Space-enabled Digital Transformation Market Size, Share & Industry Analysis, By Offering (Software and Services), By Orbit Type (LEO, MEO, GEO, and Multi Orbit/Hybrid), By End User (Government, Defense and Intelligence, Commercial Enterprises, and Research and Academia), and Regional Forecast, 2026-2034

SPACE-ENABLED DIGITAL TRANSFORMATION MARKET SIZE AND FUTURE OUTLOOK

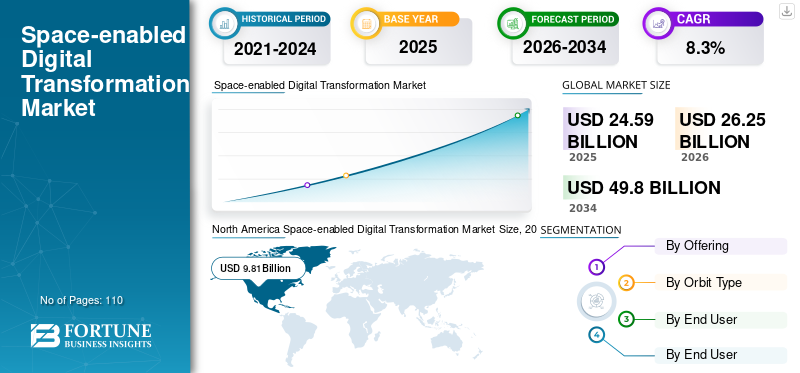

The global space-enabled digital transformation market size was valued at USD 24.59 billion in 2025. The market is projected to grow from USD 26.25 billion in 2026 to USD 49.80 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period. North America dominated the space-enabled digital transformation market with a market share of 39.89% in 2025.

Digital transformation on behalf of space refers to how space-enabled tools, such as satellite connectivity, earth observation data, positional & timed signals, are used to enhance, digitize, automate, and optimize operations of both enterprise and government sectors, including the way they connect with each other, monitor their assets, mitigate risk, and operate remotely. There is an extraordinary rise in the need for both real time data and analytics. Whether it is a company or government, both now require continuous and current visual availability of their assets, infrastructures, and environmental conditions so that they can make faster decisions, conduct predictive operations, and manage their risk proactively across large geographic areas and/or remotely from their current location. This factor plays an important role in fueling market growth.

Many key industry players, such as SpaceX (Starlink), Eutelsat Communications SA, SES S.A., Viasat, and Hughes Network Systems (EcoStar), operating in the market, are focusing on the expansion of satellite constellations, especially in LEO, to provide high-speed, low-latency connectivity and data services that enable global enterprise and government digitalization, especially in remote and underserved regions.

Download Free sample to learn more about this report.

SPACE-ENABLED DIGITAL TRANSFORMATION MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 24.59 billion

- 2026 Market Size: USD 26.25 billion

- 2034 Forecast Market Size: USD 49.80 billion

- CAGR: 8.3% from 2026–2034

- North America dominated the market with a 39.89% share in 2025.

- GEO satellites dominated the market in 2025.

- Commercial enterprises held the largest market share in 2025.

North America

North America reached USD 9.81 billion in 2025.

Europe

Europe is projected to reach USD 6.59 billion in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 5.87 billion in 2026.

U.S.

The market is estimated to reach USD 8.49 billion in 2026.

Japan

The market is projected to reach USD 1.11 billion in 2026.

Read More

IMPACT OF GENERATIVE AI

Increasing Satellite Data Volume Accelerating Adoption of Generative AI in Space Applications

The market is being greatly impacted by the development of generative AI. The improved analytical capabilities of data, along with the ability to process large amounts of satellite images and sensor outputs, have allowed for faster and better quality decisions to be made. Generative AI algorithms are helping improve the efficiency with which earth observation data can be processed, allowing organizations across all industry sectors to extract valuable insights to assist in making decisions on predictive maintenance, risk assessment, and urban planning.

- For instance, in February 2026, SpaceX filed with the U.S. FCC to launch up to one million satellites designed as orbital data centers to meet rising global demand for artificial intelligence computing and data handling in space.

The Generative AI technology is also being used to increase the efficiency of satellite networks, support autonomous operations of satellites, and provide customized satellite solutions to industries such as agriculture, shipping, and telecommunications. The combination of AI and satellite data has resulted in the ability to enable real-time automated decision-making, thus contributing to the continued growth of the AI-based platforms and services within the space sector.

SPACE-ENABLED DIGITAL TRANSFORMATION MARKET TRENDS

Growing Focus on Seamless Satellite Connectivity to Boost Market Development

The combination of 5G and satellite connections allows people to use fast internet in both cities and rural areas. As satellites can work together with 5G, areas that traditionally do not have access to reliable internet can now be reached through satellite combined with 5G. Low-latency (less delay between action and result) satellite technology, plus the speed of 5G, together will provide a better connection for Internet of Things (IoT), self-driving vehicles, smart cities, and industries to move towards a digitized operation. Global coverage also helps provide mobile communication, greater access to real-time data, and create more reliable connections in health care, transportation, and emergency service sectors. For instance,

- In February 2026, SES and Huawei announced a partnership to combine satellite and 5G networks to provide worldwide coverage of both IoT and mobile services. This collaboration highlights the growing importance of satellite and 5G convergence in addressing global connectivity challenges.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Government Investments in Space Infrastructure to Fuel Industry Development

Government investments and space policies are crucial drivers of the market, as governments worldwide continue to allocate significant resources to space infrastructure. Countries around the world continue to spend extensively on building out their spatial infrastructure for things such as national security, satellite communications, environmental monitoring, and climate change.

Additionally, a number of countries have been putting policies into effect to encourage activities such as exploration of space, developing satellite technologies, and building out digital infrastructure, all of which have created demand for satellite-based services from both public and private sectors. These same actions have enabled more efficient management of natural resources, enhanced connectivity for users in remote areas, and increased growth in space-based analysis of data for government decision-making. Furthermore, the government's investment in programs that focus on space helps encourage private sector innovation and cooperation, which also contributes to the growth of the overall market. For instance,

- In January 2026, the European Space Agency (ESA) announced a USD 17.25 billion investment in space programs for 2026-2030, focusing on satellite infrastructure, climate change monitoring, and AI-powered space data analytics.

Together, these factors strengthen the business case for space-enabled digital transformation systems by managing real time traffic demand and optimizing highway traffic flow via data-driven operations, rather than relying only on new lane construction.

MARKET RESTRAINTS

High Cost of Satellite Deployment and Maintenance May Hinder Market Growth

Costs to deploy and maintain satellite systems are considered high and have restricted entry into the Space-supported digital transformation market, largely as launching and maintaining satellite systems require significant investments of capital. Satellite manufacturers, launch service providers, and satellite operators incur high costs for developing, testing, and maintaining satellite systems, along with the costs related to acquiring orbital slots and frequency spectrum. These various sources of financial burden will limit the ability of smaller companies to enter the market and will prevent the scalability of satellite constellations in sectors that are constrained by very tight budgets.

In addition to new technology developments such as miniaturized satellites and reusable launch vehicles, the relatively large investment to develop the satellite systems continues to pose a challenge to widespread adoption of the product, particularly in emerging markets.

MARKET OPPORTUNITIES

Integration of Smart Cities into IoT Technologies Boosts Market Demand

The incorporation of smart cities into IoT (Internet of Things) technologies provides a massive opportunity through the space-enabled digital transformation market via the use of satellite-based connectivity to improve urban infrastructure and services. Satellites provide reliable connectivity in areas with limited terrestrial network infrastructure, enabling real-time monitoring of traffic, energy usage, environmental conditions, and public safety.

As smart cities continue to grow and expand, the need for a satellite-based network of IoT devices to facilitate large amounts of data processing and management will be needed to support the growth of smart cities, which will lead to the need for satellite-based IoT networks to improve urban planning, resource management, and automation. This integration facilitates innovations such as smart grids, intelligent transportation systems, and efficient waste management, all crucial for building sustainable, tech-driven cities.

- For instance, in December 2025, industry analysts reported that the global number of connected IoT devices in smart cities is expected to exceed 3.5 billion by 2028. This underscores the need for ubiquitous connectivity solutions provided by satellite networks.

Segmentation Analysis

By Offering

Services Segment to Dominate due to Connectivity-Driven Solutions

Based on offering, the market is divided into software and services.

Services are anticipated to account for the largest market share. This is owing to satellite service providers utilizing satellites to deliver connectivity and data transmission services while managing end-to-end operations for corporations and government agencies. Businesses across industries rely on satellite services such as satellite broadband, satellite data for earth observation, and satellite IoT connectivity to help facilitate digital transformation initiatives in sectors, including agriculture, logistics, and telecommunications, particularly in remote and underserved regions.

Software is anticipated to grow at the highest CAGR of 10.5% over the forecast period. This is owing to the increasing demand for AI-powered data analytics platforms, real-time insights, and scalable solutions that enhance decision-making and operational efficiency across industries, leveraging satellite data.

By Orbit Type

GEO Segment Led the Market as they Cover Larger Geographic’s Areas

Based on orbit type, the market is categorized into LEO, MEO, GEO, and multi orbit/hybrid.

GEO dominated the market in 2025, as they cover a larger area with fewer units than other orbit types. This makes GEO satellites the best choice for broadband connectivity, broadcasting, and large-scale communication services. As a result, GEO satellites have the highest levels of service as they provide stable, continuous coverage, which is critical to support applications including television broadcasting, weather forecasting, and emergency communication.

LEO is projected to grow at the highest CAGR of 11.7% over the forecast period. This is due to its low latency, high-speed data transmission capabilities, and the increasing deployment of LEO satellite constellations for global connectivity, particularly in underserved regions.

By End User

To know how our report can help streamline your business, Speak to Analyst

Commercial Enterprise Segment Led the Market due to Improve Business Operations

Based on end user, the market is classified into government, defense and intelligence, commercial enterprises, and research and academia.

Commercial enterprises held the dominant market share in 2025 and are expected to grow at the highest CAGR of 10.1% during the forecast period. This is due to rising demand for satellite-based connections to improve business operations, remote inspections, and real-time data analysis. For example, industries such as agriculture, logistics, and telecommunications are using space-based technologies to increase their supply chain efficiency, enhance their decision-making process, and extend their global market, all resulting in continued growth of commercial enterprise use.

The defense and intelligence segment is anticipated to grow at a moderate CAGR of 9.1% during the forecast period. As governments continue to invest in satellite-based communication, surveillance, and reconnaissance systems, while balancing technological advancements with budget constraints and national security priorities.

Space-enabled Digital Transformation Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Space-enabled Digital Transformation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest space-enabled digital transformation market share in 2024, valued at USD 9.33 billion, and maintained its leading share in 2025, reaching USD 9.81 billion. The market in the region is expected to increase, owing to the presence of a well-established satellite infrastructure, an advanced technological ecosystem supporting modern enterprises, and strong demand for satellite-based services from both governments and private sector organizations. In addition to hosting some of the world’s largest satellite enterprises, the region has received considerable investment in satellite communications, earth observation applications, and defense applications. Strong cooperative efforts between private sector companies and various government entities, such as NASA and the department of defense, further supports market development.

- For instance, the U.S. space‑related industries supported 347,000 private‑sector jobs and contributed about USD 131.8 billion to GDP in 2022, highlighting robust commercial activity and economic importance.

These factors play a significant role in fueling the space-enabled digital transformation market growth.

U.S Space-enabled Digital Transformation Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 8.49 billion in 2026, accounting for roughly 32.3% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is projected to record a growth rate of 7.6% in the coming years, the second-highest among all regions, reaching a valuation of USD 6.59 billion by 2026. Growth in the region is largely driven by increasing government spending in space-related technologies, which is boosting digital transformation initiatives supported by space technologies. Programs led by the European Space Agency (ESA) and Horizon Europe programs fund satellite communication technologies, earth-observing satellites, and space exploration efforts in Europe. Moreover, a growing number of industries and governmental agencies in Europe see space technology as essential to improving environmental monitoring capabilities, smart cities development projects, and digital connectivity, which will create new opportunities for Europe to benefit from the growing number of private businesses that are also entering the rapidly expanding market for commercialized space services.

U.K Space-enabled Digital Transformation Market

The U.K. market in 2026 is estimated at around USD 1.30 billion, representing roughly 5.0% of global revenues.

Germany Space-enabled Digital Transformation Market

Germany’s market is projected to reach approximately USD 1.23 billion in 2026, equivalent to around 4.7% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 5.87 billion in 2026 and secure the position of the third-largest region in the market. This is owing to rapid urbanization, increasing investments in satellite connectivity, and the rising adoption of space-based services in emerging economies such as India, China, and Southeast Asia. Furthermore, IoT, smart city initiatives, and government space initiatives continue to drive significant growth in demand for satellite data and communications and real-time monitoring solutions across multiple industries. For instance,

- According to industry experts, India’s space sector, valued at roughly USD 8.4 billion as of 2024, is projected to expand to USD 44 billion within the next decade, highlighting strong commercial demand for satellite communications and space‑enabled services.

India and China are both estimated to reach USD 0.80 billion and USD 1.37 billion, respectively, in 2026.

Japan Space-enabled Digital Transformation Market

The Japanese market in 2026 is estimated at around USD 1.11 billion, accounting for roughly 4.2% of global revenues. This is owing to the country's advanced technological infrastructure, strong government support for space initiatives, and increasing demand for satellite communications, Earth observation data, and IoT services across industries such as agriculture, logistics, and disaster management.

China Space-enabled Digital Transformation Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.37 billion, representing roughly 5.2% of global sales.

India Space-enabled Digital Transformation Market

The India market in 2026 is estimated at around USD 0.80 billion, accounting for roughly 3.0% of global revenues.

South America

South America is expected to witness moderate growth in this market during the forecast period. The South American market is set to reach a valuation of USD 1.50 billion in 2026. This is owing to increasing government investments in satellite infrastructure, the rising demand for connectivity in remote areas, and the growing adoption of space-based solutions for agriculture, environmental monitoring, and telecommunications.

Middle East and Africa

The Middle East and Africa are estimated to reach USD 1.92 billion in 2026 and are expected to grow at a significant rate in the coming years. This is owing to rapid advancements in satellite communication infrastructure, especially within the Gulf Cooperation Council (GCC) countries, including Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE). These GCC nations are investing heavily in space technology as part of their overall strategy to develop smart cities and the Internet of Things (IoT). Growth in the MEA region’s market for space-enabled digital transformation solutions will also be fueled by an increase in demand for satellite data solutions for resource management, environmental monitoring, and national security. In the Middle East & Africa, the GCC is set to reach a value of USD 0.58 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding Their Product Portfolio to Support Global Broadband Services

The global space-enabled digital transformation market holds a semi-consolidated market structure, constituting prominent players such as SpaceX (Starlink), Eutelsat Communications SA, SES S.A., Viasat, and Hughes Network Systems (EcoStar) holding significant positions. The strong market presence of these companies is supported by continuous strategic initiatives, including the integration of space-based IoT solutions, expansion of satellite connectivity services, advanced data analytics platforms, and partnerships with telecom operators, cloud providers, and infrastructure developers.

- For instance, in September 2024, SpaceX announced the expansion of its Starlink satellite network to support global broadband services, particularly in underserved and remote regions, enhancing satellite internet availability for industries such as agriculture, logistics, and telecommunications.

Other notable players in the global market include Iridium, Planet Labs, ICEYE, Maxar (Maxar Intelligence), and BlackSky. These companies are expected to emphasize new product launches, space-based data services, and long-term operations and maintenance service models to strengthen their market positioning and expand their global footprint during the forecast period.

LIST OF KEY SPACE-ENABLED DIGITAL TRANSFORMATION COMPANIES PROFILED

- SpaceX (Starlink) (U.S.)

- Eutelsat Communications SA (France)

- SES S.A. (Luxembourg)

- Viasat (U.S.)

- Hughes Network Systems (EcoStar) (U.S.)

- Iridium (U.S.)

- Planet Labs (U.S.)

- Maxar (Maxar Intelligence) (U.S.)

- ICEYE (Finland)

- BlackSky(U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: ICEYE, along with its joint venture Rheinmetall ICEYE Space Solutions, signed a USD 1.90 billion contract with Germany for radar satellite data services, marking its largest deal to date and supporting SAR‑based monitoring and analytics for defense and civil use.

- November 2025: Iridium announced a partnership with Vodafone IoT to provide NTN NB‑IoT satellite connectivity that expands global IoT coverage for connected devices, supporting enterprise digitalization and remote monitoring applications.

- November 2025: Eutelsat announced a USD 700 million rights issue as part of a ~USD 1.7 billion capital raise to reinforce its financial structure and fund strategic growth, including future LEO satellite infrastructure. This funding initiative strengthens Eutelsat’s ability to invest in next‑generation connectivity services and compete in the evolving space data and communication market.

- October 2025: BlackSky secured a multi‑year contract worth over USD 30 million to integrate its Gen‑3 tactical ISR (Intelligence, Surveillance, Reconnaissance) services into secure operational environments, supporting real‑time decision‑making for government and enterprise customers.

- September 2025: SpaceX acquired approximately USD 17 billion worth of spectrum licenses from EchoStar to enhance its Starlink satellite internet network and expand direct‑to‑cell connectivity services. This strategic move aims to deliver broadband‑speed internet directly to mobile devices in remote and underserved areas, supporting global connectivity expansion.

- July 2025: SES completed its acquisition of Intelsat to create a global multi‑orbit satellite operator with an expanded fleet of approximately 120 satellites to deliver integrated connectivity solutions worldwide. This acquisition enhances SES’s ability to serve business and government customers with broad‑coverage satellite communication and digital transformation services.

- April 2025: Hughes unveiled its HL1100W electronically steerable antenna (ESA) for LEO connectivity, approved for use on the Eutelsat OneWeb network to boost global high‑speed satellite connectivity for business and government applications. This product launch reflects Hughes’s push into compact, high‑performance connectivity solutions that support space‑enabled digital transformation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.3% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Orbit Type, End User, and Region |

| By Offering |

|

| By Orbit Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 24.59 billion in 2025 and is projected to reach USD 49.80 billion by 2034.

In 2025, North Americas market value stood at USD 9.81 billion.

The market is expected to exhibit a CAGR of 8.3% during the forecast period (2026-2034).

By end user, the commercial enterprises segment is expected to lead the market.

Government investments in space infrastructure are a key factor driving the factor.

SpaceX (Starlink), Eutelsat Communications SA, SES S.A., Viasat, and Hughes Network Systems (EcoStar) are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us