Space-Based Defense Platforms Market Size, Share & Industry Analysis, By Platform Type (Dedicated Military Satellites, Dual-use Defense-tasked Platforms, Hosted Payload Platforms, and Others), By Orbit (Low Earth Orbit, Medium Earth Orbit, Geostationary Orbit, and Highly Elliptical Orbit), By Application (ISR and SIGINT, Secure SATCOM, Missile Warning & Tracking, PNT / Navigation & Timing, Space Domain Awareness, and Defense Meteorology), By End User (Defense Ministries / DoD, Armed Forces / Space Commands, Intelligence Agencies, and Others), and Regional Forecast, 2026-2034

Space-Based Defense Platforms Market Size and Future Outlook

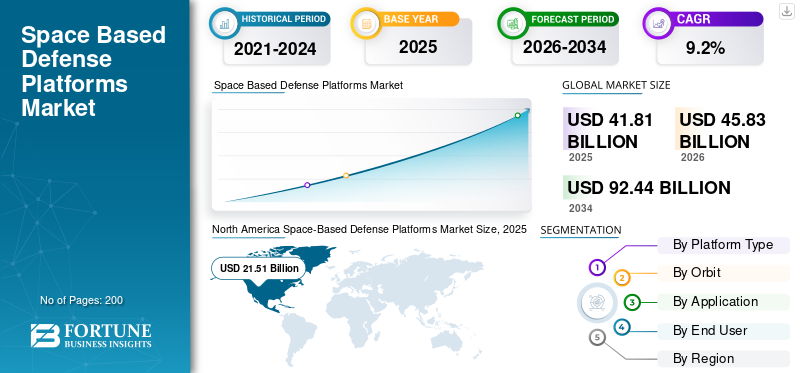

The space-based defense platforms market size was valued at USD 41.81 billion in 2025. The market is projected to grow from USD 45.83 billion in 2026 to USD 92.44 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period. North America dominated the space-based defense platforms market with a market share of 51.44% in 2025.

The space-based defense platforms market is a combination of military satellites, defense-specific commercial platforms, hosted payloads, and small satellite systems used for national security, secure communications, ISR, missile warning, navigation, space situational awareness, and surveillance and reconnaissance. The market is expanding due to rising geopolitical tensions, rising defense budgets, rising defense infrastructure, and rapid innovations in artificial intelligence and space technologies that are compelling governments to improve orbital defense capabilities.

Key players such as Northrop Grumman Corporation, Lockheed Martin Corporation, RTX Corporation, Boeing Company, Airbus Defence and Space, Thales Alenia Space, L3harris Technologies Inc., Leonardo S.p.A., and Israel Aerospace Industries are shaping the market through advanced satellite communication systems, missile-warning payloads, ISR platforms, and resilient ground networks.

Download Free sample to learn more about this report.

Space-Based Defense Platforms Market Key Takeaways

- 2025 Market Size: USD 41.81 billion

- 2026 Market Size: USD 45.83 billion

- 2034 Forecast Market Size: USD 92.44 billion

- CAGR: 9.2% from 2026–2034

- North America dominated the space-based defense platforms market with a market share of 51.44% in 2025.

- The Low Earth orbit segment is expected to show the fastest growth, registering a CAGR of 12.9% over the forecast period.

- The Space domain awareness segment is expected to show the fastest market growth, registering a CAGR of 13.9% over the forecast period.

North America

North America holds the largest market share for space-based defense platforms solutions and is anticipated to grow at a CAGR of 8.9% over the forecast period.

Europe

The market is projected to expand at a 9.5% CAGR during the forecast period, driven by rising defense spending, secure satellite communications modernization, and increasing investments in space resilience.

Asia Pacific

The region is anticipated to grow at a 10.4% CAGR, fueled by expanding defense satellite programs, space situational awareness initiatives, and growing security requirements across the Indo-Pacific.

U.S.

The U.S. market stood at USD 20.70 billion in 2025 and is growing at a CAGR of 8.7% over the forecast period.

Japan

Japan's market growth is supported by expanding X-band defense communications and intelligence-gathering satellite programs, contributing to the region's increasing investment in defense-space capabilities.

Read More

Space-Based Defense Platforms Market Trends

Proliferated LEO Defense Satellite Architectures to Reshape Market Growth

The global market is moving toward the replacement of several big expensive satellites with small constellations of LEO satellites providing the capabilities of missile detection and warning, tactical data relay, ISR, and resilient communications satellites. This trend is being propelled by increasing geopolitical tensions, anti-satellite threats, and the demand for a more robust infrastructure that could withstand any possible disruption. Rather than relying solely on the strategic GEO platforms, there is an increased use of the small replaceable satellites connected through optical crosslinks, artificial intelligence and command and control across multiple orbits.

In October 2023, the U.S. Space Development Agency awarded contracts worth about USD 1.3 billion to Northrop Grumman and York Space Systems for 100 Tranche 2 Transport Layer Alpha satellites under the Proliferated Warfighter Space Architecture.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Geopolitical Tensions Drive Demand for Space-Based Missile Warning and Resilient Defense Networks

Geopolitical tension is one of the major factors propelling the global space-based defense platforms market growth. Countries have started to focus on their satellites not just as supportive platforms, but as integral components for their security and defense systems, including missile warning systems and ISR programs and even communications between battlefield units. Due to an increase in threats from hypersonic weapons, ballistic missiles, and other electronic and anti-satellite threats, there is an increasing importance on deployment of multi-orbit satellites, space communication systems that are shielded, space situational awareness, and AI-supported surveillance & reconnaissance platforms.

MARKET RESTRAINTS

High Program Cost and Schedule Risk Restrains Market Growth

High development cost, payload complexity, and long qualification cycles continue to be a major restraint on the market. Defense satellites must include radiation-hardened electronics, secure payloads, encrypted ground systems, launch integration, and years of validation before they can enter service. This makes the market difficult for smaller buyers and can delay even well-funded national security programs. As defense budgets are spread across weapon systems, naval modernization, air defense, cyber and space technologies, governments may slow, restructure, or cancel satellite programs if costs rise too fast. This restraint is particularly acute in protected satellites communication, missile-warning, and command-and-control programs, where technical failures can directly affect defense capabilities and operational readiness.

MARKET OPPORTUNITIES

Commercial and Dual-Use Satellite Integration Opens New Growth Opportunities

Major opportunity in the global market is the growing use of commercial and dual-use satellite networks for military missions. Defense agencies are increasingly looking beyond fully owned military satellites and using commercial LEO/MEO connectivity, hosted payloads, and data services to improve resilience, reduce deployment timelines, and lower program risk. This creates strong growth opportunities for satellite operators, payload suppliers, ground-segment providers, and analytics companies supporting secure SATCOM, ISR, space situational awareness, and battlefield connectivity.

MARKET CHALLENGES

Electronic Warfare and Signal Interference Challenge Space-Based Defense Reliability

Major challenge for the market is the rising use of electronic warfare, especially GPS/GNSS jamming, spoofing, SATCOM interference, and cyber-linked disruption. Modern defense infrastructure depends on satellites communication, PNT, ISR feeds, space situational awareness, and real-time surveillance and reconnaissance, but these links can’t be replaced by relatively low-cost electronic attack systems. This creates a difficult operating environment for defense ministries and key players as future platforms must be technologically advanced enough to operate in contested, jammed, or spoofed conditions. As a result, market growth is not only tied to launching more satellites, but also to building resilient waveforms, anti-jam payloads, hardened ground stations, AI-enabled anomaly detection, and backup navigation methods.

Impact of Russia-Ukraine and Middle East Conflicts

Russia-Ukraine and Middle East Conflicts Accelerate Demand for Resilient Space-Based Defense Platforms

The Russia-Ukraine war and ongoing Middle East conflicts have made space-based capability a frontline requirement rather than a distant strategic asset. Ukraine has shown how commercial and military satellites can support battlefield connectivity, targeting, ISR, and real-time command links, while Russian jamming and spoofing have exposed the vulnerability of satellite communication and PNT-dependent operations. In the Middle East, missile, drone, and maritime-security threats are strengthening demand for missile warning, secure SATCOM, surveillance and reconnaissance, and space situational awareness. Together, these conflicts are pushing defense ministries to prioritize proliferated LEO constellations, hardened ground systems, anti-jam communications, AI-enabled intelligence processing, and multi-orbit resilience.

Segmentation Analysis

By Platform Type

Due to Mission-Critical Sovereign Capability, Dedicated Military Satellites Dominated Platform Type Segment

In terms of platform type, the market is categorized into dedicated military satellites, dual-use defense-tasked platforms, hosted payload platforms, and small satellite / cubesat platforms.

The dedicated military satellites segment held the largest global space-based defense platforms market share in 2025, since governments give priority to have their own, dedicated military satellite to conduct important missions such as ISR, missile warning, encrypted SATCOM, PNT services, SSA, and strategic C2 operations. The benefit of the dedicated military satellites over commercial and hosted payloads is that defense ministries have greater control over the security aspects, encryption, prioritization of tasks, data processing, and availability of the assets during hostilities. This is important for sensitive national security missions when there could be access-related issues if third-party capacity were used. Despite the rapid expansion of the small satellite and dual-use satellite subcategories, the dedicated military satellite subcategory continues to play a critical role in the defense infrastructure.

Hosted payload platforms segment is expected to grow at a highest CAGR of 12.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Orbit

Geostationary Orbit Leads Due to its Wide-Area Secure Communications Coverage

On the basis of orbit, the market is classified into low Earth orbit, medium Earth orbit, geostationary orbit, and highly elliptical orbit.

Geostationary orbit segment held the largest global market size in 2025, as GEO satellites remain the most reliable option for wide-area military communications, strategic command links, theater-level connectivity, and government-controlled broadcasting over large areas. The ability of GEO platforms to provide constant coverage over priority areas, support secure SATCOM, link deployed forces, and reduce the number of ground handovers required is mainly appealing to defense users. While LEO and MEO systems are expanding at a faster pace due to ISR, missile tracking, and proliferated architectures, GEO continues to lead in value as high-capacity defense communications satellites are costly, long-lived, and central to national security operations.

Low Earth orbit segment is expected to show the fastest growth, registering a CAGR of 12.9% over the forecast period.

By Application

Due to Persistent Battlefield Intelligence Needs, ISR and SIGINT Segment Dominated Application Segment

By application, the market is further divided into ISR and SIGINT, secure SATCOM, missile warning & tracking, PNT / navigation & timing, space domain awareness, and defense meteorology.

The ISR & SIGINT segment held the largest global market size in 2025, since space-enabled defense systems have become an important part of surveillance, electronic intelligence, maritime surveillance, border patrol, and battle situational awareness activities. The Defense customers depend upon ISR & SIGINT satellites for detecting troop movements, naval operations, missile deployment tracking, emissions detection, and decision-making processes. Moreover, it is the leading segment as all the major defense-space clients require continuous surveillance in the pre-conflict, mid-conflict, and post-conflict periods, whereas some applications such as missile warning, SDA, and defense meteorology are mission-specific. The growing geopolitical tensions are expected to boost the demand for ISR & SIGINT services during the forecast period.

Space domain awareness segment is expected to show the fastest market growth, registering a CAGR of 13.9% over the forecast period.

By End User

Due to Centralized Procurement Authority, Defense Ministries / DoD Segment Dominated End User Segment

Based on end user, the market is segmented into defense ministries / DoD, armed forces / space commands, intelligence agencies, and homeland / border / maritime security.

Defense ministries / DoD held the largest global market demand in 2025, as most space-based defense platforms are funded, approved, and procured through national defense ministries, departments of defense, and central acquisition agencies. These organizations control the largest defense budgets and are responsible for long-term programs covering military satellites, secure SATCOM, ISR, missile warning, PNT resilience, space situational awareness, and protected command-and-control networks. Additionally, armed forces, space commands, and intelligence agencies are increasingly important operational users, Defense Ministries / DoD remain the primary budget holders and contracting authorities behind large-scale satellite constellations, ground systems, and defense infrastructure modernization.

Armed forces / space commands segment is expected to show the fastest market growth, registering a CAGR of 10.9% over the forecast period.

Space-Based Defense Platforms Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Space-Based Defense Platforms Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share for space-based defense platforms solutions, and is anticipated to grow at a CAGR of 8.9% over the forecast period. North America dominates as the U.S. has the world’s most advanced and highest-funded defense-space ecosystem, supported by the U.S. Space Force, Space Systems Command, the National Reconnaissance Office, Missile Defense Agency, and major contractors such as Northrop Grumman, Lockheed Martin, RTX, Boeing, L3Harris, and SpaceX. The region also leads in dedicated military satellites, protected SATCOM, missile warning and tracking, ISR, PNT modernization, space situational awareness, and proliferated LEO architectures.

U.S. Space-Based Defense Platforms Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at USD 20.70 billion in 2025, growing at a CAGR of 8.7% over the forecast period.

Europe

Europe market is anticipated to grow at a second fastest pace by registering a CAGR of 9.5% during the forecast period. Europe market is supported by rising defense budgets, sovereign ISR requirements, secure SATCOM modernization, and stronger focus on space-domain resilience after the Russia-Ukraine war. With Russia considered within Europe, the region has a broad mix of legacy military-space capability and fast-growing NATO/EU investment. France, the U.K., Germany, Italy, and Russia remain the core defense-space buyers, while Poland, the Nordics, Spain, and other European countries are increasingly investing in dual-use platforms, hosted payloads, and small satellite architectures.

France Space-Based Defense Platforms Market

France reached a valuation of USD 1.57 billion in 2025, and is anticipated to grow at the CAGR of 8.1% during the forecast period.

Asia Pacific

Asia Pacific is anticipated to grow at a CAGR of 10.4% over the forecast period, driven by China’s large military-space architecture, India’s expanding defense satellite roadmap, Japan’s X-band defense communications and intelligence-gathering satellites, South Korea’s reconnaissance programs, and Australia’s move toward resilient multi-orbit communications. The region’s demand is shaped by Indo-Pacific security competition, maritime-domain awareness, border surveillance, missile-warning needs, and rising investment in space situational awareness.

China Space-Based Defense Platforms Market

The Chinese market revenues stood at USD 3.77 billion in 2025, and is anticipated to grow at the CAGR of 9.1% during the forecast period.

South Korea Space-Based Defense Platforms Market

The South Korean market stood at USD 0.59 billion in 2025, accounting for roughly 7.02% of Asia Pacific revenues.

Rest of the World

Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a 6.4% CAGR during the forecast period. Middle East & Africa has the largest share, driven by secure SATCOM, ISR, missile threat awareness, border monitoring, maritime surveillance and sovereign security programmes. Latin America is slower to develop, with demand focused on dual-use Earth observation, anti-trafficking surveillance, disaster response, strategic communications, and border security.

Latin America Space-Based Defense Platforms Market

The market in Latin America reached a valuation of USD 0.67 billion in 2025 and is anticipated to grow at the CAGR of 4.9% during the forecast period.

Middle East & Africa Space-Based Defense Platforms Market

Middle East & Africa market stood at USD 2.53 billion in 2025 and is expected to reach USD 4.58 billion in 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players Strengthen Space-Based Defense Through Resilient, Multi-Orbit Architectures

The leading competitors in the market include large-scale defense and aerospace firms including Northrop Grumman Corporation, Lockheed Martin Corporation, RTX Corporation, Boeing, L3Harris Technologies, Airbus Defence and Space, Thales Alenia Space, Leonardo, BAE Systems, Israel Aerospace Industries, and SpaceX. Their competitive edge lies in secure SATCOM services, ISR payloads, missile-warning capabilities, SSA, and resilient terrestrial networks.

The nature of competition in the global market is evolving from large-scale dedicated satellites to proliferated LEO constellations, hosted payloads, dual-use satellite systems, and AI-enabled satellites. For instance, the U.S. Space Development Agency contracted with Northrop Grumman and York Space Systems in October 2023 for USD 1.3 billion for 100 Tranche 2 Transport Layer Alpha satellites.

LIST OF KEY SPACE-BASED DEFENSE PLATFORMS COMPANIES PROFILED IN REPORT

- Space Exploration Technologies Corp. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (U.S.)

- The Boeing Company (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- BAE Systems plc (U.K.)

- Airbus SE (Netherlands)

- Thales Alenia Space SAS (France)

- Leonardo S.p.A. (Italy)

- Israel Aerospace Industries Ltd. (Israel)

- Elbit Systems Ltd. (Israel)

- OHB SE (Germany)

- Sierra Space Corporation (U.S.)

- York Space Systems LLC (U.S.)

- Viasat, Inc. (U.S.)

- Eutelsat Group (France)

- SES S.A. (Luxembourg)

- Telespazio S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- December 2024: The European Union signed the concession contract for IRIS, a secure multi-orbit satellite constellation planned with 290 satellites. The program is valued at USD 11.10 billion, and is led by the SpaceRISE consortium, including SES, Eutelsat, Hispasat, Airbus Defence and Space, Thales Alenia Space, OHB, Telespazio, Deutsche Telekom, Orange, Hisdesat, and Thales SIX.

- October 2024: Northrop Grumman received an award to build and launch two Next-Generation Overhead Persistent Infrared Polar spacecraft, bringing the cumulative program value to about USD 4.20 billion for the company.

- June 2024: Lockheed Martin secured a USD 977.50 million contract extension for Next-Generation Overhead Persistent Infrared missile-warning satellites.

- March 2024: The U.S. Space Force awarded Boeing a USD 439.60 million production contract for the WGS-12 Wideband Global SATCOM satellite. The satellite is intended to expand protected wideband military communications capacity for the U.S. and allied users.

- January 2024: The U.S. Space Development Agency awarded contracts worth up to USD 2.50 billion to L3Harris Technologies, Lockheed Martin, and Sierra Space for 54 Tranche 2 Tracking Layer satellites. Each company is expected to provide 18 satellites carrying infrared sensors for missile warning, missile tracking, and preliminary fire-control capability.

- January 2024: Rocket Lab became a prime contractor for a U.S. Space Force / Space Development Agency military satellite project valued at about USD 515 million. The contract covers 18 Tranche 2 Transport Layer Beta satellites, expanding Rocket Lab’s role from launch and components into full defense satellite prime-contracting.

- October 2023: The U.S. Space Development Agency awarded about USD 1.30 billion to Northrop Grumman and York Space Systems for 100 Tranche 2 Transport Layer Alpha satellites. Northrop Grumman received about USD 732 million for 38 satellites, while York received about USD 617 million for 62 satellites, supporting beyond-line-of-sight targeting, missile warning, missile tracking, and global military communications.

- August 2023: The U.S. Space Development Agency awarded around USD 1.50 billion to Lockheed Martin and Northrop Grumman for 72 Tranche 2 Transport Layer Beta satellites, with each company to build 36 satellites.

REPORT COVERAGE

The global space-based defense platforms market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry expert’s developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform Type

|

|

By Orbit

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value is anticipated to reach USD 45.83 billion in 2026 and will increase to USD 92.44 billion by 2034.

In 2025, the North Americas market value stood at USD 21.51 billion.

The market is expected to exhibit a CAGR of 9.2% during the forecast period.

Dedicated military satellites segment led the market by platform type.

Rising geopolitical tensions drive demand for space-based missile warning and resilient defense networks.

Top players in the market include Space Exploration Technologies Corp., Northrop Grumman Corporation, Lockheed Martin Corporation, RTX Corporation, The Boeing Company, L3Harris Technologies, Inc., Airbus SE, Thales Alenia Space SAS, Leonardo S.p.A., and Israel Aerospace Industries Ltd.

North America held the largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us