The Japan market is projected to reach USD 0.12 billion by 2026, the China market is projected to reach USD 1.9 billion by 2026, and the India market is projected to reach USD 0.33 billion by 2026.

Soy Flour Market Size, Share & Industry Analysis, By Type (Full-fat and Defatted), By Application (Bakery & Confectionery, Meat Substitutes, Soup & Sausages, Meat & Poultry, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

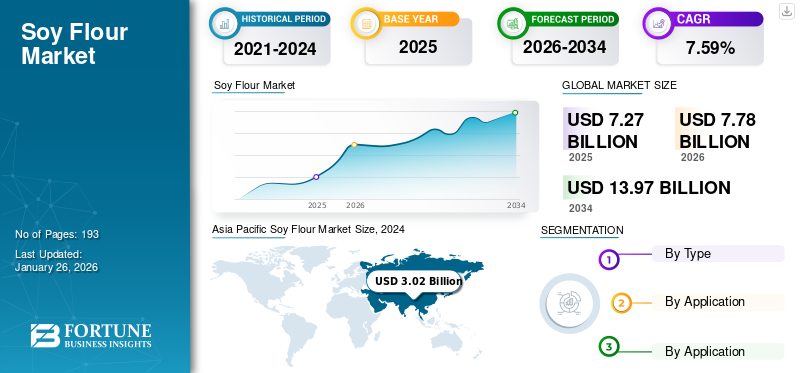

The global soy flour market size was valued at USD 7.27 billion in 2025. The market is projected to grow from USD 7.78 billion in 2026 to USD 13.97 billion by 2034, exhibiting a CAGR of 7.59% during the forecast period. Asia Pacific dominated the soy flour market with a market share of 44.55% in 2025.

Soy flour is a powder made from soybeans. It is one of the fastest-growing segments of the global soy derivatives market. The emerging vegan and plant-based diet, coupled with the rising popularity of protein-rich foods and the growing consumption of processed foods, is driving the demand for soy flour globally. The emerging trend of non-GMO flour is likely to contribute to the industry's growth in the upcoming years. Some of the prominent players operating in the global market are Cargill Inc., DuPont, Wilmar International, CHS Inc., and ADM.

Download Free sample to learn more about this report.

SOY FLOUR MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 7.27 Billion

- 2026 Market Size: USD 7.78 Billion

- 2034 Forecast Market Size: USD 13.97 Billion

- CAGR: 7.59% from 2026–2034

- Asia Pacific dominated the soy flour market with a 44.55% share in 2025.

- The defatted soy flour segment held the largest market share in 2024.

- The bakery & confectionery segment accounted for the dominant market share in 2024.

North America

North America accounted for USD 1.93 billion in 2025 and is expected to reach USD 2.06 billion in 2026 due to rising demand for non-GMO and protein-based products.

Europe

Europe generated USD 0.47 billion in 2025 and is projected to reach USD 0.50 billion in 2026, supported by growing consumption of plant-based meat alternatives.

Asia Pacific

Asia Pacific led the market with USD 3.24 billion in 2025 and is projected to reach USD 3.47 billion in 2026, driven by strong demand for protein-rich foods.

U.S.

The soy flour market is projected to reach USD 1.87 billion by 2026, driven by increasing demand for protein-enriched and non-GMO food products.

Japan

The soy flour market is projected to reach USD 0.12 billion by 2026, supported by rising consumption of processed and plant-based foods.

Read More

SOY FLOUR MARKET TRENDS

Adoption of the Product in Snacks Industry to Shape Market Landscape

The product has been widely adopted in ready-to-eat snacks in recent years. The product contains a rich protein content and offers a crunchiness to snack products. Additionally, RTD snack manufacturers are adding soy flour along with several other traditional flours such as wheat, rice, and gram flour to enhance the nutritional content. It is further contributing to the industry's growth. For instance, in December 2024, Bikano, one of the emerging Indian snack companies, launched an Indian traditional snack item – soy sticks. The new product is made from rice flour, soy flour, and spices. Such development will drive the product demand during the forecast period.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Food Fortification for Better Health and Wellness to Drive Market Growth

In the post-pandemic era, consumers are often seeking nutrition-rich and fortified food products to achieve their health & wellness. Soy flour is one of the key ingredients rich in protein, lysine, and minerals such as iron. Infusion of soy flour along with other flours, including wheat and corn, will enhance the nutritional quality of end products such as cookies, bread, and other processed foods. Owing to its rich protein and essential amino acids, soy flour has become one of the most versatile options for food industry players, including bakery, processed meat, tortilla, and other snacks. Its functional and nutritional aspects make it a cost-effective way to enhance the nutritional value of processed foods.

Rapidly growing demand for fortified processed food and beverages is significantly driving the global soy flour market growth. Furthermore, increasing demand for protein-rich supplements and weight management products among adults is leading key companies to invest in research and development activities to develop new products. It is further contributing to the soy-based products, including flour, across the globe.

MARKET RESTRAINTS

Digestive-related Allergies Associated with Soy to Hamper Market Growth

Despite their nutritional benefits and functionality, soy products, including flour, have several limitations. One of the key restraints is the prevalence of allergies associated with soy. Soy allergy is a more common allergy among infants, children, and adults across the globe, especially in the U.S. and Europe. It may cause serious reactions and irritations in soy-sensitive users. Additionally, soy contains high fiber and antinutrients, such as phytic acid and trypsin inhibitors, which may cause digestive discomfort, such as bloating or flatulence, among users. Therefore, consumers are often looking for allergen-free food products. It may negatively impact the global soy flour market growth in the near future.

MARKET OPPORTUNITIES

Consumers Shift Toward Non-GMO Flours to Change the Industry Landscape

A larger proportion of the population across the globe is shifting toward non-GMO. As awareness about the benefits of non-GMO foods, health consciousness, and environmental benefits associated with non-GMO foods is expanding gradually, individuals are inclining to opt for such products over traditional ones. According to the non-GMO Project, a non-profit organization promoting organic and non-GMO foods, in 2024, nearly two-thirds (65%) of consumers prefer to purchase products that are certified USDA organic or non-GMO in the U.S. As a result, companies are incorporating this trend to commercialize their offerings by launching products in this category in order to achieve significant growth in the future. It will drive the industry’s growth during the forecast period. For instance, in February 2022, Benson Hill Inc., one of the key soybean manufacturing and processing companies, launched the TruVail line of non-GMO soy protein ingredients, including a high-protein flour, a “less processed” soy protein concentrate, and texturized proteins for protein-rich and plant-based food applications.

Segmentation Analysis

By Type

Defatted Segment Leads Market Due to High Nutritional Content and Reduced Fat

Based on type, the market is divided into defatted and full-fat.

The defatted segment held a leading share of the global market in 2024. During the process of defatting, the processor removes most of the natural oils in soybeans. Thus, it contains high protein content and a concentrated nutritional profile. Furthermore, as fat is reduced during the defatting process, this flour offers a lower-fat and lower-calorie option compared to regular soy flour. High protein, low-fat, and extended shelf life make it an ideal ingredient in bakery and processing food applications such as bread, cookies, pancakes, processed meats, pizza toppings, and other food products. The wide application of the defatted flour in the food industry primarily contributes to the steady growth.

The full-fat is another prominent segment exhibiting steady growth. Unlike defatted flour, full-fat soy flour contains high protein content and essential ingredients for building and repairing tissues. Furthermore, it contains various beneficial components such as vitamins, minerals, and isoflavones. Thus, the full-fat flour has been significantly used in protein-rich packaged meals, supplements, and other applications. Increasing weight management supplements and protein-rich processed and packaged meals are driving segment growth.

By Application

Multiple Applications of the Product Influenced Bakery & Confectionery Segment Growth

Based on application, the market is classified into bakery & confectionery, meat substitutes, soup & sausages, meat & poultry, and others.

The bakery & confectionery segment held the dominant share in 2024, mainly due to the wide application of the product in bakery manufacturing products. Soy flour, especially defatted flour, offers various functional benefits, including enhanced protein content, improved dough machinability, and contributes to better crumb structure and texture. Therefore, it is significantly utilized in producing bakery products such as bread, cookies, and cakes. Increasing protein-fortified bakery products is likely to drive the segment expansion in the coming years.

The meat substitutes segment is anticipated to grow at the fastest CAGR during the forecast period. Globally, meat substitutes are significantly increasing due to changing consumers' food choices, rising popularity of the vegan diet, technological advancements, celebrity endorsements, and growing preference for sustainable and ethical food choices. Owing to unique functional properties such as fat retention, stable consistency, texture, and stable emulsion, soy flour has been widely used in manufacturing meat substitutes ranging from sausages to hamburgers, meatballs, and pâtés. Therefore, the demand for the product is anticipated to expand at the highest growth rate.

Soy Flour Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and Middle East & Africa.

Asia Pacific

Asia Pacific Soy Flour Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific maintained a strong presence in the global market, reaching USD 3.24 billion in 2025, accounting for 44.55% share, and is expected to reach USD 3.47 billion in 2026. Increasing health concerns and protein-rich food product demand among millennials and Gen-Z consumers are significantly driving the demand for the product across the region. Furthermore, rising disposable income, the growing women's employment rate, and urbanization are driving the demand for processed foods, including bakery, processed meals, and meat & poultry products. Soy flour is used as one of the key ingredients in the processed foods industry. It is driving the market growth across the region, including China, India, Australia, and Japan.

China is one of the key markets for soy flour in the Asia Pacific region. Increasing soy consumption in the country is positively influencing the product demand. According to the USDA Foreign Agricultural Service’s Global Agricultural Information Network (GAIN) report, the domestic consumption of soybeans in the country has been estimated at 124.4 million tons for 2025-26.

North America

In 2025, the North America market stood at USD 1.93 billion, representing 26.59% of global demand, and is projected to grow to USD 2.06 billion in 2026. North America is one of the key markets in the global space. The increasing non-GMO, organic, and natural trends are widely influencing the soy flour demand growth in the region. According to the Pew Research Center, more than 51% of adults strongly believe that GMO products are harm to health. As a result, non-GMO soybean flour is anticipated to emerge in the American countries such as the U.S., Canada, and Mexico. Additionally, adult demographics are increasingly shifting toward protein-rich products to achieve their physical and athletic goal is further contributing to the market growth in the region. The U.S. market is projected to reach USD 1.87 billion by 2026.

Europe

The Europe region captured 6.41% of the global market in 2025, generating USD 0.47 billion in revenue, and is projected to reach USD 0.5 billion in 2026. Rapidly growing plant-based protein product consumption, particularly meat alternatives popularity is driving the product demand in European countries such as Germany, Italy, France, and the U.K. According to the Good Food Institute, a non-government organization promoting a vegan diet, the retail sales of vegan meat/plant-based meat alternatives were valued at USD 404.67 million in 2023. Soybean flour is one of the key ingredients used in producing meat alternatives, and the rising popularity of plant-based meat alternatives in European countries is likely to propel the market growth. The UK market is projected to reach USD 0.04 billion by 2026, while the Germany market is projected to reach USD 0.06 billion by 2026.

South America

South America is one of the emerging markets for soybean flour. Growing urbanization and disposable income across South American countries such as Brazil, Argentina, and Peru are likely to create a potential market for processed foods and bakery products. It is anticipated to drive the product demand across the region. Additionally, Brazil is one of the key soybean manufacturing countries in the world. According to the U.S. Foreign Agriculture Service, Brazil produced nearly 169 million metric tons of soybeans in 2024/25, which accounts for 40% of the global soybean production. Easy accessibility of raw material and the emerging processed food industry are likely interconnected to drive the demand for soybean flour across the region.

Middle East & Africa

The Middle East & Africa market accounted for USD 0.27 billion in 2025, representing 3.73% of the global industry, and is expected to reach USD 0.29 billion in 2026. The Middle East & Africa market is anticipated to grow at a steady CAGR during the forecast period. Increasing adoption of Western culture, paired with the rising convenience food products demand is likely to influence the soybean flour market. Additionally, soybean flour is a cheaper ingredient available to enhance the protein content in end-products such as bread, meat and sausages, snacks, and supplement products. It allows food manufacturers operating in sectors such as bakery, processed and packed products in order to cater to consumers at an affordable price. It is anticipated to drive the product demand in the near future.

Latin America

In 2025, Latin America represented USD 1.36 billion, accounting for 18.73% of the worldwide market, and is projected to grow to USD 1.46 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding Production Capacity to Meet Product Demand

The global soy flour market share is highly competitive, with companies focusing on penetrating activities such as expanding their production capacity, developing new products, product innovation, technology adoption, and expanding geographical reach. Emerging players such as

Cargill Inc., DuPont, Wilmar International, CHS Inc., Archer Daniels Midland Company, Bob’s Red Mill Natural Foods, and others are some of the major players in the global market. Cargill Inc. holds the leading position in the industry with its strong geographical presence, diversified portfolio, and processing capacity in the soy flour segment. For instance, in November 2023, Cargill Inc. completed its expansion and modernization project at its soybean processing unit in Sidney, Ohio. The company has invested USD 475 million to improve and increase the soy processing facilities in the U.S.

LIST OF KEY SOY FLOUR COMPANIES PROFILED

- Cargill Inc. (U.S.)

- ADM (U.S.)

- CHS Inc. (U.S.)

- DuPont (U.S.)

- Wilmar International Ltd (Singapore)

- Foodchem International Corporation (China)

- Sun Nutrafoods (India)

- Seasons International Pvt. Ltd (India)

- American International Foods, Inc. (U.S.)

- Avi Agri Business Limited (India)

KEY INDUSTRY DEVELOPMENTS

- September 2024 - Bartlett, a family-owned company, opened a new soybean processing plant in Cherryvale, Kansas. The new plant has the capacity of approximately 49 million bushels of soybeans annually.

- February 2024 – Amfora Inc., a biotechnology company specializing in developing sustainable protein products, launched its ultra-high plant protein products - Amfora Ultra-High Protein Soy flour, Texturized Vegetable Protein, and Crisps to the market.

- September 2023 - Grain Processing Corp. (GPC), part of the KENT Corp., acquired a soy flour manufacturing and warehouse facility in Oskaloosa, Iowa. The newly acquired 64,000-square-foot production plant will allow the company to increase its clean-label soy processing capacity.

- May 2022 – ADM, one of the key global food ingredients manufacturing companies, expanded its non-GMO soybean processing plant in Mainz, Germany. The base expansion plan will allow the company to meet the growing market demand for non-GMO food ingredients demand in the region.

- November 2021 - Ag Processing Inc., an American cooperative agriculture processing company, expanded the soybean processing capacity of its Sergeant Bluff, IA soybean processing plant.

REPORT COVERAGE

The soy flour market report analysis provides global soy flour market share, size & forecast by all the segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the prevalence of the product in key regions/countries, key industry developments, new product launches, and details on partnerships, mergers & acquisitions in key countries. The report covers the global industry analysis, a detailed competitive landscape with information on the market share, and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.40% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.78 billion in 2026 and is projected to reach USD 13.97 billion by 2034.

The market is expected to exhibit a CAGR of 7.59% during the forecast period of 2025-2032.

By type, the defatted segment led the market in 2025.

Growing food fortification for better health and wellness propels market expansion.

Cargill Inc., DuPont, Wilmar International, CHS Inc., and ADM are some prominent players in the global market.

Asia Pacific dominated the market in 2025.

Popularity of non-GMO foods to shape the industry landscape in the near future.

Seeking Comprehensive Intelligence on Different Markets?Get in Touch with Our Experts

Speak to an Expert

- 2021-2034

- 2025

- 2021-2024

- 193

-

(Offer valid till 15th Jul 2026)

Download Free Sample

Jump to Content

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Food & Beverages

Clients

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us