth of this market is driven by several factors, including greater compliance with regulatory requirements, meeting the need for enhanced data privacy, and allowing government organizations to retain full control over their data.

Furthermore, many key market players, such as Microsoft Corporation, Amazon Web Services, Inc., Oracle Corporation, Alphabet Inc. (Google LLC), and IBM Corporation, are focusing on forming partnerships with regional telecom operators, technology companies, and government entities. These partnerships aim to build compliant sovereign-cloud ecosystems. These collaborations help vendors combine hyperscale cloud capabilities with local operational control and regulatory compliance.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Adoption of Generative AI Boosting Investment in Cloud Solutions for Secure Data Compliance

Generative AI is shaping and driving the sovereign cloud demand for secure, compliant cloud environments that meet regulations and compliance requirements. Organizations around the globe are utilizing generative AI tools to facilitate the analysis of vast amounts of enterprise data, such as customer records, financial reports, and internal operational documents. They are also using these tools to better utilize the machine learning models created using generative AI. As a result, enterprises and governmental agencies are developing concerns about the processing of data through AI, such as data residency, privacy protection, and the transfer of data across national borders.

- In July 2024, Capgemini Research Institute stated that 80% of organizations increased their investment in generative AI compared with 2023, highlighting the growing need for secure cloud infrastructure to support expanding AI workloads.

Generative AI has clearly added a significant dimension of strategic importance to sovereign cloud infrastructure for both government and private enterprises in many regions. AI-driven workloads require advanced computing resources, scalable storage capabilities, and a strong framework for governance to support secure, compliant data processing. The fulfilment of sovereignty requirements will lead to many more countries and organizations investing in trusted digital infrastructures that enable both sovereign-cloud adoption and AI innovation.

- In January 2025, the European Commission announced plans to mobilize EUR 20 billion to finance up to five AI gigafactories to strengthen regional AI computing capacity and secure digital infrastructure across Europe.

SOVEREIGN CLOUD MARKET TRENDS

Rise of Partnerships between Global Hyperscalers and Local Providers Boosts Market Growth

Partnerships between global hyperscalers and local providers are increasing the sovereign cloud market growth due to an increase in demand for enhanced cloud capabilities and regional presence from end-user organizations. The global hyperscalers provide significant scale, artificial intelligence infrastructure, product range, and research and development strength. On the other hand, the local telecommunications, defense, and technology companies provide knowledge of regulatory requirements regarding regional compliance, a trusted operational footprint and a governance structure that operates within the country. This partnership model helps cloud providers address strict requirements around data residency, local administration, regulatory alignment, and operational independence without forcing customers to give up access to modern cloud and AI services.

As a result, sovereignty-focused cloud offerings are transitioning toward co-developed sovereign offerings. The global hyperscalers provide the technology that supports the cloud sovereignty offerings, and the local partner is responsible for the day-to-day operations, governance, or legal control of the cloud offering in the relevant jurisdiction.

- In June 2025, Microsoft announced expanded sovereign cloud solutions for Europe and highlighted its National Partner Cloud model, including partnerships such as Bleu in France and Delos Cloud in Germany.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Cloud Adoption in Regulated Industries to Fuel the Market Growth

With the rapid shift of industries such as banking, healthcare, government, energy, and telecommunications to the cloud, there comes a need for these heavily regulated organizations to update their old infrastructure, support digital services, and utilize AI and Analytics. In addition, many of these industries must work within strict requirements of data residency, auditability, security, and operational control. Sovereignty-focused cloud solutions will allow these organizations to take advantage of the scalability and flexibility of the cloud while maintaining their sensitive workloads within defined legal jurisdictions and governance structures.

- In May 2025, Oracle announced that organizations across Germany, including an insurance association and a healthcare technology provider, selected Oracle EU Sovereign Cloud to manage critical data and applications.

- In the EU, 84.67% of large enterprises used paid cloud computing services in 2025, up from 77.77% in 2023, while 66.78% of medium-sized enterprises used paid cloud services in 2025, up from 59.09% in 2023.

The uptake of cloud by large enterprises, including those in highly regulated sectors, indicates an increasing need for cloud computing platforms that meet sovereignty and compliance requirements.

MARKET RESTRAINTS

High Infrastructure Costs and Scalability Limitations May Hinder Market Growth

Sovereign cloud environments contain unique IT infrastructure requirements from a legal perspective. These cloud environments need to be physically located in the specific nation of operation. This imposes significant geographical constraints on the ability to establish an infrastructure base compared to standard public clouds that use perimeter security installed globally on multi-level servers distributed around the world. Sovereign-clouds require a fully dedicated physical infrastructure base, including local data centers, isolated networks, local operation teams, geo-specific operational staff, and geo-specific encryption and governance personnel. Thus, the total amount of capital needed to build compliant facilities (e.g., secure data centers, power, network connections, and regulatory audits) is exponentially greater than that of public clouds or other forms of private clouds.

- In November 2025, AWS officially opened the European Sovereign Cloud and stated that the initiative is backed by approximately USD 8 billion investment in infrastructure, job creation, and skills development.

Consequently, cloud solutions provide stronger control over data security and compliance. However, the high cost of infrastructure development and limited scalability across jurisdictions may slow adoption among small and medium-sized enterprises and organizations with constrained IT budgets.

MARKET OPPORTUNITIES

Growing Government Investments in National Digital Infrastructure Fuels Market Growth

Government funding for secure cloud infrastructure and national data platforms is becoming increasingly important, as governments around the world strive to gain more control over their critical data, public services, and cybersecurity frameworks. Cloud service providers are being encouraged to establish local data centers, sovereign cloud zones, and compliant digital platforms to support government and regulated industry workloads.

- In October 2025, the European Commission launched a tender worth up to USD 210 million for sovereign cloud services for EU institutions, highlighting the increasing role of government procurement in accelerating such cloud adoption.

Various governments are making domestic cloud infrastructure a priority in an effort to create broad-based digital sovereignty strategies and reduce reliance on foreign cloud services while improving their data governance. Large-scale public investments into digital infrastructure will continue to create long-term commercial opportunities for sovereign cloud providers and their technology partners.

Segmentation Analysis

By Enterprise Type

Rising Adoption of Sovereign Cloud Solutions by Large Enterprises to Meet Compliance and Data Security Demands

Based on the enterprise type, the market is bifurcated into Small & Medium Enterprises (SMEs) and large enterprises.

Large enterprises accounted for the largest market share in 2025, as they generate greater amounts of sensitive data, engage in cross-border business, and operate under more stringent compliance regimes than smaller enterprises. They typically have larger budgets for secure execution of cloud migration. In April 2024, Capgemini reported that 52% of organizations planned to include sovereignty in their cloud strategy.

Small & Medium Enterprises (SMEs) are anticipated to grow at the highest CAGR of 29.5% over the forecast period, as sovereignty-focused cloud offerings become more accessible through managed services and localized infrastructure. Rising digital adoption is helping smaller firms adopt compliant cloud solutions more quickly. In 2023, the European Commission reported that 41.7% of small businesses used cloud services, showing strong room for future expansion.

By Application

Increasing Focus on Data Sovereignty Fueling Market Growth in BFSI, Healthcare, and Government Sectors

Based on the application, the market is divided into data sovereignty, operational sovereignty, and digital sovereignty.

Data sovereignty accounted for the largest market share in 2025 and is expected to grow at the highest CAGR of 28.6% during the forecast period. This is owing to organizations placing increased focus on protecting sensitive data by limiting its geographic location (jurisdiction) to avoid any potential loss of control. This is especially important for sectors such as BFSI, healthcare, and government. In April 2024, Capgemini reported that 69% of organizations considered data sovereignty a key factor in their cloud strategy.

Digital sovereignty is projected to grow at a prominent CAGR of 26.1% during the forecast period, as organizations will also require significant control over their cloud administration, monitoring, and governance. This is especially critical for industries that are governed by high levels of control due to the nature of their operations and require a secure environment to operate their mission-critical infrastructure and proprietary data. In February 2026, Microsoft stated that Microsoft Sovereign Cloud supports secure AI operations even in disconnected environments.

To know how our report can help streamline your business, Speak to Analyst

By Industry

Strong Government & Public Sector Focus on Data Residency and Security to Drive Market Growth

Based on the industry, the market is categorized into BFSI, healthcare, government & public sector, manufacturing, and others (energy & utilities, etc.).

The government & public sector accounted for a dominant market share in 2025. This growth is owing to organizations managing large amounts of sensitive information, such as citizen data, defense data, and administrative data, which needs to be kept in compliance with laws regarding data residency and national security. In October 2025, the European Commission announced a USD 210 million tender for sovereign cloud services, highlighting strong government investment.

Healthcare is anticipated to grow at the highest CAGR of 30.0% during the forecast period. This is owing to the fact that hospitals and healthcare providers are rapidly digitizing patient records and clinical systems. This increases the need for secure cloud environments. In 2024, Healthcare Information and Management System Society (HIMSS) reported that 86% of healthcare organizations were already using AI technologies, reflecting secure digital infrastructure.

Sovereign Cloud Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Europe

Europe Sovereign Cloud Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe captured the largest sovereign cloud market share in 2024, valuing at USD 45.75 billion, and also maintained the leading share in 2025, with USD 56.27 billion. The market in Europe is experiencing significant growth, as the region has a robust regulatory framework and is increasingly focused on ensuring data sovereignty and digital sovereignty. Many regulations, such as the General Data Protection Regulation (GDPR), have strict requirements for organizations to keep control over the manner in which their data is collected and distributed, as well as how it is eventually stored, processed, or transferred. Owing to this, companies and government agencies prefer to use cloud services that limit where their data can physically exist to their regional or national areas.

- In 2025, Eurostat reported that 52.7% of enterprises in the European Union used paid cloud computing services, reflecting the region's strong cloud adoption base that supports demand for sovereignty-focused cloud solutions.

U.K. Sovereign Cloud Market

The U.K. market in 2026 is estimated at around USD 13.72 billion, representing roughly 7.0% of global revenues.

Germany Sovereign Cloud Market

Germany’s market is projected to reach approximately USD 13.21 billion in 2026, equivalent to around 6.8% of global sales.

North America

North America is projected to record a growth rate of 26.6% in the coming years, which is the second-highest among all regions, and is estimated to reach a valuation of USD 57.50 billion by 2026. The market in North America is expected to increase, owing to its advanced cloud infrastructure and strong regulatory environment. Many organizations from various sectors, such as banking, financial services, insurance, healthcare, government, and defense, are dealing with very sensitive information and require a secure environment in the cloud to comply with strict regulations. Therefore, enterprises and public organizations are increasingly using sovereignty-focused cloud solutions due to their ability to help safeguard sensitive data and provide organizations with greater operational control over critical workloads. These factors play a significant role in fueling the growth of the market.

- In June 2025, the National Institute of Standards and Technology (NIST) published its Zero Trust Architecture practice guide, developed with 24 technology vendors, highlighting the growing focus on secure cloud infrastructure in the U.S.

U.S. Sovereign Cloud Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 40.57 billion in 2026, accounting for roughly 20.8% of global sales.

Asia Pacific

The Asia Pacific region is estimated to reach USD 54.92 billion in 2026 and is expected to grow at the highest CAGR of 32.5% during the forecast period. This growth is owing to the accelerated digital transformation within the region, as well as increased attention being paid to data sovereignty regulations and data protection by both governments and businesses in China, India, Japan, South Korea, and Singapore. These countries continue to adopt cloud technologies and strive to improve data protection through regulations.

- In September 2025, the Asian Development Bank reported that cloud spending in Asia and the Pacific reached USD 203 billion in 2024, highlighting the region's rapidly expanding cloud infrastructure base.

In the region, India and China are both estimated to reach USD 9.09 billion and USD 12.53 billion, respectively, by 2026.

Japan Sovereign Cloud Market

The Japan market in 2026 is estimated at around USD 11.15 billion, accounting for roughly 5.7% of global revenues. This is owing to the increased government support for data sovereignty. The demand for secure cloud solutions, particularly in the finance and healthcare sectors, as well as stricter laws governing the use of personal information in Japan will also continue to contribute to this growth.

China Sovereign Cloud Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 12.53 billion, representing roughly 6.4% of global sales.

India Sovereign Cloud Market

The India market in 2026 is estimated at around USD 9.09 billion, accounting for roughly 4.7% of global revenues.

Rest of the World

In the rest of the world, the Middle East & Africa is estimated to reach USD 8.93 billion in 2026 and is expected to grow at a prominent growth rate in the coming years. This is owing to an increase in investment in digital transformation, increased regulations regarding data privacy, and push for local data residency and sovereignty-focused cloud solutions.

In addition, South America is set to reach a value of USD 4.61 billion in 2026. The region’s growth is based on the increased demand for secure cloud infrastructure within many sectors (specifically banks and health care) as well as due to more stringent regulations around data sovereignty.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Sovereign Cloud Capabilities and Strategic Partnerships by Key Players to Propel Market Competition

The global sovereign cloud market has a semi-consolidated structure, with prominent players such as Microsoft Corporation, Amazon Web Services, Inc., Oracle Corporation, Alphabet Inc. (Google LLC), and IBM Corporation holding significant positions. These companies are driving market growth through continuous investments in secure cloud infrastructure, compliance with regional data residency regulations, and advanced data protection technologies. Advancements in cloud technologies, such as enhanced encryption, multi-layered security frameworks, and real-time data processing are enabling secure, compliant, and efficient cloud services for both government and enterprise applications.

Other notable players in the global market include OVH Group S.A., Hewlett Packard Enterprise Development LP, T-Systems International GmbH, Orange S.A., and Huawei Technologies Co., Ltd. These companies are increasingly focusing on improving cloud infrastructure usability, enhancing compliance with local data protection laws, and scaling cloud services to meet rising demand. Strategic investments in these cloud ecosystems, partnerships for data sovereignty, and expansion into new regional markets are expected to strengthen their market positioning.

LIST OF KEY SOVEREIGN CLOUD COMPANIES PROFILED

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Alphabet Inc. (Google LLC) (U.S.)

- OVH Group S.A. (France)

- Hewlett Packard Enterprise Development LP (U.S.)

- Amazon Web Services, Inc. (U.S.)

- T-Systems International GmbH (Germany)

- Orange S.A. (France)

- Huawei Technologies Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Microsoft expanded its sovereign cloud capabilities to support AI workloads, introducing new security, data governance, and compliance features to help enterprises maintain control over sensitive data while deploying AI models in regulated environments.

- January 2026: IBM introduced IBM Sovereign Core, an AI-ready sovereign-enabled software platform designed for enterprises, governments, and service providers to build, deploy, and manage sovereign environments. The solution is intended to strengthen operational control, jurisdictional compliance, and digital sovereignty for cloud-native and AI workloads.

- November 2025: Google Cloud launched its first Sovereign Cloud Hub in Munich, Germany. The company aimed at strengthening its sovereignty-focused cloud capabilities across Europe. The facility enables regional customers and partners to collaborate on Google Sovereign Cloud solutions while supporting compliance with European data sovereignty, privacy, and security requirements.

- October 2025: Oracle expanded its Oracle Cloud Infrastructure (OCI) sovereign cloud capabilities, enabling customers to deploy full cloud and AI stacks in sovereign environments through offerings such as Exadata Cloud@Customer and Compute Cloud@Customer. These solutions allow governments and enterprises to run cloud workloads while maintaining local data control and regulatory compliance.

- June 2025: IBM supported Telkom Indonesia in building an AI-powered sovereign platform using IBM Watsonx, aimed at local industries such as healthcare, telecom, education, and financial services. The initiative strengthens IBM’s role in sovereign cloud and sovereign AI deployments by enabling locally governed platforms tailored to national requirements.

- June 2025: Oracle partnered with Nextcloud, a European company, to enable governments and enterprises to deploy collaboration capabilities across OCI sovereignty-focused cloud environments. This development strengthens Oracle’s sovereign cloud value proposition by combining secure cloud infrastructure with privacy-focused collaboration tools for regulated users.

- March 2025: DEEP by POST Group and OVHcloud announced a strategic partnership to deploy a sovereign cloud infrastructure in Luxembourg. The initiative aims to strengthen national digital sovereignty by providing secure cloud services for public sector and enterprise customers while ensuring compliance with European data protection and regulatory frameworks.

REPORT COVERAGE

The global sovereign cloud market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 27.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Enterprise Type, Application, Industry, and Region |

| By Enterprise Type |

|

| By Application |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 154.69 billion in 2025 and is projected to reach USD 1,318.57 billion by 2034.

In 2025, the market value stood at USD 56.27 billion.

The market is growing at a CAGR of 27.0% during the forecast period.

By application, data sovereignty segment is expected to lead the market.

Rapid cloud adoption in regulated industries to fuel the market growth.

Microsoft Corporation, Amazon Web Services, Inc., Oracle Corporation, Alphabet Inc. (Google LLC), and IBM Corporation are the major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 100

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us