Space Based Fuel Management System Market Size, Share & Industry Analysis, By Type (Satellite, Reusable Launch Vehicle, and Launch Vehicle), By Component (Engine, Tank, Pumps, Flow Control Components, Heat Exchanger, Engine Control Unit, and Others), By Fuel Type (Solid and Liquid), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

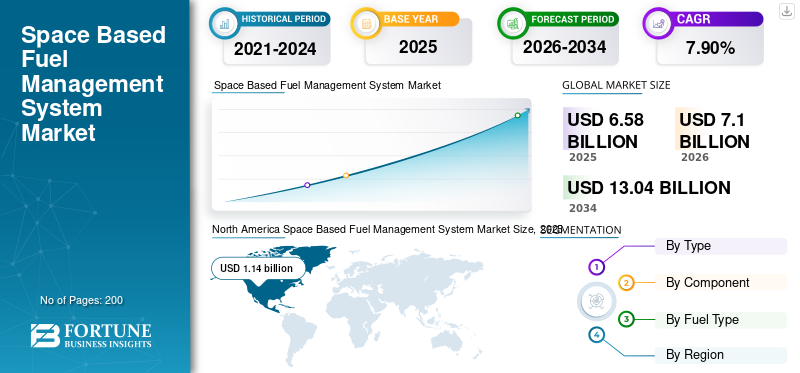

The global space based fuel management system market size was estimated at USD 6.58 billion in 2025 and is projected to reach USD 7.10 billion in 2026 to USD 13.04 billion by 2034, growing at a CAGR of 7.90% from 2026 to 2034. North America dominated the space based fuel management system market with a market share of 17.38% in 2025.

A fuel management system comprises controlling and monitoring fuel consumption in a spacecraft for propulsion. Furthermore, it gives access to insights using metric and fuel data. The implementation of a fuel management system improves fuel efficiency and reduces fuel-related cost.

Many space agencies and private companies around the world are currently focused on developing satellite constellations in Low Earth Orbit (LEO). This will drive the global market of space based fuel management system. Moreover, the evolution of satellites and launch vehicle platforms and increasing research and development activities to develop cost-effective propulsion technologies and fuel management systems are other factors contributing to the growth of the LEO-centric space based fuel management system. For example, in June 2022, Thrust Me signed a contract with the European Space Agency (ESA) to provide the GOMX-5 mission under ESA's General Support Technology (GSTP) program with an NPT30-I2-1.5U electric propulsion system. The rising demand for the satellite launch segment is expected to boost the global market size from 2023 to 2030.

Download Free sample to learn more about this report.

Space Based Fuel Management System Market KEY TAKEAWAYS

- 2025 Market Size: USD 6.58 billion

- 2026 Market Size: USD 7.10 billion

- 2034 Forecast Market Size: USD 13.04 billion

- CAGR: 7.90% from 2026–2034

- North America dominated the market with a 17.38% share in 2025.

- Launch vehicle segment accounted for the largest market share in 2026.

- Engine segment accounted for the largest market share in 2026.

Asia Pacific

Emerging market, driven by increasing space launches for communication, navigation, and surveillance applications.

North America

USD 1.14 billion in 2025, supported by rising government funding for space exploration programs.

Europe

Growth is driven by increasing satellite launches and higher investments by the European Space Agency.

U.S.

Demand is supported by rising government budgets for space exploration and launch programs.

Japan

The market is projected to reach USD 86.3 million by 2025, driven by expanding space exploration activities.

Read More

Space Based Fuel Management System Market Trends

Download Free sample to learn more about this report.

Increased Focus on Solid Nitrogen Space Based Fuel Management System for Improved Efficiency

Solid nitrogen is a series of solid forms of the element nitrogen, which was first observed in 1884. Although solid nitrogen is mainly a subject of academic research, low-temperature and low-pressure solid nitrogen is an essential component of celestial bodies in the outer solar system, while high-temperature & high-pressure solid nitrogen is a powerful explosive with higher chemical energy. It is denser than other non-nuclear materials.

- North America witnessed space based fuel management system market growth from USD 0.84 Billion in 2021 to USD 0.91 Billion in 2022.

Moreover, solid nitrogen rocket fuel makes the spacecraft compact and lighter and increasing need for customization is projected to give in development of the fuel system. The key players are focused on making a new form of nitrogen called N5+N5. Nitrogen has long been associated with rocket propellants and explosives such as nitroglycerin and TNT (trinitrotoluene). This is attributed to the fact that nitrogen gas (N2) is very stable. Compounds with two or more nitrogen atoms per molecule readily decompose to N2, releasing a lot of energy in the process. Owing to such advantages, there is an increase in adoption of solid nitrogen in space based fuel management system. In July 2019, NASA signed eight contracts with various U.S. companies for the supply of nitrogen and oxygen to NASA centers for a variety of activities.

Space Based Fuel Management System Market Growth Factors

Rising Commercial Space Flights to Accelerate the Demand for Space Based Fuel Management System

Space tourism is human space travel for recreational purposes. The space tourism industry has developed significantly in the U.S. and Europe due to accessibility to launch facilities, commercial space launches, technological breakthroughs, and space travel. The market is consolidated and dominated by a few players with large shares. These players plan to utilize research & development to build orbital and suborbital launch vehicles to travel into space in the next few years. These companies have invested huge amounts of money as the industry is expected to grow exponentially. Furthermore, there is increasing demand for fuel management systems due to the serial production of satellites and launch vehicles platforms.

In August 2022, Blue Origin launched six passengers on a supersonic flight to the edge of space. The flight was completed in a few minutes, 66 miles above west Texas. Moreover, SpaceX launched four astronauts to the international space station on 26 February 2023. The mission was named as Crew-6 and the launch took place using Falcon-9 at NASA’s Kennedy Space Center in Florida. Such developments in the customization of satellites lead to market growth.

Increasing Satellite Constellations to Drive the Market Growth for Space Based Fuel Management System

Satellites missions with similar properties and functions for a common purpose are increasing across the globe. For example, in May 2019, SpaceX launched the first 60 satellites under Starlink constellation. Moreover, currently, the number of constellations has increased to more than 3,000 and accounts for half of all active satellites in space.

According to the U.S. government accountability office, nearly 5,500 active satellites were in orbit by spring 2022, and another 58,000 are projected to launch by 2030. Other satellite constellation-based projects, such as Oneweb and Kuiper, aim to launch more than 5,000 satellites in the coming years. Such projects are anticipated to drive the space based fuel management system market growth. Moreover, a large constellation of satellites in low earth orbit is the main cause of rising demand for satellite based fuel management system.

RESTRAINING FACTORS

Integrated Powertrain Solution that Limits the Choice of Fuel Management System Components to Hamper the Market Growth

The Integrated Main Propulsion System (MPS) Performance Rebuild Process provides project integration management and MPS post-flight data files required for post-flight reporting to validate flight performance. This process/model was used as the basis for the currently operational Space Launch System (SLS) work.

Furthermore, this process uses methods, including multiple software programs to model the performance of the integrated propulsion system during ascent of the launch vehicle. It is used to evaluate the performance of integrated propulsion systems such as fuel tanks, delivery systems, rocket engines, and pressurization systems during ascent based on in-flight pressure and temperature data. Moreover, the IMP system has various disadvantages such as high installation cost, low service life, high operation, and maintenance cost. Such factors are not feasible and can hamper the market growth.

Space Based Fuel Management System Market Segmentation Analysis

By Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Launch Vehicle Segment is Anticipated to Dominate the Market Owing to Increase in Number of Launches

The Reusable Launch Vehicle segment dominated the market accounting for 1.36% market share in 2026. Based on type, the market is segmented into satellite, reusable launch vehicle, and launch vehicle. The launch vehicle segment dominates the market due to the growing number of launches planned during the forecast period. A launch vehicle is a typical rocket-powered vehicle designed to launch payloads from the Earth to space. Most rockets operate from a launch pad supported by a rocket control center and systems such as rocket assembly and refueling. Furthermore, in September 2022, ISRO signed a contract with HAL and L&T for the development of five Polar Satellite Launch Vehicles (PSLV).

The reusable launch vehicle segment is to witness moderate growth during the forecast period. The growth in the segment is owing to the increase in focus for the development of 3D-printed rocket engines and launch vehicles.

- The reusable launch vehicle segment is expected to hold a 1.36% share in 2022.

By Component Analysis

Engine Segment is Anticipated to Command the Market Owing to Critical Performance in Space Vehicle

By component, the market is segmented into engine, tank, pumps, flow control components, heat exchanger, engine control unit, and others. The engine segment dominated the market in 2022. The main engine used in space provides more power and thrust required for orbital motion, planetary orbit, and off-planet landing and scaling. The Reaction Control and Orbit Maneuvering System powers the spacecraft's track keeping, position, and attitude control system. Owing to the complexity of operation, the segment is projected to dominate the market during the study period.

Heat exchanger segment will witness significant growth during the study period. Moreover, a heat exchanger uses turbine exhaust gas to heat and expand liquid oxygen and gaseous nitrogen to pressurize the oxidizer and fuel tanks. This helps to improve the efficiency of the engine along with cooling down of the system. Owing to this, the heat exchanger segment is projected to witness growth in the years. The engine segment is expected to hold a 22% share in 2025.

The others segment has a gas generator, piping, and allied components required for spacecraft propulsion systems. Gas generator is one of the most crucial components in any bipropellant liquid rocket engine. Owing to the importance of the component, the segment is projected to grow during the forecast period.

By Fuel Type Analysis

Owing to Wider Applications in Satellite and Launch Vehicles the Liquid Segment is Dominating the Market

The market is divided into solid and liquid, by fuel type. The liquid segment is projected to dominate the market during the forecast period, owing to the high usage in satellites, launch vehicles, and other systems. Liquids are desirable as they are fairly dense and have a high specific impulse (ISP). As a result, the volume of the fuel tank can be relatively small. A lightweight centrifugal turbo pump is used to pump rocket fuel from the tank into the combustion chamber. This keeps the fuel under the required pressure. Owing to such advantages over solid propellant rockets, the segment is projected to dominate the market.

The solid segment is anticipated to witness moderate growth during the study period. Solid-fuel rockets are much easier to store and handle than liquid-fuel rockets. The high propellant density also ensures a compact size. These features, along with their simplicity and low cost, make solid-fuel rockets ideal for military and space applications. The solid segment is projected to generate USD 1.76 billion in revenue by 2025.

REGIONAL Analysis

North America Space Based Fuel Management System Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America dominated the market with a valuation of USD 1.14 billion in 2025 and is projected to reach USD 1.23 billion in 2026. The growth in this region is owing to the rise in the allotment of budgets for space exploration programs by the government in collaboration with space agencies. For the fiscal year of 2022, the U.S. government allotted a budget of USD 7.6 billion for space exploration programs in the region.

Europe

The Europe space based fuel management system market held the highest market share in the base year. The high growth of the market is attributed to this region due to increase in satellite launches during the study period. Moreover, the European Space Agency (ESA), approved a budget of USD 18.11 billion in the ministerial-level council meeting in 2022, which is 17% more than that of 2019. Europe is anticipated to grow at a CAGR of 7.1% during the forecast period.

Asia Pacific

The market in Asia Pacific is one of the emerging markets of space based fuel management system. This growth is attributed to the rise in demand for space launches for telecommunication, communication satellite, surveillance, and navigation applications. Key emerging economies, such as India, China, Japan, and others, hold major contributions in the growth of space based fuel management system.

- The space based fuel management system market in Japan is expected to reach USD 86.3 million by 2025.

- China is projected to witness a strong CAGR of 9.2% during the forecast period.

The rest of the world region is anticipated to witness moderate growth in this market during the forecast period. The increase in space program investments in the Middle East region is anticipated to boost the demand in the region. Furthermore, the UAE has launched a National Space Program, which accomplished Mars orbiter mission in February 2021.

KEY INDUSTRY PLAYERS

Introduction of Efficient Technologies for Developing Advanced Propulsion Systems is the Key Focus of Market Players

The global market is highly fragmented with the presence of various key players such as Airbus, Accion System, Benchmark Space System, Cobham, Exotrail, IHI Aerospace Co. Ltd, Lockheed Martin Corporation, and others. The increased demand for next-generation propulsion systems for space launch activities drives the dominance of key players in the market. Furthermore, rise in investments from government agencies gives a boost to the players for development of advanced propulsion systems with less carbon emission to maintain sustainability. Such factors give rise to competitiveness amongst players to develop efficient propulsion systems.

List of Top Space Based Fuel Management System Companies:

- Airbus (Netherlands)

- Accion System (U.S.)

- Benchmark Space System (U.S.)

- Cobham (U.S.)

- Exotrail (U.S.)

- IHI Aerospace Co. Ltd (Tokyo)

- Lockheed Martin Corporation (U.S.)

- Microcosm Inc. (U.S.)

- Moog Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- February 2023– Blue Origin signed its first contract with NASA to launch a mission to study the magnetic field around Mars. The company recently developed the New Glenn heavy lift rocket, scheduled for launch in late 2024, on NASA's ESCAPADE mission with two spacecraft from Space Force Station Cape Canaveral, Florida.

- November 2022- NASA issued a change order to SpaceX to further develop the Starship manned landing system to meet the requirements of long-term manned lunar exploration under Artemis. With this addition, SpaceX will deploy its second manned landing demonstration mission in 2027 as part of NASA's Artemis IV mission.

- April 2022– OneWeb signed a deal to deploy at least some of the remaining LEO broadband satellites using India's largest rocket, according to a company executive. Furthermore, the company reached an agreement with New Space India Limited, the commercial arm of Indian space agency ISRO, covering the launch of an undisclosed number of satellites from the Satish Dhawan Space Centre.

- July 2021– SpaceX won a USD 178 million launch services contract for NASA's first mission. The mission will focus on Jupiter's icy moon Europa and weather viable conditions existing on the surface.

- August 2020- The U.S. Air Force awarded a contract to rocket builders United Launch Alliance and SpaceX to launch national security missions. The award represents the second phase of the military's National Security Space Launch Program, hosted by the Air Force's Space Missile Systems Center in Los Angeles, California.

REPORT COVERAGE

The research report provides a detailed analysis of the market. It comprises all major aspects such as R&D capabilities and optimization of the manufacturing process. Moreover, the report offers insights into the space based fuel management system market trends and primarily highlights key industry developments. In addition to the above-mentioned factors, it mainly focuses on several factors that have contributed to the global market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.90% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Component, Fuel Type, and Geography |

|

By Type

|

|

|

By Component

|

|

|

|

By Fuel Type

|

|

By Geography

|

|

Frequently Asked Questions

According to Fortune Business Insights, the global space based fuel management system market was valued at USD 6.58 billion in 2025 and is projected to reach USD 13.04 billion by 2034, growing at a CAGR of 7.90% from 2026 to 2034. This growth is fueled by rising satellite constellations, increased space missions, and innovations in propulsion technologies.

The market is likely to grow at a CAGR of 7.90% over the forecast period (2026-2034).

A space based fuel management system is a technological framework designed to monitor, control, and optimize fuel consumption in spacecraft, satellites, and launch vehicles. It enhances propulsion efficiency, reduces mission costs, and provides vital metrics for space navigation and performance analysis.

North America led the market with a 17.38% share in 2025, driven by government funding, strong space infrastructure, and major players like SpaceX, Lockheed Martin, and NASA. The U.S. alone allocated USD 7.6 billion for space exploration in 2022.

The launch vehicle segment is leading the market due to the increasing number of global satellite and crewed space launches. This includes traditional rockets and reusable launch vehicles, which are gaining traction due to cost efficiency.

The market is segmented into solid and liquid fuels. Liquid fuel dominates due to its high specific impulse, density, and widespread usage in satellites and launch vehicles, making it more suitable for long-duration missions.

Commercial space flights, driven by companies like Blue Origin and SpaceX, are boosting demand for advanced fuel management systems. The growth in space tourism requires reliable propulsion systems, which in turn, accelerates demand for efficient fuel management technologies.

Solid nitrogen is emerging as a promising propellant due to its high chemical energy and compact storage benefits. Research into advanced nitrogen compounds like N5+N5 is expected to revolutionize next-gen propulsion systems.

Key players include Airbus, Accion Systems, Benchmark Space Systems, Cobham, Exotrail, IHI Aerospace, Lockheed Martin, and Northrop Grumman. These companies are focusing on next-gen propulsion systems and sustainability-driven innovations.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us